RCLCO’s Mid-Year 2018 Sentiment Survey Results – Optimism Pulls Back Slightly

In This Report:

- The RCLCO Real Estate Market Sentiment Index (RMI) has decreased modestly since year-end 2017, as respondents predicted six months ago.

- Looking ahead, real estate is expected to experience moderately declining market conditions over the next 12 months; however, the RMI is expected to remain above 50, indicating fairly healthy market conditions.

- Modest increases in interest rates are expected to have minimal to moderate impact on real estate markets, skewing slightly to worse overall market conditions.

- Just over two-thirds of survey respondents now expect the next real estate downturn to be in 2020 or later, including one-fourth of respondents who expect the next downturn to be in 2021 or later, which puts the next cyclical peak significantly later than in previous surveys.

- While most product types exhibited little cycle movement since six months ago, remaining in the stable phases of the real estate cycle, several product types moved definitively into the late stable phase of the real estate cycle.

- RCLCO’s outlook for generally positive, though moderating, operating and investment performance through the remainder of 2018 is consistent with the majority of survey respondents.

Over the past few years, RCLCO sentiment surveys have indicated continued confidence in the current real estate market, stabilizing from a sharp decline to lower levels in the run-up to and after the June 2016 Brexit vote and a weakening stock market in early 2016. Sentiment reversed direction—turning positive—in the wake of the unanticipated outcome of the 2016 U.S. presidential election with the promise of a GOP-controlled Congress that would promote business-friendly policies that many believed would serve to continue the expansion of the U.S. economy. Respondents have remained positive since the 2016 U.S. presidential election, and the passing of the “Tax Cut and Jobs Act” (TCJA) in late 2017 pushed sentiments to levels not seen since the year-end 2015 survey. As the excitement of the tax overhaul appears to have diminished, perhaps because of concern about the impact of the massive spending increases enacted in March 2018, sentiment has resumed its downward trend at a pace similar to before the passing of the TCJA. Respondents believe that the expansion will begin to slow, as evidenced by a less positive outlook for the next 12 months than in the previous survey. Nevertheless, respondents continue to push out the next downturn farther into the future, with the largest number of respondents expecting the downturn to begin in 2020 despite most respondents believing that a majority of the real estate sectors are firmly in the “late stable” stage of the cycle.

With the 10-year U.S. Treasury yield recently breaking the 3% threshold for the first time since 2013, the impact of rising interest rates on U.S. real estate markets is a key focus of this survey.

Overall Sentiment Is Down Slightly, Returning to the Same Level as One Year Ago

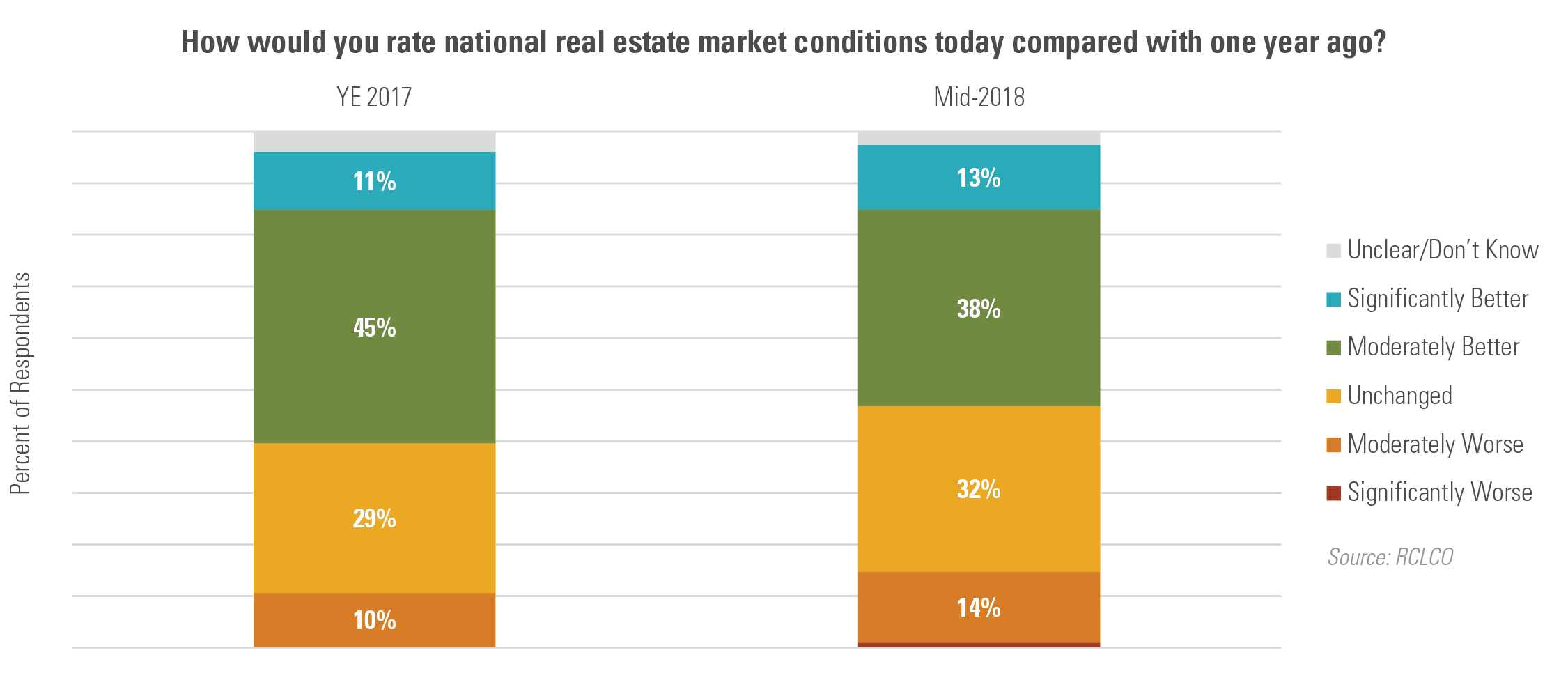

Sentiments about current national real estate conditions remain at a relatively high level, and slightly below where they were six months ago. Just over one-half (51%) of survey respondents say national real estate market conditions are moderately or significantly better today than they were 12 months ago. This is five percentage points lower than in the year-end 2017 survey and one percentage point lower than in the midyear 2017 survey. The share of respondents reporting worse market conditions today than one year ago remains a small but increasing minority (14%), four percentage points higher than in the year-end 2017 survey.

