Headwinds for Hotels as Construction Ramps Up

The Hotel Sector’s Strong Run

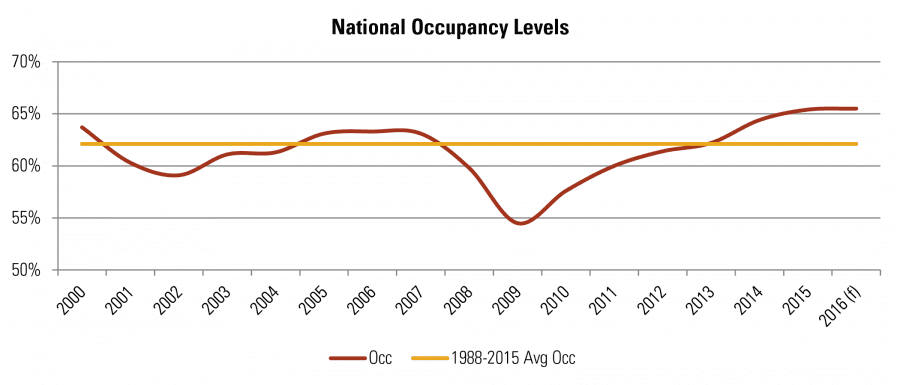

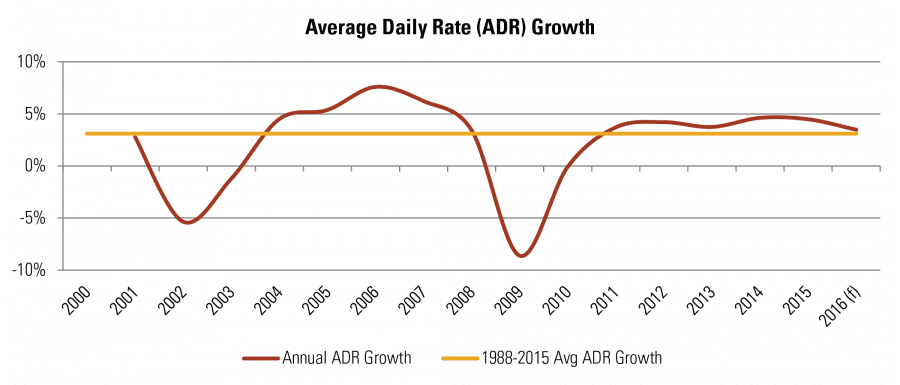

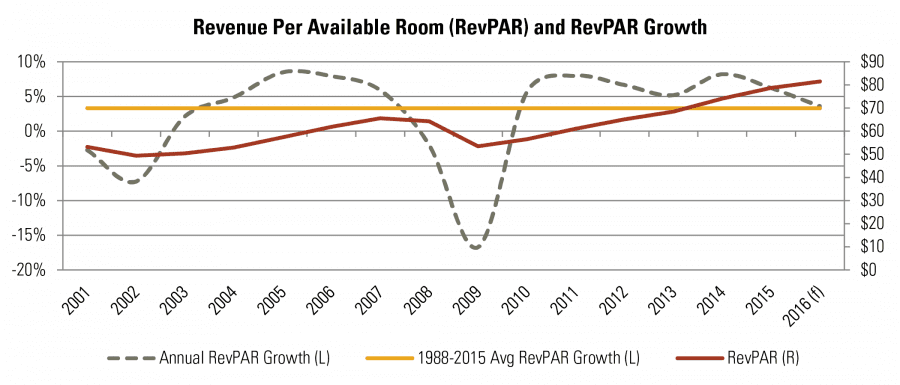

The hospitality sector has enjoyed robust performance post-recession, characterized by very healthy occupancy and average daily rate (ADR) growth. Historically strong occupancy levels, currently estimated at 65.5% for 2016, or over 300 basis points above the 1988-2015 long-term average, and ADR growth above long-term averages, have pushed revenue per available room (RevPAR) to historical highs. Moreover, the hotel sector has also enjoyed the strongest NOI growth of all major asset classes since 2010.[1] Given the volatile nature of the asset class, however, due to its by-the-night lease terms and relatively discretionary demand drivers, the sector is more sensitive to demand shocks, which are likely to be magnified by a large wave of oncoming supply.

Source: CBRE U.S. Hotel Horizons Report

Source: CBRE U.S. Hotel Horizons Report

Source: CBRE U.S. Hotel Horizons Report

But Will It Last?

