Who Should Control Rent Control? Impacts of Prop 10 and Interactive Tools to Better Understand Its Nuances in Various California Markets

This November, Californians will vote on Proposition 10, a ballot initiative that seeks to repeal the Costa Hawkins Rental Housing Act of 1995. If passed, it promises to have far-reaching impacts on California’s real estate markets and economy. Investors, legislators, and tenants anxiously await, fervently debating potential effects on rents and affordability, as well as housing supply and construction activity.

A repeal of Costa Hawkins would likely lead to tighter rent regulations, especially in cities that are already grappling with concerns regarding affordability and rental housing shortages. Stricter rent control laws would likely compound the imbalance between housing supply and demand, with developers challenged to achieve desired returns as projected revenue growth may be capped. While some tenants would benefit from being shielded against sudden and significant rent increases, many, especially those in lower income ranges, could struggle to secure housing as competition for limited housing intensifies. Meanwhile, the quality of rental stock may decrease as increased rent control disincentivizes landlords to reinvest in aging real estate. Lower rent growth for multifamily properties would lead to lower future income, repricing of existing assets and development sites, and reduced property taxes. Effects of Prop 10 may not be limited to the real estate industry; California’s labor economy could also suffer from reduced labor mobility and high competition for housing.

While there is a lot of uncertainty regarding the consequences of Prop 10, we have attempted to characterize ramifications for various players in detail below.

Introduction

Costa Hawkins Rental Housing Act of 1995

Costa Hawkins is a California state law that places the following limitations on local rent control laws:

- It excludes certain property types (single-family homes and condominiums) from the purview of municipal rent control ordinances.

- It restricts cities from imposing rent control on residences constructed after February 1, 1995. It also ordains that residences that were exempted from existing rent control policies at the time Costa Hawkins passed must remain exempt. For example, based on preexisting local rent control laws, buildings erected after 1978 in Los Angeles or after 1979 in San Francisco cannot be subject to rent control regulations.

- It prohibits “vacancy control,” thereby allowing landlords to bring rents in controlled units to market rates when they are vacated.

A repeal of Costa Hawkins would put the decision-making power for rent control regulations back in the hands of cities.

Summary of Current Rent Control in California

Currently, 15 cities in California have some form of rent control, capping annual rent increases on controlled units.[1] For example, in Los Angeles, the Rent Stabilization Ordinance (RSO) mandates a cap of 3% to 8% on rent increases (depending on yearly inflation) for units in buildings constructed before October 1978. Landlords in San Francisco (of units built before June 1979) and Santa Monica (of units built before April 1979) can raise rents by an annually determined percentage tied to inflation. A maximum annual rent increase of 5% is allowed in San Jose. San Diego, the second-largest city in California (by population), has no rent control laws.

If Prop 10 passes, local rent control laws will automatically revert to their original ordinances, unless new local measures are also approved. Various cities already have ballot measures to amend original laws—Berkeley, for example, has a measure that will exempt new construction from rent control for 20 years and also restore vacancy control. The City of Santa Monica also originally imposed vacancy control; if Prop 10 passes, it will automatically go back into effect.