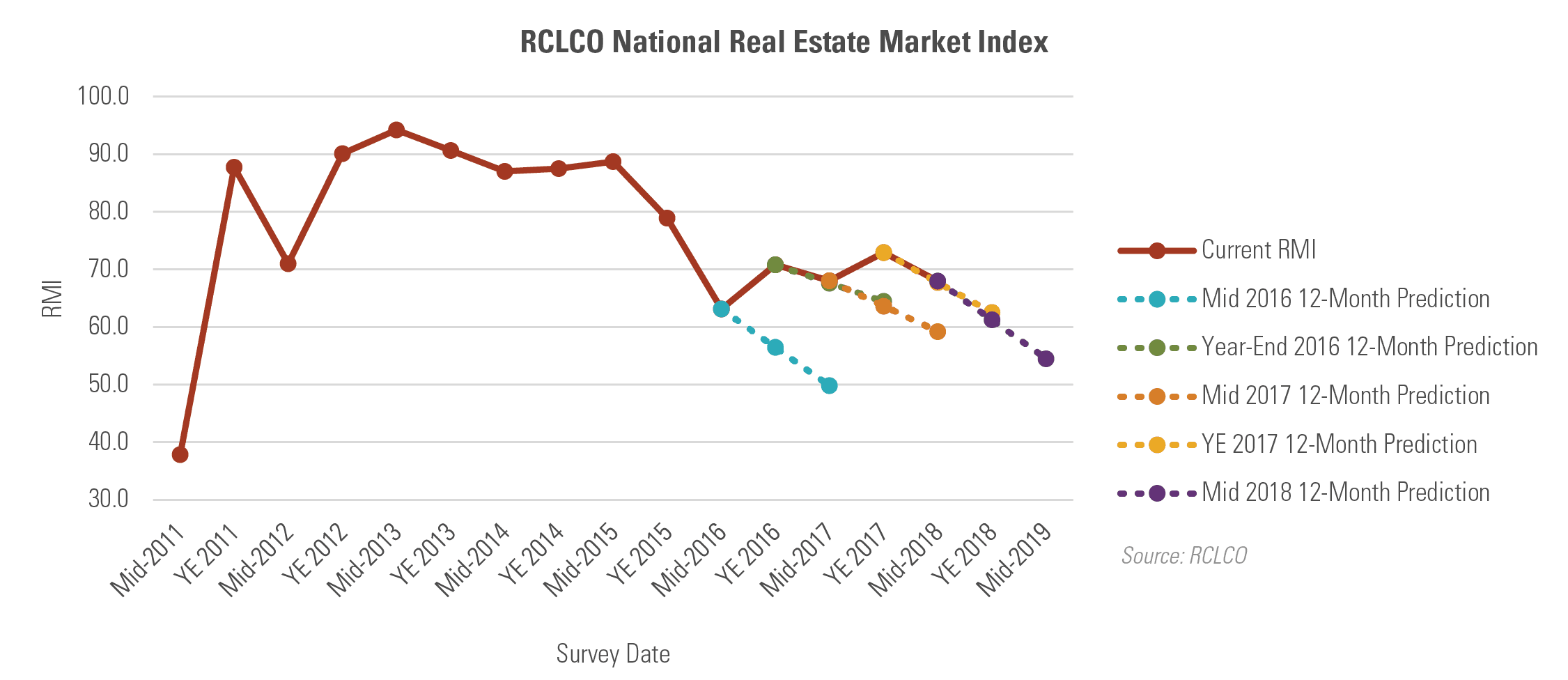

This decrease in sentiment is reflected in RCLCO’s Real Estate Market Index (RMI),[1] which measures sentiment on a 100-point scale. The RMI decreased to 68.0 in this survey, which is 4.9 points below where it was six months ago. This increase was anticipated by respondents in the year-end 2017 survey, who predicted the RMI to be 67.7 at midyear 2018. Respondents in the midyear 2017 survey, who did not anticipate the increase in RMI in year-end 2017, anticipated the current RMI to be 59.2 at midyear 2018, well below the current RMI indicated by midyear 2018 respondents. Respondents expect sentiment to continue to decline to the mid-50s within the next 6-12 months.

Since the abrupt decline in midyear 2016, sentiment has broken its downward trend. Current sentiment is lower than it was six months ago, in line with expectations of the year-end 2017 respondents. With RMI stabilizing in the range of 68 to 73 over the past two years, real estate markets continue to experience very good market conditions that are indicative of the mature phase of the current real estate cycle.

Sentiment reached its lowest point since midyear 2011 in midyear 2016, with the RMI falling sharply from 78.9 in the year-end 2015 survey to 63.1 in midyear 2016. The decrease in sentiment was reflective of respondents’ unease about the future due to the Brexit vote, declining oil prices, and a struggling stock market. This unease resulted in 80% of respondents anticipating the next recession to start in 2018 or sooner and an expectation from respondents that RMI would continue to trend downward to the low-50s within 12 months.

Year-end 2016 respondents exhibited increased optimism for the health of real estate markets, which was largely attributed at that time to the anticipated positive impacts of the newly elected president, with the support of a Republican Congress. By midyear 2017, current sentiment remained close to its year-end 2016 level, but only a third of respondents still expected President Trump to have a positive impact over the next 12 months. With the business-friendly TCJA passing in late 2017, sentiment once again jumped to an unanticipated recent high of 72.9. Despite the brief uptick in sentiment, it appears that the TCJA only temporarily lifted sentiment as both current and predicted future sentiment point towards a resumed downward trend in the RMI.

