Honey I Shrunk the Apartments: Average New Unit Size Declines 7% Since 2009

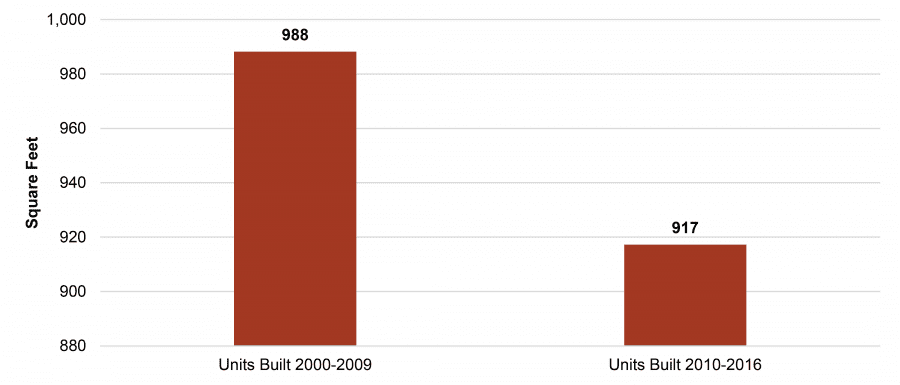

Average New Apartment Size Drops by 70 Square Feet

From micro-units to co-living, the biggest—or at least, most talked about—trends in rental apartments today are all about living smaller, trading personal space for community amenities or hip urban locations. But how much has the needle actually moved toward smaller units?

Analyzing the top 20 U.S. metro areas reveals that meaningful change is in fact afoot. The size of the average new apartment unit built from 2010 to the present is down 70 square feet—7%—compared with those built during the 2000-2009 period.

Change in Average New Apartment Unit Size

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

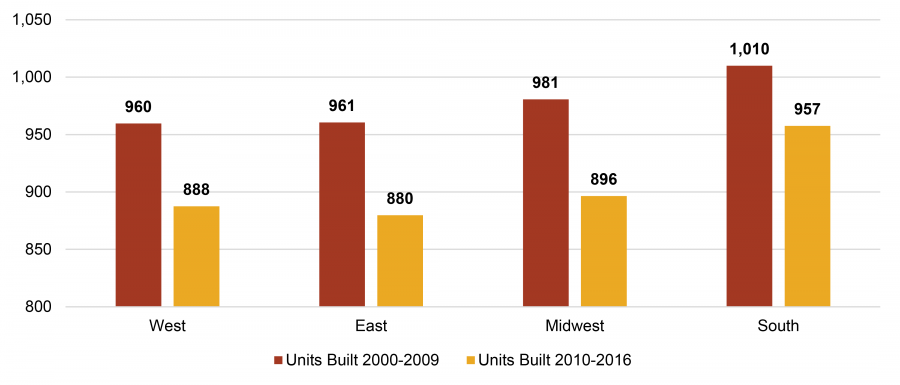

Unit Size Down Across Geographic Regions

The decline in unit size is not isolated to the coasts; rather, unit size is declining across the country. In fact, aggregating the markets surveyed by region, the Midwest has experienced the largest percentage decrease. Furthermore, of the 20 markets analyzed, only two saw average new unit size increase this period—San Diego and Riverside, California. The rest saw average unit size diminish by as much as 25%.[1]

