Looking Beyond the Luxury Market – Are Homebuilders Building More for You and Me?

Building for the Top

Is the entry-level home a thing of the past? It has largely appeared that way throughout much of the post-recession period, as homebuilders have disproportionately targeted the luxury market through larger and more expensive offerings. Stricter mortgage financing standards have impeded the ability of entry-level buyers to qualify, pushing builders toward upper market segments with the least credit risk. Moreover, low levels of lot availability, rising labor costs, and increased regulatory burdens have amplified the appeal of lower-volume, higher-margin new housing options.

As the recovery endures, however, market-depth limits for luxury new housing segments are beginning to emerge. A recent Redfin analysis found luxury home prices rose by 0.7% in 4Q 2016 year-over-year, compared with 6.1% price growth for non-luxury properties, which marked the eighth consecutive quarter the segment has underperformed relative to the rest of the market.[1] With this recent softening at the top of the market, are builders beginning to expand their appeal to broader market segments?

Where to Next? A Primer on Missing Middle Demand

As RCLCO has previously reported, there is a growing mismatch between buyer preferences and available new home supply. American homebuyers overall continue to prefer larger homes than those they currently occupy. However, the emerging demographic evolution of the two largest demographic cohorts—with millennials increasingly aging into prime family formation years and baby boomers becoming empty nesters—suggests trending consumer preferences toward more midscale and mid-priced, or “missing middle,” product. Both groups are more amenable to smaller floor plans, primarily due to price point or lifestyle considerations, respectively.

Post-recession, younger buyer segments have largely been on the sideline of the for-sale housing market recovery. First-time homebuyers’ share of the overall housing market remained low at 35% in 2016, which while up from 32% in 2015, was well below the historical average of 40% market share and especially significant given younger households’ relatively high current share of the U.S. household base.[2] This low share is not entirely attributable to changing consumer preferences toward rentership, as 70% of millennials still expect to become homeowners by 2020.[3] Moreover, 55% of non-owners cited “can’t afford to buy a home” as the main reason they are not currently homeowners, compared with 31% attributing their rentership to life stage or consumer preference factors.[4] Though millennials prefer larger homes than they currently occupy, 2,375 square feet versus an existing median of 1,705 square feet, affordability considerations suggest that smaller floor plans at more attainable price points are the only option for many of those seeking to enter the for-sale market.

Older generations are rapidly transitioning into later life stages as well, where both the absence of children at home and lower appetite for household maintenance reduce the appeal of larger homes. Baby boomer (1946-1964) and senior (pre-1946) buyers, who are typically in the best financial position to afford new housing, desire smaller floorplans with medians of 1,879 square feet and 1,791 square feet, respectively, to accommodate their changing lifestyles.[5] Among likely movers, 73% of baby boomers and 83% of seniors are seeking either the same size or smaller floor plans, creating a market opportunity for higher-quality, smaller-format new construction.[6]

New Product Increasingly Targeting the Middle of the Market

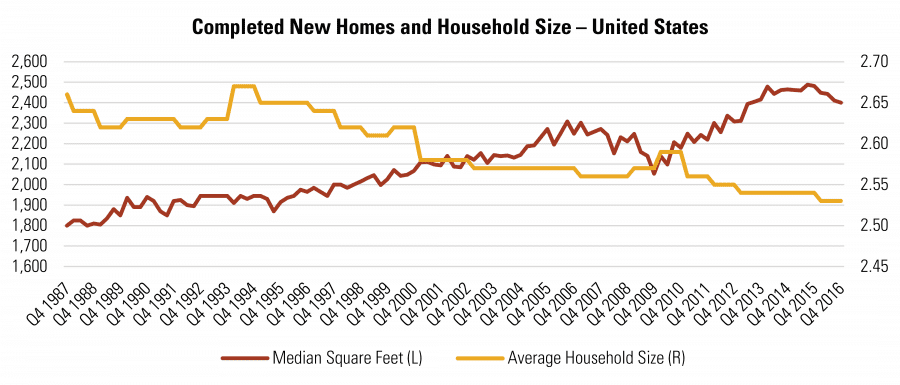

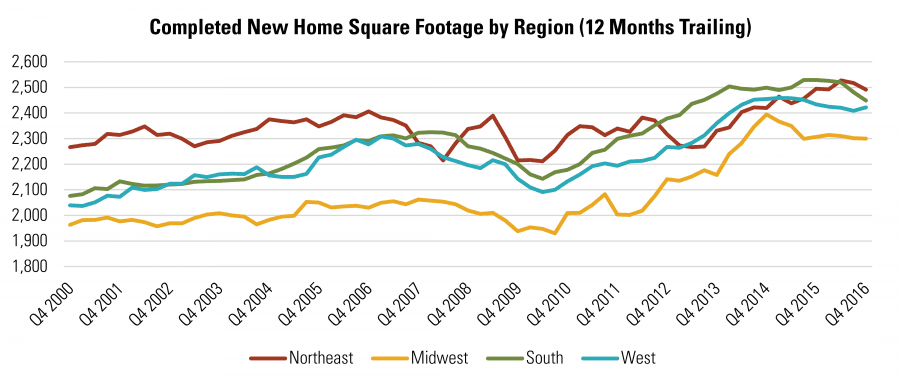

The past few decades have been characterized by increasingly larger homes—with the only exception occurring between 2008 and 2010 due to economic uncertainty and a first-time homebuyer tax credit incentivizing entry-level homes—while average household sizes have dropped to historical lows. With a softening luxury home segment, alongside the rising influence of entry-level millennials and downsizing baby boomers, homebuilders are beginning to shift their approach in order to expand market appeal. After largely plateauing throughout 2014 and 2015, with a Q3 2015 peak of 2,488 square feet, median new home sizes have begun to gradually decline over the past year to 2,400 square feet in Q4 2016. This moderate shrinkage trend is largely consistent across each geographical region for which data is available, suggesting this phenomenon has broad geographical traction.