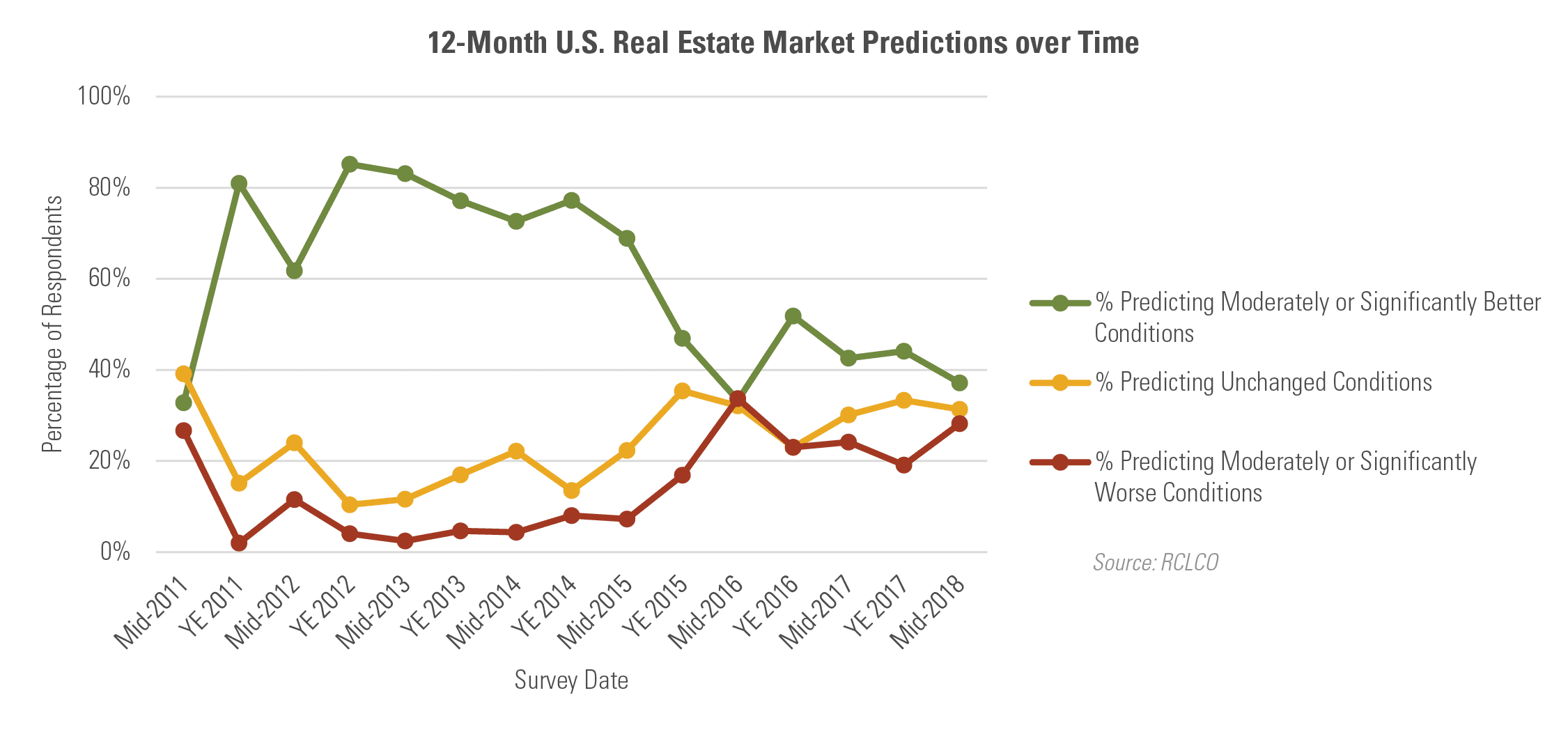

While sentiments remained relatively stable from the year-end 2016 survey to the year-end 2017 survey, sentiments declined in the midyear 2018 survey, beginning to resemble the future sentiments of respondents in the midyear 2016 survey: 37% of respondents expect real estate market conditions to improve over the next 12 months, which is below 44% of respondents six months ago and in line with the 33% of respondents in the midyear 2016 survey. The percentage of respondents anticipating worse conditions within the next 12 months is significantly higher in this survey (28%) than in the previous survey (19%), albeit materially lower than in the midyear 2016 survey (34%). The proportion of respondents expecting unchanged real estate market conditions has remained stable, with 31% of respondents predicting unchanged conditions in the midyear 2018 survey, slightly below the 33% in the year-end 2017 survey.

Rising Interest Rates Not Anticipated to Significantly Impact Economic Indicators

