Evaluating the Top-25 Most Active Markets: A Look at Single-Family Housing Momentum

U.S. Metro Areas Driving the Housing Market

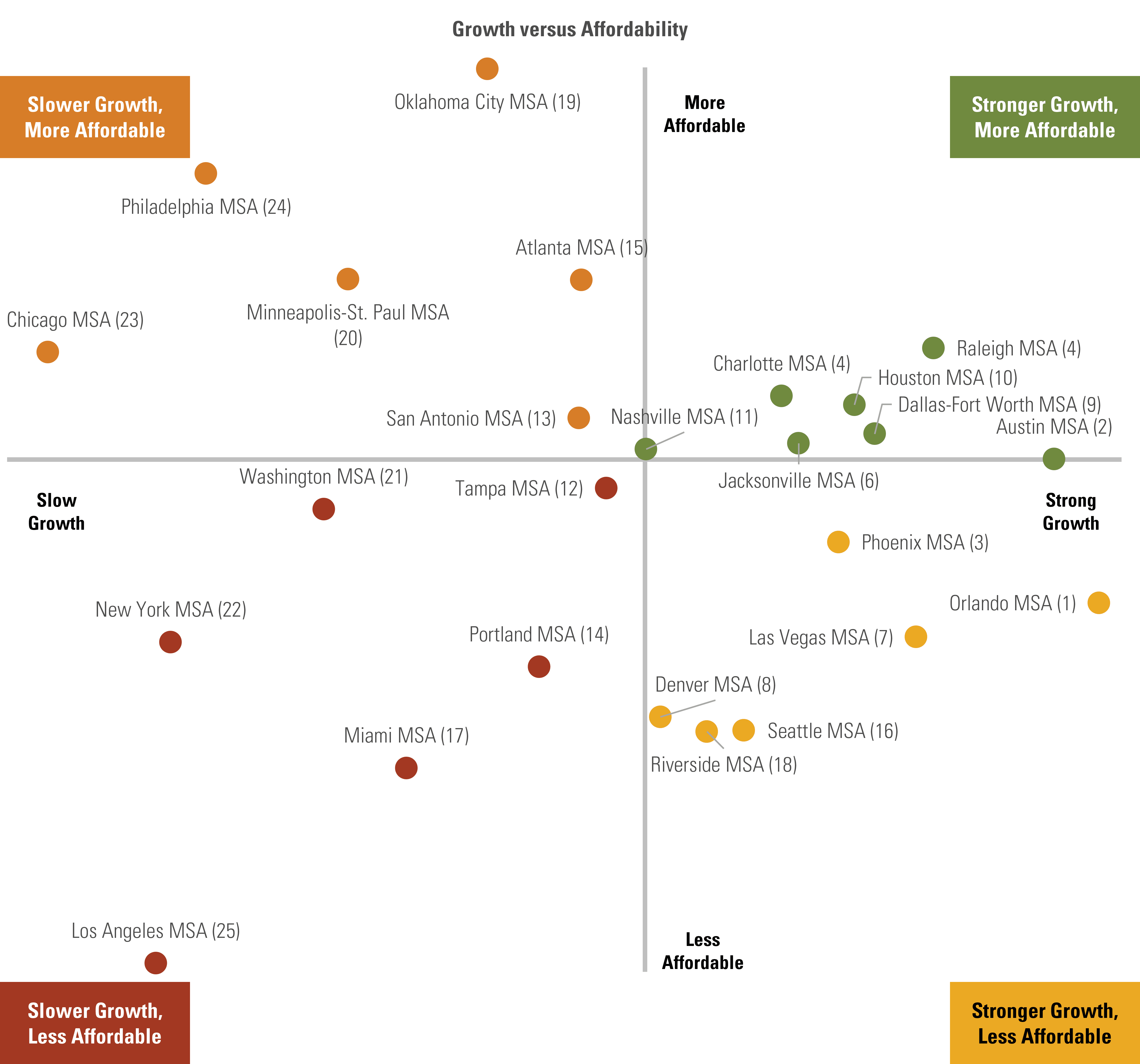

While the overall U.S. housing market has expanded since the Great Recession, it’s clear from the data that some metro areas have lost some momentum while others continue to thrive. RCLCO identified the 25 most active metros[1] and ranked them relative to each other in terms of their potential for continued single-family homebuilding. RCLCO used lessons learned from nearly 50 years of industry experience, client insights, and our firm’s national and local market expertise to provide perspective on factors that contribute to demand for new single-family homes. The metros with the greatest momentum are generally, but not exclusively, areas that are relatively affordable and have strong domestic net in-migration and solid growth fundamentals. The maps and charts below show our 2Q 2018 ranking versus our 2Q 2016 ranking, and highlight markets exhibiting disproportionate growth relative to their sizes and stronger affordability characteristics.