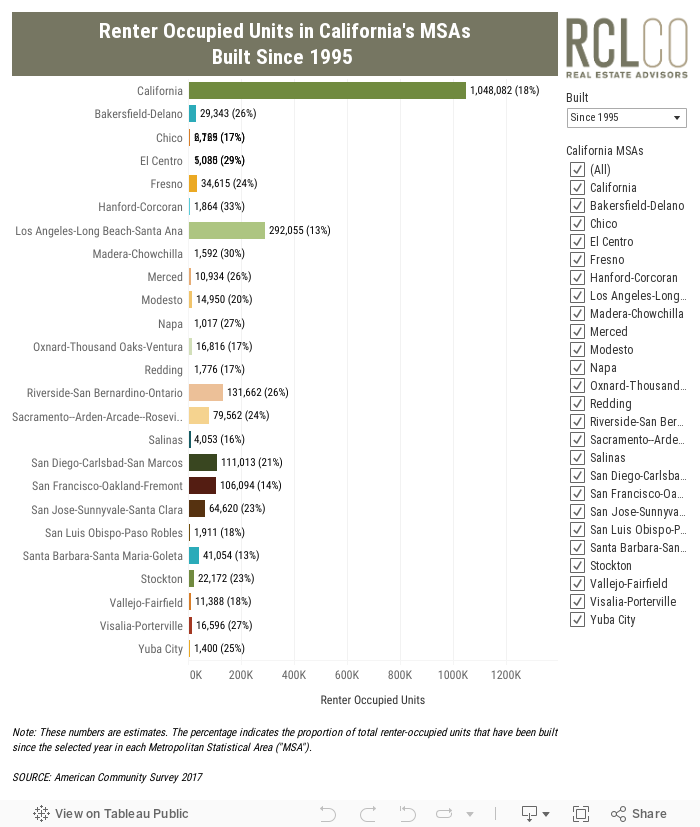

The interactive exhibit below provides an estimate of the number of multifamily units that could be affected by the expansion of rent control. If rental units built after 1995 are no longer exempt from rent control, over one million units in California not currently subject to rent control could be brought under its purview.

Potential Impacts of Rent Control

If Prop 10 were to pass, RCLCO expects most major California cities would evaluate changes to current rent control laws, likely leading to tighter regulations. Probable effects include:

1. Exacerbation of Supply Shortage

If new rent control laws were to apply to new construction, given lower projected rent increases, developers would achieve lower returns on their investments (unless initial rents are set higher than those in a market with less regulations), assuming construction costs remain constant. As a result, these new projects may not achieve required returns and therefore no longer be financially feasible. A recent study by a UC Berkeley economist discusses the adverse effect of rent control on new construction by presenting corroborative research, including a University of Toronto study that found that rent control resulted in a significant fall in new construction in Ontario.[2] The Legislative Analyst’s Office also stated that significant expansions of local rent control policies would prompt a substantial decrease in new construction.[3]

In addition, existing owners may be inclined to convert their rental properties to for-sale residential properties, or even other commercial buildings (if zoning laws allow). A recent Stanford study found that landlords in San Francisco impacted by a 1994 ballot initiative redeveloped their properties in ways that made them exempt from rent control policies (e.g., converting them to owner-occupied), decreasing regulated rental housing supply by 15%.[4]

Historically, building owners have found creative ways to evade rent control laws—converting controlled homes to short-term vacation rentals via Airbnb, for example—and will continue to do the same in order to achieve the highest returns from their investments. Recent years have also seen a marked increase in investment into single-family rentals, especially from institutional investors. Single-family homes are currently not subject to rent control regulations; however, if this were to change under a Costa Hawkins repeal, institutional investment into this property type could reverse course and these players could become net sellers of single-family homes in California.

