Have We Reached the Light at the End of the Tunnel?

RCLCO National Sentiment Survey Part 1

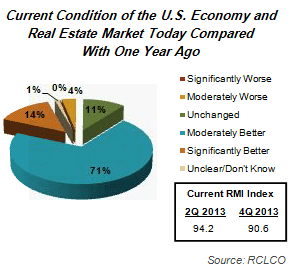

In the last three years of the RCLCO National Sentiment Survey, real estate professionals have exhibited nothing short of exuberant optimism regarding the state of the economy and regional and national real estate markets. As the downturn of 2009 fell further into the past, our respondents saw a brighter light at the end of the tunnel, with the National Current Real Estate Market Index (RMI1) reaching 94.2 in 2Q 2013 and 90% of respondents agreeing that conditions were “better” than one year earlier.

|

|

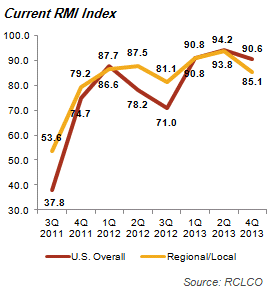

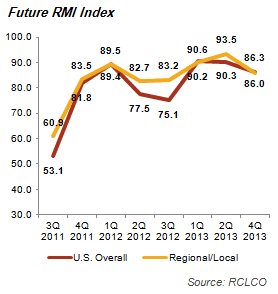

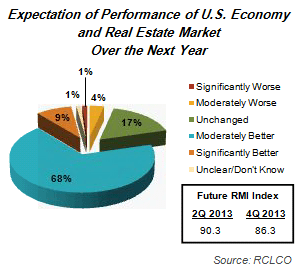

Heading into 2014, it appears that some real estate professionals have gotten close enough to the light to begin to squint. After a year of dramatic improvements in sentiment, respondents are no longer reporting increasing levels of optimism, with Current RMI falling to 90.6 nationally (-3.6) and 85.1 regionally (-8.7). Sentiments about conditions in the year ahead have also begun to flatten, with Future RMI at 86.3 nationally (-4.1) and 86.0 regionally (-7.5). With sizeable federal budget and employment cuts, it is not surprising that the Washington, D.C./Baltimore/Virginia region has the lowest Regional Current RMI at 57.1, down 28 points from 2Q 2013. The region remains the least optimistic about the future as well, with a Regional Future RMI at 69.2, although 50% of respondents do expect moderately better conditions in the coming year.

|

|

Although current and future sentiment is less bullish than in prior periods, this is likely an indication that economic and real estate market conditions are reaching stability, not a signal that conditions are beginning to turn down. For Sentiment Survey results to indicate a period of distress, Current National RMI would have to drop 17 times more than the decrease seen in the last 6 months. Nonetheless, with some increase in uncertainty about the prognosis for real estate and the economy, now is an ideal time to identify a set of indicators—quantitative and qualitative—specific to your business and market, determine where you stand in the cycle, and decide on the best cycle strategy for your company. See here for strategies RCLCO recommends for preparing your company for a future downturn, whenever it may occur. Primary among these strategies is to monitor your markets, and to have a plan!

For-Sale Optimism Remains, Despite Mixed Indicators

As 2013 came to an end, our respondents’ optimism was not the only indicator to experience a deceleration. Various indicators began to suggest that the for-sale housing market recovery was experiencing a slowdown. For example, the S&P/Case-Shiller Home Price Indices continued to show year-over-year improvements, but the pace of price increases slowed, with 90% of their 20 major cities showing lower monthly growth in the 4Q 2013. Single-family housing starts and permits both declined in December, and NAHB’s Housing Market Index of builder confidence slipped back slightly in January.

As 2013 came to an end, our respondents’ optimism was not the only indicator to experience a deceleration. Various indicators began to suggest that the for-sale housing market recovery was experiencing a slowdown. For example, the S&P/Case-Shiller Home Price Indices continued to show year-over-year improvements, but the pace of price increases slowed, with 90% of their 20 major cities showing lower monthly growth in the 4Q 2013. Single-family housing starts and permits both declined in December, and NAHB’s Housing Market Index of builder confidence slipped back slightly in January.

