RCLCO futuRE Series: A Driverless Vehicle Roadmap for the Real Estate Practitioner – Part 3

What Should Building Owners and Developers Be Doing Today in Anticipation of this Mega Shift?

Introduction

In 2015, RCLCO published in this space a two-part series on the potential impact of driverless cars on real estate and land use. These articles have helped frame the national discussion on key structural changes that will affect real estate as autonomous vehicles become increasingly widespread over the coming decades.

Even before autonomous vehicles become pervasive, building owners and developers will need to adapt to a range of shorter-term trends:

- Changing commuting patterns and public transit use—driven in particular by accelerating adoption of shared vehicles (transit on demand) and marked improvements in rubber tire or bus rapid transit.

- Radically evolving parking behavior and needs, and in the long term the likely obsolescence of large on-site parking facilities.

- Dramatic transformation in the organization of logistics, warehousing, and last-mile delivery, which is tied to the wholesale evolution of the retail industry itself.

So When and (More Importantly) So What?

The most thoughtful research and commentary to emerge over the past 12 to 18 months have suggested that while the first commercially available, optionally self-driving cars is very near indeed (within a handful of years), the probable timeframe when cars will be routinely navigating urban places without drivers behind the wheel is much longer—probably at least 20 years and even more like 30.

The evidence seems to suggest that while vehicles will progress quickly in the coming years through phases of increased automation and intercommunication, the logistical and safety complications, and the needs and magnitude of infrastructure investment (a fascinating topic and perhaps the subject of part four in this series) to reach true autonomy, are daunting. It will take time and much innovation several steps beyond the technology we have today to resemble the utopian future we have in mind.

RCLCO believes that within the investment timeframe of all but the longest minded real estate investors, most users will come and go from homes and places of work playing an active role in the navigation of their own vehicles or riding in mass transit or ridesharing vehicles that have a driver in them.

But while the evolution will be slow, and may even happen with missteps along the way, technology within the next five to 10 years will begin to play a much more dramatic role in private vehicle traffic and planning management and will rapidly improve the efficiency of and range of options that constitute mass transit.

This is critical because while the time to full adoption may be several decades, there will be a very interesting intermediary period beginning quite soon, during which land use economics will begin to shift meaningfully. The shrewd real estate strategy is to begin planning for this evolution today, well before its ripple effects are felt, and even if the Jetsonian future we all imagine is still far off.

So What Will Change Soon in Terms of How Vehicles Move People?

1. Congestion Relief

Before we get to a fully autonomous future, we will be incrementally developing the necessary “smart grid” that will allow us to use our existing road infrastructure far more efficiently. Lane directions will be more easily changed, traffic–responsive signalization will be far better, congestion pricing for road use will drive different consumption patterns, and so forth. Our efficient use of highways, in particular, will be significantly better as our human-guided cars begin to talk to each other and share information and more of them have limited automation (e.g., adaptive cruise control, lane centering), all of which will hopefully also improve highway safety.

2. City Districts Begin to Shift to Autonomous-Only Zones

Several factors suggest we will need to begin closing traffic to self-driven cars in our most urban and congested areas sooner rather than later. In other words, a near-term step in the evolution to driverless cars is moving in the densest areas to a complex mix of conventional transit, shuttle, and rideshare, all increasingly autonomous, which will dramatically reduce their cost of use, capacity, and safety.

This will start with closed loop systems (like the Olli autonomous people mover system that already exists at National Harbor near Washington, D.C.) and begin to mix in shared and then eventually privately owned autonomous vehicles as the technology matures.

As an example, the City of Las Vegas is already running test projects with autonomous vehicles on Las Vegas Boulevard, and it’s not hard to imagine the Strip and places like it evolving to be self-driving only, with many vehicle types moving people in autonomous road vehicles with varying cost-of-use implications.