Average New Apartment Unit Size by Region

|

% Change by Region |

-8% | -8% | -9% | -5% |

| West Markets | East Markets | Midwest Markets | South Markets |

|

Denver Los Angeles Riverside-San Bernardino San Diego San Francisco Seattle |

Boston New York Philadelphia Washington, DC |

Chicago Detroit Minneapolis St. Louis |

Atlanta Dallas Houston Miami Phoenix Tampa |

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

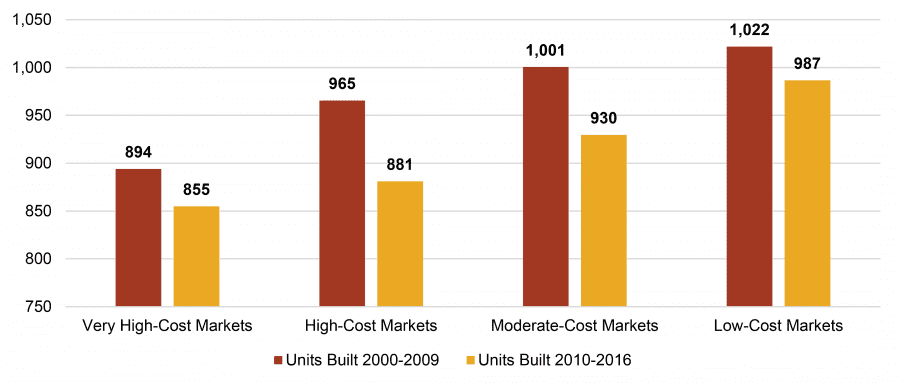

High- and Moderate-Cost Markets See Largest Size Reductions

Aggregating the markets by relative housing cost shows how pricing economics have influenced the change.[2] Average unit size shrunk the most in moderate- and high-cost markets, where there has been an attractive combination of strong demand fundamentals for new product in general and larger base unit sizes relative to the very high cost markets. As a result, new supply in high- and moderate-cost markets today is sized much more comparably to that in very high-cost markets—the gap in size between the average new unit in New York and Washington, D.C., for example, has closed quite a bit.

By comparison, average new unit sizes only declined 4% in the very high-cost markets overall. Average new unit sizes in these markets were already at least 100 square feet smaller than in the other markets, making it more difficult to trim additional square footage at an equivalent rate.

Perhaps not unsurprisingly, low-cost markets have seen the smallest reduction in new unit size (3%) this period. Without the price pressure seen in higher-cost markets, there has been less impetus to push sizes down.

Average New Apartment Unit Size by Market Cost

|

% Change by Market Cost |

-4% | -9% | -7% | -3% |

| Very High Cost | High Cost | Moderate Cost | Low Cost |

|

New York San Francisco |

Boston Chicago Los Angeles San Diego Washington, DC |

Atlanta Dallas Denver Houston Miami Minneapolis |

Detroit Phoenix Riverside-San Bernardino St. Louis Tampa |

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

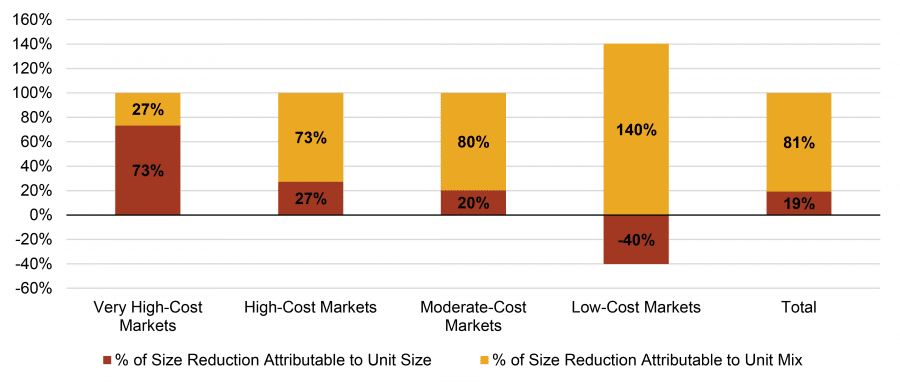

Except in Very High-Cost Markets, Change Driven by Shifting Unit Mix

Overall, approximately 80% of the reduction in average new unit size is attributable to changes in unit mix—in other words, increasing the share of studio and one-bedroom units at the expense of larger unit types—rather than shrinking floorplan sizes for units of a particular type. In fact, unit sizes in low-cost markets actually increased slightly in the latest generation of new rental community development. As market cost increases, however, the influence of unit mix decreases, from causing 140% of the change in average unit size in low-cost markets to only 27% in very high-cost markets. This is due to the fact that unit mix in higher-cost markets is already more heavily weighted toward smaller unit types.

Attribution Analysis: Is the Decrease in Average Unit Size Attributable to Changing Unit Mix or Shrinking Units?

