In-Depth Look at Top-Selling MPC’s

RCLCO recently reported that year-to-date 2012 home sales at top master-planned communities are the strongest in three years, up sharply over 2011 (RCLCO Advisory, March 29, 2012). In this new and expanded Advisory we further explore the strategies the top MPCs are using to accomplish those stronger sales. An updated version of our original MPC Advisory is included below as Part 1, followed by Part 2 which further explores the key themes in greater depth, and Part 3, an interview with Robert McLeod, the founder and visionary behind the growth and evolution of community developer Newland. Part 4 lists some of the trends RCLCO and its client’s are monitoring for the future.

Part 1: Master-Planned Communities Are Achieving Stronger Sales

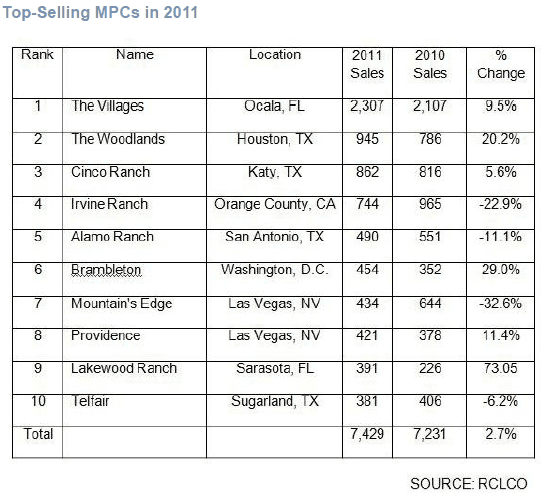

(The following is an updated and expanded version of our March 29, 2012 Advisory) Year-to-date 2012 home sales at top master-planned communities (MPCs) are the strongest in three years, up sharply over 2011. It appears that the recovery has finally come to MPCs. Every year since 1994, RCLCO has conduct- ed a national survey identifying the top-selling MPCs, followed by in-depth interviews among the top 20 to reveal the trends behind the numbers. Although our research shows that sales in 2011 were not universally stronger than in 2010, most MPCs report that year-to-date sales for 2012 are up substantially. A majority of the communities are optimistic that this is a trend, not a blip. Most of the top-selling MPCs report that in 2011 and early 2012 they are seeing a deeper buyer pool with better credit. Buyers that have been sitting on the sidelines for the past few years are feeling more secure about buying, and they’re back in the market now that the future economic outlook seems a little clearer. Meanwhile, MPCs are also finding that they’re competing with a lower volume of short sales and foreclosures in their projects compared with last year.

In 2010, sales were starting to improve but there was no confidence that a good month or two of sales indicated a trend. In 2011, the pattern of consistently improving sales became more pronounced, and 2012 has been even stronger. In 2011, there was an even stronger flight to quality than in 2010, pushing MPC market share higher as both builders and consumers believed MPCs were safer places to invest in lots and homes. Now those buyers are showing up in greater numbers.

It’s important to look at both the circumstances behind increased sales and the proactive strategies participants have employed to bolster their sales. Certainly the improving economy and job growth are major factors, with communities near job centers noting the correlation between their sales and employment growth in those areas. However, through our interviews RCLCO has identified key themes that have led to the success of the top-selling MPCs that are worth considering for MPCs that are still struggling to recover, as well as for future planned communities. Admittedly, some of the critical success factors (such as being a mature community) cannot be replicated by new MPCs, but many indicate what it takes to succeed in the current environment. This article focuses on some of the key strategies MPCs have used that we believe will help other existing and new MPCs be more successful as the market recovers.

Strategies that Increase Sales

Although there are many things master-planned communities have done to enhance their success, it’s rare that success happens overnight. In fact, all of the top-selling MPCs started before the recession. In many cases this allowed them to realize a level of critical mass in terms of product in place, landscaping, and amenities, and a prior track record of success that helped both their builder customers and homebuyers feel more secure about investing in the community. Their low land basis from having purchased the prop- erty pre-real estate boom also gave them more pricing flexibility.

Many of the best-selling communities also have favorable locations relative to major job centers. That may be harder to replicate in the future, at least at a large scale, given lack of available land near job centers in most major metropolitan areas. However, new developments can include a broader range of commercial uses and incorporate a job center within the project. It’s also likely that these new communities will be smaller in scale on sites that enjoy closer proximity to existing job centers.