3. Emergence of Affordable Last-Mile Transit Alternatives

As we have argued in the past, transit on demand—what we today think of as Uber and Lyft—will evolve quickly as that technology improves, users continue to become comfortable with this as a transit alternative, prices become more compelling, and so forth. Driverless technology is so critical for transit on demand (Uber and Lyft today) to change behavior because removing the human driver will dramatically reduce the cost of service provision.

Transit on demand, we posit, will begin to serve as an alternative to bus mass transit, particularly in less urbanized areas. As this fleet of vehicles becomes more diverse, technology-enabled, and eventually driverless, this transportation mode will rapidly accelerate the rate at which people can reduce their private car use, or go carless altogether, particularly in more suburban locations. This technology will also accelerate the last-mile distribution shift discussed below.

With this future in mind, among other strategies, RCLCO is counseling our clients to:

- Begin to Disaggregate Parking and BuildingsWe are undoubtedly over-parking buildings today relative to future demand, recognizing that we have no choice today but to continue doing so. During this evolutionary period and even before we have fully autonomous cars, cars may become self-parking, ride sharing will continue to increase (even before it is autonomous), and parking inventory will be much more efficiently managed, but still necessary.

What today is an important preference for (ample) parking within one’s own office or residential building is not likely to be as important even in the near future, and might appear downright wasteful in 20 or 30 years when consolidated and offsite (and potentially remote) parking will function just as well for the human and much better from a vehicle management point of view.

- District Parking

Developers of long-term, large-scale projects should begin to consider district parking solutions in which parking is shared among buildings in a centralized structure. This may ease the pain over parking buildings relative to likely future need in the near term and being able to under-park them in the future.Universities and other places where people already move within the “project” more efficiently by bus, shuttle, walking, and bike, are already pushing parking to consolidated structures on the campus edge.

-

Treat Parking Like Its Own Land Use, Not a Supporting Amenity

At the Coloradan, a luxury condominium building under construction in Denver, developer East West Partners is building integrated but independently operated (and as a single separate condo) parking, where homebuyers are welcome to pay for a space, but which is not in any way tied to their unit. The developer is pushing the market today, but acknowledging that parking needs are already very diverse and may be far different in the foreseeable future, and the owner of that parking preserves their optionality in terms of who is the customer.

- Convertible Parking

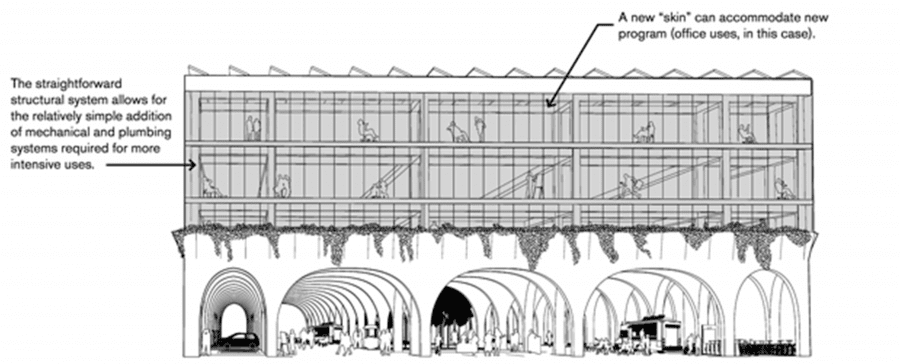

To the degree to which you have to build parking for today’s consumer, plan parking space that is convertible to another use. Creative architects have begun to play with (preferably above-ground) parking floorplates that convert to office or other uses with moderate additional investment. - The Uber Queue Dilemma

Anticipate that pick-off and drop-off congestion will become much more pervasive—much like we didn’t consider the Amazon package dynamics in the apartment lobby. Shared ride services will disrupt private car use at an accelerating pace, and one implication is the complicated queuing in urban places as passengers are picked up and dropped off, which building owners will need to plan for.

