No News Is Good News: Stable Outlook Ahead

RCLCO National Market Sentiment Survey 3Q 2015 Results Part 1

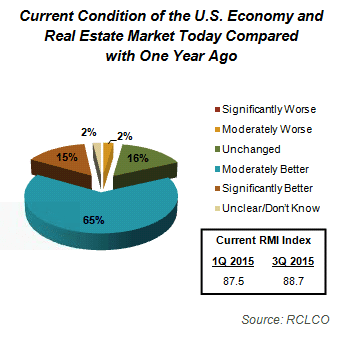

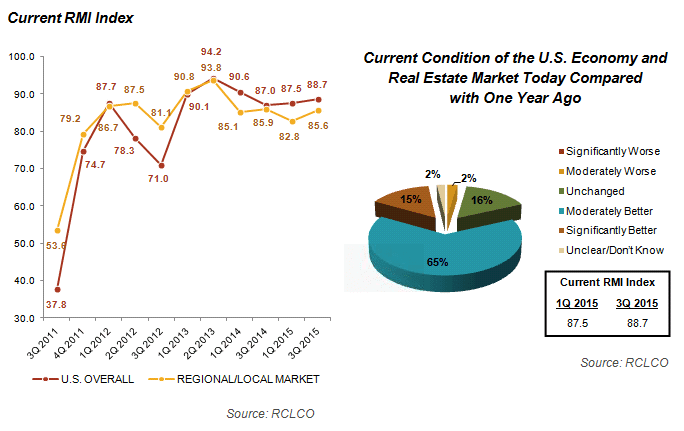

RCLCO’s latest Market Sentiment Survey results are in, and they paint the same story as they have for the past few years: moderate gains over the past year and cautious optimism for the year ahead. For the fourth survey in a row, respondents to RCLCO’s National Market Sentiment Survey report modest improvement in the national economy and real estate market over the past 12 months. Approximately two-thirds of respondents describe national conditions as “moderately better” today than one year ago, and another 15% report that national conditions are “significantly better.” Together these increase RCLCO’s National Current Real Estate Market Index (RMI1) a modest one point above the RMI from January 2015.

Local and regional sentiment is similarly positive: 49% report “moderately better” conditions today than a year ago and 30% indicate “significantly better” conditions. The positive perception restores the Local/Regional RMI to 2014 levels at 85.6, after a brief dip in sentiment six months ago (1Q 2015 RMI was 82.8).

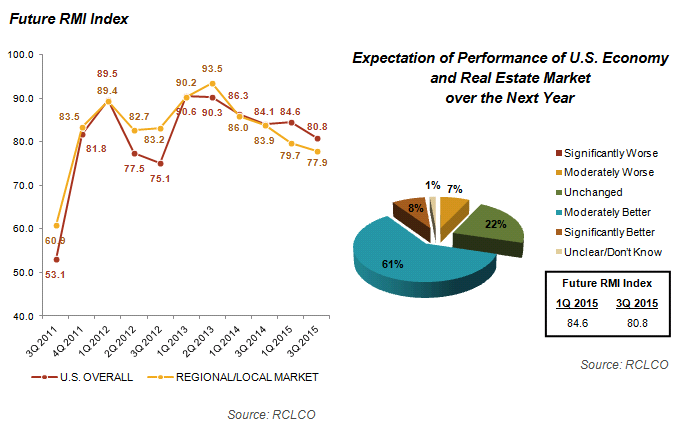

Looking forward, 61% of respondents anticipate national conditions to continue to experience modest improvement over the next year. Relative to 1Q 2015, however, a growing proportion of respondents anticipate unchanged national economic conditions one year from now: 22% expect growth to flat line over the next year, as compared with 14% in the previous survey. Expectations of unchanged conditions also gained share at the regional/local level, where 24% foresee no change in the regional/local economy, as compared with 20% six months ago, but these feelings are tempered by parallel growth in the proportion of respondents (17%) who predict “significantly better” regional conditions over the next year. In line with these changing sentiments, RCLCO’s Future Real Estate Market Index dropped slightly to 80.8 (-3.6) for national conditions and 77.9 (-1.8) for regional/local conditions. Overall, then, the theme of cautious optimism that has characterized respondent sentiment since 1Q 2014 continues to prevail, but with some increase in caution from one survey to the next.

Looking forward, 61% of respondents anticipate national conditions to continue to experience modest improvement over the next year. Relative to 1Q 2015, however, a growing proportion of respondents anticipate unchanged national economic conditions one year from now: 22% expect growth to flat line over the next year, as compared with 14% in the previous survey. Expectations of unchanged conditions also gained share at the regional/local level, where 24% foresee no change in the regional/local economy, as compared with 20% six months ago, but these feelings are tempered by parallel growth in the proportion of respondents (17%) who predict “significantly better” regional conditions over the next year. In line with these changing sentiments, RCLCO’s Future Real Estate Market Index dropped slightly to 80.8 (-3.6) for national conditions and 77.9 (-1.8) for regional/local conditions. Overall, then, the theme of cautious optimism that has characterized respondent sentiment since 1Q 2014 continues to prevail, but with some increase in caution from one survey to the next.

