Ready for Changing Tides? How Real Estate Companies Can Prepare for a New Cap Rate Era

Three Things to Know

- For the past two decades, the real estate industry has been almost singularly defined by declining cap rates: since 2000 cap rates have declined on average by 400 basis points.

- Market indicators suggest that the declining cap rate era is approaching its end and that moderate cap rate expansion is likely.

- Successful real estate companies will adapt their investment paradigm to this new market context heeding the need to: focus on operations, build organizational flexibility, and leverage data in making informed choices.

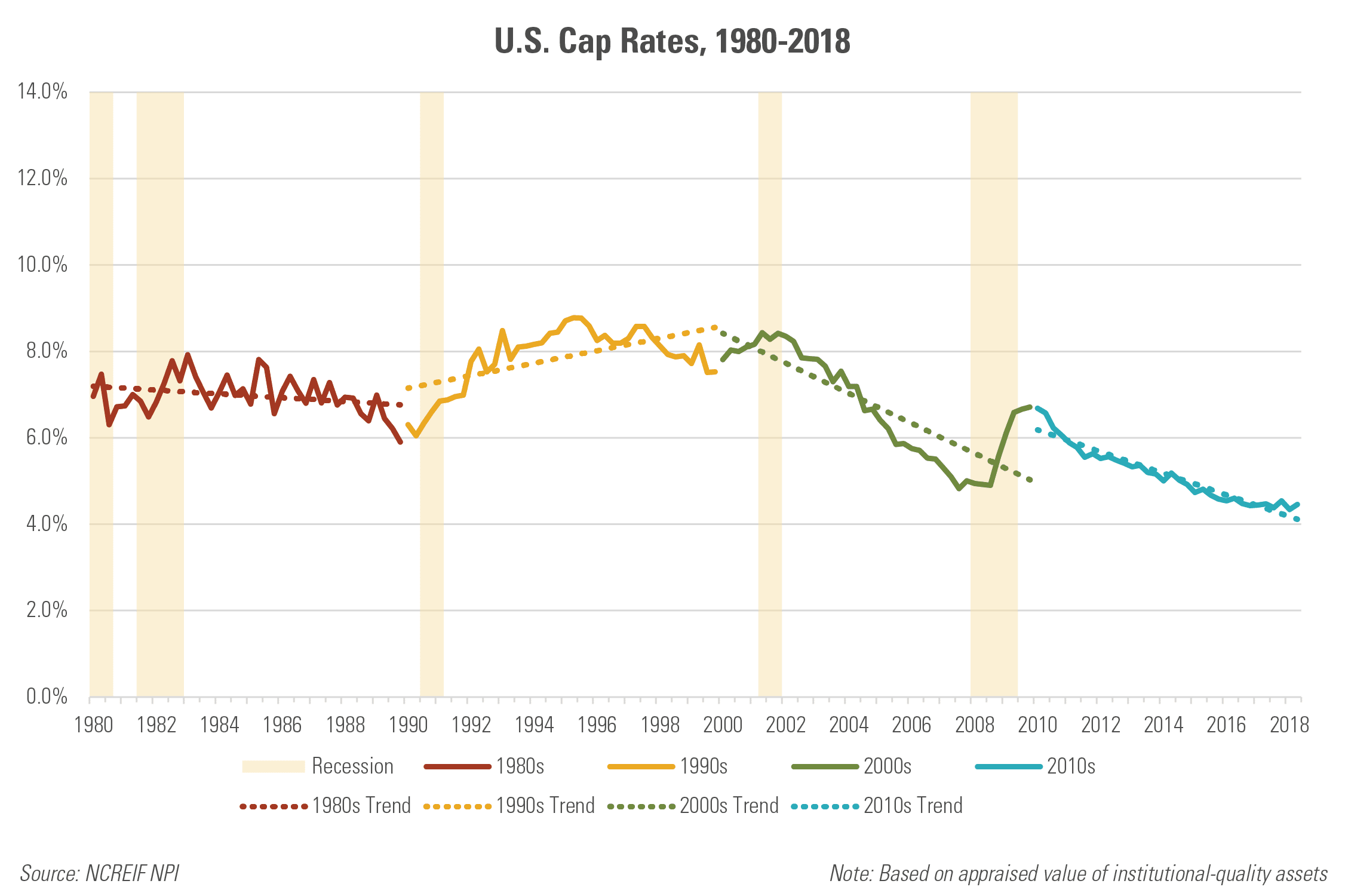

For real estate investors, the past two decades have been a period of dramatic and rapid cap rate compression. At the turn of the millennium, cap rates for institutional assets peaked at 8.4%; today, the same bucket of assets is appraised at an effective cap rate of 4.4%. The 400 basis points of cap rate compression has been a bonanza for investors across property types and geographies: the value of an identical cash flow stream has increased by 75% over this period even after accounting for inflation.

These strong tailwinds, though, are dissipating, and most indicators suggest that the two decade-long era of persistent cap rate compression is at or near its end. For investors and operating companies, the departure from a market context in which cap rate compression is the norm demands an equally significant shift in the operating paradigm.

