The Opportunity is Now! Plan for a Market Evolution from a Place of Strength

What’s Ahead–Clouds Gather, but Still on the Horizon

We start 2019 eyes wide open to the fact that it is now nine years since the trough of the post-2008 recession. In this space for several years we have suggested that economic cycles are almost certain to remain a reality and that every company’s or investor’s cycle planning should reflect a hypothesis as to when that event might be, what will cause it, and how significant the impact might be on their real estate positions. For better or for worse, the one thing we know for certain, paraphrasing Jeremy Newsum, is that we are one year closer to the end of this cycle than we were a year ago today. But it doesn’t give any more optics on when and what kind of a cycle we will inevitably experience.

While consumer confidence and job formation, two key leading economic indicators, remain high, we are certainly in the mature phase of the economic, real estate, and capital markets cycles, and there are indeed more warning signs on the horizon.

When?

Economists’ track record for predicting the timing of recessions is not good, but the economy’s recent slowing may give credence to many economists’ belief that a recession is likely in the next two years. RCLCO agrees that the probability of a real estate market downturn between now and 2022 is high, and while certainly not inevitable, our contingency plan anticipates it.

We believe that the downturn is most likely to begin later in this period, in 2020 or 2021. This is consistent with the current performance of two indicators that have generally predicted recessions: an inverted yield curve, and a decline in employment. The yield curve has not yet inverted, and inversion most often signals a recession 9-15 months later. And employment growth continues to be strong.1

What Will Cause a Slowdown?

The duration of the current expansion, the trade war with China, the slowing economies of our trading partners around the world, slowing in the U.S. housing sector, the growing instability and certainty of government behavior such as U.S. Federal Government shutdown and Brexit, are but a few of the factors contributing to rising uncertainty. History tells us that economic reversals are often triggered by an exogenous or unforeseen event, or structural challenges that were overlooked or underappreciated, making them difficult to describe, let alone predict. We have experienced recessions in which deteriorating real estate fundamentals were a compounding effect (2008) and recessions through which real estate fundamentals remained relatively functional (2001).

And What Will Be the Effects?

With respect to the unpredictability of recessions, our hypothesis is that the next cycle will be more akin to 2001 than 2008. Therefore, we are counseling our clients that the next slowdown is likely to be easier to work through than 2008, with the primary risks being pricing and temporary liquidity, most likely without the radical disruption in demand that we experienced following 2008.

Where Are We Now–Froth Moving Out of the Market

We perceive that the markets are, in fact, acting on this outlook in some measure already.

- Property prices are moderating subtly to reflect evolving interest rate conditions and a more cautionary market outlook.

- Challenging real estate deals are having difficulty finding buyers and/or need to adjust pricing to close.

