Sequestration—What Me, Worry?

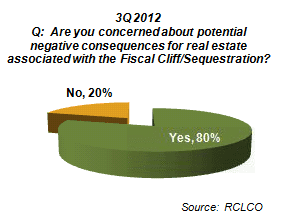

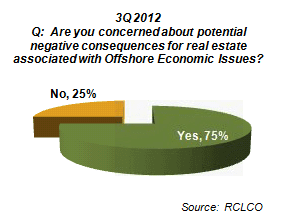

Two months before the presidential election, and a full quarter before Congress kicked the latest fiscal cliff and sequestration can down the road until March of this year, RCLCO asked industry professionals if they were concerned about potential negative consequences for real estate associated with the dysfunction hap- pening in Washington. In 3Q 2012, a full 80% of real estate market participants indicated they were indeed concerned—and 20% indicated that it was a non-issue. In the same survey, 75% indicated that they were con- cerned about the negative impact that offshore economic issues (e.g., Eurozone meltdown, China slowdown, 3Q 2012 3Q 2012 etc.) could have on real estate here in the U.S.

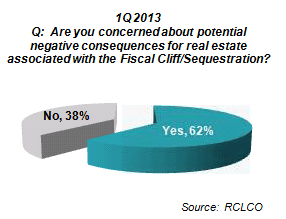

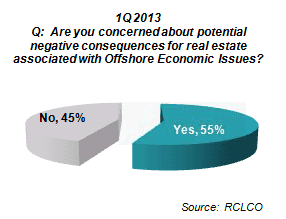

Fast forward to 1Q 2013, and the percentage of real estate professionals who indicate they remain concerned about domestic budgetary and offshore economic activities has certainly declined, but remains at relatively elevated levels. Just over 60% of respondents to the RCLCO 1Q 2013 National Real Estate Sentiment Survey indicated they are concerned about the fiscal cliff/sequestration, and a slight majority, 55%, indicated they are concerned about offshore economic issues.

Curiously, when asked “are you doing anything to insulate yourself or your company from potential risks as- sociated with either the Fiscal Cliff/Sequestration or Offshore Economic Activities,” the majority of respondents answered “no” (Fiscal Cliff: 53% no; Offshore Activity: 64% no). Beware the Ides of March, or sometime soon thereafter…

Increasing Moderately

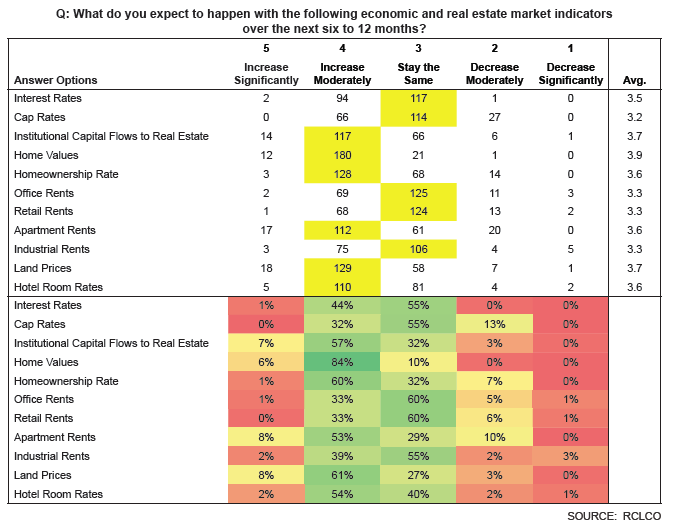

Irrespective of any fiscal cliff or Eurozone/China worries, the majority of real estate market participants antici- pate that key economic and real estate market indicators will either stay the same, or improve moderately over the next six to 12 months. Few, if any, respondents expect market fundamentals to deteriorate. At the same time, few expect the markets to improve at a rapid pace over the next year.

The consensus view is that interest rates and cap rates will remain steady over the next six to 12 months. Most respondents believe that office, retail, and industrial rents will also hold steady, although nearly one-third expect these rents to increase moderately. Land prices, homeownership rates, and home values are forecasted to increase over the coming year, as are hotel room rates and apartment rents. These survey results are entirely consistent with the expectation that most real estate industry sectors have turned the corner and are poised for positive momentum and growth in 2013 and beyond.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us