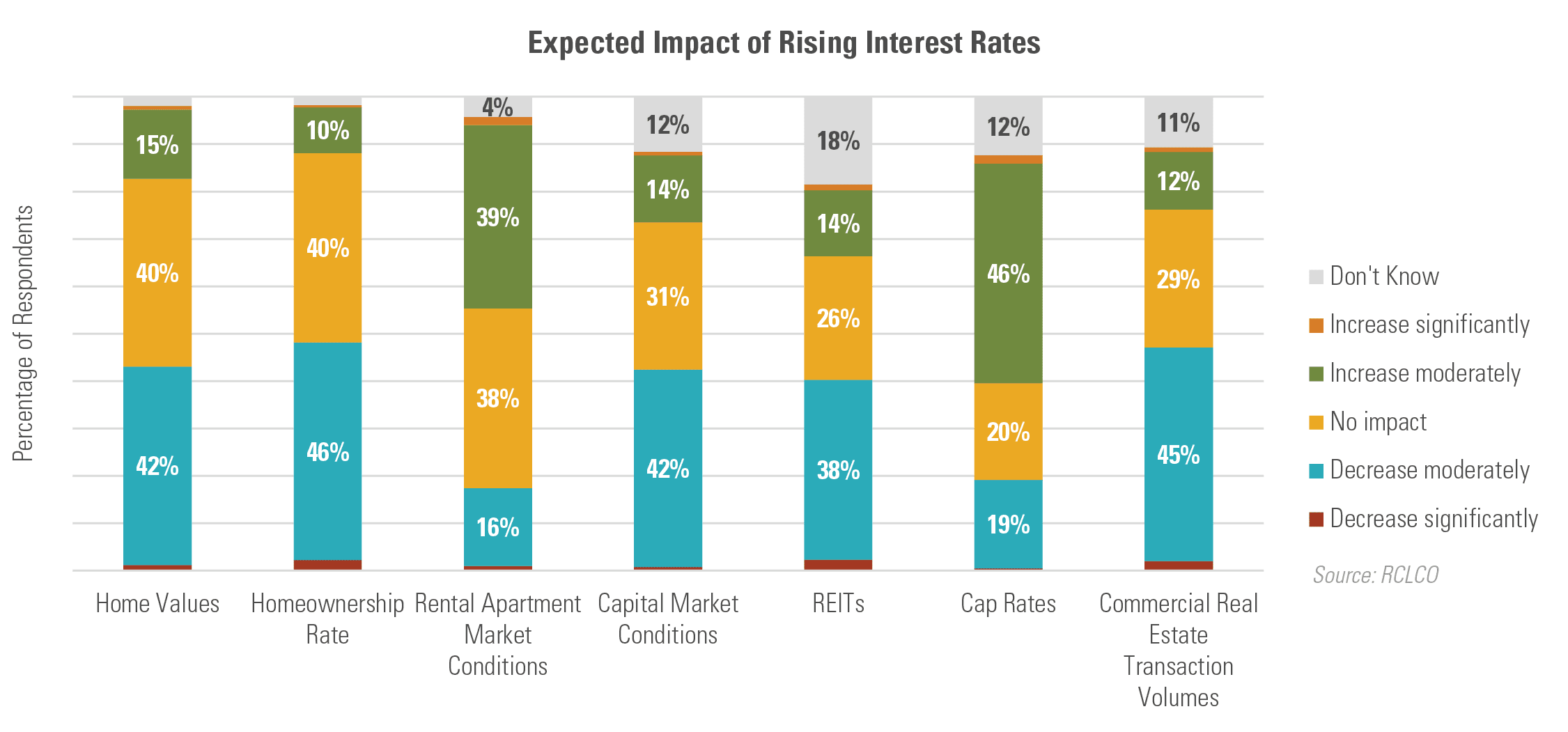

Since the Great Recession in 2008, the Federal Reserve has kept interest rates low in an effort to stimulate continued economic growth. With the 10-year U.S. Treasury rate breaking 3% earlier this year in April for the first time since 2013, it is natural to wonder if the low interest rate environment in which we have been operating since the Great Recession is coming to an end. Respondents to the midyear 2018 RCLCO survey were asked what impact rising interest rates would have on various real estate indicators and market conditions. The consensus is that moderate increases in interest rates will not greatly affect the overall real estate market. As illustrated in the chart below, very few respondents believe that rising interest rates will have a significant impact on any of the economic indicators, with most believing that rising interest rates will have no impact or a moderate impact on economic indicators.

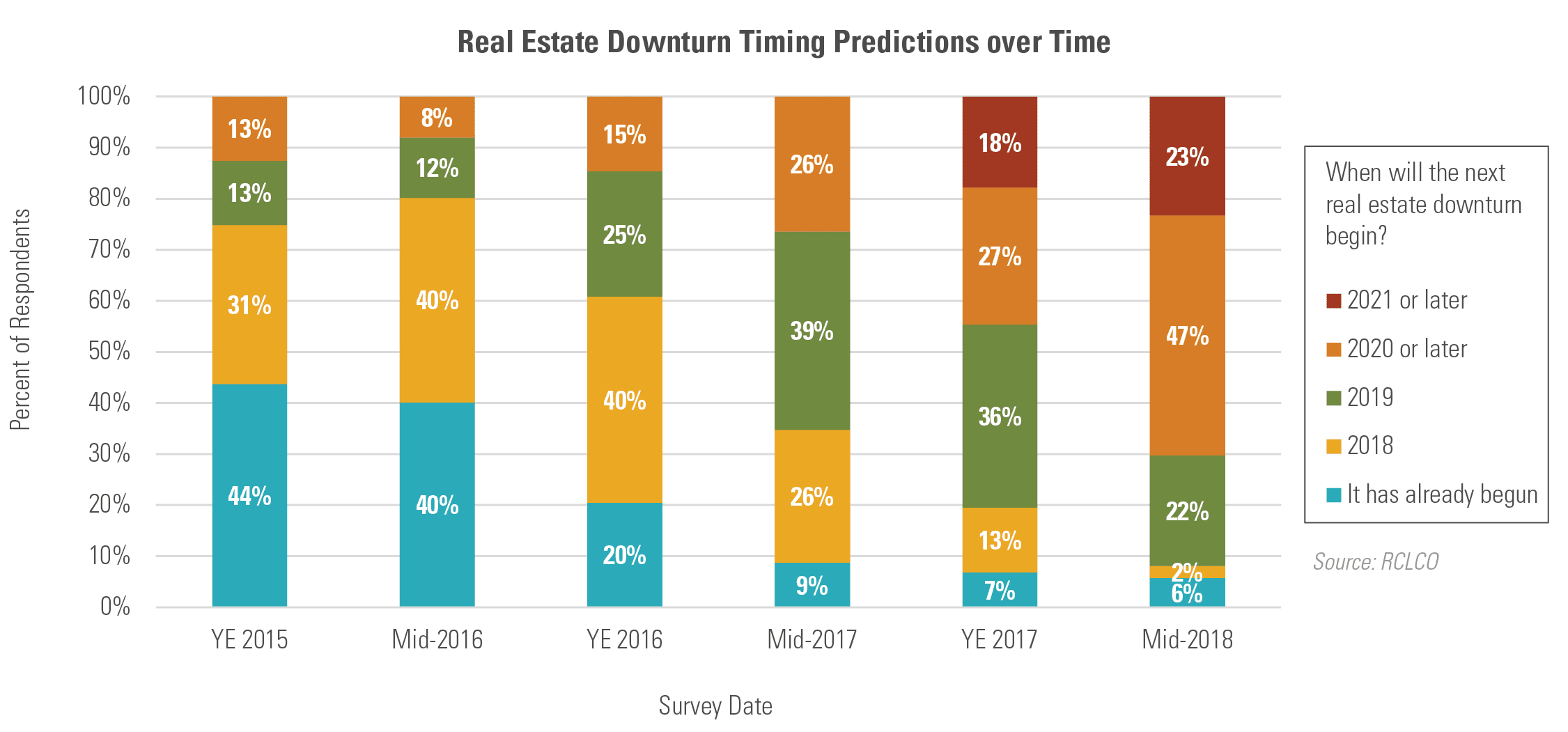

Respondents Continue to Push Real Estate Downturn Expectations Further into the Future

Over two-thirds of midyear 2018 respondents (70%) believe that the downturn will not begin until 2020 or later,[2] a substantial increase from the 45% in the last survey. Moreover, nearly half of the midyear 2018 respondents believe that the downturn will begin in 2020, an increase of 20% from the last survey. Significantly fewer respondents in the midyear 2018 survey compared to the last survey believe that the next downturn will begin in 2019 (22% and 36%, respectively). Fewer than 10% of respondents believe the downturn has already begun. As has been the case in previous surveys, respondents continue to push the anticipated downturn farther into the future.