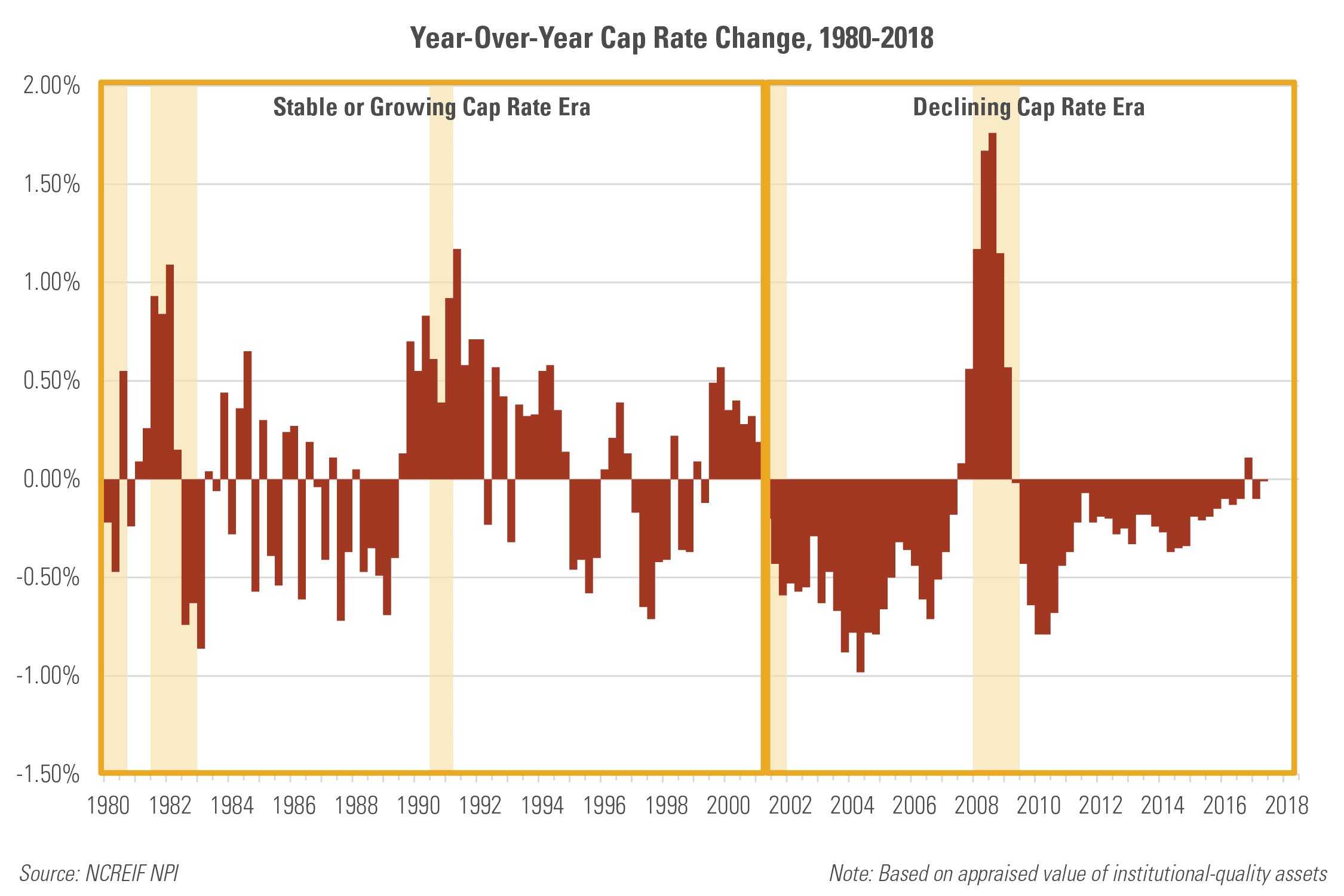

As the contemporary institutional real estate industry took shape in the 1980s, cap rates hovered steadily around 7% despite rapidly declining interest rates and economic growth. Following the recession of the early 1990s, cap rates entered a moderate expansionary period peaking at just below 9% in 1995. Throughout these two decades, cap rates stayed within a relatively tight 250 basis points band with little systemic trend up or down: roughly half the time, cap rates showed a year-over-year decline (53%) and half the time cap rates increased (47%).

Beginning in the early 2000s, the real estate market entered a dramatically different era: over the following 18 years, cap rates declined by 400 basis points peak-to-trough. The cap rate declines were driven by a number of factors (many unlikely to repeat in the coming years) including declining interest rates and the increased volume and sophistication of institutional capital in the sector. The Great Recession was a period of dramatic, but temporary, cap rate expansion. And, removing the Great Recession – a notable exclusion – cap rates declined year-over-year in all but one quarter between 2001 and today.

Given current market fundamentals, the pattern of the last two decades is unlikely to repeat itself and investors face the imperative to adapt accordingly. Market forecasters and industry participants nearly universally anticipate cap rate declines to reverse themselves over the near-term, and monetary policy and interest rate forward curves suggest the market has reached a cap rate floor with little room for a continued decline. While the future is predictably unpredictable, investors can be confident that the dramatic cap rate compression of the most recent era was a singular event and that the real estate industry is entering an era of either flat or expanding cap rates.

Strategy Implications

The end of a declining cap rate era fundamentally changes the nature of the real estate industry and the method of value creation. The best real estate companies will adapt to the new paradigm, building a business around the following pillars in a market experiencing limited cap rate compression.