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

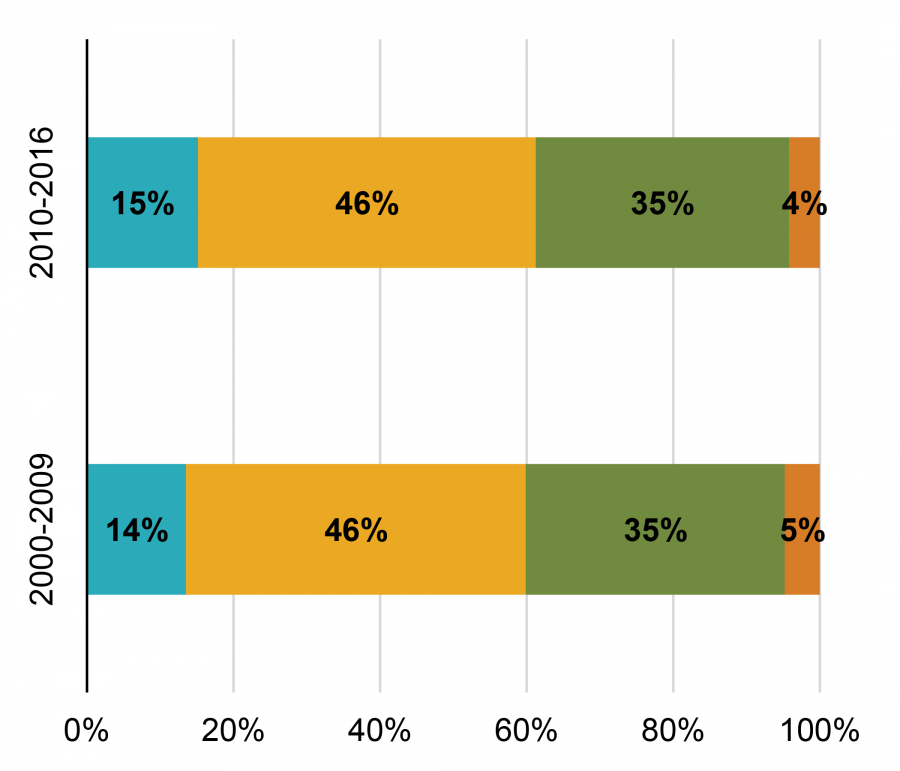

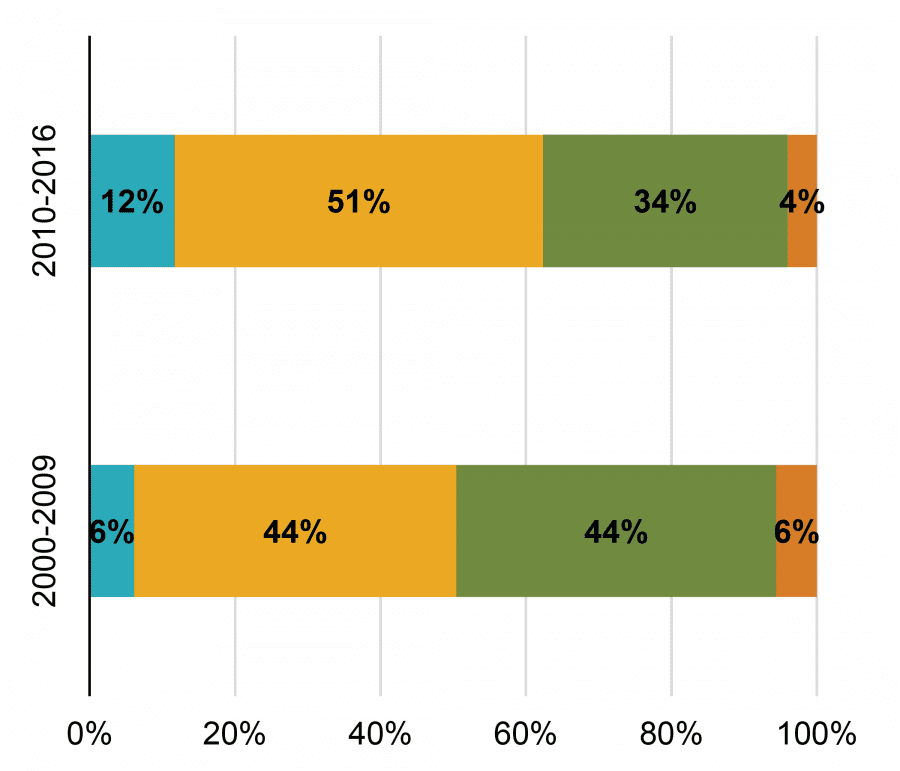

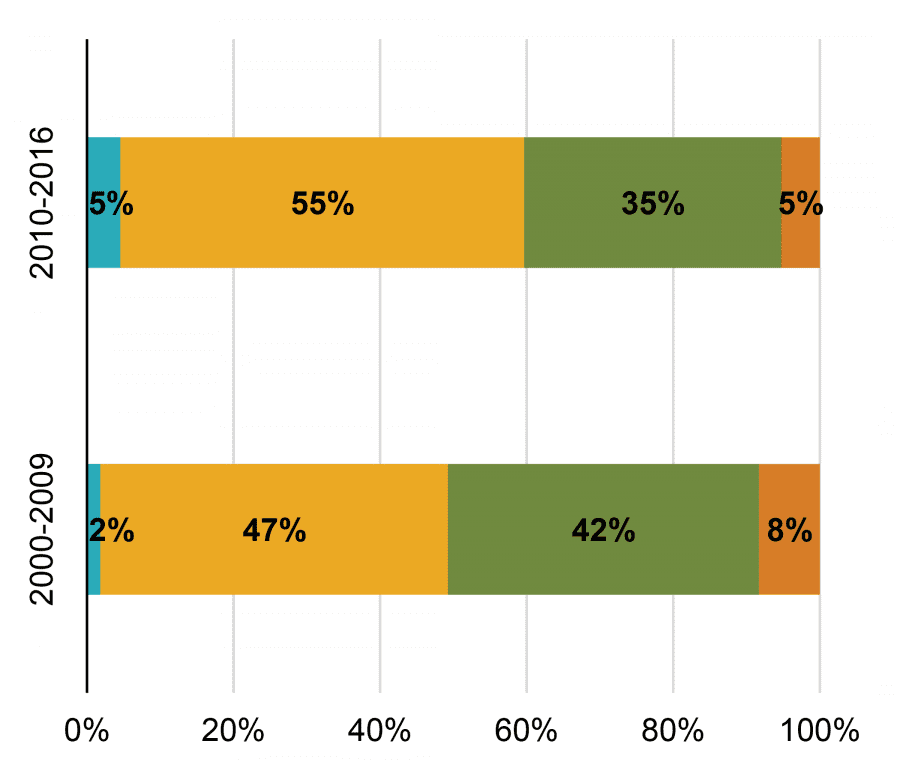

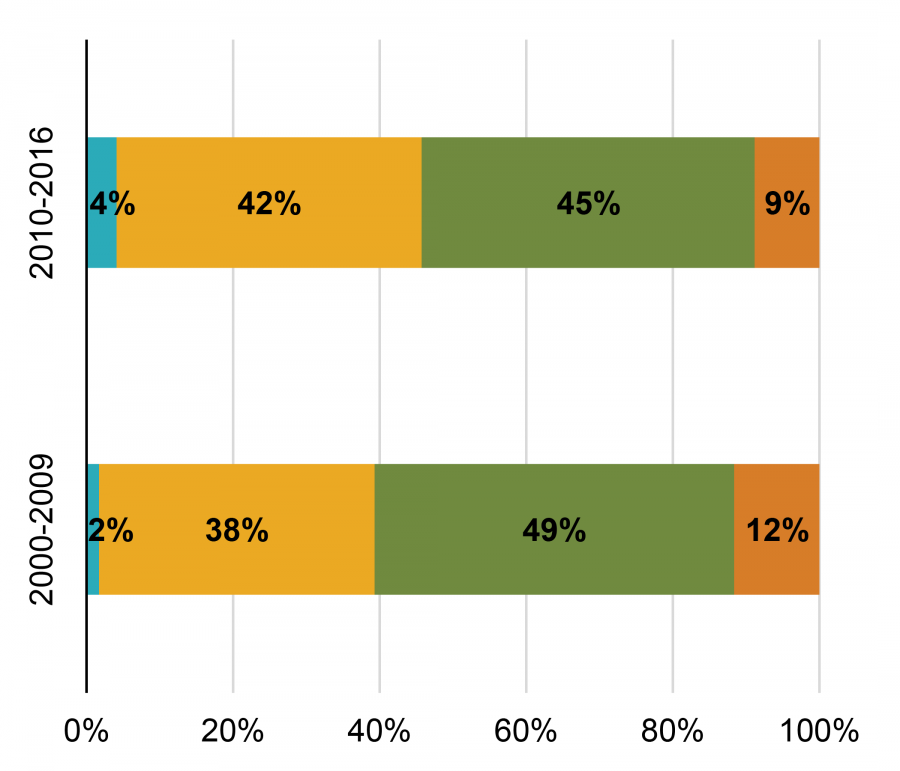

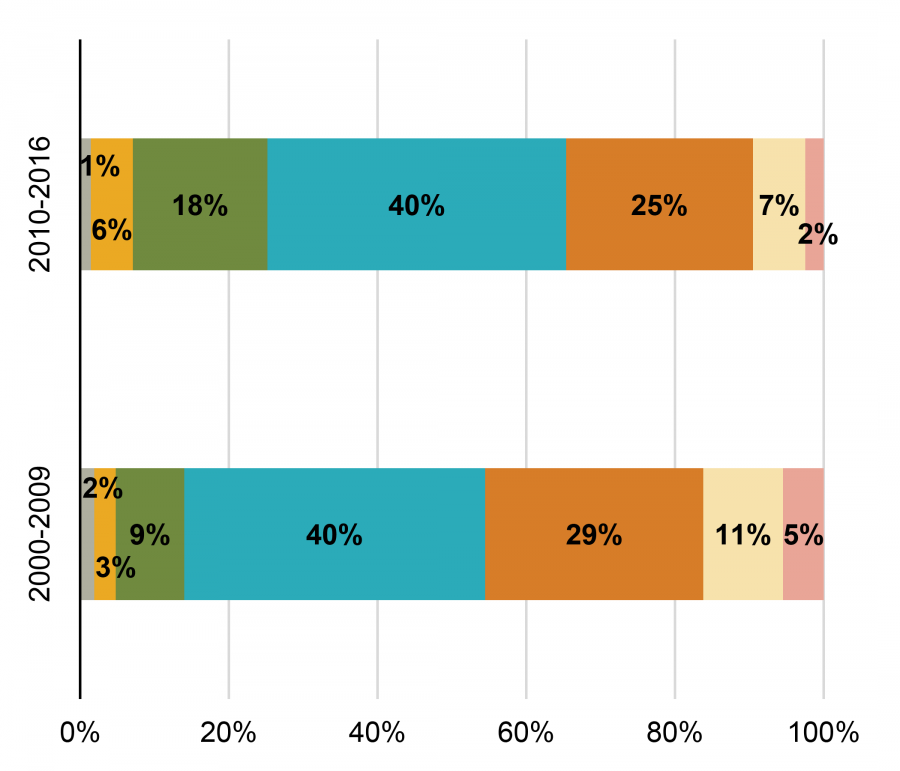

At the heart of the change in unit mix is the reduction in new two-bedroom units as they are squeezed out by more studios and one-bedroom units, particularly in high- and moderate-cost markets where average unit size has decreased the most.

Distribution of New Units by Unit Type

|

Very High-Cost Markets

|

High-Cost Markets

|

|

Moderate-Cost Markets

|

Low-Cost Markets

|

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

Two-bedroom units accounted for over 40% of new supply in high- and moderate-cost markets in the 2000-2009 period. From 2010-2016, however, they have comprised 35% of new units. In these markets, studio and one-bedroom units previously accounted for approximately one-half of the combined unit mix in these markets; they now account for closer to two-thirds. Studios alone have doubled their share of the unit mix in these markets. In effect, the average unit mix in high- and moderate-cost markets has been moving closer to the distribution in very high-cost markets.

In very high-cost markets, the mix of unit types delivered since 2009 is not much different than in the 2000-2009 period. Most of the reduction in average unit size in very high-cost markets, therefore, is attributable to smaller floorplans, rather than shifting unit mix.