- District Parking

- Revisit Your Definition of Transit-Oriented Development

As we develop inexpensive last-mile transportation alternatives as discussed above, developers and owner/operators should take account of the following likely trends:- Urban-ish Locations Evolve

Explore potential development or acquisitions in areas just beyond the tight fixed-rail transit stations radii, which will become better transit-served even with this interim technology. In major urban areas we already consider the “$5-$7 Uber shed” (depending on the city minimum) as an alternative to truly transit-oriented locations and can document a price premium in these zones in some instances. UberPOOL and other advanced “slugging” systems will accelerate this. In time, and accelerating as the driver is gradually phased out, the last mile of travel will become even cheaper. - Leapfrog Development

Consider investment in attractive “satellite towns” with high quality of life (Frederick, Maryland; Petaluma; Princeton; Ojai; the Texas Hill Country), from which commute times may shrink considerably as our road networks are able to move much more traffic more quickly and express buses become viable, even well before fully autonomous vehicles. Hopefully the quality of life in these and new edge towns can be preserved.Similarly, developers should consider compact and middle-density transit villages on the suburban fringe. If “new towns” can offer cute product and walkability, and value, residential demand might leapfrog existing and in many cases uninspiring suburbs, creating a new and sustainable model of distributed growth. Advanced carpooling and a high-speed, technology-enabled bus system, should open up this opportunity even in advance of significant private ownership of fully autonomous vehicles.

- Take to the Seas

Waterways are the next highways—autonomous ferry service may materialize quicker than cars (there are far fewer potential human conflicts)—with automation making water travel and upriver or downriver commercial concentrations increasingly appealing. Autonomous operation means lower operating costs and much shorter headways, perhaps finally making this transit mode feasible.

- Urban-ish Locations Evolve

- Invest in Changing Logistics Dynamics

The way we move goods is likely to evolve more quickly than the way we move people, and the potential for value lift in industrial assets will be considerable and may materialize quite soon.- Invest in Inland Ports

Driverless (and more fuel efficient) trucks will become feasible more quickly than cars (smart highways are more nearly feasible today than smart urban grids), likely pushing warehousing and freight transfer facilities to places more remote from urban centers and into larger and more concentrated mega facilities. - Last-Mile Distribution

Maybe it isn’t overpriced after all! Freight will have to be broken into conventional delivery in town, which, along with the evolution of retail and the redevelopment pressure on close-in logistics space, will make these small infill industrial assets even more expensive in the future than they are today. - Retail Redux

Reposition retail portfolios to focus on experience instead of goods—home delivery by a non-human device will accelerate quickly (delivery by drones) is not science fiction by any means and other forms of more efficient delivery will become increasingly important even before the next generation of smart drones and other flying autonomous vehicles. Don’t underestimate the threat to convenience retail, including groceries, or the human need to interact publicly in exciting places to eat, exercise, experience art, or seek healing.

- Invest in Inland Ports

Conclusion

We’re not speaking out of both sides of our mouths. The utopian future we have been promised—reading the paper while our private vehicle speeds around town at high speed—is on its way, but it will take decades to be realized and widespread. In reality, it will be difficult to capitalize on its coming in the foreseeable future.

But the impact of marginal advances in a smart transportation infrastructure will begin to drive income and asset values in almost every asset class even within a five to seven year investment period.

The real estate industry does not have a good track record of responding creatively to technology evolution despite the clear evidence that there is money to be made from doing so. Much as the wholesale move to the private car in the post-WW II era radically changed American urban economics, so too will autonomous vehicles. Are we prepared to thrive, or will we just react?

Article and research prepared by Taylor Mammen, Managing Director, and Adam Ducker, Managing Director.

References

[1] Axiometrics rental growth in San Jose, Seattle, and San Francisco from 2010-2017 YTD.

![]()

RCLCO’s mission is to help clients make strategic, effective, and enduring decisions about real estate. In 2017, we celebrate 50 years of providing the best minds in real estate with cutting-edge analytics, actionable advice, and the highest level of customer service. Our work includes market, economic, financial, and impact analyses; investment portfolio strategy and implementation; entity-level strategic planning; and management consulting.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us