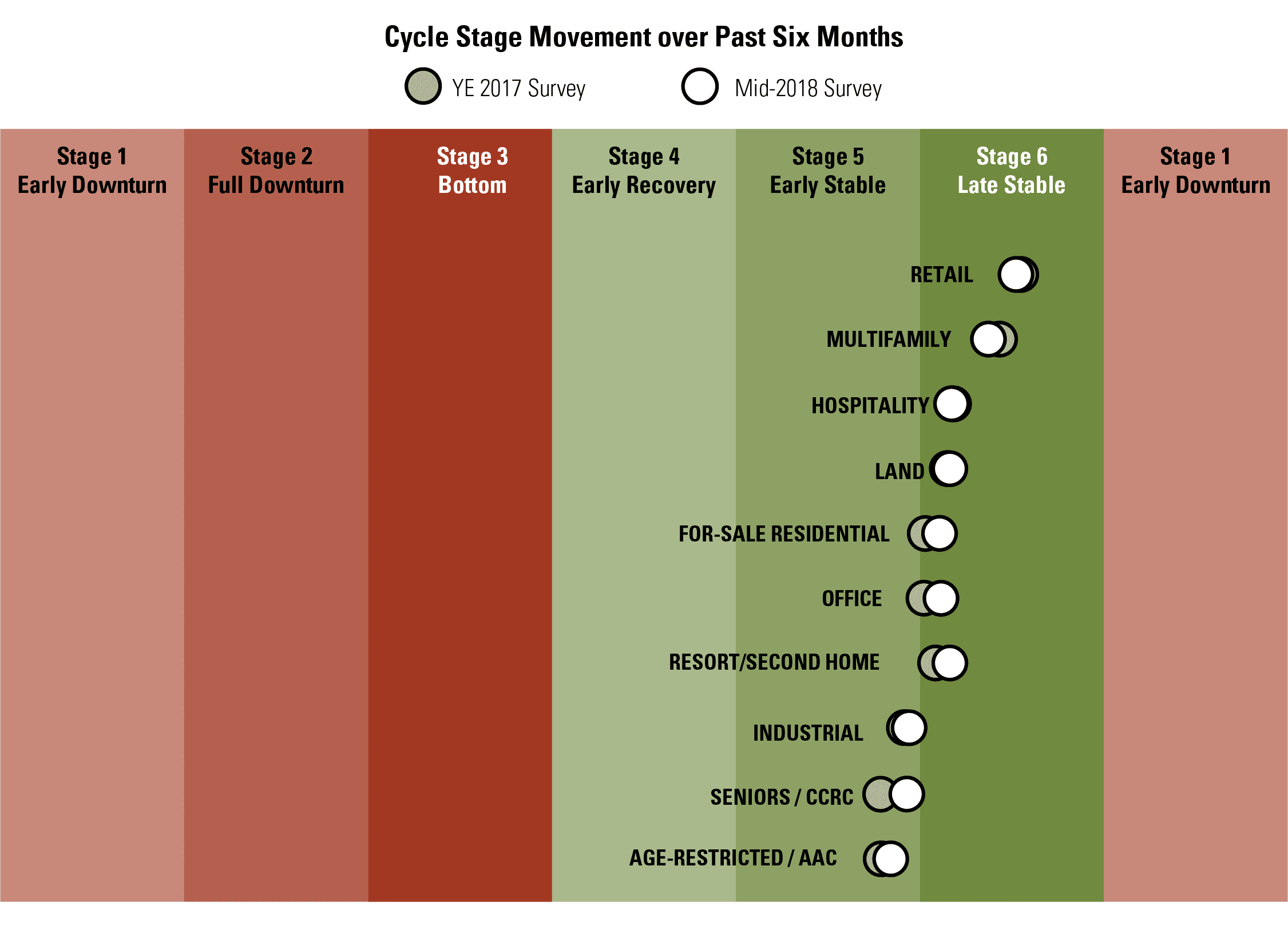

Marginal Cycle Movement for a Majority of Product Types over the Past Six Months

Respondents report slight cycle movement for most product types over the past six months, with all products either in or creeping towards the late stable phase of the real estate cycle, consistent with the slight decline in sentiment since RCLCO’s year-end 2017 survey.

In this survey, for-sale residential, office, and resort/second home product types all moved definitively into the late stable phase, with seniors and age-restricted land uses continuing to creep closer to this phase. Hospitality, land, and industrial exhibited almost no cycle movement. Notably, both retail and multifamily moved “backwards,” albeit slightly, in the cycle during the midyear 2018 survey, reinforcing the notion that there has been little change since the last survey.

“Late Stable” Phase Anticipated for All Land Uses in 12 Months

Despite minimal cycle movement across all land uses, respondents believe that all land uses will be firmly in the late stable phase within the next 12 months. Retail and multifamily are expected to be the farthest along, sitting at the top of the cycle and approaching the early downturn phase. Following closely behind retail and multifamily, land, hospitality, for-sale residential, office, and resort/second home are also expected to move farther along in the late stable stage.

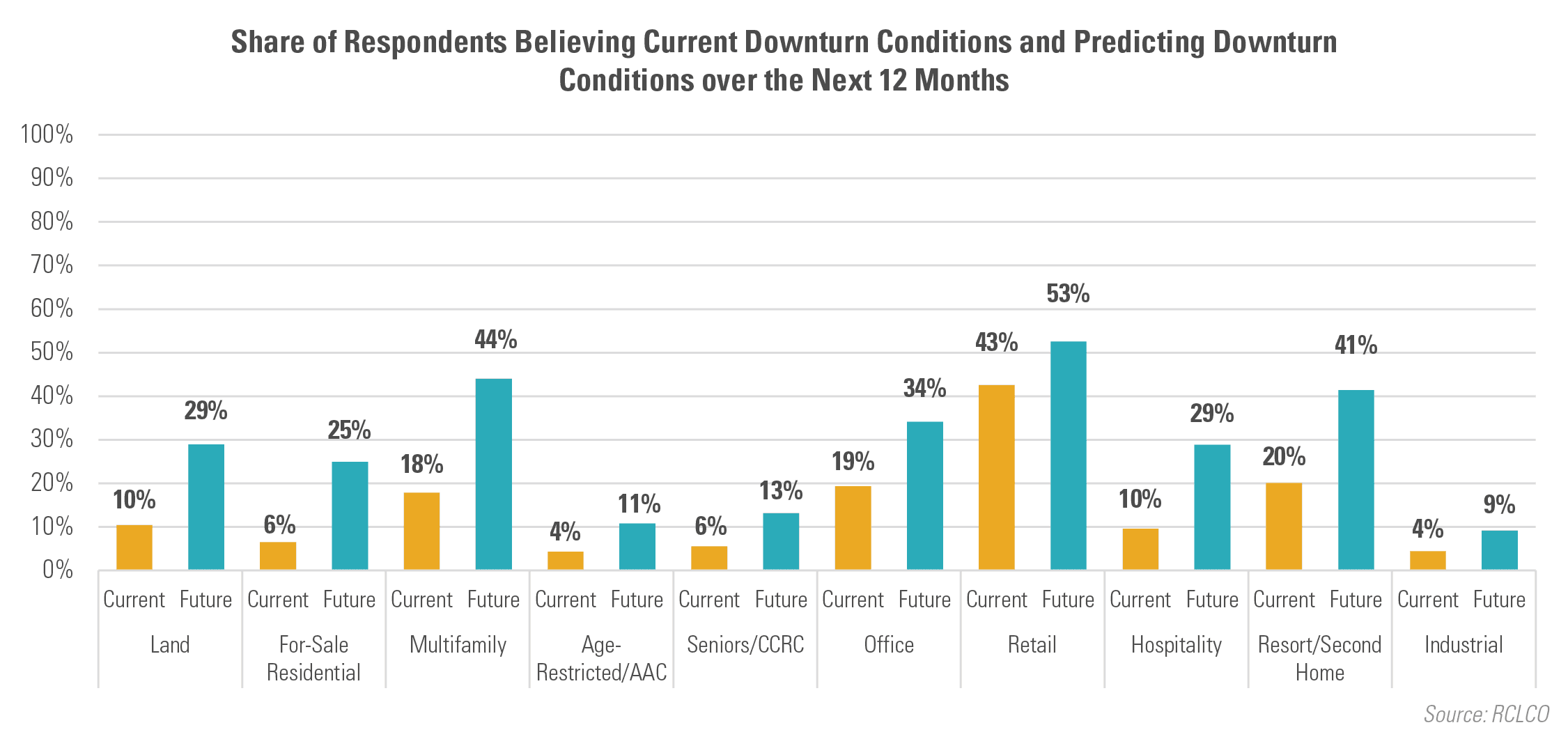

Share of Respondents Believing Current Downturn Conditions and Predicting Downturn in Next 12 Months Increases among Certain Land Uses and Decreases among Others