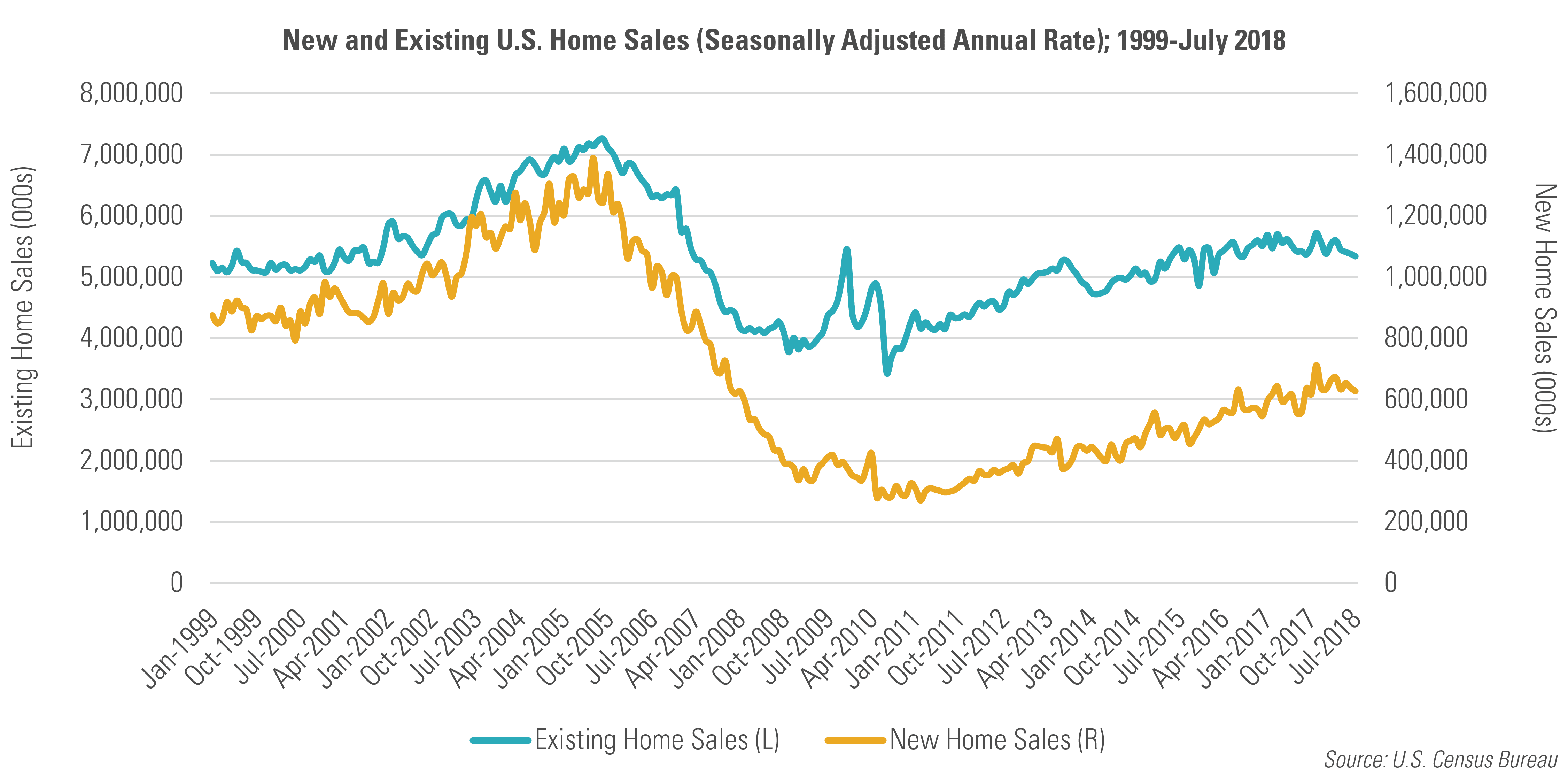

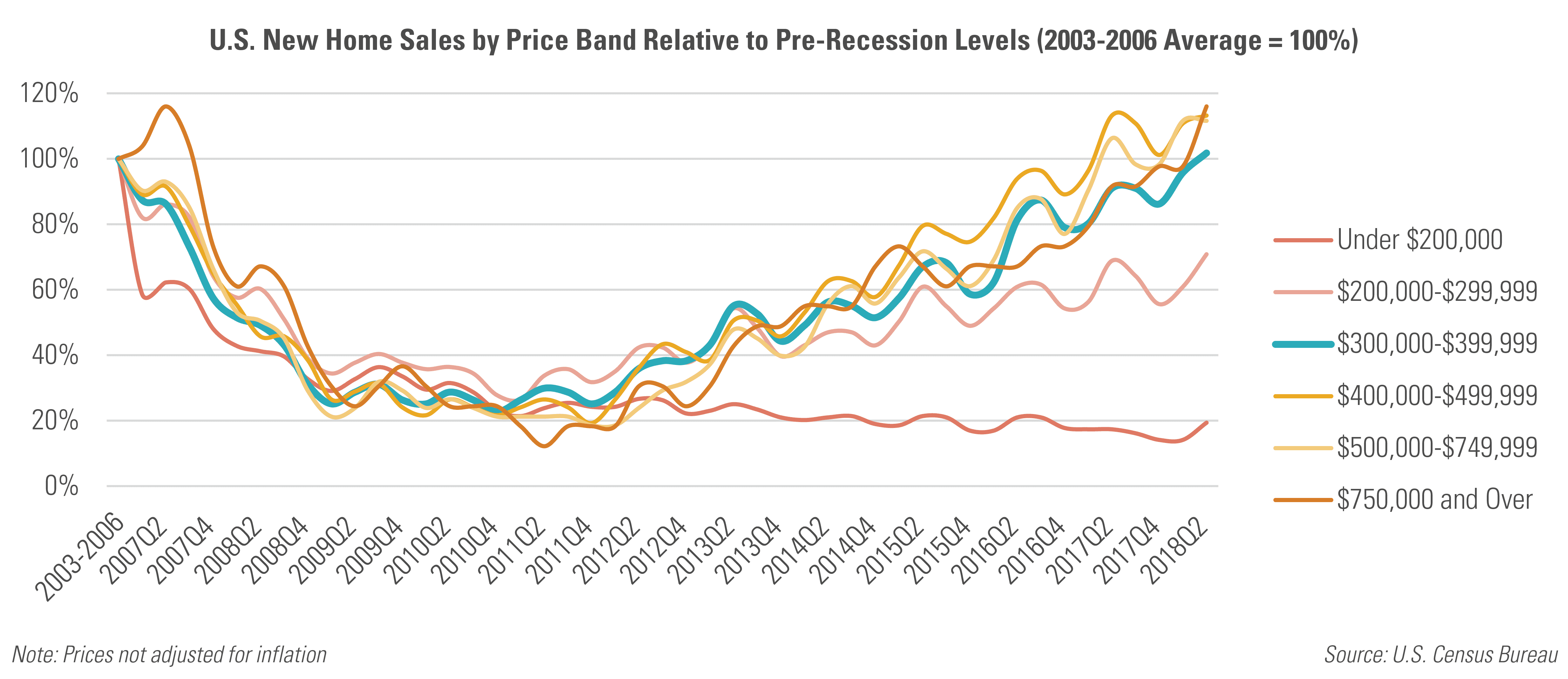

Nationally, single-family housing construction activity has increased at a slower pace than in past economic recoveries, and the supply of homes for sale, measured by months of inventory and vacancies, is below long-term trends. Given tight resale inventory and a new home market priced out of reach for many entry-level consumers, a large share of potential buyers remain on the sidelines, contributing to a depressed homeownership rate, though it has increased very slightly in the past two years as deliveries of more attainable products have increased. Nationally, however, new home sales at lower price points have not reached pre-recession levels (see chart below) given rising labor, land, and material costs, forcing builders and developers to push densities or otherwise innovate to deliver lower-priced products.