Floorplans Getting Smaller, Too

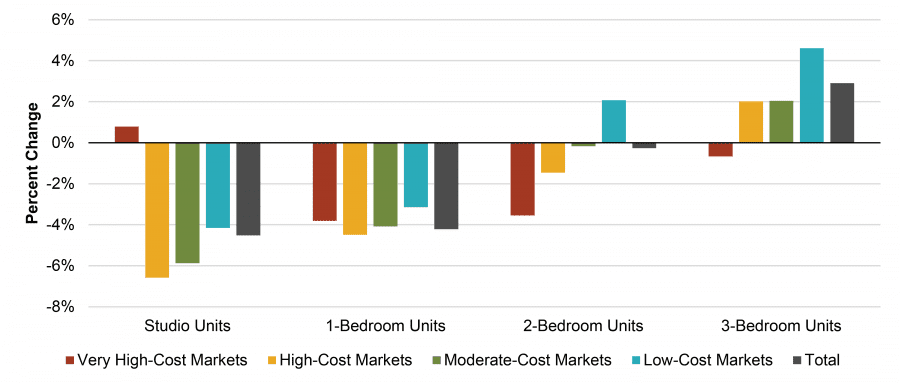

In addition to a higher mix of smaller unit types, floorplans for given unit types have also generally gotten smaller this period, particularly among studio and one-bedroom units, which have both shrunk by approximately 4% overall, or 25 to 35 square feet, respectively. Only the very high-cost markets have seen a marked decrease in two-bedroom size, however. Interestingly, three-bedroom size has actually increased in three of the four market categories, indicating that those units are becoming larger at the same time that they are becoming a smaller share of the overall unit mix.

Change in Average New Unit Size This Period (2010-2016) Compared with Last (2000-2009)

