RCLCO Forecast: Does the Housing Market Still Want the Suburbs?

This is the third installment in a series examining New US Housing Demand, relative to underlying demand drivers.

Part 3: Where the Active Market Wants to Live

The National Association of Realtors Community Preference Survey tells us a lot about where people currently live as compared to where they’d like to live, and understanding those differences points to opportunities to fulfill unmet housing demand. To really understand how to apply the survey information we need to remember it’s not just about what people say they want in a survey, we also have to know who they are and how many of them are actively in the market for a new home.

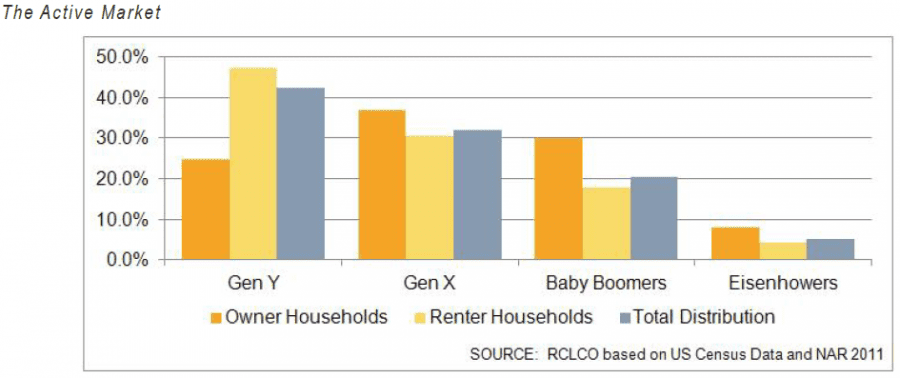

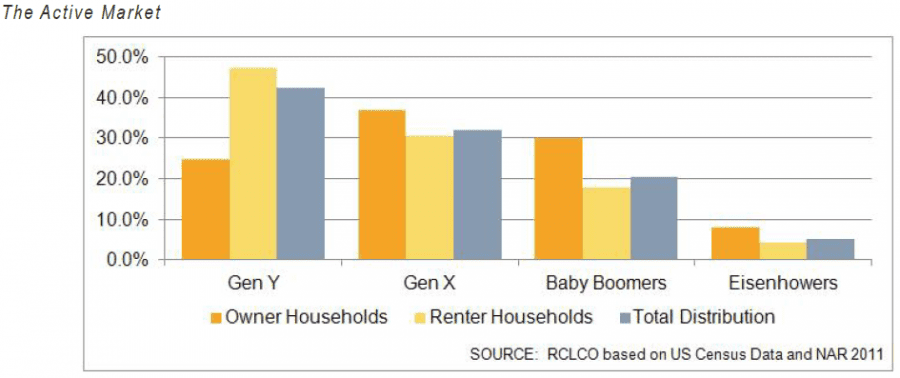

The active market is comprised of those households moving around in the housing market, buying or renting new and existing homes. As shown on the chart below, Gen Y is a very important segment of the housing market, holding sway over the active renter housing market, though they currently comprise a fairly modest share of the for-sale market. Given their age (10 to 29), only 22% of Gen Y’s currently head households and actually make housing decisions, which today is generally a decision to rent. The share of Y’s that head households is growing by 12% a year, and although they’re now largely renters, as more of them become household heads the percent that will become homeowners will also grow. Gen X still largely dominates the active market for for-sale housing at 37%, followed by the Baby Boomers with 30%.

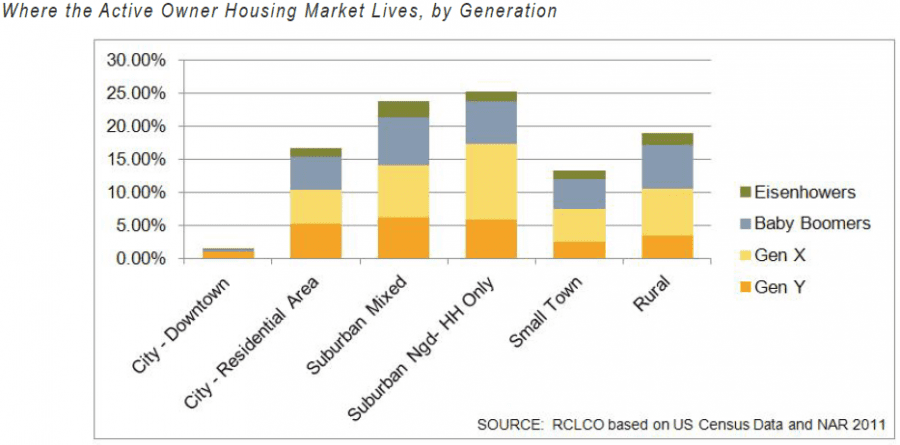

If we apply the NAR survey results against the size of the active for-sale market for each generation relative to where they currently reside, we find that a majority are in the suburbs:

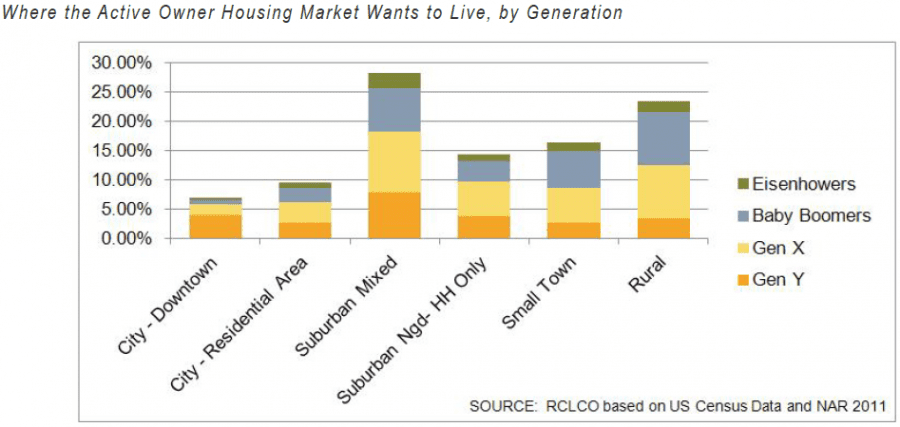

As shown on the chart, a majority of owner households, across all generations, currently live in “housing- only” suburban neighborhoods, and/or mixed suburban areas, defined as places with a mix of houses, shops, and businesses. But where would they live if they could—would they abandon the suburbs? Well, as many have reported, more Gen Y’s would head downtown. But more would head to mixed suburban areas, as would Gen X’s and Boomers.

So if there is dissatisfaction with the suburbs, it is for suburban areas that lack shopping, services and employment, not that consumers want to abandon them entirely. This likely refers to suburban areas that are further out toward the edge of metro regions, since they may be farther from shopping and employment. But this also applies to any place planned as a “residential only.”

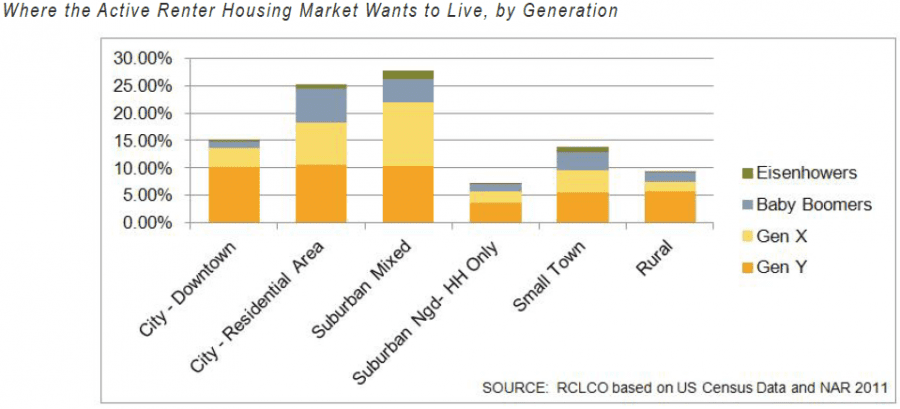

What about the active renter market? The chart below shows the distribution of the active rental market (renters in turnover) by generation, relative to where they say they want to live.

As you can see from the chart, active renters are not very interested in housing-only suburban neighborhoods. Many want to live in the residential area of a city, or even downtown, especially Gen Y’s. But the single largest share of the active market are those Y’s, X’s, Boomers and Eisenhower’s who would prefer to live in a mixed-suburban environment.

The data show that both owner and renter households active in the market prefer suburban mixed areas— but can those preferences be accommodated? Many mixed-suburban areas are already built out or in the process of becoming built-out, and they are not always the easiest places to go get entitlements for new infill developments. Nonetheless, where it can be done, the market for it is deep.

This analysis also points to opportunities to increase the appeal for master-planned community develop- ments, for them to be planned not just as places with a range of sizes and prices of single family homes, but as places with a broader diversity of housing as well as commercial development. Ideally this will include at least village-scale retail and being located closer to jobs, and where possible incorporating job centers within the actual development.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us