Nonetheless, demand conditions across the U.S. are strengthening as millennials move into prime family formation ages, with 27-year olds representing the largest age group in the U.S., and baby boomers looking to downsize as their children move away. Additionally, after years of income stagnation, data from the U.S. Census Bureau indicates that the U.S. median real household income has increased over the past three years, with current incomes surpassing the previous 2007 peak by 3.1%. These strong underlying demographic and economic fundamentals, coupled with substantial pent-up demand generated by household growth and years of housing undersupply, are likely to drive single-family housing demand in the near future, though high housing prices and difficulties obtaining financing will continue to produce headwinds.

For-Sale Housing Momentum Index

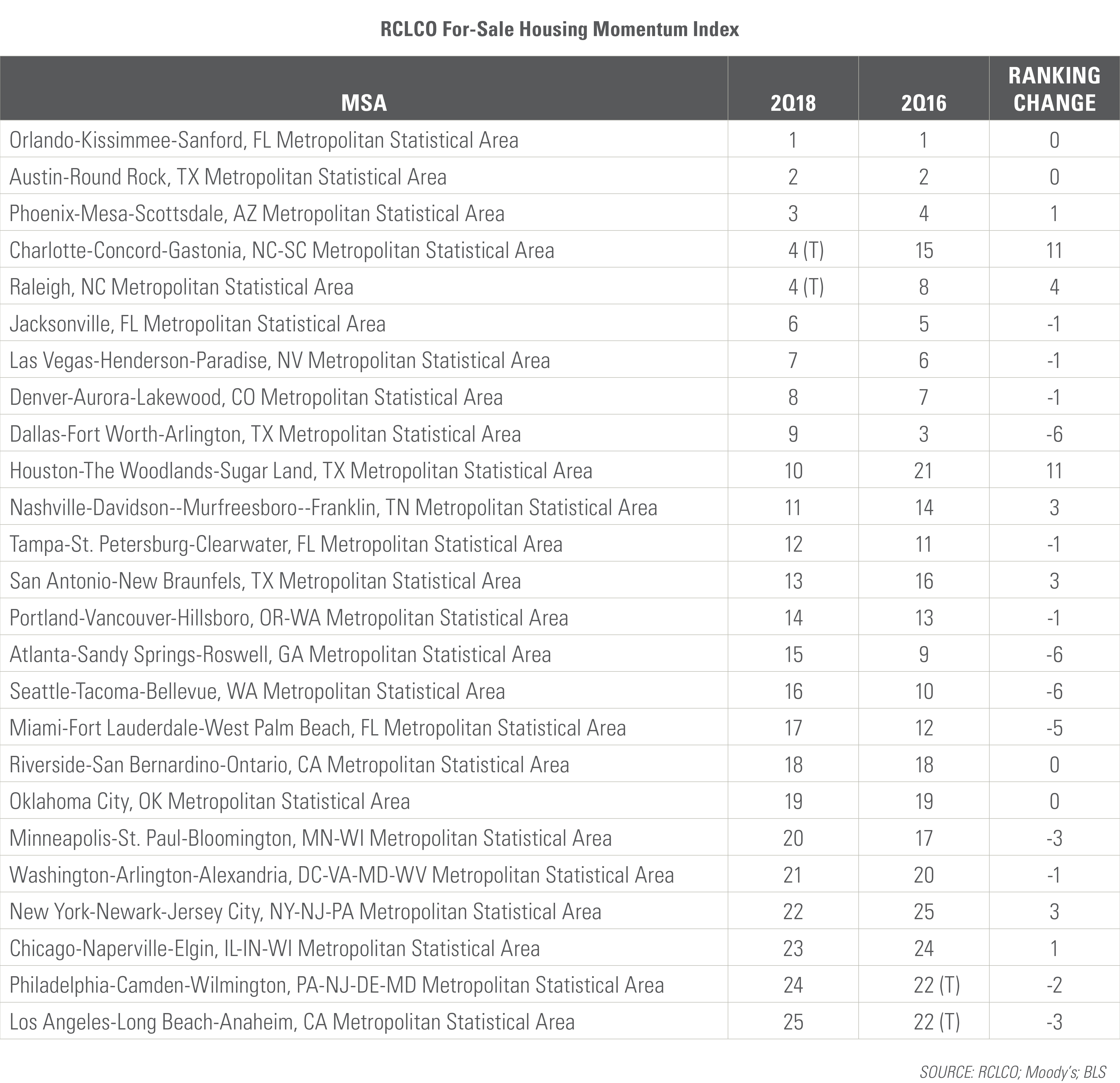

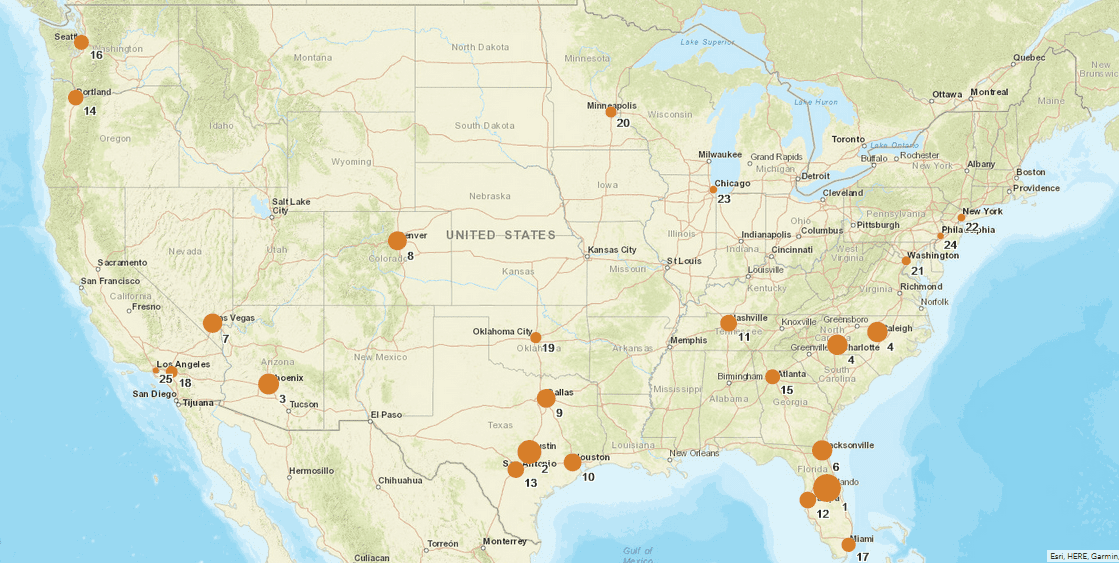

RCLCO developed a momentum index to identify for-sale housing markets with the most momentum, because local fundamentals tend to have greater cyclical impacts than those of national or regional fundamentals.[2] RCLCO analyzed the 25 most active single-family housing markets in the United States (since 2011) in order to focus on the most dynamic housing markets of greatest interest to larger investors and homebuilders. The top-25 markets were then ranked relative to one another based on each MSA’s share of national population and employment growth relative to its size, change in single-family building permits, and the current unemployment rate (see the Methodology section for additional details). The top-ranking markets are those with strong demand drivers and thus the best potential for further for-sale single-family homebuilding. While Houston, Dallas, Atlanta, and Phoenix continue to dominate the single-family market by volume, our rankings highlight the most dynamic markets experiencing disproportionate growth relative to the size of the market.

Due to its robust historical and projected growth of population, employment, and permitting activity, the Orlando MSA tops RCLCO’s For-Sale Momentum Index for the second quarter of 2018, maintaining its number-one ranking from our 2016 ranking. Of the analyzed markets, Orlando ranks first in projected percentage population growth through 2Q 2019, and demonstrated strong employment growth over the past 12 months relative to its share of U.S. jobs. Austin similarly maintained its number-two ranking given strong employment growth driven by significant domestic in-migration resulting from its robust technology sector and corporate relocations. In third position on the list, Phoenix performed well over the past 12 months with strong employment and population growth leading to an uptick in permitting activity, which is expected to continue over the next 12 months.