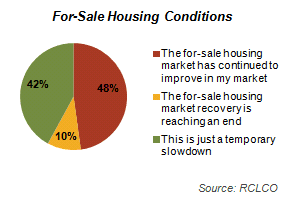

However, only 10% of Sentiment Survey respondents believe that the for-sale housing market recovery is reaching an end. Nearly one-half of respondents report continuing improvements in their regional/local for-sale housing markets, and 42% believe that negative indicators reflect only a temporary slowdown.

Respondents on the Bubble: Multifamily Rental

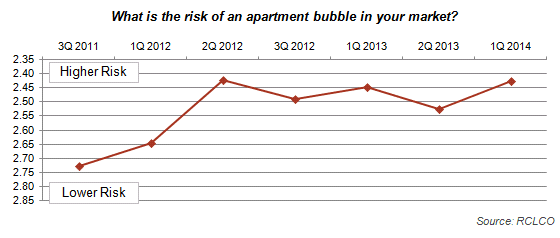

As respondents stay optimistic about the for-sale housing market in light of these mixed indicators, sentiment about multifamily rental continues to create anxieties among respondents. Concern about the risk of a rental apartment bubble increased sharply from late 2011 to early 2012, and has since continued at this elevated level. This quarter’s survey shows slightly increased apprehension about a rental bubble, with nearly 60% of respondents reporting a moderate to significant risk in their market, up from one-half in 2Q 2013 and 40% in late 2011. However, Northeasterners2 perceive less risk of an apartment bubble, with no respondents foreseeing a significant risk, and nearly 20% of respondents reporting no risk.

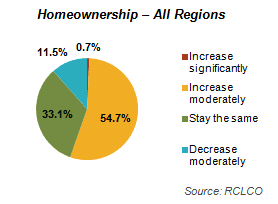

So, were our historically pessimistic Northeasterners just in the holiday spirit? It’s possible, but a more likely factor affecting respondents’ assessment of the risk of an apartment bubble is their expectation regarding homeownership rates. As homeownership rates hit their lowest point in 18 years, their future trajectory is creating a split of opinion among survey respondents: 55% expect homeownership rates to increase moderately in the next six to 12 months, while the other 45% expect no change or a moderate decrease.

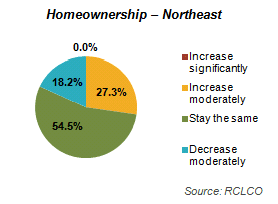

Unlike the rest of the country, nearly 75% of respondents in the Northeast expect unchanging or moderately decreasing home ownership rates in the next six to 12 months. Anticipated stable homeownership rates, along with more challenging site acquisition and entitlement processes, may be contributing to the lack of concern about a possible rental apartment bubble in this region. Southerners3 are expecting the most significant increases in homeownership rates and likewise are the most worried about an apartment bubble, with 92% of respondents reporting at least a slight risk.

|

|

As demonstrated by this sentiment, it is important to resist labeling many indicators as purely positive or negative, as a synthesized analysis of various indicators will often form a more complete, telling picture of current and future market conditions. When determining where your company is in the cycle, a mix of indicators and internal data will help lead you to the light at the end of the tunnel, however bright it may be.

Stay tuned for next week’s Advisory, RCLCO’s National Market Sentiment Survey Results Part 2, for more recommendations on leading your business through this dynamic market.

1The Real Estate Market Index (RMI) is based on a quarterly survey of real estate market participants and is designed to take the pulse of economic and real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate economic and real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

2The Northeast refers to New England, New York, New Jersey, and Pennsylvania.

3The South refers to the Baltimore/Washington, D.C./Virginia, Florida, Southeast, and Texas/South Central regions.

Article and Research prepared by Len Bogorad, Managing Director, and Trish Kennelly, Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. RCLCO’s Strategic Planning and Litigation Support Advisory Group produced this newsletter. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/strategic-planning

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us