RCLCO National Real Estate Sentiment Survey: For-Sale Housing Gaining on Rental Apartments

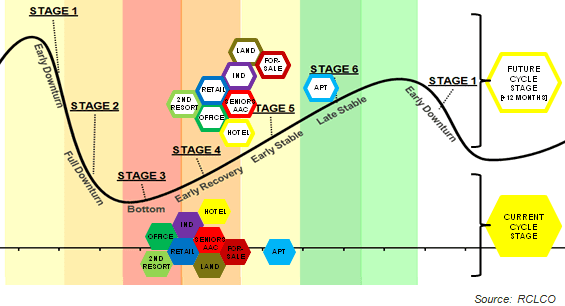

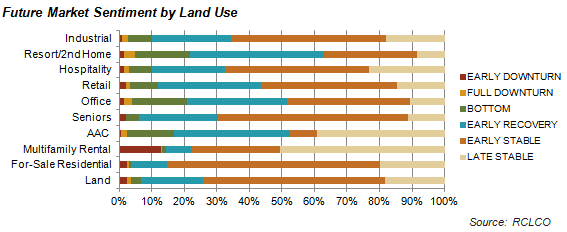

In the last year, great strides have been made across all sectors of real estate. In RCLCO’s Q3 2012 Market Sentiment Survey, multifamily rental apartments led the pack in Stage 4-Early Recovery, as other land uses continued to bump along the bottom. This quarter’s survey results are telling quite a different story. The resort/second home and office sectors are nearing Stage 4-Early Recovery, and all other sectors with the exception of multifamily rental are steadily climbing towards Stage 5-Early Stable.

But one theme remains the same: multifamily rental continues to outpace the crowd. In fact, 51% of respondents expect to see multifamily rental reach Stage 6-Late Stable in the next year, up from 34% in Q1 2013. Another 13% predict a pass over the peak into Stage 1-Early Downturn, up from only 8% in the last survey.

Sentiments regarding land and for-sale residential are improving at the quickest pace, consistent with U.S. Census reports showing that single-family housing starts are continuing to rise more than 10% year-over-year. These improvements are so substantial that a Deutsche Bank July 2013 Housing Report predicts household formations will approach historical norms in the next year. Senior/active adult communities have seen the least improvement in sentiment over the last year, and were surpassed by the hospitality sector this quarter. Although sectors other than multifamily rental have not recovered rapidly, we expect all of these sectors to continue to progress towards full expansionary phases of the cycle in the next year.

On the bright side, future sentiments have been rising substantially among our respondents across sectors in the last year. Every real estate sector is forecasted to move to the next rung in the recovery and expansion stage of the cycle over the next six to 12 months, with the exception of some mixed feelings about multifamily rental—perhaps based on fears of an apartment bubble on the horizon.

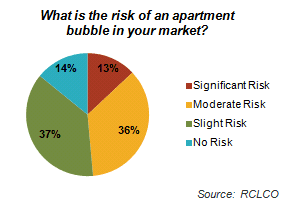

Don’t Burst Your Bubble

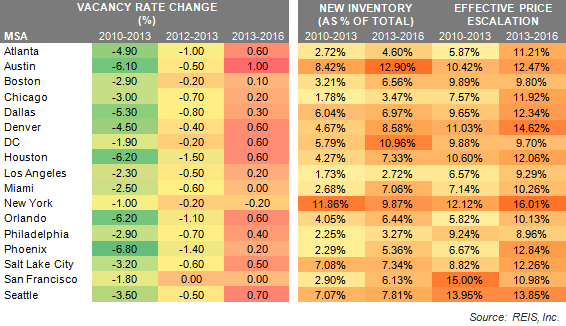

Assessment of the risk of an apartment bubble has not changed significantly since the last survey, but remains at fairly elevated levels, with approximately one-half of survey respondents believing there is a moderate or significant risk of an apartment bubble in the market where they are most active. This uneasiness may be coming from the huge increases in supply and future pipelines—particularly in certain submarkets. The rental apartment stock has increased by 11.86% in New York since 2010, and by over 5% in the Dallas, Seattle, Austin, and Salt Lake City MSAs and Washington, D.C. According to NAHB, multifamily housing starts averaged 325,000 in the first quarter of 2013—the highest since the 1980s.

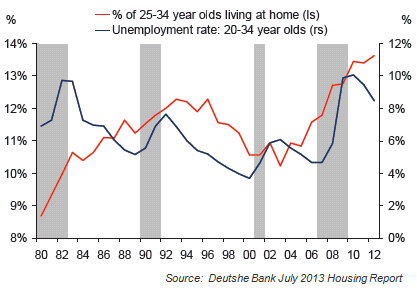

Even with these large supply increases, every major MSA has seen vacancy rates drop since Q1 2010, with an average reduction of 360 basis points (bps). And this is happening simultaneously with average rent escalations of 8.4%. Pent-up demand is still substantial, as over 13% of 25-34 year olds are currently living at home. As job growth continues and unemployment falls, history tells us that many young adults living at home are likely to move out.

Although market fundamentals have been steadily improving across the nation since 2010, current trends support the beliefs of many respondents that some markets may be reaching a tipping point. Forecasts through 2016 show vacancy rates increasing in most of the major markets, with increases as high as 100 bps in Austin and 70 bps in Seattle. Although both of these markets have experienced rapid population and job growth, large pipelines will likely create some risk in the coming quarters.

A number of markets are showing signs of sustaining strong growth, with vacancy rates continuing to decrease or stay level in light of new construction and price escalations. Large levels of pent-up demand and high barriers to entry in markets such as New York, San Francisco, Boston, and Miami appear likely to keep those markets healthy. Although we do not currently foresee a nationwide rental apartment bubble, at this stage in the cycle it is critical to evaluate the situation and prospects in a specific market and submarket, with particular attention to the pipeline and employment prospects.

Article and Research prepared by Len Bogorad, Managing Director and Trish Kennelly, Associate.

RCLCO provides real estate economics, strategic planning, management consulting, and implementation services to real estate investors, developers, financial institutions, public agencies, and anchor institutions. Our real estate advisors help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. Interested in learning more about RCLCO’s Strategic Planning and Litigation Support services? Please visit us at www.rclco.com/strategic-planning.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us