Surprises from RCLCO’s Economic Hot Spot Map

RCLCO first published an Economic Hot Spot map in 2013. At the time, the economy was recovering from the Great Financial Crisis at a very uneven pace across regions. The idea was to get a sense of where growth was currently happening and why. Based on trailing and forward 12-month indicators of factors such as growth, income levels, and economic structure, the map gave us a good indication of regional growth patterns.

In fact, the map turned out to be quite telling. Many of the high-ranking markets at the time were tech and energy related—and subsequently experienced substantial job growth that led to some of the hottest commercial real estate markets in the country, in terms of both demand and new construction. In fact, the top 15 large markets in our 2013 rankings accounted for 58% of net office absorption and 64% of new office construction in the 51 largest markets in the United States in 2014 and 2015.

We returned to the rankings this month to see how things have changed and found several surprises.

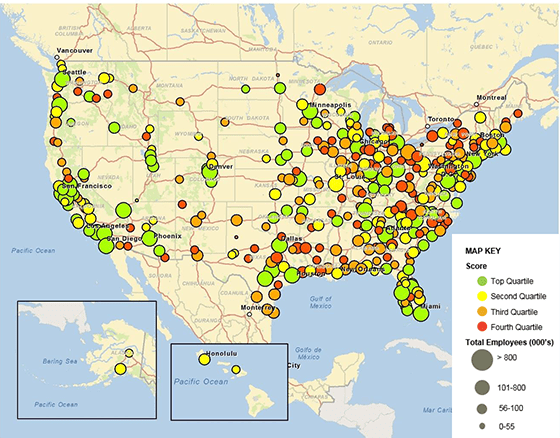

Economic Hot Spot Map

Source: GIS, RCLCO

Tech Expands to More Regions While Energy Markets Fall

One big surprise was a decline in the rankings of two large tech hubs—Austin and San Jose—although both stayed in the top-15 markets. Overall, movement in tech market rankings was mixed. With employment tightening and costs rising in the key hubs, job growth seems to be expanding into other locations, particularly those with urban, walkable locations and desirable life styles. Case in point: San Francisco rose in the rankings and San Jose’s rank declined as the San Francisco South of Market submarket exploded, offering walkable work and living options, restaurants galore, public transportation, and a cool vibe in newly rehabbed office buildings. Seattle maintained its high ranking while Portland rose significantly in the ranking.

Not unexpectedly, several of the energy markets fell in the rankings. Houston fell from the top 10 to 35 among the largest markets. Bismarck, North Dakota, the top-ranked small market in 2013, fell to fifth position, and even diversified markets such as Dallas fell by 10 spots or more.

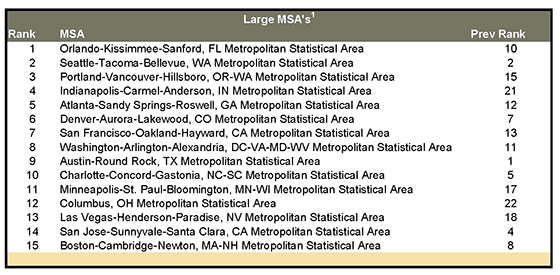

Economic Hot Spot MSA Rankings – Large

Source: RCLCO

Resort-Area Markets Rebound Strongly

As the economy recovers, money is again flowing into resort and entertainment-oriented markets of all sizes, which moved up in the rankings. Large markets such as Orlando and Las Vegas rank well, but the trend is particularly notable in smaller markets, with Bend-Redmond, Hilton Head, and Napa ranking in the top-five small markets. National increases in second-home sales over the last few years, coupled with an increase in foreign investments in vacation-oriented real estate (particularly in Hawaii and Florida), have contributed to these markets’ success. (As an aside, it is notable that large movements in the rankings, particularly for some of the mid-size and smaller markets, are a good reminder of how volatile smaller markets can be if they are largely dependent on a single industry or employer.)

STEM Workers Continue to Drive the Economy

According to the Bureau of Labor and Statistics, STEM (science, technology, engineering, and math) employment will expand 1.7 times faster than non-STEM employment between 2010 and 2020 nationally. A higher share of STEM workers continues to be a strong indicator of economic growth within MSAs, due in part to the high-paying nature of these professions. The five MSAs with the highest % of workers with STEM professions (San Jose, Washington, D.C., Seattle, Denver, and Raleigh) all rank in the top 20 of the large MSAs.