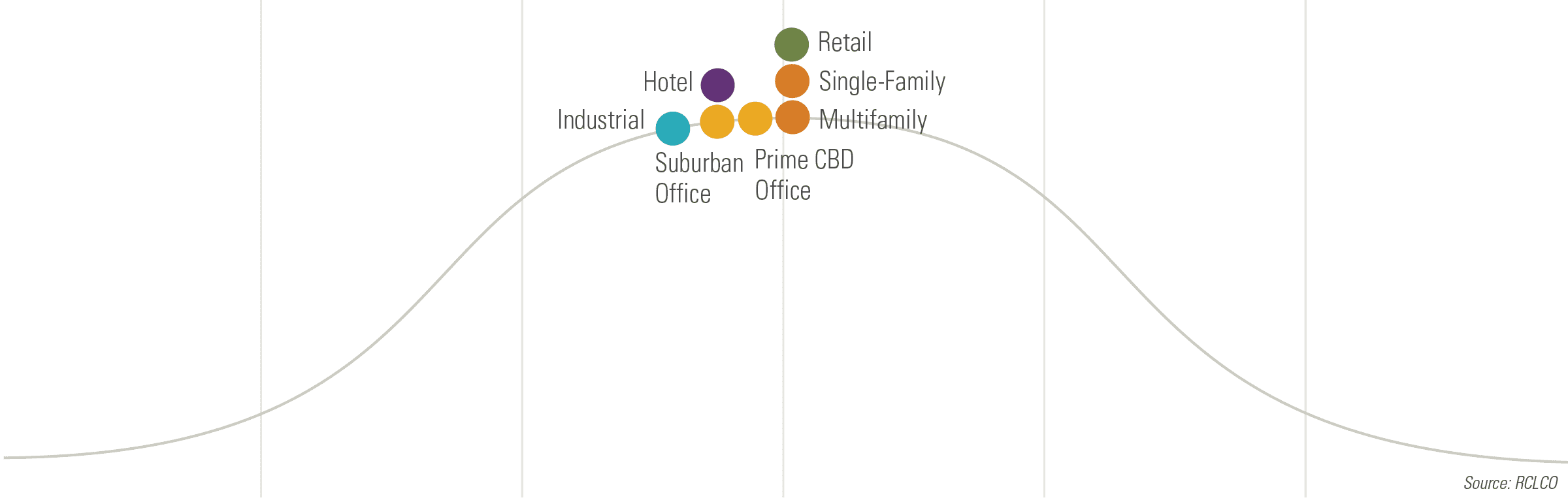

- Smart developers are working diligently to move away from sectors with signs of overbuilding (in many cases high-end and Class A urban multifamily and office projects in markets with elevated pipelines) and to middle market (workforce housing, suburban office, industrial, etc.) or niche sectors (life sciences, data storage centers, niche housing segments, close-in logistics centers, etc.) that are less under threat from competitive supply.

- Investment underwriting in many income-producing sectors is becoming more disciplined (particularly on the revenue side, although not yet diligent enough on the cost side), and pipelines are waning marginally in some markets as a result.

- Construction costs continue to grow at above-average rates (and faster than revenues are growing in most sectors), perhaps 5% or more this year (not quite as bad as 2017 and 2018).

- Patient capital (“dry powder”) continues to form, intent to deploy when a dislocation appears, but avoiding the temptation to deploy early.

- The for-sale housing sector is the first property type to exhibit signs of a slowdown. Reduced affordability is making it challenging to maintain new home sales velocity without shifting the mix to include a greater share of “attainably priced” homes. We believe this reflects unique conditions in the for-sale market—specifically, higher mortgage interest rates and rapid recent price increases in supply-constrained markets driving pricing to unaffordable levels—rather than necessarily representing a leading indicator for other property types.

Caution remains the name of the game, and the most talented investors, developers, and owners already have their playbook in place, and capital relationships secured, to remain in business through the inevitable cyclical disruption.

What to Do Now–Or How to Be in Business Through a Tough Couple of Years

Most players find themselves in defensive mode during the downturn and early recovery stages of the cycle. It is those who are able to switch to offense early that tend to profit the most from others’ misfortunes. For any company that doesn’t have an explicit strategy prescribing its action plans through each phase of the real estate cycle, the time to prepare one is yesterday. This plan should not only describe behavior and activity during the declining stage of the cycle, but also what you will do and how you will capitalize activity in the early phases of the recovery. This is the optimal time—but also the hardest—to be in business.

Our advice can be summarized as follows:

- Manage balance sheets with rigor; only cash is really cash, and liabilities are really liabilities.

- Develop or dialogue with capital partners committed to fund through a rough patch. This should include an outlook on how the market will behave and, specifically, your plan for what to buy or start, and when. Such an arrangement can be structured now, but it is much harder to organize when the downturn is already underway.

- If there is refinancing to be done, do it now. As of this writing, we have a moment of reprieve in rates. We do not expect a big spike in borrowing costs, particularly if the economy softens, but access to debt and terms will likely worsen when access to debt would be most helpful.

- Consider pruning in places where you think the fundamentals are problematic. This may include asset or land sales where pricing and supply/demand outlook are misaligned. It may also mean extending options, or committing to favorable takeout scenarios, even if you risk giving away some upside. This is not the time to be asset rich or highly leveraged. Cash WILL be king, and debt service capacity is nothing to toy with.

- Be rigorously honest in OpEx underwriting and CapEx forecasting (is it really offensive or defensive?). Recognizing that doing so risks pushing you out of the market, getting this wrong has painful downstream consequences, including upsetting capital partners who must be willing to fund when the buys are best.

- Consider technology investments (including workforce communication and collaboration enhancements, customer-facing marketing and service enhancements, artificial intelligence and machine learning, etc.), especially if you are confident they will enhance near-term productivity or improve competitiveness. Perhaps counter-intuitively, if such opportunities exist, the return on them will be great during lean years, and impossible to undertake when times are tough and cash is precious.

- Have a human capital plan. Companies need to have a well-developed approach for managing costs and retaining the talent that will be needed to thrive later on.

The old adage “a recession is a terrible thing to waste” is usually understood to be tongue in cheek, but some players have managed to work through a weaker period with fewer sleepless nights, and a wise few have in the past been positioned to pounce on the upside early.

Another year or two to position your firm to do this really would be a terrible opportunity to miss. Do it today.

Article and research prepared by Adam Ducker, Senior Managing Director, and Charlie Hewlett, Managing Director.

References:

Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us