Although there has been less family-oriented household growth in recent years, new and existing families are still one of the most important market segments for MPCs. Therefore, being close to, or including, good schools remains one of the keys to high sales. MPCs influence school quality by choosing locations where good schools already exist, or through providing sites for new schools, facilitating the creation of charter schools, or recruiting private schools. We’ve also observed that as quality MPCs attract new families into existing schools, test scores (viewed by many buyers as a measure of school quality) often improve.

Some critical success factors are easier for developers and builders to replicate or influence than others. Some of the more proactive strategies we’ve seen used by the top communities include:

- Product innovation – Developers and builders in top communities have recognized that to compete with the overhang of “recently new homes” and distressed resales, their product not only needs to be competitively priced, it really needs to be a new product. That means the product is not just new relative to year built, but truly better, with floor plans that better address how people want to live, including better technology, greater energy efficiency, and new spaces in the plans.

- Product availability – Critical to the success of top-selling MPCs is their ability to provide an inventory of speculative homes across multiple price points and orientations. Most buyers are not willing and/or able to wait for a home to be built, but even the best MPCs are still struggling to carry speculative inventory as many builders remain cautious.

- Marketing – Most MPCs report an increase in use of social media as well as finding other innovative, cost-effective ways to stay top-of-mind with consumers. All of the most successful communities have taken a careful look at where they’re spending marketing dollars and where they are having the greatest success and have made adjustments, in many cases accomplishing more with less.

- Strategic Investments – Top-selling MPCs continued to invest in amenities, marketing, programming, and maintenance throughout the downturn, which gave buyers confidence and allowed them to capture the buyers that were looking in 2011 and 2012.

- Lifestyle – As with good quality schools, this major differentiator between the best-selling communities and their competition hasn’t changed since we started our survey in 1994. Buyers choose MPCs because they deliver the right amenities, services, schools, and retail that provide the desired great lifestyle.

- New business lines – Many MPCs have also creatively sought other ways to generate income, including expansions into multifamily, business parks, assisted living facilities, and other types of vertical development in order to help them weather the downturn.

- Incentives – Some of the MPCs are offering buyer incentives such as free power for a year and $1,000 gift cards at Bridgeland in Houston, and a year membership at the new Sports and Health Club at Brambleton in Northern Virginia.

- Helping with financing – Successful MPCs have been helping both builders and homebuyers get credit throughout the downturn. With builders this includes subordinating the cost of the lot until the house is sold, and with consumers it includes items such as credit coaching. Among those MPCs that still cater to first-time or entry-level buyers, credit coaching, coordinated by the builders, has been key to lowering the “bust-out” rate (rejection rate) of first-time buyers seeking credit. The bust-out rate has decreased when credit coaches have been engaged by builders to work with prospective buyers to raise credit scores to acceptable levels. Lending standards are still difficult for would-be homebuyers, and the builders in top-selling communities are helping them get the counsel needed to raise scores.

While it’s clear that many of the keys to success in MPCs are similar to what worked in the past (good schools, desirable lifestyle, multiple product lines), there are proactive strategies that developers and builders are employing, as listed above, that have had a substantial impact on their sales success. Part 2, below, explores these strategies in greater depth:

Part 2: In-Depth Look at Key Strategies for Achieving Stronger Sales

Product Innovation

One of the proactive strategies we’ve seen used by the top communities includes product innovation. Developers and builders in top communities have recognized that to compete with the overhang of “recently new homes” and distressed resales, their product not only needs to be competitively priced, it really needs to be a new product. That means the product is not just new relative to year built, but truly better, with floor plans that better address how people want to live, including better technology, greater energy efficiency, and new spaces in the plans.

Both builders and developers have clearly done their homework throughout the recession and new home designs today are some of the best we’ve seen in years, born of necessity. In order to sell new product, builders cannot simply offer the same house as the short sale down the block or in the neighborhood across the street. They have had to truly innovate new home designs. From the top-selling MPCs, this has taken three forms: one, offering a completely new product type, two, rethinking the floor plans of traditional product to meet today’s lifestyles, and three, making the home more energy efficient.

At Brambleton, outside of Washington, D.C., they offered two new products, a 2 over 2 that allowed them to fully utilize all the square feet in the home in an effective manner. It also allowed them to hit a price point in the D.C. area that was attractive to buyers. In addition, they introduced a Boston Brownstone Townhome that buyers have really liked.

At Brambleton, outside of Washington, D.C., they offered two new products, a 2 over 2 that allowed them to fully utilize all the square feet in the home in an effective manner. It also allowed them to hit a price point in the D.C. area that was attractive to buyers. In addition, they introduced a Boston Brownstone Townhome that buyers have really liked.

