Cycle Update—Moving Right Along

RCLCO’s National Market Sentiment Survey 1Q 2015 Results – Part 2

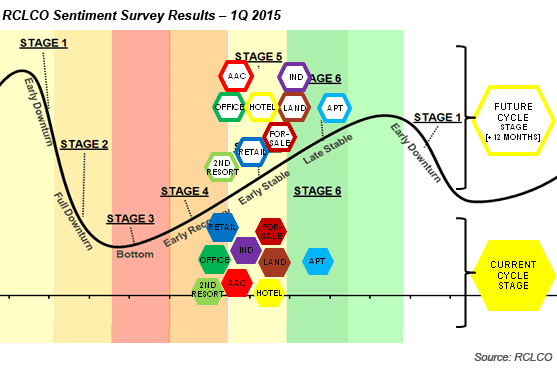

Moving into the new year, most land uses are in the early stable stage of the cycle, with multifamily rental continuing to lead the pack and second home/resort trailing behind. Office, retail, and hospitality have moved slowly out of the bottom, with one-third of respondents reporting that office and retail remain in the early recovery stage, and 22% of respondents reporting that hospitality remains in the early recovery stage. However, an uptick in forward movement is expected from these uses—hospitality and retail had the most forward momentum of any land uses in the past year. Additionally, retail and office are two of respondents’ top three land uses in terms of expected forward momentum in 2015.

While one-half of respondents believe that second home/resort is still in early recovery, expectations for the year ahead are positive, with 42% of respondents expecting this use to be in early stable in the next year. In fact, more forward momentum is expected from this land use than any other in the next year. Most other uses—land, condo, age-restricted/active adult, seniors, industrial, and for-sale residential— are considered to be in the early stable stage of the cycle, with steady but moderate growth expected in the year ahead.

At this early stable stage, real estate markets are at their closest to equilibrium. Some pent-up demand and forward momentum in the marketplace remains, as it takes time to gear up and deliver new projects. At this stage, developers should continue to start new projects per their investment/yield matrix. However, this is also a time to become more selective in terms of land acquisition, and slow asset acquisitions by increasing hurdle rates to avoid marginal deals.

On the Edge—Multifamily Rental

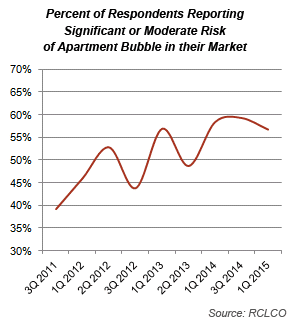

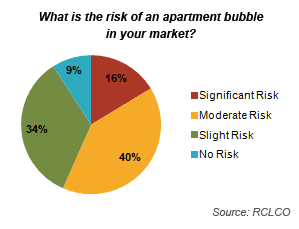

Multifamily rental has moved only slightly towards early downturn as it continues to sit in the late stable stage of the cycle. Worries of an apartment bubble remain steady, with 16% reporting a significant risk, and 40% reporting a moderate risk, in the market where they are most active. In this survey, 67% of respondents report that multifamily rental is in late stable, but fewer than 5% have seen a pass over the peak into early downturn at this point. Although 17% of respondents expect this use to move to early downturn in the year ahead, most expect it to still be in late stable a year from now.

The late stable stage of the cycle is the time to begin to consider selling assets that are not long-term holders. As difficult as it can be when the rental apartment market is healthy, this is the stage to dispose of marginal deals and assets not wanted after the peak, and to tighten underwriting criteria and raise hurdle rates for new deals. This is also the stage in the cycle to consider refinancing with flexible, low-cost debt, and to identify capital sources that will enable your company to take advantage of dislocations in the next downturn.

Regional Differences—Oil and the Mouse

In addition to monitoring and adjusting for the cycle, a slew of other factors, including socioeconomic, technological, global, and political, continue to create uncertainty for the future of U.S. real estate. Although some of these trends can be seen through a national lens, a deeper dive into regional sentiments reveals the importance of a close handle on regional differences in dynamics, demand drivers, and macro conditions—one of the many necessary elements in an informed strategy.