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

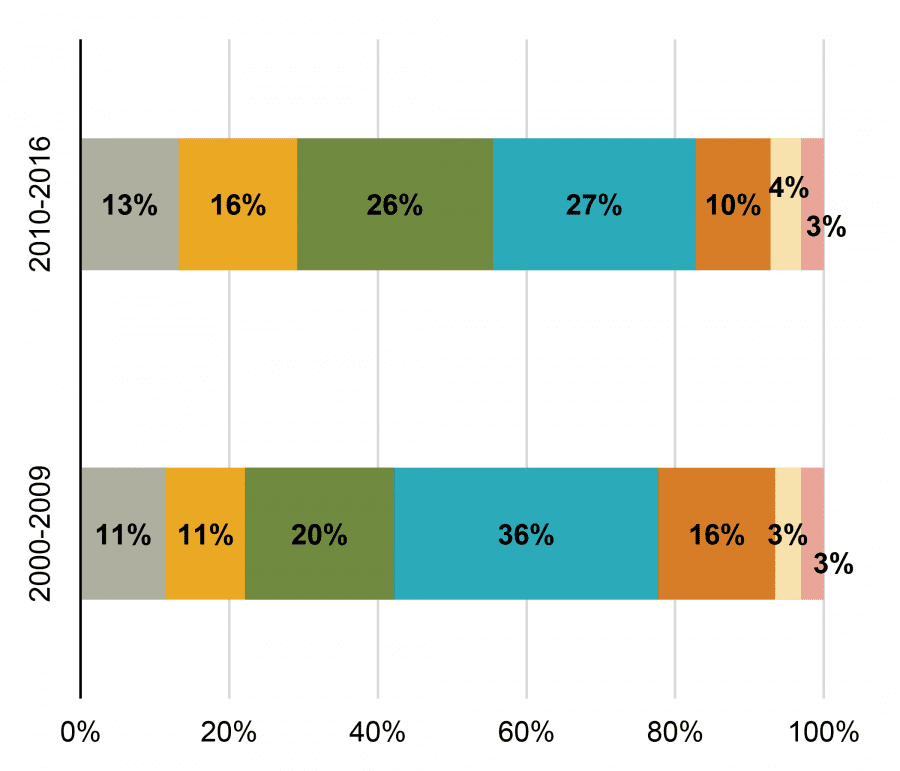

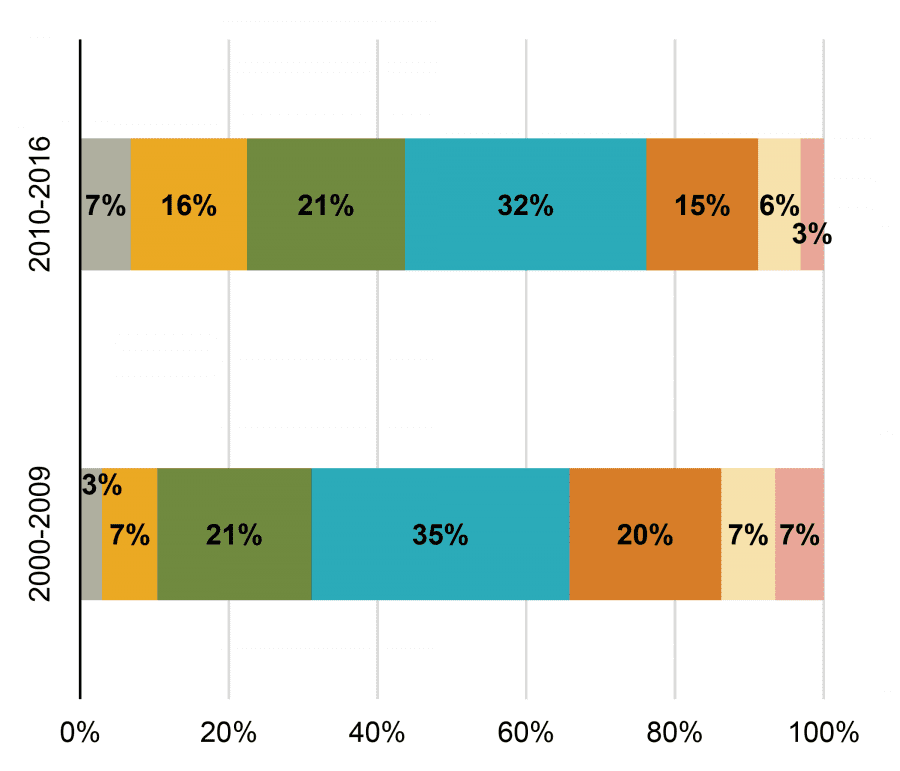

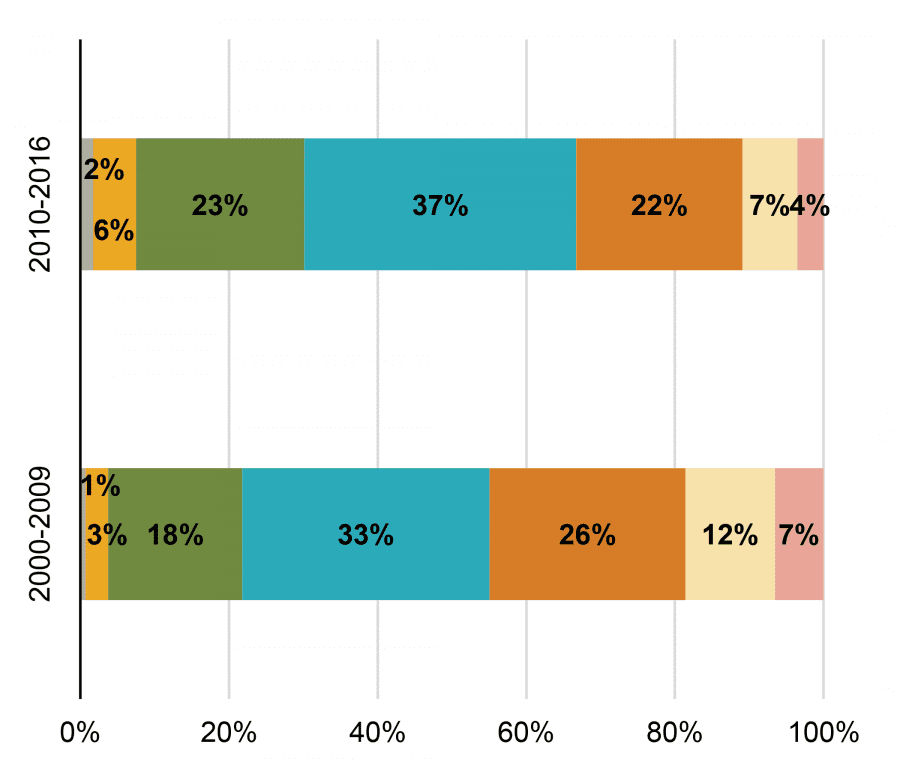

Share of Units Under 600 Square Feet Doubles

Taking a closer look at the unit types where floorplans are shrinking the most—studio and one-bedroom units—reveals that the mix is shifting away from units 800 square feet or larger at all markets, regardless of cost levels, and the most dramatic change is occurring at the smallest end of the size spectrum. The share of units under 600 square feet doubled to 15% of new studio and one-bedroom supply during the 2010-2016 period compared with 2000-2009. Furthermore, units under 700 square feet increased from 25% to 37%.