In Telfair, located in Sugar Land, Texas, the builders have offered a larger multigenerational product, strategically targeting the multigenerational and international buyers who have recently been a larger segment of the market. Builders are responding to the different cultural norms that result from the region’s diversity, including such features as secondary kitchens, popular with South Asian home buyers. According to Jennifer Taylor from Newland, “our builders have been very successful in meeting the consumer with targeted product such as prayer rooms, dirty kitchens, and dual master bedrooms on the first floor.” Although such features are not the norm in most floor plans, by offering these attributes to select plans builders are able to capture additional new homebuyers for whom these are very important additions.

Builders are responding to the different cultural norms that result from the region’s diversity, including such features as secondary kitchens, popular with South Asian home buyers. According to Jennifer Taylor from Newland, “our builders have been very successful in meeting the consumer with targeted product such as prayer rooms, dirty kitchens, and dual master bedrooms on the first floor.” Although such features are not the norm in most floor plans, by offering these attributes to select plans builders are able to capture additional new homebuyers for whom these are very important additions.

Irvine Ranch on the other coast in California has spent significant time and money understanding what their consumers want in their homes. Key new features they have focused on in 2011 that have had a big impact are the outdoor “California Room” and big open entertaining spaces. They have learned that buyers don’t require 3,000 square feet; they just need a great house that fits their lifestyle (for the typical Irvine customer that equals three to four bedrooms with ample entertainment space). In addition to providing updated floor plans, Irvine Ranch has taken it a step further with helping homebuyers. They have designers that help buyers with everything from electrical, rooms, countertops, paint colors, and flooring. Therefore, while they are still production homes, they allow the consumer to customize the home as much as possible with thousands of options from which to choose. They have found this to be a key experience for buyers right now as it adds a very interactive, personal touch to the home buying process.

Focus Property Group has developed best sellers Mountain’s Edge and Providence in Las Vegas, which have both maintained their position among the 10 Top-Selling Master-Planned Communities produced by RCLCO every year. John Ritter, Focus Property Group founder and CEO, said marketing for the commu- nities has been fine-tuned, including utilizing more in the way of social media relative to traditional print advertising. He also credits the builders for adapting to market changes. “Our builders have successfully retooled their floorplans and pricing and differentiated their product from resales with environmentally conscious and energy efficiency features,” he said. “For example, KB Home has developed its ZeroHouse 2.0 and Pardee Homes, LivingSmart homes. Part of their sales pitch is a direct cost comparison of an older house versus the new house. New homes clearly beat resales in energy efficiency.” Ritter also cited Lennar’s Next Gen homes which allow extended families to live together in one home with separate living spaces.

Product Availability

Critical to the success of top-selling MPCs is their ability to provide an inventory of speculative homes across multiple price points and orientations. Most buyers are not willing and/or able to wait for a home to be built, but even the best MPCs are still struggling to carry speculative inventory as many builders remain cautious.

The good news for MPC developers is that builders are once again buying lots on a regular schedule and in bigger quantities, and many of the large, national builders are aggressively trying to tie up lot positions within the top-selling projects. One of the issues that continues to be a challenge for most of the top-selling MPCs is the struggle to get builders to build speculative inventory, which is tough to do when they are concerned about inventories already. However, it’s hard to compete with left over inventory from the last building cycle unless homes are move-in ready. Buyers are not typically willing or able to wait. Most surveyed MPCs report that distressed inventories in their communities are significantly down, exerting much less competitive influence on their new sales than in the past, however, they still believe they are losing sales to buyers who need a home immediately.

In many markets, builders are still having trouble getting construction loans on homes without a buyer, therefore making it more challenging to build speculative product. Banks are requiring them to put down more equity which is hurting their returns. In turn, some of the MPC developers are helping the builders by reducing the amount of deposit they are requiring on the lots and/or subordinating lot sales to builders, i.e. taking a second position behind the construction loan, with builders paying for the lots as the homes are sold. Alternatively, some developers have offered lots at a discounted price and participated in the sales price of the final product (base price and true-up later), but that has been less of a trend.

