Going Steady: Expectations Optimistic, But Moderate

RCLCO National Market Sentiment Survey Results Part 1

Over the past three years, RCLCO’s National Market Sentiment Survey has reported the industry’s optimistic expectations for recovery, albeit not without plenty of roadblocks and setbacks along the way. In light of monumental demographic shifts on the horizon, uncertain government conditions, and Mother Nature’s unpredictability, this midyear 2014 installment of the Market Sentiment Survey indicates a vision that many of us have all but forgotten—steady, moderate growth.

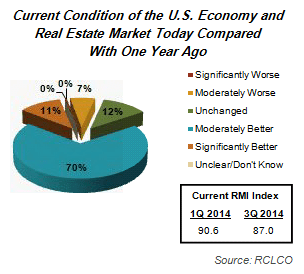

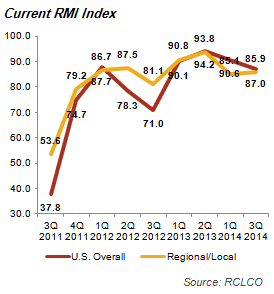

The current National Current Real Estate Market Index (RMI1) declined slightly to 87.0, indicating continued improvement in conditions, with 70% of respondents reporting that national economic and real estate market conditions are moderately better today compared with one year ago, and another 11% reporting that they are significantly better. Current Regional RMI held steady at 85.9, with 81% of respondents reporting moderately or significantly better conditions compared with one year ago.

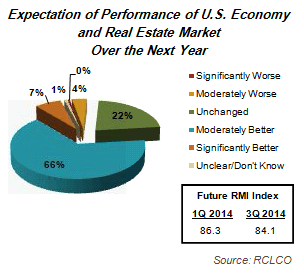

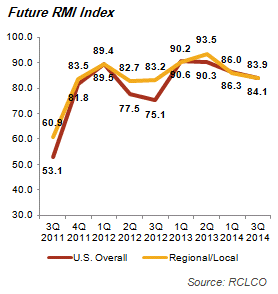

Future National and Regional RMI both declined modestly to 84.1 and 83.9, respectively. These RMIs represent the 66% of respondents who expect national and regional economic and real estate conditions to moderately improve over the next year, as well as the 22% of respondents who expect conditions to remain unchanged, compared with the just 9% who expected conditions to remain unchanged in 1Q 2013. In 2Q 2013, 14% of respondents expected significantly better national conditions in the next year, whereas only 7% of current respondents expect to see significant improvements in the next year. This leveling of expectations is what we would have anticipated as real estate moves through the cycle from recovery stages into a period of more steady, moderate growth ahead.

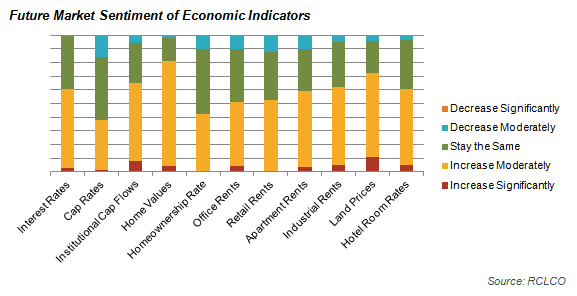

Respondents’ expectations for a wide variety of economic indicators also tell the story of positive, albeit moderate growth. In fact, 87% of respondents expect the following indicators to stay the same or increase moderately over the next six to 12 months: capitalization rates, institutional capital flows to real estate, office rents, retail rents, apartment rents, industrial rents, land prices, and hotel room rates. Expectations around home prices continue to be the most optimistic, with 80% of respondents expecting moderate to significant increases in the next six to 12 months—stay tuned for Part 2 of the Market Sentiment Survey Results next week for details on this and other trends in the for-sale residential industry.

As respondents expect the movement from recovery to moderate, steady growth to continue, it is no surprise that while 40% of respondents expect interest rates to stay the same in the next six to 12 months, 58% are expecting a moderate increase. This expectation also mirrors the Fed’s March statement announcing plans to further reduce bond purchases, and eliminate the “Evans Rule”: the historical use of a 6.5% unemployment rate as the target for raising interest rates. Interest rates will continue to be an important indicator to monitor, although we expect only gradual increases in the coming months.

Respondents’ predictions of steady, moderate growth suggest that many land uses have reached the early stable stage in the real estate cycle. With growing net operating incomes and prices, forward momentum in the marketplace, and more freely flowing capital, the early stable stage can often result in growth that is exceeding organizational capacity. This offers a strong opportunity to improve processes and efficiency within your firm, and ultimately capitalize on the growing opportunities across the industry. At the same time, it is important to become more selective on land acquisitions by increasing hurdle rates to eliminate marginal deals.

Rising Temperatures… and Coffee Prices

With record highs being reached throughout the world, the temperature isn’t the only thing heating up in the last few months—the debate on climate change has continued to be pushed towards the forefront. Even the Starbucks morning crowd is beginning to feel the heat—multiple sources report that the recent increase in Starbucks’ prices is attributable to the rising costs of Arabica beans caused by droughts in Brazil, which scientists believe to be induced at least partially by climate change.

A new “Risky Business” report, just released by a bipartisan team including former Treasury Secretary Henry Paulson, ex-New York Mayor Michael Bloomberg, and hedge-fund billionaire Tom Steyer, says that the effects of climate change go far beyond the price of a morning cup of Joe. The report focuses on climate change as an economic risk to U.S. businesses. The report estimates effects of climate change will cost the country billions of dollars over the next two decades.

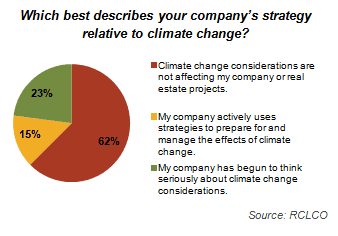

When we asked our industry contacts to best describe their company’s strategy relative to climate change, 15% of respondents report actively using strategies to prepare for and manage the effects of climate change. These strategies include green and sustainable development practices, water and energy conservation plans, use of LEED options, and use of carbon credits, among others. Another 23% of respondents report that their companies have begun to think seriously about climate change considerations, while the remaining 63% of respondents say that climate change considerations are not affecting their companies or real estate projects.

These survey results are consistent with what we are hearing as we work with our clients. Some see a market opportunity in positioning as a leader on environmental issues, while others plan to continue to monitor changing environmental regulations and respond accordingly.

Stay tuned next week for RCLCO’s National Market Sentiment Survey Results Part 2 to find out where we are in the cycle, and what the “new normal” may look like.

1The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of economic and real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate economic and real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Article and Research prepared by Len Bogorad, Managing Director, and Trish Kennelly, Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. RCLCO’s Strategic Planning and Litigation Support Advisory Group produced this newsletter. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/strategic-planning

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us