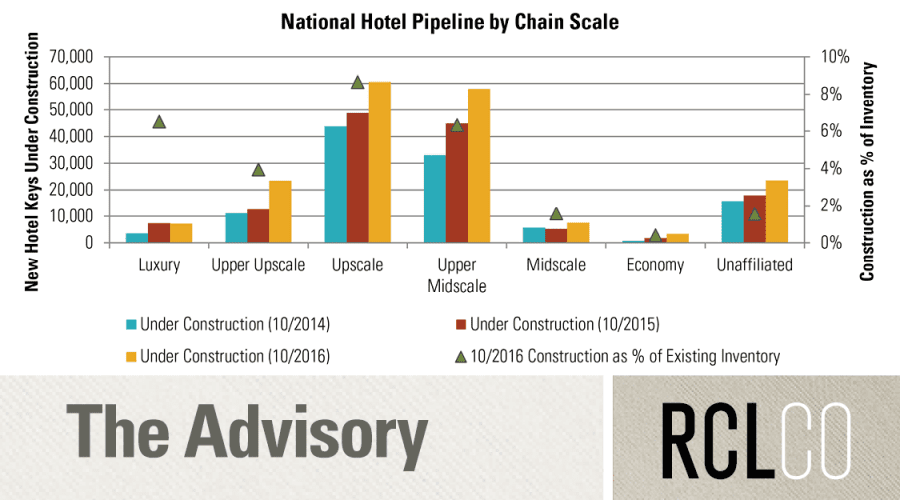

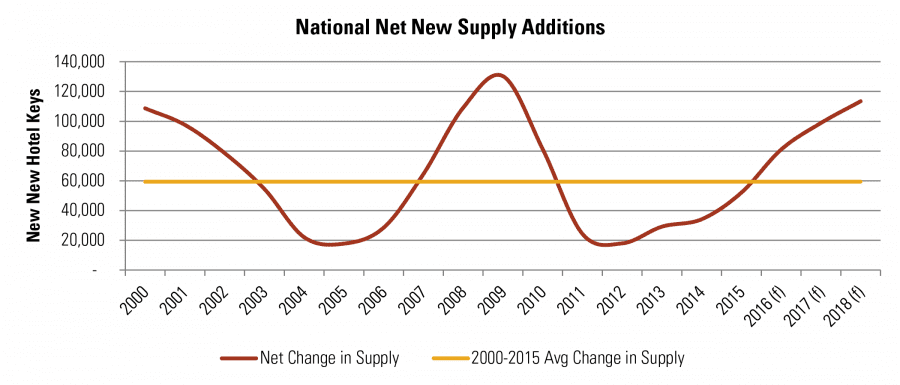

Much of the recent strong performance in the sector has been buoyed by low levels of supply additions, with new deliveries remaining below the long-term average through 2015. Softening international and transient corporate travel led to flat occupancy rates and reduced average daily rate growth in 2016, but a pickup in new supply is also dampening growth. Moreover, with over 180,000 hotel keys under construction as of October 2016, up 32% from a year earlier, a wave of additional supply is expected to hit the market over the next 18 to 24 months—perhaps just as the sector is reaching the late stages of the real estate cycle.

Source: CBRE U.S. Hotel Horizons Report

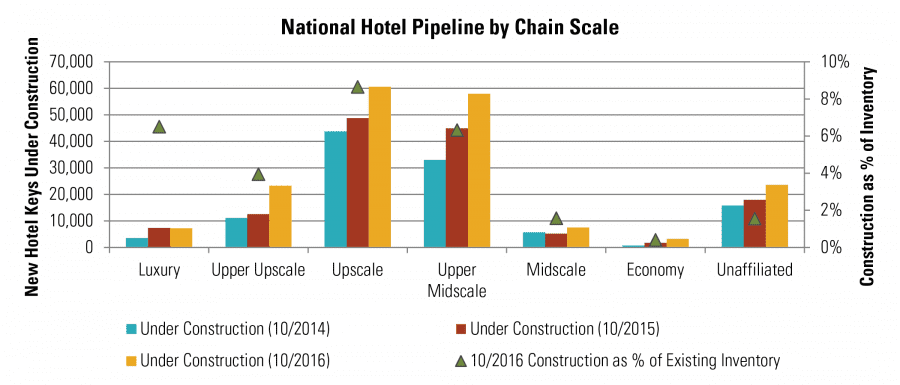

The hotel construction pipeline is distributed across the middle and upper hotel chain scales. “Upper Midscale” and “Upscale” chain scales, often of the “select service” variety (e.g., Courtyard by Marriott, Hilton Garden Inn), continue to account for a disproportionate share of the construction activity. “Select service” properties have been favored for their leaner operations and diverse market appeal, which enable them to perform across a range of markets and locations, but significant upcoming supply will test their endurance. In addition, upper tier chain scales, including “Luxury” and “Upper Upscale,” have also seen a substantial uptick in new construction: the number of hotel keys under construction has increased by 104% and 110% respectively between October 2014 and October 2016, a greater percentage increase than both the 61% overall uptick and the percentage increases in all other chain scales except “Economy.” Though still representing a lower share of overall inventory than the mid-tier chain scales, rising levels of new construction may be especially troublesome for the higher service level hotels, given softening international and corporate transient travel alongside rising labor costs.