The interviewees all agreed that having product available in multiple price points was critical to achieving high levels of sales. Lakewood Ranch in Sarasota, Florida works with 18 different builders to offer mul- tiple product lines and price points. According to Jimmy Stewart, Vice President of Sales at LWR, “having a property as large as ours (48 square miles) certainly lends itself to the flexibility of product segmentation. From modest multi-family residences to grand estates, we are able to offer products from the high $100s to $4 million- plus and all price points in between. The resultant financial and architectural spectrum creates the opportunity to broaden our market considerably, thus enhancing sales”. Most of the top-selling MPCs still put a strong focus on product differentiation and segmentation. In the past, neighborhoods were typically segmented based upon home price and lot size and, to a lesser extent, by buyer segment and orientation. A newer trend in MPCs is to offer a wider product array targeting niche buyers, including targeting homebuyers by age and/or ethnicity. Tefair is an example of targeting ethnic buyers as described above, and Riverstone and Sienna Plantation, also in Fort Bend County, Texas, are tweaking product types to appeal to an increasingly diverse buyer population.

The interviewees all agreed that having product available in multiple price points was critical to achieving high levels of sales. Lakewood Ranch in Sarasota, Florida works with 18 different builders to offer mul- tiple product lines and price points. According to Jimmy Stewart, Vice President of Sales at LWR, “having a property as large as ours (48 square miles) certainly lends itself to the flexibility of product segmentation. From modest multi-family residences to grand estates, we are able to offer products from the high $100s to $4 million- plus and all price points in between. The resultant financial and architectural spectrum creates the opportunity to broaden our market considerably, thus enhancing sales”. Most of the top-selling MPCs still put a strong focus on product differentiation and segmentation. In the past, neighborhoods were typically segmented based upon home price and lot size and, to a lesser extent, by buyer segment and orientation. A newer trend in MPCs is to offer a wider product array targeting niche buyers, including targeting homebuyers by age and/or ethnicity. Tefair is an example of targeting ethnic buyers as described above, and Riverstone and Sienna Plantation, also in Fort Bend County, Texas, are tweaking product types to appeal to an increasingly diverse buyer population.

Stapleton in Denver, Colorado has experienced the trend of empty nesters moving to Stapleton to be near their children and grandchildren. According to Heidi Majerik of Stapleton, “they are looking for a low maintenance, main floor master, single-family detached product. Providing that product in our small lot program has been a challenge. We have recently found a small regional builder in Colorado who has solved this problem. They offer a ranch with a finished basement on a 45’ wide by 90’ deep lot that includes front yard and ex- terior maintenance through a home owner’s association that appeals to the 55+ buyer.” They will be launching this new product at Stapleton in the fall.

Stapleton in Denver, Colorado has experienced the trend of empty nesters moving to Stapleton to be near their children and grandchildren. According to Heidi Majerik of Stapleton, “they are looking for a low maintenance, main floor master, single-family detached product. Providing that product in our small lot program has been a challenge. We have recently found a small regional builder in Colorado who has solved this problem. They offer a ranch with a finished basement on a 45’ wide by 90’ deep lot that includes front yard and ex- terior maintenance through a home owner’s association that appeals to the 55+ buyer.” They will be launching this new product at Stapleton in the fall.

Last year RCLCO had reported that prior to the downturn, most MPCs had a large number of product lines targeting a broad range of home buyer segments. However, as the housing boom pushed prices higher across all regions of the country, many MPCs strayed from their segmentation models, providing larger and larger homes and higher prices. Many MPCs were left without a lower-priced, entry level product. Even those with some segmentation between neighborhoods were providing segmentation primarily at the higher price points. RCLCO has found that revisiting segmentation strategies has been one of the keys to improving sales during the downturn. Interviews in 2011 confirm this trend. Many of the top-selling MPCs introduced lower-priced and/or different product to attract the entry-level buyer. Examples include the Twin Villa (essentially a duplex), a relatively new product at Cinco Ranch in Katy, Texas. It has done very well at the $140,000-$150,000 range, as a good entry-level product.

Marketing

Most MPCs report an increase in the use of social media as well as finding other innovative, cost-effective ways to stay top-of-mind with consumers. All of the most successful communities have taken a careful look at where they’re spending marketing dollars and where they are having the greatest success and have made adjustments, in many cases accomplishing more with less.

Marketing has been a key differentiator among top-selling projects. Each one of them has been able to maintain their market presence during the downturn. In addition, most of them have been re-focusing their efforts with less dollars, less print, more social media, more programming, and increased internet adver- tising. Focus Properties with both Mountains Edge and Providence is a prime example of this. They have fine-tuned their marketing efforts with fewer dollars. According to John Ritter of Focus Property Group, “We have maintained our ‘experiential marketing’ by providing events throughout the year that generate traffic. The programs are not only amenities for residents of our master plans, but also opportunities for their friends and residents throughout Southern Nevada to become familiar with our communities and have a positive association with them.”