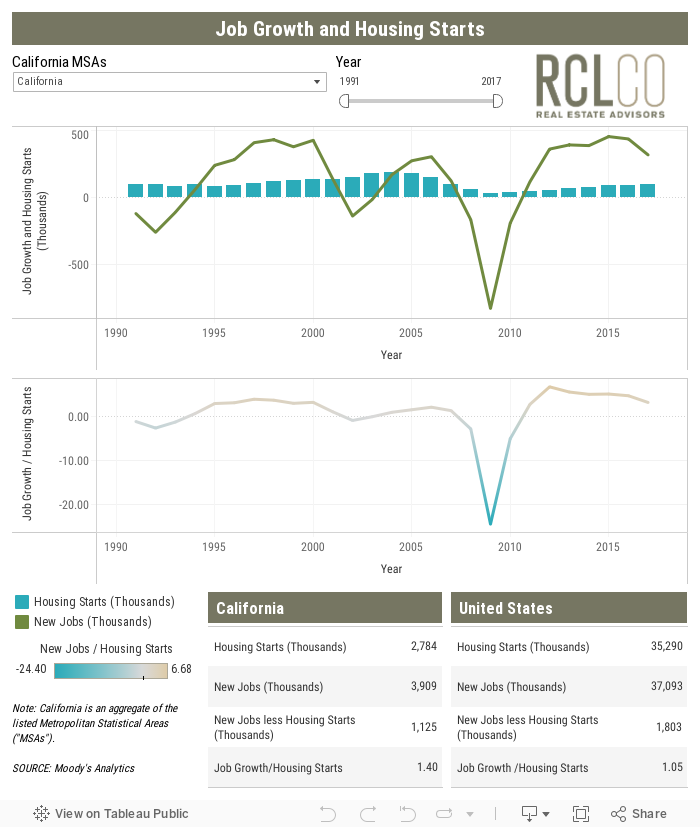

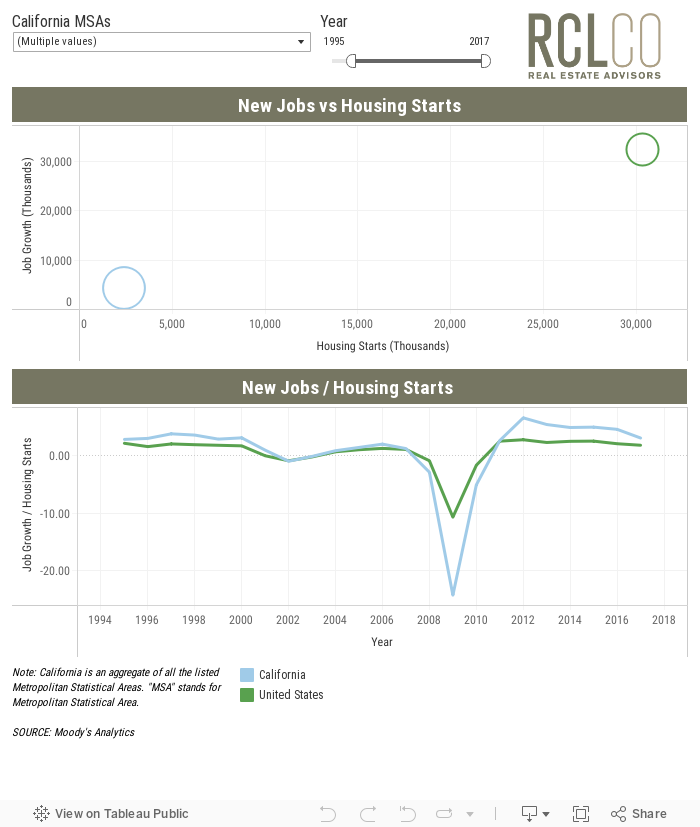

A decline in new construction and rise in conversions would worsen severe housing shortages already faced by many California cities. To demonstrate the imbalance between housing demand and supply, we have created the interactive dashboard below comparing economic growth (a primary driver of housing demand) to housing construction activity. These charts depict the relationships between job growth and housing starts in California’s Metropolitan Statistical Areas (“MSAs”). In many MSAs, and in California as a whole, the gap between new jobs and housing starts, representing a supply deficit, has widened over the past five years.

From 1991 to 2017, California MSAs added over 3.9 million jobs, but fewer than 2.8 million units started construction. California MSAs are responsible for 62% or 1.1 million of the U.S.’s 1.8 million housing start deficit relative to jobs.

2. Increased Competition for Housing and Increasing Affordability Gap

Increased rent restrictions will protect tenants in controlled units against rent surges, allowing numerous households to continue residing in their homes for longer than they could afford to otherwise. However, excess demand (due to supply shortages) would translate into increased competition for more limited housing, which could disproportionately harm lower-income households. Increased competition would grant landlords the power to select tenants from large demand pools, and they are likely to choose tenants that are financially better off.

It’s unlikely all rental units will be rent controlled (e.g., some think new construction will be excluded, at least for some period of time). Such non-controlled units would likely experience greater annual rent increases as markets become increasingly supply-constrained. Given excess demand, these units would likely be absorbed, but by higher-income households. This would widen the disparity in living conditions across households with different incomes. This is especially true considering that the stagnation in rents in rent-controlled units would be reflected in the reduced quality of housing, as restricted rent increases would limit, if not eliminate, the incentive for landlords to invest, and even maintain, their properties. Property managers devote funds to renovations and upkeep in order to remain competitive—but given the abundance of prospective renters relative to supply, this may no longer be necessary or prioritized.