While most respondents do not believe that product types are already in downturn phases of the cycle, the notable exception continues to be retail, which 43% of respondents believe is currently experiencing downturn conditions, albeit slightly less than the 47% of respondents in the last survey. Roughly one-fifth of respondents, compared with one-fourth in the last survey, believe that resort/second home (20% vs. 24%), office (19% vs. 26%), and multifamily (18% vs. 20%) have already reached downturn. Despite fewer respondents believing that these land uses are in the downturn phases of the cycle, overall sentiment is down by 4.9 points according to the RMI.

In one year, 53% of respondents expect retail to be in downturn (a decrease of 4 percentage points), and 44% expect multifamily to be in downturn (an increase of 1 percentage point). Since the last survey, for-sale residential experienced the largest increase in those predicting downturn conditions, with 25% of respondents predicting downturn phases of the cycle in the next 12 months compared with 20% in the last survey.

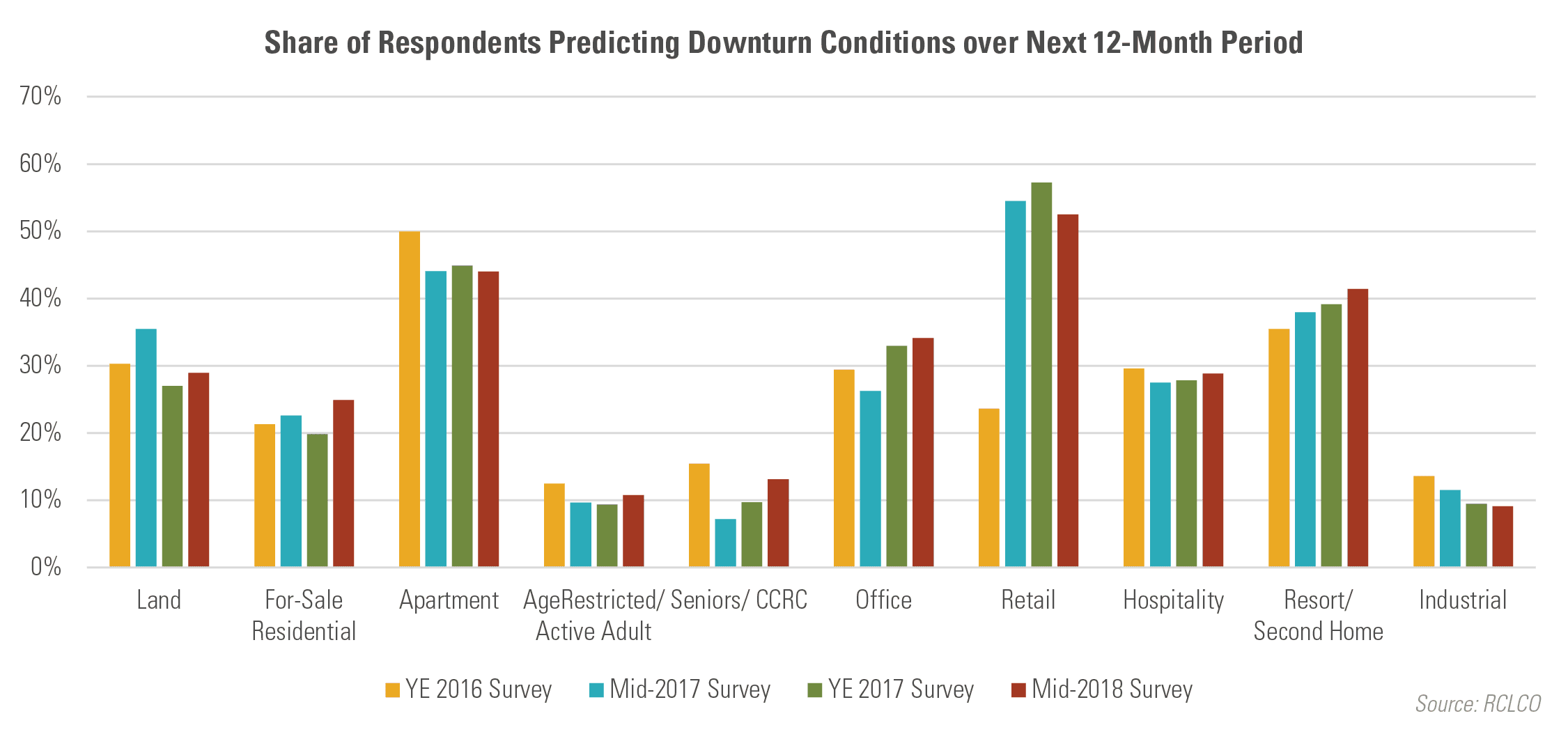

Consistent with respondents to the last survey, optimism for most product types is in line with where it was six months ago, with no land uses experiencing a significant increase in the share of respondents predicting a downturn over the next 12 months. Furthermore, three out of the 10 land uses—apartment, retail, and industrial—experienced a decrease in the share of respondents predicting downturn conditions 12 months in the future. For-sale residential experienced an increase in the share of respondents predicting downturn conditions 12 months in the future, which is a reversal of the decline in respondents predicting downturn conditions in the last survey. RCLCO believes that the change in sentiment could potentially be attributed to the higher costs of home ownership as a result of the tax overhaul and anticipated higher mortgage rates.

The RCLCO Point of View

As we stated six months ago, real estate continues to be in a “late stable” stage of the market cycle for most property types in most geographies. Supply is a concern in some markets and some property types, but not as much as in previous cycles. Interest rate and cap rate increases raise potential risks, but our “base case” doesn’t anticipate significant spikes in either. Moderating operating performance and flattening/increasing cap rates make it increasingly difficult to coast toward sufficient returns, necessitating a focus on market and operating fundamentals. This is particularly important as we reach full employment, which will tighten labor markets for all aspects of the real estate business (from construction to maintenance and other service roles) and place pressure on profitability.