DC: Back on Track

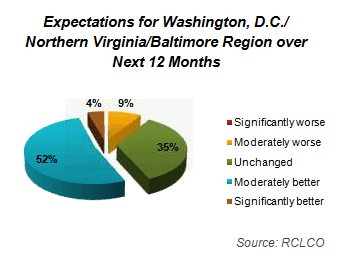

Sentiment among respondents who work primarily in the Washington, D.C./Northern Virginia/Baltimore region reported feeling more positive about current regional conditions than they did six months ago, which is consistent with much-improved job growth in the D.C. metropolitan area. Over one-half of respondents indicated that conditions are “moderately better.” As a result, the region’s Real Estate Market Index jumped 13.9 points from 60.0 to 73.9, restoring the RMI to 3Q 2014 levels after a brief but meaningful slump in sentiment in the last survey. This increase in RMI is not only an improvement in absolute terms but also relative to the change in the nation overall, whose current RMI only increased one point. However, the region’s current RMI is still well below the national RMI of 85.6. Over 40% of the region’s respondents anticipate continued moderate gains in regional performance. However, many remain reserved about the future, with 30% anticipating growth to flat line. Relative to sentiment in other regions, the capital region and Texas have the least positive one-year outlooks.

Sentiment among respondents who work primarily in the Washington, D.C./Northern Virginia/Baltimore region reported feeling more positive about current regional conditions than they did six months ago, which is consistent with much-improved job growth in the D.C. metropolitan area. Over one-half of respondents indicated that conditions are “moderately better.” As a result, the region’s Real Estate Market Index jumped 13.9 points from 60.0 to 73.9, restoring the RMI to 3Q 2014 levels after a brief but meaningful slump in sentiment in the last survey. This increase in RMI is not only an improvement in absolute terms but also relative to the change in the nation overall, whose current RMI only increased one point. However, the region’s current RMI is still well below the national RMI of 85.6. Over 40% of the region’s respondents anticipate continued moderate gains in regional performance. However, many remain reserved about the future, with 30% anticipating growth to flat line. Relative to sentiment in other regions, the capital region and Texas have the least positive one-year outlooks.

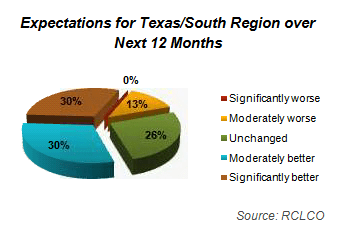

Texas: Split Opinions

Respondents from Texas are split regarding regional performance of late: approximately one-third reported unchanged or worsened conditions, one-third reported moderately better conditions, and one-third reported significantly better conditions. Expectations for the next year follow the same pattern, although the percentage of respondents who anticipate unchanged conditions increased to 26%. Overall, the Texas current RMI fell somewhat to 73.9 (-5.3), which interestingly is the same level as the RMI for the Washington, D.C., region, although a much higher percentage of Texas respondents (30% vs. 4% in the D.C. area) expect significantly better conditions.

Respondents from Texas are split regarding regional performance of late: approximately one-third reported unchanged or worsened conditions, one-third reported moderately better conditions, and one-third reported significantly better conditions. Expectations for the next year follow the same pattern, although the percentage of respondents who anticipate unchanged conditions increased to 26%. Overall, the Texas current RMI fell somewhat to 73.9 (-5.3), which interestingly is the same level as the RMI for the Washington, D.C., region, although a much higher percentage of Texas respondents (30% vs. 4% in the D.C. area) expect significantly better conditions.

When Will Things Turn South?

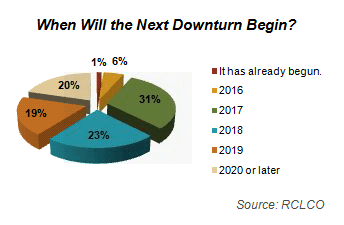

Simply put, there is no consensus among respondents on the timing of the next national downturn, although everyone agrees that it has not yet begun. The largest share of respondents anticipates the next downturn to begin in 2017-2018. Even so, a full fifth of respondents expect the market to continue to grow until 2020 or later.

Even when analyzing responses at the regional level, there is little agreement on the timing of the next downturn. Respondents who work primarily in Texas, the South (excluding Florida), and Washington, D.C., tend to be comparatively optimistic about timing, with only about one-third estimating an earlier (2016-2017) downturn, while two-thirds expect to avoid a downturn until at least 2018. Respondents working in Florida and the Midwest stand out as being slightly more cautious, with closer to one-half of respondents in these regions anticipating a downturn in 2016-2017.

Even when analyzing responses at the regional level, there is little agreement on the timing of the next downturn. Respondents who work primarily in Texas, the South (excluding Florida), and Washington, D.C., tend to be comparatively optimistic about timing, with only about one-third estimating an earlier (2016-2017) downturn, while two-thirds expect to avoid a downturn until at least 2018. Respondents working in Florida and the Midwest stand out as being slightly more cautious, with closer to one-half of respondents in these regions anticipating a downturn in 2016-2017.

Overall, it feels like somewhere in the middle innings of a ballgame that may or may not have a long time more to go. Experience teaches us that this is the stage of the cycle to be thinking about and putting in place strategies and contingencies for the inevitable eventual market downturn, which can happen on a dime. In past downturns, companies that prepared not only survived the last downturn, but thrived by taking advantage of opportunities that others could not, and were early movers in the upswing. Companies that were complacent about the good times, or assumed there was nothing they could do once things did turn down, did not fare nearly as well.

Up Next: Keep an eye out for Part 2 of the results from RCLCO’s latest National Market Sentiment Survey in mid-July as we take a closer look at where different real estate products are in the market cycle. We will also share what we learned about respondents’ use of EB-5 and their opinions about the program.

1 The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of economic and real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate economic and real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Article and Research prepared by Len Bogorad, Managing Director, and Clare Healy, Associate.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. RCLCO’s Strategic Planning and Litigation Support Advisory Group produced this newsletter. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/strategic-planning

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us