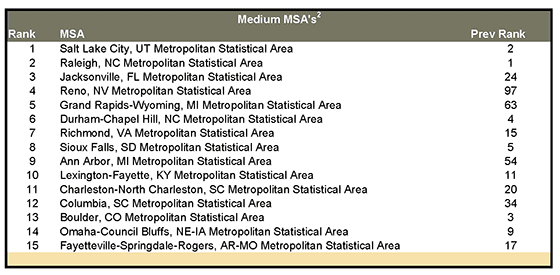

Economic Hot Spot MSA Rankings – Medium

Source: RCLCO

The Midwest Makes a Comeback

The biggest surprise in the new rankings was the improvement of some Midwest markets—particularly Indianapolis (ranked 4 among large MSAs), Minneapolis (11), and Columbus, Ohio (12). Minneapolis maintains solid growth and ranks high on economic structure factors, including growth in the working population, high income levels, and high employment to population ratios. Columbus ranked similarly to 14th-ranked San Jose on a number of population growth factors and the number of new jobs created, and Columbus’s future economic growth is forecasted to be even stronger than San Jose’s. (While the effectiveness of numerous policy changes to drive employment growth in Ohio over the past few years can be debated, the state has been striving to attract aerospace, advanced manufacturing, biohealth, financial services, logistics, and information technology companies.)

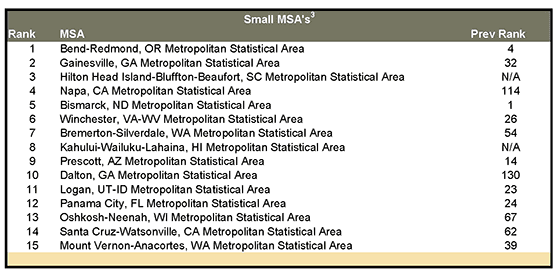

Economic Hot Spot MSA Rankings – Small

Source: RCLCO

Indianapolis is a prime example of a Midwest market that performs exceptionally well in the new rankings—increasing from 21st to fourth. Overall, Indianapolis has a growing job base in industries that are integral to the nation’s economy. It is a major healthcare hub, including several large hospital systems as well as the Indiana University Medical Center, the second-largest medical school in the nation, with a research and teaching faculty of more than 1,100 people. Additionally, the area is attracting tech companies, drawn to the educated work force and low costs. One example is Appirio, a cloud services firm, which moved its headquarters from San Francisco to Indianapolis in 2015, beating out other locations such as London and Tokyo. Why? The firm particularly cited an abundance of nearby universities from which it could hire.

A number of other factors likely played into this decision as well (in addition to a nice subsidy from the state in the form of programs such as tax credits and training grants). From the employer’s perspective, office rents in downtown Indianapolis at less than $20 per square foot on average are about one-third of rents in downtown San Francisco, which are starting to exceed $60 per square foot again. For the young people that are often working at tech firms—want to start a family and buy a house? That will cost you at least $2 million for about 1,500 square feet of space in prime tech areas in the San Francisco Bay Area, such as for a South of Market condo or older house in the Mountain View/Palo Alto area. In Indianapolis you can grab a downtown condo in the $350,000 to $500,000 range that will likely sport 2,000 square feet of space or more. Or if you want to commute, how about a 5,000 to 7,000 square foot McMansion in a prime submarket with good public schools in the $600,000-$700,000 range (and be sure to plan to pay for private schools if you want to stay in San Francisco). The significant difference in cost of living creates a different income need. Median household incomes in Indianapolis are approximately $53,000 as compared with $86,000 in San Francisco. Appirio says its salaries are more than 75% higher than Indiana’s average, so firms like this result in a nice boost to local income levels even when their salary levels are lower than in more expensive markets. And, in fact, Moody’s Analytics forecasts Indianapolis median household income growth of 5.4% in 2016, the highest in the country, following 4.8% growth in 2015. Appirio is not the only tech firm to locate in Indianapolis; Angie’s List, Geofeedia, and Interactive Intelligence are among other firms that are committed to adding tech jobs in the area. And what about that cool urban walkable vibe? Well, it may not be San Francisco, but downtown Indianapolis has come a long way in the last 20 years. A variety of retail and restaurant options, entertainment, sports stadiums, and museums are now located in downtown Indianapolis, as well as jobs encompassing a variety of industries, including medical and technology. In response, the residential market is strengthening. For example, the number of downtown apartments has increased by 80% since 2007, and rents have increased by over 8% per year over the past four years.

Is Indianapolis likely to take over New York or San Francisco as the new prime commercial real estate hot spot? Probably not, but the economic data is suggesting that jobs are expanding to new locations in states that are fiscally healthy and in areas that offer more affordable lifestyles. This trend is worth watching as the tech market and its employees mature and move into a different life stage—one that still values interesting, walkable downtowns and neighborhoods, but often requires good schools, a little space for kids, and more affordable housing and office space.

1 Large Metropolitan Regions are characterized by having total employment over 800,000 employees. 37 Metropolitan Regions meet this criteria, the listed MSA’s rank in the top ten.

2 Medium Metropolitan Regions are characterized by total employment between 100,000 and 800,000 employees. 158 Metropolitan Regions meet this criteria, the listed MSA’s rank in the top ten.

3 Small Metropolitan Regions are characterized by having total employment of less than 100,000 employees. 168 Metropolitan Regions meet this criteria, the listed MSA’s rank in the top ten.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us