Distribution of New Studio and One-Bedroom Units by Size

|

Very High-Cost Markets

|

High-Cost Markets

|

|

Moderate-Cost Markets

|

Low-Cost Markets

|

SOURCE: Axiometrics; RCLCO. Includes data from the top U.S. 20 metro areas by population.

In very high- and high-cost markets, the largest growth has occurred in the share of units under 600 square feet. Most striking is the change in high-cost markets, where units smaller than 600 square feet only comprised 10% of new studios and one-bedrooms between 2000 and 2009 but represent 24% of those unit types built this period.

In moderate-cost and low-cost markets, the shift is occurring away from one-bedroom units 800 square feet or larger in favor of ones in the 600- to 800-square-foot range. Where one-bedrooms 800 square feet or larger comprised 45% of new studio and one-bedroom supply in these markets from 2000-2009, they have accounted for only one-third of those unit types from 2010-2016. Even today, however, units smaller than 600 square feet remain rare in these markets. The shift in unit sizes suggests a rightsizing of the one-bedroom supply more than adoption of the studio and micro floorplans that have gained a stronger foothold in markets with higher housing costs.

Appendix: Change in Average New Unit Size by Market

|

Rank by % Change in Avg Unit Size |

MSA |

Avg Apt Unit Size |

Size Difference |

||

|

Units Built 2000-2009 |

Units Built 2010-2016 |

Square Ft. |

% |

||

|

1 |

Philadelphia-Camden-Wilmington, PA-NJ-DE-MD |

1,097 |

828 |

-269 |

-25% |

|

2 |

Detroit-Warren-Dearborn, MI |

1,156 |

889 |

-267 |

-23% |

|

3 |

Seattle-Tacoma-Bellevue, WA |

901 |

768 |

-132 |

-15% |

|

4 |

Minneapolis-St. Paul-Bloomington, MN-WI |

1,030 |

913 |

-117 |

-11% |

|

5 |

Boston-Cambridge-Newton, MA-NH |

1,025 |

914 |

-110 |

-11% |

|

6 |

San Francisco-Oakland-Hayward, CA |

923 |

825 |

-98 |

-11% |

|

7 |

Washington-Arlington-Alexandria,DC-VA-MD-WV |

970 |

880 |

-90 |

-9% |

|

8 |

Atlanta-Sandy Springs-Roswell, GA |

1,066 |

969 |

-97 |

-9% |

|

9 |

St. Louis, MO-IL |

1,030 |

937 |

-94 |

-9% |

|

10 |

Miami-Fort Lauderdale-West Palm Beach, FL |

1,089 |

993 |

-97 |

-9% |

|

11 |

Tampa-St. Petersburg-Clearwater, FL |

1,077 |

1,002 |

-76 |

-7% |

|

12 |

Dallas-Fort Worth-Arlington, TX |

970 |

909 |

-61 |

-6% |

|

13 |

Denver-Aurora-Lakewood, CO |

960 |

908 |

-53 |

-5% |

|

14 |

Los Angeles-Long Beach-Anaheim, CA |

958 |

916 |

-41 |

-4% |

|

15 |

Chicago-Naperville-Elgin, IL-IN-WI |

912 |

879 |

-33 |

-4% |

|

16 |

New York-Newark-Jersey City, NY-NJ-PA |

890 |

866 |

-24 |

-3% |

|

17 |

Houston-The Woodlands-Sugar Land, TX |

990 |

978 |

-12 |

-1% |

|

18 |

Phoenix-Mesa-Scottsdale, AZ |

977 |

965 |

-12 |

-1% |

|

19 |

San Diego-Carlsbad, CA |

1,010 |

1,042 |

32 |

3% |

|

20 |

Riverside-San Bernardino-Ontario, CA |

998 |

1,086 |

87 |

9% |

SOURCE: Axiometrics; RCLCO

References

[1] Refer to report Appendix for market-by-market size data.

[2] The definition of relative market cost is based on the approximate rent per square foot for new product in urban areas of each MSA. Rent for the typical new rental apartment in very high-cost markets tends to be in the $4.00+/square foot (SF) range, high-cost markets between $3.00 and $4.00/SF, moderate-cost markets between $2.00 and $3.00/SF, and low-cost markets sub-$2.00/SF.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us