Looking at specific product types, rental apartments, CBD office, and hospitality investments continue to hover around “peak” conditions, while other property types continue their steady marches toward maturity at varying paces. Only retail is following a unique trajectory given changing consumer behavior and preferences and the impacts of e-commerce.

Economists, as do our survey respondents, identify 2020 as the most likely timing for the next recession, if only because they can’t identify any trend or event in the near term that would disrupt current positive trends sooner. While the yield curve is not completely flat, it would be prudent to monitor as it has been one of the most reliable predictors of recessions. Historically, when the yield curve is flat, a recession has always begun six months to two years later. If the yield curve becomes flat soon, this would be consistent with a recession beginning in 2019 or 2020. We are operating under this perspective as well, though as the expansionary phase of the cycle continues, it is advisable for all of us in the real estate industry to prepare contingency plans, revisit strategies for the late stable and early downturn phases of the cycle, and be prepared to react quickly to potential alternative outcomes.

Who Took the Survey?

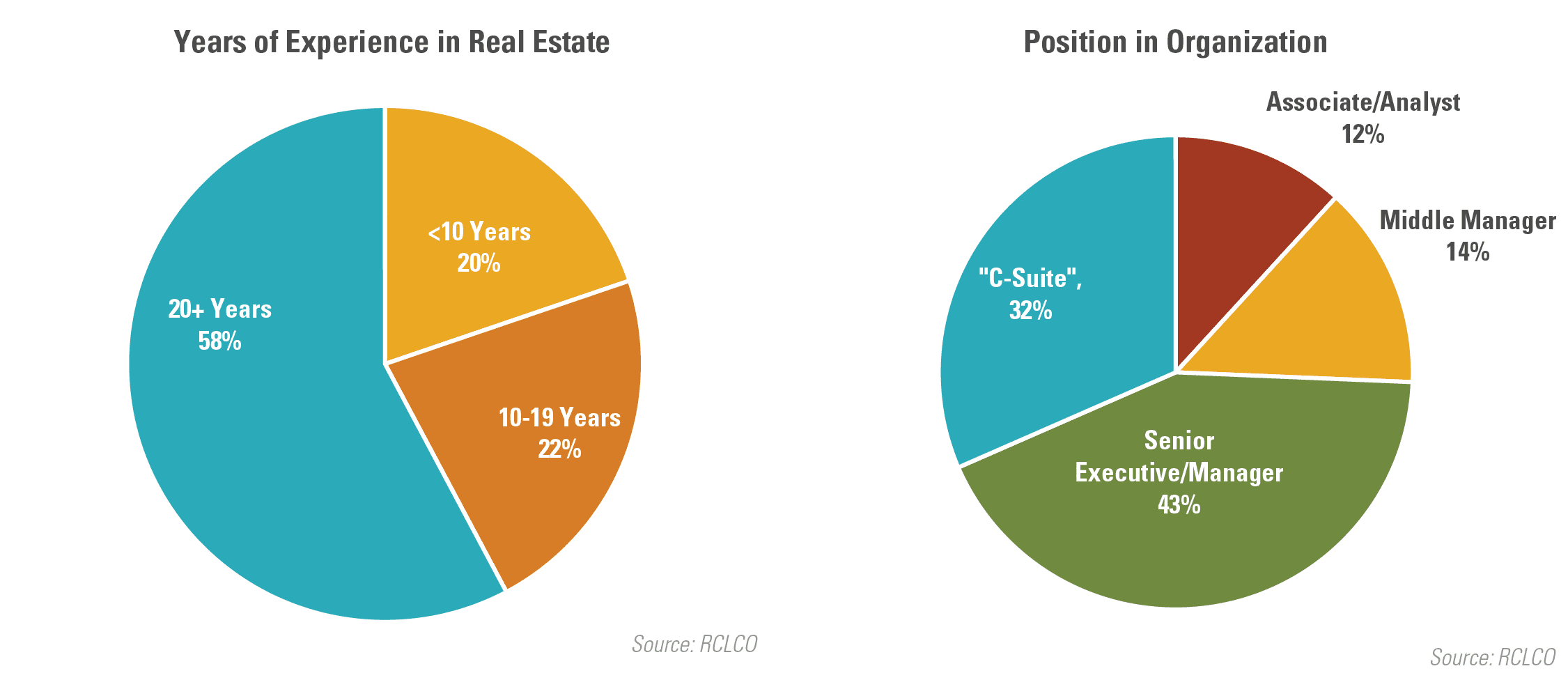

RCLCO’s Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and across the industry. Nearly three-fifths of respondents have worked in the real estate industry for 20 years or more, and 75% of respondents are C-suite or senior executives in their organizations.