In this survey, sentiment remains constant in many regions, while some have seen significant changes. Sentiment in Northern California continues to be the most positive in the country, as strong job growth prevails. Sentiment also remains high in the Northeast, despite Winter Storm Juno and the rise of the dollar. Respondents in the Mountain West, Southeast, and Southern California are feeling generally positive per their usual, as Baltimore/Washington, D.C./Virginia respondents continue to report some of the most negative sentiments in the country, likely driven by continuing slow job growth and concern about federal budget issues. Moderate sentiment remains in the Midwest and Southwest, where some economic indicators have improved but demand has generally not increased dramatically. The Pacific Northwest is showing much lower sentiment than past surveys, likely driven by declining affordability and fear of oversaturation in some sectors.

In contrast, two regions have seen significant transformation in sentiment over the last six to 12 months—one for better and one for worse.

Sentiment on the Rise—Florida

What do Mickey Mouse and the Baby Boomers have in common? They are both drivers behind the expanding economy and positive sentiment in Florida. The tourism industry, anchored by The Mouse and a growing presence from Universal Studios, led Orlando to the number one spot on Forbes’ Top Cities for Job Growth in 2014, with 3.7% growth, more than twice the national average in large metropolitan areas.1 Miami also showed strong job growth, coming in fourth on the list with 3% growth. As the number one destination for retirees by a wide margin, Florida is just at the beginning of a long-term, Baby Boomer growth spurt. The impact of retiring Boomers is demonstrated by The Villages—an age-restricted community in Central Florida, and the top-selling master-planned community of 2014, with 2,601 home sales in the past year. With multiple growth factors at play, it is no wonder sentiment among Floridians is well above average, with 95% of respondents reporting better conditions than a year ago.

Blurred Lines—Texas/South Central

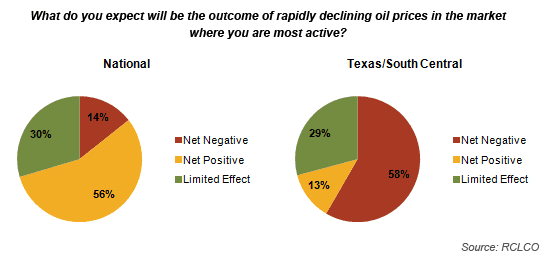

The Texas markets are used to the national spotlight as the recession leaders, growth champions, miracle makers, and employment havens. According to the Brookings Institution, Texas cities accounted for five of the 20 strongest-performing metro areas during recovery from the recession—mirrored in sentiment results of past surveys. But the spotlight now shines a little too bright, as oil prices have tumbled to near six-year lows, and highly dependent markets, particularly Houston, begin to feel the heat. Respondents in Texas/South Central are reporting the least positive sentiment since data collection began in 2Q 2012, with over 25% of respondents expecting conditions to worsen in the year ahead, though it’s important to put an expectation of “worsening conditions” into proper context as job growth exceeded 4% in both Houston and Dallas-Fort Worth in 2014 (each market added well over 100,000 jobs). Although low oil prices will slow Texas’ employment growth, the direct impact of oil prices is likely to be felt primarily in Houston, Midland-Odessa, and South Texas markets such as Corpus Christi and Victoria, where high concentrations of upstream energy jobs are located, though a prolonged depressed oil price could have more widespread impacts. Although slowed job growth may create challenges in some sectors with robust pipelines, progress towards more balanced levels of residential inventory, which have reached record lows in most major markets, could have a moderating effect on the rapid price increases in single-family housing in many Texas markets, which have had significant impacts on affordability. While 58% of respondents from this region expect the result of lower oil prices to be a net negative for the market—compared with the 56% of national respondents who are expecting a net positive impact—it remains to be seen what the magnitude of these effects will be.

1 According to Forbes, represents data as of November 2014, non-agricultural employment only.

Article and Research prepared by Len Bogorad, Managing Director, and Trish Kennelly, Senior Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. RCLCO’s Strategic Planning and Litigation Support Advisory Group produced this newsletter. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/strategic-planning

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us