Top Dogs and Underdogs: Where Are We in the Cycle?

RCLCO National Sentiment Survey Part 2

In 3Q 2012, RCLCO’s National Sentiment Survey reported the majority of land uses bumping along the bottom, but with high hopes for the coming years. Over a year later, some land uses have lived up to expectations, while others continue the uphill struggle to stability. With the International Monetary Fund raising its 2014 growth outlook for the U.S. GDP to 2.8%, which land uses can be expected to lead the way? And which may be reaching stability?

Top Dog: Multifamily Rental

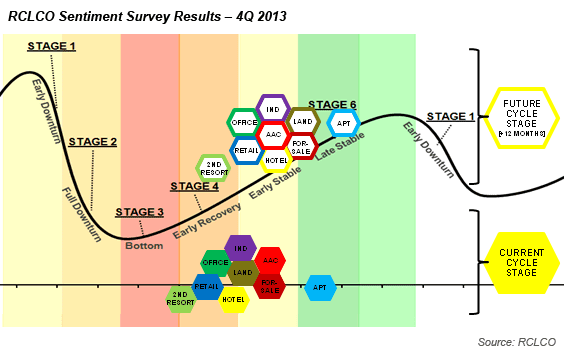

The land use most likely to make it to the top of the peak first comes as no surprise, as multifamily rental has been far ahead of the pack throughout the recovery. With the most forward momentum of any land use this quarter, multifamily rental continues to climb, with 55% of respondents believing that the industry is currently in late stable, and another 7% believing that it is in early downturn. Very little change is expected in 2014, with just 9% of respondents predicting a move into early downturn.

Most Popular Underdog: Active Adult Communities

Active adult/age-restricted communities have seen the smallest increases in both expansionary cycle movement and future expectation of any land use since late 2012. But just as any underdog would, this sector showed a leap forward in the last six months, at a pace topped only by multifamily rental. This underdog is also receiving continued support from builders, as the NAHB 55+ SFD Housing Market Index showed its eighth consecutive quarter of year-over-year improvements in 3Q 2013. Active adult also had the largest growth spurt in future expectations for 2014, with 50% of respondents expecting a continuation into early stable for the next year, and another 25% expecting a transition into late stable.

Most Improved: Office

In 3Q 2012, office remained stuck in the bottom of the cycle, far below all other commercial land uses. However, with the largest move forward since 3Q 2013, office catapulted more than an entire cycle stage forward in the past year and one-half, far above respondents’ predictions. This rapid improvement was likely informed by strong market fundamentals, including the steady decline of office vacancy rates, which fell to 11.5% in 4Q 2013.1 Although office has made great strides in current sentiment, expectations for the future remain low. In fact, respondents expect slower forward movement from office in the next year than from any other land use, apart from multifamily rental.

Most Likely to Succeed (Eventually): Second Home/Resort

As with all land uses, second home/resort has seen steady growth through recovery, although current sentiment levels are somewhat below 1Q 2013 expectations. Consistent with the more cyclical nature of the 2nd home/resort industry compared with real estate overall, respondents’ high hopes for second home/resort in the coming year have not been dampened. In fact, respondents are expecting more forward motion from second/home resort in the next year than all other land uses, with the exception of for-sale residential.

Best Looking: Land

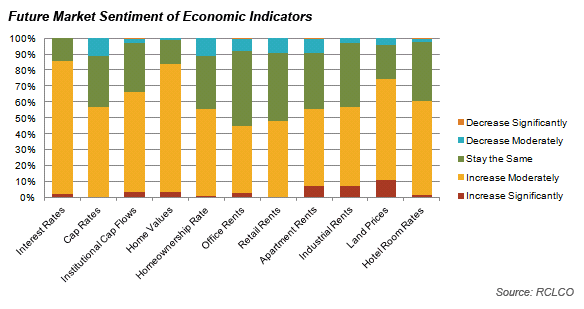

Land has continued steady, but substantial, growth since late 2012, and throughout the last six months, coming in just ahead of expectations from 1Q 2013. In addition to its steady movement up from the bottom, land prices continue to be one of respondents’ most steadily increasing economic indicators. Predictions for land over the next year remain some of the highest, with 70% of respondents expecting land to continue into early or late stable, and 75% foreseeing a significant or moderate increase in land prices over the next six to 12 months.

Most Modest: For-Sale Residential

The for-sale housing market has continued to recover, although at a more modest pace than many Americans were hoping for. In late 2012, for-sale residential was climbing its way out of the bottom, and has since moved quite significantly, with 60% of respondents currently placing the land use in early to late stable. With rising prices in many areas, resolving foreclosures, and investors buying up inventory, 90% of respondents believe that this modest growth and recovery is likely to continue. However, interest rates are one economic indicator to keep a close watch on, as 85% of respondents foresee modest-to-significant increases over the next six to 12 months, which could potentially adversely affect the expansion of the for-sale housing market.

Most Likely to Relocate (to Cyberspace): Retail

Respondents are showing signs of slowing optimism in the retail sector this quarter, as future expectations for the sector moved slightly backwards from 2Q 2013’s expectations. In addition, retail rents remain among respondents’ slowest-growing economic indicators in the past year. This outlook may reflect primarily the mediocre holiday shopping season, but more permanent changes in the retail industry could also be fueling the less-than-optimistic outlook on this land use.

When RCLCO asked how the growth of the internet and e-commerce would affect the demand for new retail development over the next five years, 53% of respondents reported a slight reduction (1%-9%), while another 30% reported a significant reduction (10%-19%). E-commerce is undoubtedly a growing industry, with just 0.6% of all retail sales being e-commerce in 1999, a percentage that has grown to nearly 6% today, according to U.S. Census Bureau. This growth in e-commerce will be fueled by the growth of Millennial spending power, as a DDB Worldwide survey recently found that those ages 18-34 were more likely than their older counterparts to engage in nearly every online shopping activity.

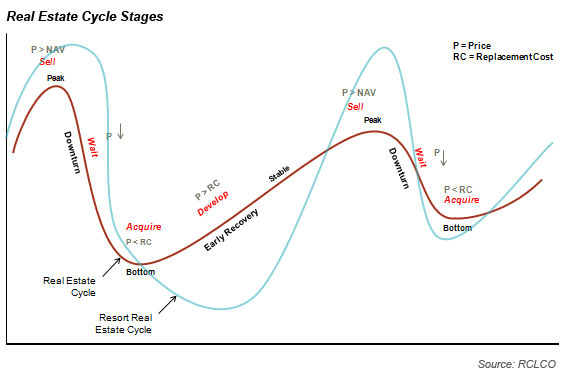

From top dogs to underdogs, expectations for 2014 remain generally positive, with every land use forecasted to be in the early or late stable stage of the cycle by 4Q 2014. This optimism is also reflected in expectations for various economic indicators, with modest increases expected in home values, land prices, institutional capital flows, hotel room rates, industrial rents, and, to a lesser extent, apartment, retail, and office rents. Steady, but moderating, optimism may serve as a reminder that real estate is one of the most cyclical industries in the economy. Choosing to plan and strategize for the unavoidable ups and downs of the real estate cycle will leave your company prepared and productive, like a dog with a bone.

1According to CoStar

Article and Research prepared by Len Bogorad, Managing Director, and Trish Kennelly, Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. RCLCO’s Strategic Planning and Litigation Support Advisory Group produced this newsletter. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/strategic-planning

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us