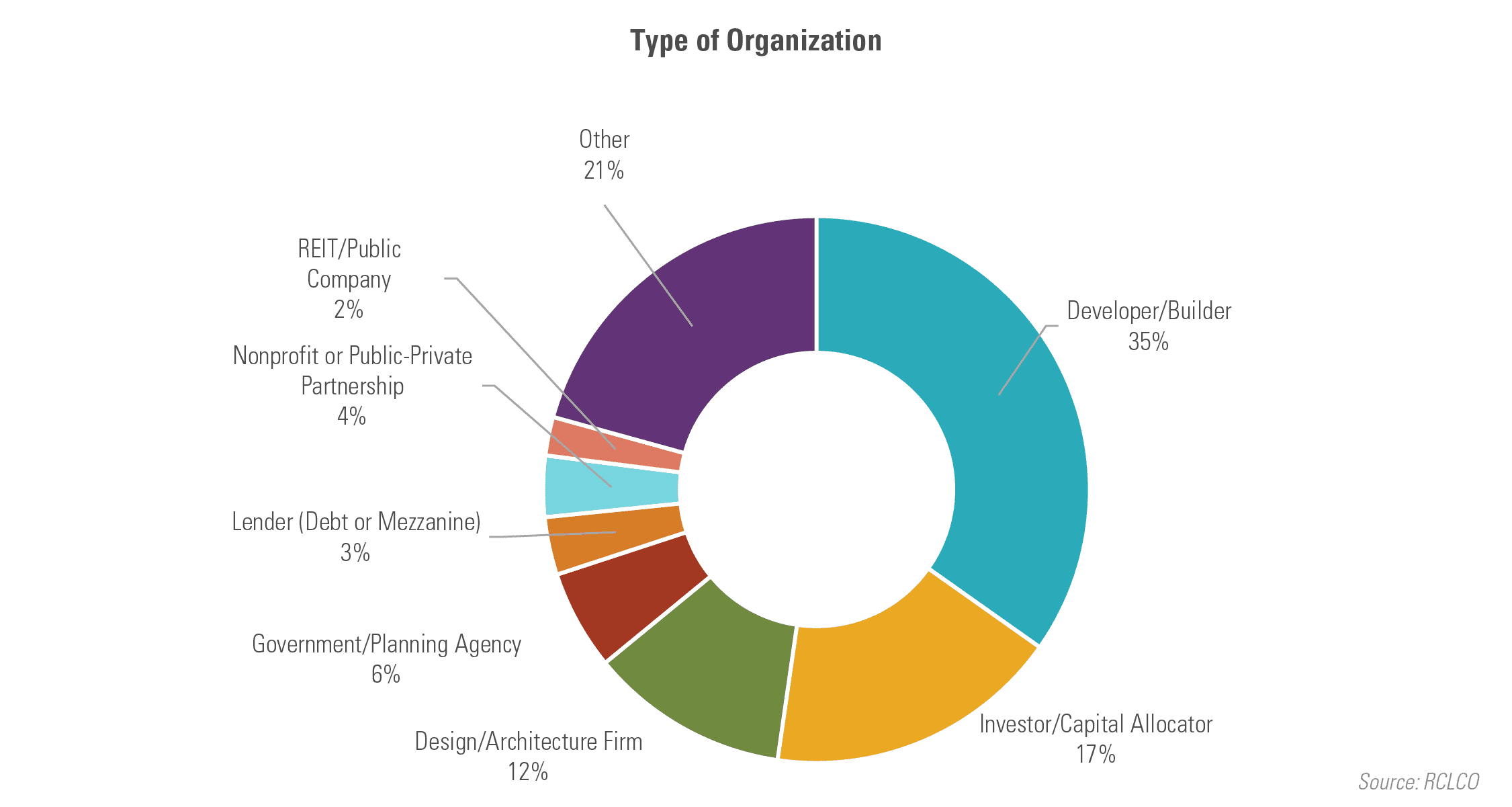

Developers and builders comprise the largest share of respondents, at 35% of the sample. Another 17% are investors or capital allocators, followed by 12% in design or architecture firms. The remaining one-third of respondents come from a variety of other types of organizations within the real estate industry.

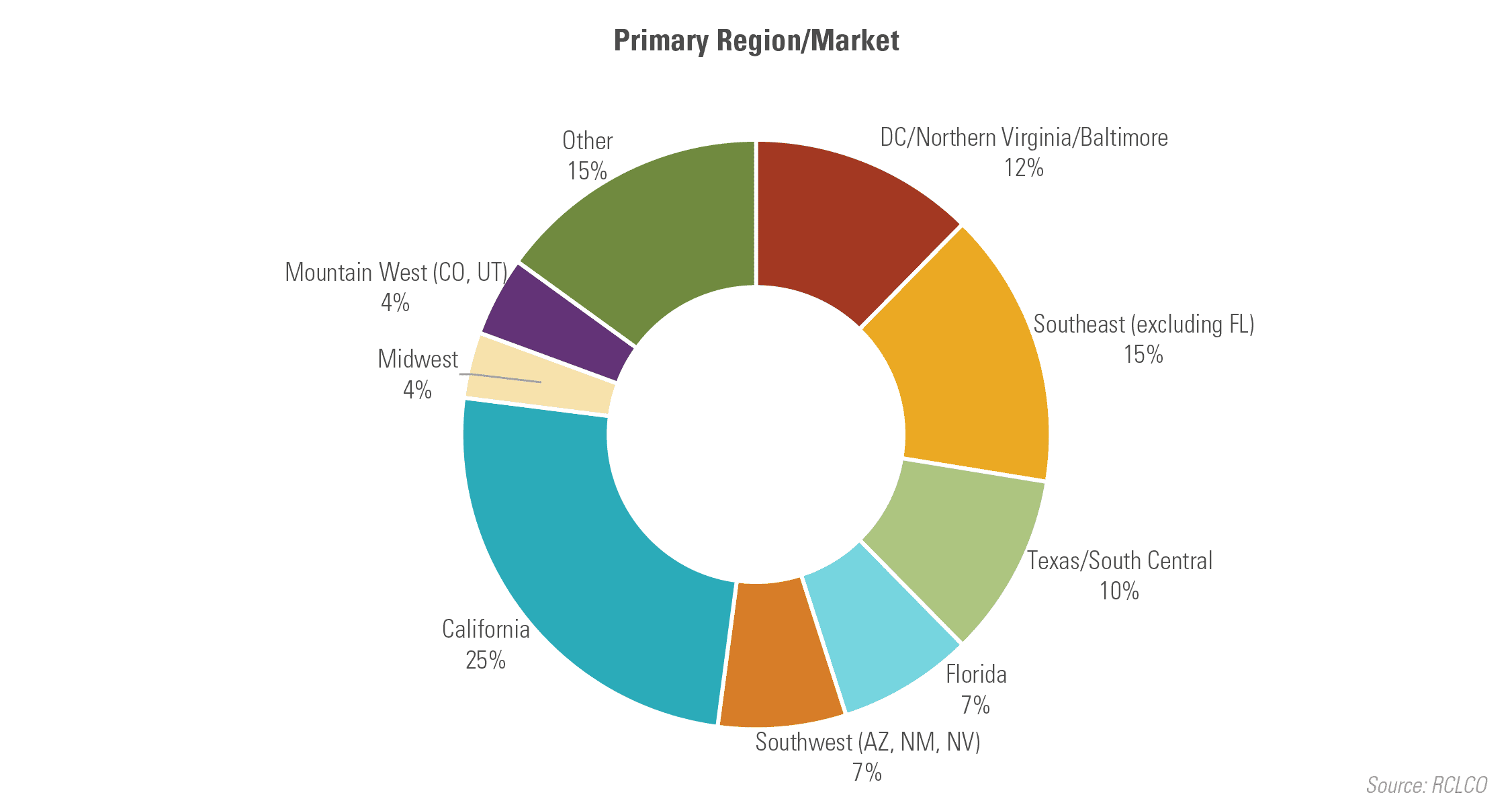

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Article and research prepared by Len Bogorad, Managing Director, and John Rendleman, Associate.

RCLCO’s mission is to help clients make strategic, effective, and enduring decisions about real estate. We proudly celebrate more than 50 years of providing the best minds in real estate with cutting-edge analytics, actionable advice, and the highest level of customer service. Our work includes market, economic, financial, and impact analyses; investment portfolio strategy and implementation; entity-level strategic planning; and management consulting.

Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us