The New Model for Commercial Real Estate Demand

While U.S. commercial real estate markets are continuing to recover, they have improved more slowly from the 2008 recession than they did from previous downturns. While some of this is due to cyclical economic factors, new secular forces are a significant cause of the slow recovery. Global integration of economies and capital markets, as well as new technology that is wholly embraced by the youngest generation of workers, are affecting both the volume of real estate demand and how real estate is used.

In some ways, real estate demand seems to have recently disconnected from economic trends. But in reality, new forces must be incorporated into demand models going forward. Working and shopping are now integrated into social experiences, particularly for Gen Y. While technology is unlikely to replace the need for physical spaces, it is allowing corporate and government users to continue to reduce space usage per employee. Space is being used more strategically to build a corporate brand, support collaboration, and improve productivity, as well as to reduce costs. Spaces across all property types are increasingly being expected to create a positive environment for social interaction with less of an environmental footprint.

Going forward, there will be winners and losers as properties differentiate themselves based on those that can serve a new world of users who are globally and technologically integrated. Certain office and retail properties are examples of properties that are particularly at risk of long-term obsolescence and above-average vacancy, although certainly not the only property types subject to new secular trends. Space usage is changing in the industrial sector, which is certainly challenging retail in a race for the most efficient distribution of goods. Thus owners should be keenly aware of current trends that are differentiating the performance of individual properties.

A Slow Economic Recovery

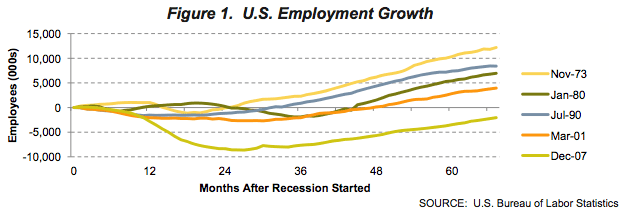

Given, this has been a slow economic recovery. It is now more than five years from the start of the 2008 downturn, and the U.S. job market has yet to return to peak employment levels (Figure 1). In contrast, the job market returned to peak employment levels within two to four years after the start of the previous four recessions. While sectors such as energy, technology, healthcare, and other services are expanding, long-term structural unemployment remains in low-skilled jobs, particularly in the construction and manufacturing sectors and within the younger population base. The good news is that the job market continues to recover, including younger workers as well as construction-based industries serving the housing market and U.S. and export-based manufacturing.

A Disconnect in Real Estate Demand

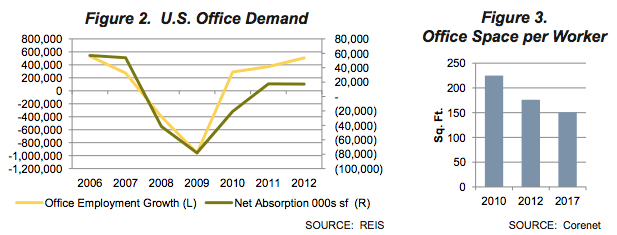

Despite the improving economy, commercial real estate demand has responded unusually slowly due to secular changes in capital markets as well as how space is being used. One example is the office market, where historically office demand has been closely related to changes in office employment. But current trends are diverging from history as demand for office space has significantly lagged job growth since 2009 (Figure 2).

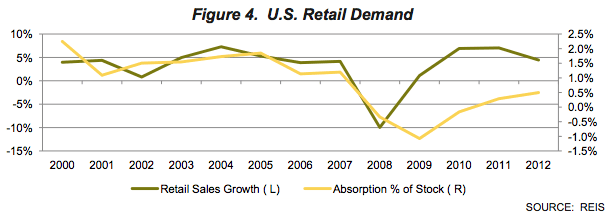

Much of this discrepancy can be explained by new trends in the usage of office space. For example, Corenet’s survey of more than 280 commercial real estate executives indicated that office space per worker is quickly shrinking (Figure 3). In fact, executives indicated that space per worker shrank by 22% from 2010 to 176 square feet per worker in 2012 and is expected to shrink by another 14% by 2017.

Another example is the retail sector, which is facing similar trends. Demand for neighborhood and community centers generally follows retail sales trends. But recent demand for retail space has been significantly lagging improving job markets and fairly robust increases in consumer spending (Figure 4).

E-commerce is one of several factors that are changing the retail sector. While e-commerce sales continue to gain market share (Figure 5), the overall trendline masks significant changes within retail categories.

For example, the clothing and apparel sector is already the largest sector for electronic shopping and mail-order houses. Apparel e-commerce sales as a percentage of total apparel sales are quickly approaching a critical level where store usage starts to decline—a level that has already been reached in the toys, books, and electronics categories. This is of particular concern for malls and lifestyle centers and some power centers that have large exposures to clothing and apparel retailers. Lower-quality malls in secondary locations will face further re-tenanting challenges, and revenues will be further pressured as many retailers, particularly larger stores that frequently replace in-line tenants in failing malls, pay less rent than clothing retailers. Top malls that play a critical role in retailer branding are less likely to be impacted. Retail, a decreasingly competitive way to distribute goods, will more likely need to integrate social networking, technology, and entertainment features.

Our expectation is that commercial real estate markets will continue to recover in line with the economic recovery. However, secular changes in space usage will cause the recovery to be uneven by both property type and location. Global integration of economies and capital markets will also continue to have a significant impact on the market. Real estate will serve a new role in the years ahead. No longer just a place of shelter, space usage will compete with technology as a tool that can be used to improve corporate revenues, productivity, and efficiency. Properties that have physical attributes that can serve these needs and that are located in strategic locations with large, wealthy, and growing population bases are most likely to succeed.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us