Another example of more social media is at Bridgeland where they have developed numerous, profes- sionally filmed You-Tube videos which are prominently displayed on their website and show not only the natural beauty of the community, but also the way the community lives by highlighting scenes from com- munity events. Peter Houghton, Vice President of Master-Planned Communities, says that “we have found YouTube ads and social media are very effective tools for Bridgeland since they allow us to post pictures and articles that are forwarded by the viewers to multiple recipients at no cost to the developer”.

Bridgeland, in Houston, Texas, also coordinates community events such as its annual dog-themed Howl-OWeen Fest and annual Nature Fest, both of which draw from a large area well beyond the community itself. Bridgeland hosts the festivals’ activities among its ubiquitous parks and lakes which allow it to showcase these significant differentiators of the community.

Bridgeland, in Houston, Texas, also coordinates community events such as its annual dog-themed Howl-OWeen Fest and annual Nature Fest, both of which draw from a large area well beyond the community itself. Bridgeland hosts the festivals’ activities among its ubiquitous parks and lakes which allow it to showcase these significant differentiators of the community.

Another key trend is the use of Customer Relationship Management (CRM) tools. Newland, with both Cinco Ranch and Telfair on the list, have been more focused on customer outreach, using sophisticated CRM tools to help them maintain a conversation with their prospects. Irvine Ranch also maintains a strong database of active shoppers, segmented by income, to whom they send frequent emails. This allows them to target and communicate with future buyers appropriately (e.g. they won’t send a potential townhome buyer an announcement about a new luxury community opening). In addition, they use Pinterest, a pinboard-styled social photo sharing website. The service allows users to create and manage theme-based image collections. The site’s mission statement is to “connect everyone in the world through the ‘things’ they find interesting.”

Top-selling MPCs still have sales centers, many of which have been re-tooled in the past year. At Newland, they like to hire residents for their information centers, believing it makes for a more genuine experience. At Nocatee in Jacksonville, Florida they utilize the sales center to get buyers interested in the project and qualify them to be sent to specific builders in the project. At Bridgeland, Sienna Plantation, and Riverstone, the developers are proactively coaching builders on selling community to complement the efforts at the sales centers.

At Irvine Ranch they recently opened Irvine Pacific’s Design Center, a 6,700 square foot stand-alone space in Woodbury Town Shopping Center. It is used primarily for those that just purchased a home to help design the new home as described above. While not a traditional sales center, they often use the center for prospective buyers by holding events there. In addition, the design center does travelling events. They recently sponsored a cooking event in each of the models in a new community where they partnered with the appliance manufacturers to show them off.

Part 3: An Interview with Robert B. McLeod, Chairman and Chief Executive Officer, Newland Communities

The following is an interview with Robert B. McLeod, the founder and visionary behind the growth and evolution of Newland becoming one of the largest privately held community developers in the country. Under Robert’s leadership, Newland and its affiliates have developed, acquired, completed, and managed for third par- ties a combined total of more than 140 projects, including many of the Top-Selling Master-Planned Communities.

RCLCO: How many times have we heard that as a result of the Great Recession, “everything has changed” – in your view, did the recession change the MPC de- velopment model, in terms of the relationships among land, talent (developer), builder, debt, and equity? If so, what does that mean for the future of the MPC?

McLeod: In general, each party in planned community developments will expect more input as they work to control their own destiny. Equity partners have shifted from long-term pension funds and life companies, who were more removed from the day-to-day operations, to short horizon, actively engaged private equity and/or international investors. These new investor types also want significantly more reporting, and more interaction with management and operations. Debt providers will also be looking for more in the way of reporting and oversight.

With a new set of investor partners, our teams have adapted to these changes, sometimes requiring them to adhere to a slightly different set of parameters and management goals. There’s some learning initially. We don’t think this impacts at all our ability to create great places to live and work.

It has changed the relationships among our teams as well. We find we are working across disciplines even more than ever now, making sure we bring to bear all perspectives on key decisions, earlier in the process, from operations (what’s the land tell us, what’s possible from a jurisdictional perspective, what’s the best approach to development phasing), marketing (how do customer needs and changing priorities affect how people live and what we create), finance (what are the financial impacts, good and bad, of the proposed approaches, and how do we feel about our assumptions, considering market, consumer and competitive factors).