Source: Smith Travel Research

Hotel Pipeline Highly Concentrated

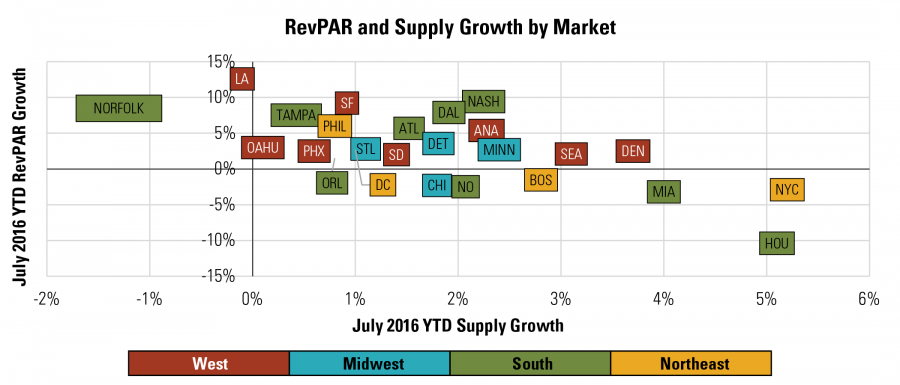

As the national hotel sector faces stiffening supply headwinds overall, the story of hotel performance is ultimately market-specific. Property level economics have begun to decline in areas with large supply additions: even markets with strong and diverse demand drivers, such as Boston, Seattle, Denver, and New York City, have seen RevPAR growth below the national average amidst significant supply additions. Other markets without significant construction activity, on the other hand, have continued to enjoy strong RevPAR growth.[2]

Source: Smith Travel Research

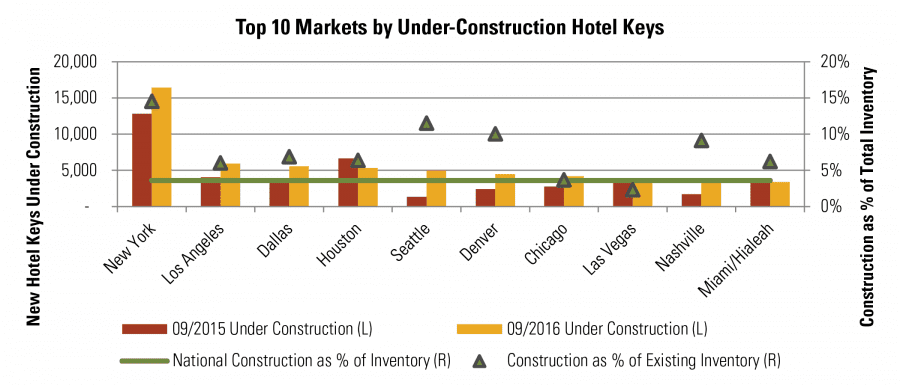

The hotel pipeline continues to be highly concentrated in major hospitality markets, with the top 10 markets by construction activity representing 31% of the nation’s under construction hotel keys, despite only accounting for 16% of existing supply.

Source: Smith Travel Research

“Checking Out” and “Checking In”

Despite excellent performance over the past few years, moderating demand drivers and the wave of new supply will likely present headwinds for the hospitality sector in the near term. Add to the mix a healthy volume of 2017 and 2018 maturities from pre-recession vintage CMBS, and hotels may be among the first in this cycle to experience broader distress. Some existing owners may therefore be forced to “check out” from certain hotel assets, giving others the chance to “check in.”

Notes

[1] Anika Khan and Julianne Causey, “Commercial Real Estate Chartbook: Q1,” Wells Fargo Securities, May 23, 2016, accessed November 29, 2016, https://www08.wellsfargomedia.com/assets/pdf/commercial/insights/

economics/real-estate-and-housing/cre-chartbook-2016q1-20160520.pdf; Other major asset classes include Multifamily, Office, Retail, and Industrial sectors.

[2] Some may be asking whether we think shared accommodations platforms, like Airbnb, could be creating headwinds for the hospitality sector, as well. While this is a complicated issue with many moving pieces, our view is that, though every market is different, shared accommodation services are having minimal impact on hospitality performance in the aggregate, as they mainly compete with the leisure demand segment, which is the smallest one, and are largely serving previously unmet or underserved demand. In essence, we think they are primarily growing the pie versus taking a large piece of it.

Article and research prepared by Sara Kramer, Vice President, and Mark Trainer, Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/expertise.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us