Although there was little change from 2016 at the top of our mid-year 2018 ranking, there are several markets that have moved substantially up or down the rankings compared with two years ago:

- Charlotte (+11) – Given the large concentration of the financial services sector in Charlotte, the market was slow to recover following the Great Recession, and permit projections in 2016 were still very conservative. But the market has picked up dramatically and is expected to maintain its momentum in the coming 12 months.

- Houston (+11) – Since oil crashed in 2014, Houston has far exceeded employment projections given its increasingly diversified economy. Although recent job growth was driven by many lower-paying industries, including jobs associated with post-Harvey rebuilding efforts, oil prices are elevated again and the market is expected to add approximately 90,000 to 100,000 jobs in the coming year.

- Miami (-5) – Employment growth expectations for Miami have dropped over the past 12 months, and affordability concerns, driven by high costs and land scarcity, have depressed single-family permit growth in the market.

- Seattle (-6) – Existing single-family home prices increased more than 25% since 2Q16, with the median resale price now exceeding $500,000. At its current pace, housing in the MSA is expected to become unaffordable to households with the median income later this year, driven by a combination of high growth and limited new single-family housing deliveries.

- Atlanta (-6) – The market experienced very strong growth from 2014-2016 following a slow recovery from the recession, but employment growth has since moderated and is expected to be more in line with long-term trends in the coming year.

- Dallas (-6) – Dallas has been the top-performing single-family market in the nation during the past several years. While Dallas is expected to remain among the top single-family markets in the coming year, growth has moderated over the past year, thus somewhat depressing its strong momentum from the past.

As noted previously, strong growth fundamentals (relative to past performance and market size) and affordability are significant drivers of a market’s position on the Momentum Index, though these two factors explain only a portion of the Index, with affordability issues often stunting growth of single-family home construction in otherwise economically healthy markets. These high-growth markets are often accommodating the growth through higher-density, for-sale attached or rental products. At the same time, being affordable does not overcome weaker growth outlooks, as the chart below indicates.

It’s important to note that this data measures momentum looking ahead for the next 12 months, and capitalizing on that momentum requires that builders and developers offer new homes congruent with homebuyer affordability levels. It’s similarly important to note that by this time next year most real estate product types may be in the late stable stage of the cycle, so economic conditions should be carefully monitored as circumstances may change. Continued strong growth in median new home prices may dampen demand potential in some markets. We plan to update this information periodically and adjust as we move through the housing cycle.

Methodology

We looked at a variety of leading and lagging metrics to determine the for-sale housing markets with the most momentum among the 25 most active housing markets—those with the greatest single-family permitting activity from 2011 to 2015. Our analysis focused on metrics in four main areas that drive demand for new, for-sale housing: single-family permits, population growth, employment growth, and low unemployment levels. We ranked each MSA’s fair share of national growth relative to each other (an MSA’s fair share describes the MSA’s share of growth over a period of time relative to its share at the beginning of the time period). In total, we looked at 10 different indicators among the four categories to analyze each of the 25 markets. Moody’s Analytics’ historical and projected economic and demographic data were used for this analysis.

Want to learn more about migration or demand drivers fueling single-family, for-sale housing growth in your local market? Contact RCLCO’s Community and Resort Advisory Group.

References

[1] Based on single-family permitting from 2011 to 2015.

[2] Robert H. Edelstein and Desmond Tsang, “Dynamic Residential Housing Cycles Analysis,” Journal of Real Estate Finance and Economics, July 2007.

Article and research prepared by Todd LaRue, Managing Director, and Cameron Pawelek, Senior Associate.

RCLCO’s mission is to help clients make strategic, effective, and enduring decisions about real estate. We proudly celebrate more than 50 years of providing the best minds in real estate with cutting-edge analytics, actionable advice, and the highest level of customer service. Our work includes market, economic, financial, and impact analyses; investment portfolio strategy and implementation; entity-level strategic planning; and management consulting.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us