SOURCE: U.S. Census Survey of Construction; Current Population Survey

SOURCE: U.S. Census Survey of Construction

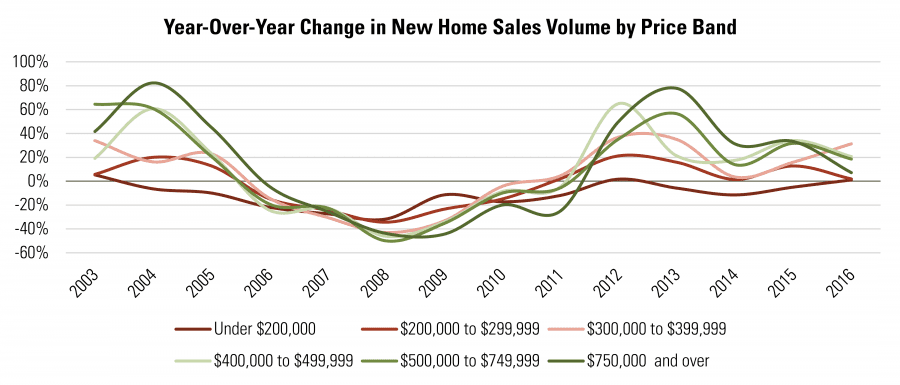

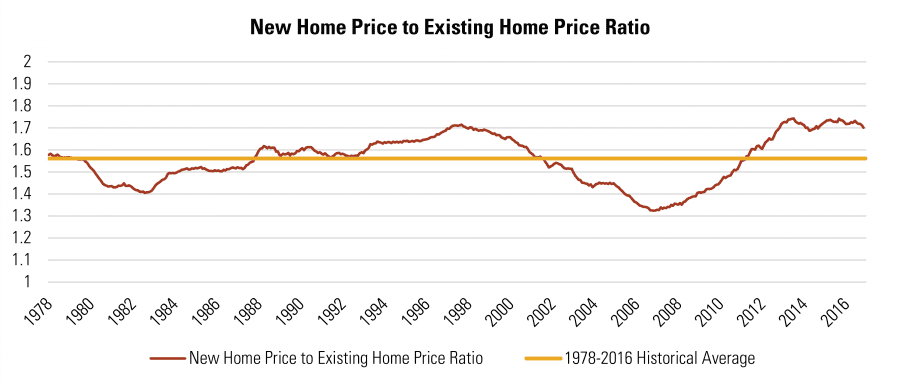

With new home sizes declining moderately, the increase in average new home price slowed to 3.4% in 2016, the lowest annual increase since 2011. Throughout much of the recovery, high-priced product fueled the new home market, with annual sales volume increases generally above 20% year-over-year. However, the upper end of the market has slowed significantly over the past year, with an especially precipitous drop-off in sales volume growth in the $750,000+ price band. Conversely, accelerating sales growth within the more moderately priced $300,000 to $400,000 band has propelled the new home market forward by creating more attainable options for prospective homebuyers. Moreover, the ratio of new home prices to existing home prices also registered a modest decline over the past year, suggesting new home product is becoming slightly more attainable relative to existing homes, even though this ratio remains near historical highs.

SOURCE: U.S. Census Survey of Construction

SOURCE: U.S. Census Survey of Construction, Case-Shiller Home Price Index

Will the Trend Continue?

As the luxury market shows signs of softening, homebuilders are beginning to adapt to changing demographic conditions by constructing more moderately priced and sized new home product. Though underlying constraints, such as strict mortgage financing standards and escalating costs, remain largely unchanged from the beginning of the recovery, strengthening demand drivers from the aging of millennials and baby boomers, along with rising household incomes for average Americans, have increased the relative appeal of “missing middle” product options for builders. These more moderately priced for-sale product options will become increasingly important to the extent rising interest rates further erode affordability. Though yielding lower per-home margins, savvy builders and developers are recognizing the positive bottom-line benefits of higher-velocity, higher-density development strategies.

References

[1] Phil Banker, “Luxury Homes Outpaced by Rest of Market,” MReport, January 25, 2017, accessed February 08, 2017, http://www.themreport.com/news/01-25-2017/luxury-homes-outpaced-rest-market.

[2] National Association of Realtors, 2016 Profile of Home Buyers and Sellers, Chicago: NAR, 2016, https://www.nar.realtor/sites/default/files/reports/2016/2016-profile-of-home-buyers-and-sellers-10-31-2016.pdf.

[3] M. Leanne Lachman and Deborah L. Brett, Gen Y and Housing, Washington, DC: ULI, 2015, http://uli.org/wp-content/uploads/ULI-Documents/Gen-Y-and-Housing.pdf.

[4] National Association of Realtors, Aspiring Home Buyers Profile, Chicago: NAR, 2017, https://www.nar.realtor/sites/default/files/reports/2017/2017-aspiring-home-buyers-profile-02-01-2017.pdf. 2017 Aspiring Home Buyers Profile survey includes all age groups, but 59% of non-owners are aged 34 and under.

[5] Rose Quint, Housing Preferences Across Generations, Washington, DC: NAHB, 2016, http://www.nahbclassic.org/generic.aspx?sectionID=734&genericContentID=249797&channelID=311&_ga=1.135937459.347344660.1485838344.

[6] Urban Land Institute, America in 2015: A ULI Survey of Views on Housing, Transportation, and Community, Washington, DC: ULI, 2015, http://uli.org/wp-content/uploads/ULI-Documents/America-in-2015.pdf.

Article and research prepared by Sara Kramer, Vice President, and Mark Trainer, Senior Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us