3. Uncertain Impact on Homeownership

In view of the potential increase in for-sale housing offerings, home prices may dip, and more households could have the opportunity to purchase a home.[4] However, considering that rent growth would be constrained and home prices in California are already quite high, it is unclear if renters in rent-controlled units would transition to ownership housing as renting remains attractive at the controlled rent levels.

4. Changing Property Values and Repricing of Development Sites

Investors who increasingly view rent controlled apartments as bond-like assets, given high occupancy and stable cash flows, could assume more aggressive—i.e., lower—cap rates, resulting in higher asset values. Alternatively, investors who seek the opportunity to reposition rent controlled apartments and increase rents as units are vacated may perceive increased risk due to uncertainty surrounding vacancy control, and therefore underwrite to higher cap rates, leading to lower asset values. Long-term, all other things being equal, lower growth in net operating income would lead to lower increases in property values.

If new rent control laws were to apply to new construction, values for development sites may also decline. For new developments to achieve target returns, lower rent growth projections would have to be offset either by higher initial rents, or lower development costs (construction plus land). As construction costs are unlikely to decrease, land prices would have to adjust. Sites that cannot support other commercial uses would be discounted more than those that can, but most development sites would lose some value due to lower overall demand for rental residential development.

5. Uncertain Effect on Transaction Activity

There is a good chance many owners may be inclined to sell their properties—considering rising interest rates and rent regulations, property values would be expected to have peaked. On the flip side, buyers, underwriting lower rent growth and smaller capital gains, may be unwilling to purchase properties at their peak values. Depending on the magnitude of discounts that both buyers and sellers are willing to accept, transaction activity may spike or drop in the near-term.

6. Uncertain Economic Impact, Most Likely Negative

A lower housing burden for many would raise disposable incomes for renter households in controlled units, and lead to increases in consumer spending in the economy. At the same time, reduced construction activity and lower taxes could stifle business and government expenditures. Slower net operating income growth would lead to slower increases in property values, and consequently lower growth in property tax payments in the future. According to the Legislative Analyst’s Office, the success of Prop 10 could lead to a reduction of tens of millions of dollars in state and local revenues per year due to decreased property tax revenues and increased regulatory costs.[5] The economy may also be adversely affected by reduced mobility of tenants, who may decline new jobs opportunities in other regions in order to maintain a grasp on their scarce rent-controlled residences in supply-constrained markets.[4] Furthermore, employers in California may find it increasingly difficult to attract talent given the increased competition for rental housing, which could lead to slower employment growth.

Rent control is undoubtedly a hot topic as the November 6th election approaches. It remains to be seen how each of California’s cities would change their rent control laws, but the effects could be extreme on all involved.

References

[1] Alameda, Berkeley, Beverly Hills, East Palo Alto, Hayward, Los Angeles, Los Gatos, Mountain View, Oakland, Palm Springs, Richmond, San Francisco, San Jose, Santa Monica, and West Hollywood.

[2] Kenneth Rosen. “The Case for Preserving Costa-Hawkins: Three Ways Rent Control Reduces the Supply of Rental Housing.” Fisher Center for Real Estate and Urban Economics, 2018.

[3] Mac Taylor. Review of Proposed Statutory Initiative Pertaining to Rent Control (presented to the Attorney General, Pursuant to Elections Code Section 9005). Legislative Analyst’s Office, 2017.

[4] Rebecca Diamond, Timothy Mcquade, and Franklin Qian. “The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco.” National Bureau of Economic Research, 2018.

[5] California Secretary of State. “Prop 10 Expands Local Governments’ Authority to Enact Rent Control on Residential Property. Initiative Statute.” Official Voter Guide, 2018.

Article and research prepared by Derek Wyatt, Principal; Sara Crockett, Vice President; and Suveda Dhoot, Analyst.

RCLCO’s mission is to help clients make strategic, effective, and enduring decisions about real estate. We proudly celebrate more than 50 years of providing the best minds in real estate with cutting-edge analytics, actionable advice, and the highest level of customer service. Our work includes market, economic, financial, and impact analyses; investment portfolio strategy and implementation; entity-level strategic planning; and management consulting.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us