- Focus on the Operations: Since 2000, cap rate compression has been a primary source of value creation for real estate investors, at times overshadowing the importance of the nuts and bolts of operating real estate. Leaving a period in which cap rate compression can “save” a deal, successful companies will find a way to build a competitive advantage in the marketplace through soft and hard product and service offerings that demand a premium.

- Build Organizational Flexibility: Steady or expanding cap rates create intense pressure on real estate organizations – unsurprisingly, periods with the highest number of defaults and foreclosures overlap neatly with periods of rapid cap rate expansion. In order to manage a sustained period of flat or expanding cap rates, companies will develop internal flexibility to shift resources and focus attention on different organizational needs as the market context changes. Investment in developing strong asset and property management skillsets is especially impactful. Organizations that have developed nimble structures and processes are best positioned to capitalize on these shifts.

- Leverage Data in Making Informed Choices: In the face of a changing cap rate paradigm, developing enhanced rigor around investment and operational decisions will be a key differentiator for real estate companies. Companies that effectively integrate systems to operationalize proprietary data and market data will be able to identify opportunities more quickly and adjust to adverse conditions in a way that best mitigates exposure.

RCLCO regularly helps companies develop proactive strategies and position themselves to capitalize on changing market contexts including a new cap rate paradigm. For more information, contact RCLCO’s strategy planning and management consulting team.

Notes

Cap rates, or capitalization rates, reflect the rate of return on a real estate asset. The rate is calculated by dividing property Net Operating Income (NOI) by the asset’s value.

Article and research prepared by Eric Willett.

RCLCO’s mission is to help clients make strategic, effective, and enduring decisions about real estate. We proudly celebrate more than 50 years of providing the best minds in real estate with cutting-edge analytics, actionable advice, and the highest level of customer service. Our work includes market, economic, financial, and impact analyses; investment portfolio strategy and implementation; entity-level strategic planning; and management consulting.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us