From a land perspective, we no longer look at large scale MPCs and plan ahead for “replacement product”. We now ask ourselves, even though we are a development company, does it make more sense to look for a builder partner and bulk sale a certain area? We also believe it makes sense to plan the future phases in smaller land areas, allowing for product flexibility as things continue to change.

RCLCO: It appears that Newland did fairly well through the downturn. Overall, our interviews over the past several years indicate that sales for top performing MPCs began to stabilize in 2010, reversing a severe downward trend that began in 2006/2007. Total sales for the top ten communities was higher in 2011 than in 2010, but still far below the peak of 22,000+ homes sales that took place in 2005 in the top 10. What surprised you the most about the market in 2011?

McLeod: In 2011, I think we were surprised by the slowing of some markets halfway through the year, and the robust nature of some others. Results were surprisingly strong in some markets, but disappointing in others. Overall we saw 2011 start at a relatively stronger pace, although last year’s Spring season did not materialize as everyone initially thought, plus the world economy was further challenged by major events, such as the Japanese earthquake and tsunami and events in Europe and the Middle East. We know it will be bumpy along the way through recovery—that we can expect.

RCLCO: As a group, did your MPC’s meet, exceed, or fall short of expectations?

McLeod: Overall, our communities met our expectations for 2011, with several communities exceeding our goals for the year. We had some product lines perform differently than expected, meaning we thought they would appeal to a certain buyer group and they ended up appealing to a mix of buyers.

RCLCO: Have you calculated the percent of market sales were you able to capture? Is this more or less than in years past?

McLeod: Yes, we closely track our market share in each of our active markets and submarkets. The majority of our communities have continued to increase market share over the years, with several communities more than doubling market share during the last five years. This is an overall trend we’ve seen—welllocated MPCs are performing better than overall.

RCLCO: Can you point to key strategies, initiatives, external events, etc. that attributed to your sales in 2011?

McLeod: A large part of the success we’ve had in 2010 and 2011 has been due to the groundwork we laid following the downturn—the repositioning, re-segmentation, re-pricing, and rebranding exercises that many of our communities underwent. We truly aligned our focus on the customer across all areas of our business, and it impacted not just our builder product, but in some communities we totally changed our community presentation approach, or the amenities we built. We looked at the work we did, and made sure we applied it holistically throughout our community development, not just to the home product. That earlier work in 2008 and 2009 contributed to later successes in 2010 and 2011.

RCLCO: The majority of our MPC survey respondents believe that 2012 is going to deliver moderate increases in home sales and home prices. For 2012, how would you define your expectations for the housing market in general and specifically for the areas where you have developments—Optimistic, Moderately Optimistic, Neutral, Pessimistic?

McLeod: I think we’re optimistic—optimistic, but realistic—for 2012. The early results for 2012 have been very positive so far.

RCLCO: We are hearing that year to date 2012 MPC sales are up from 2011 already. As a group, what have Q1 2012 sales looked like for your MPCs? Has this influenced your perspective on sales and pricing for the coming year?

McLeod: For most of our active communities, our home sales so far this year are exceeding 2011 levels. We expect 2012 home sales to be near or slightly above last year.

RCLCO: We are still hearing that few builders are back to buying in bulk. Is that true in your communities overall, or are you seeing regional differences?

McLeod: We’re still seeing builders purchase in smaller rolling take downs. We are seeing builders increasing the number of lots they want per takedown, though they are not at the large lot positions per takedown they were before the downturn. They definitely are increasing their volume though, and in some markets, like the west side of Houston, and parts of Tampa, we’re seeing builders jockeying to secure land positions in a greater way than we have the last few years.

RCLCO: How are builders buying lots? Developed, raw, entitled?

McLeod: Builders are purchasing finished lots (entitled and developed).

RCLCO: Have lot prices begun to stabilize?

McLeod: We’re finding stabilizing or increasing lot prices in markets which have had time to work through the correction and good locations and submarkets. If you look at the supply of finished lots in the stron- gest submarket and strongest markets, that’s where you’ll see stabilized, and even increasing, lot prices.

RCLCO: Are you planning any new projects?

McLeod: Yes, we’ve been very busy planning new communities that we plan to open over the next 18 months. We’ll grand open two new communities later this year. Waterset is a new community located in the Apollo Beach area of South Hillsborough County in Tampa, Florida. We had to push back the start of this community because of the downturn, and now are getting ready to open this year with a redesigned plan, new products and buil

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us