Cycles Are Alive and Well—How About Your Strategy?

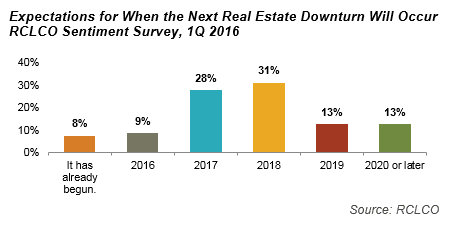

Recent volatility in the financial markets and nervousness on the part of the Fed about the health of the U.S. economy, and slow GDP growth in the fourth quarter of last year, have reminded everyone that economic and real estate market cycles are alive and well. In RCLCO’s latest 1Q 2016 Market Sentiment Survey, 17% of real estate market participants opined that the real estate industry is either already in a downturn, or would face a downturn in 2016. The percentage of respondents who think that the next real estate downturn will occur jumps to 28% in 2017 and 31% in 2018. In other words, survey respondents expect that there is approximately a 75% chance that we will have experienced a real estate market downturn by the end of 2018.

It’s Inevitable

Economic and real estate cycles are inevitable. And for the record, a cycle is a terrible analogy for changing economic and real estate market conditions. Far from being a perfect sine wave, “cycles” are more like ocean waves. Sure, they generally look alike, but each one has its own unique characteristics, each one is precipitated by unseen forces lurking under the surface, and each one breaks a little differently with unpredictable results. Even though it is impossible to accurately predict the cause or triggering event(s), timing, magnitude, or impact of any one cycle (or wave), we should continue to expect that the markets will experience periods of expansion followed by periods of contraction—the tide will eventually turn.

Based on the analyses we read and conditions we observe, RCLCO’s opinion is consistent with the opinions of survey respondents: that the likelihood of a real estate downturn will increase over the next several years, from low likelihood in 2016 (roughly on the order of 25%) to a relatively high likelihood by the end of 2018 (more like 75%). Please note that these probabilities should be used to inform downside scenario considerations and should not be read as an economic forecast or prediction.

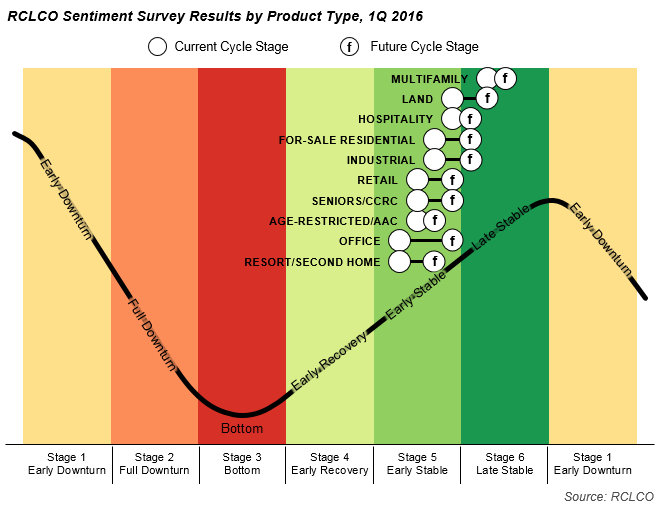

The impact of these changing tides on real estate—from availability and cost of capital to local market dynamics—is similarly impossible to predict. Overall, the equilibrium dynamic of real estate will likely shift in favor of the demand side of the equation, challenging operating fundamentals at the macro level. However, the cycles for property types and locations are not perfectly correlated with national economic or real estate cycles.

One key factor in local real estate markets’ resilience will be the strength of the local economy. Simply stated, the lower the job losses during the downturn, the less real estate markets will tend to suffer. At the individual asset or project level, the actual impact of the downturn will also vary greatly based on many factors, including the sponsorship, capital structure, tenancy profile, leases and the timing of their maturity, location, and local market dynamics. As such, some locations or opportunities miss a cycle; others are more challenged by a cycle.

Capital markets, on the other hand, are much more responsive to national conditions. This is why, regardless of the strength of a particular project, it is reasonable to assume that capital will become less available and more expensive during and immediately following the next downturn. Therefore, real estate developers and investors should put together a proactive “cycle strategy” now to enhance their ability to weather the storm, however mild or severe the next downturn should prove to be.

Cycle Strategy Planning

If cycles are inevitable, then it follows that companies should plan for all phases of the cycle, including the downturn. Trying to know the precise moment that the market will turn is a fool’s errand; it is inherently unknowable. What really matters is having a process for monitoring economic and real estate market indicators and having a plan for dealing with a number of possible outcomes and probabilities. Market monitoring and cycle planning should be a critical component of every real estate company’s strategy.

Key questions that everyone in the real estate industry—developers, owners, operators, investors, lenders and service providers alike—should be asking themselves are:

- How well prepared am I for a slight hesitation or mild economic slowdown?

- What about a more severe and, by its very nature, unanticipated downturn?

- What economic and real estate market indicators should I be tracking to help gain perspective on where my market(s)/product(s)/segment(s) are heading?

- What predetermined cycle strategies should I have on my play sheet ready to deploy as conditions change?

While no one will ever “know” when a downturn has begun, there will be strong indications in advance of a peak that the market is becoming overheated, which would be the time to be ready to act. It will be abundantly clear to everyone that the market has moved from one phase of the cycle to the next within three to six months of when it has happened—but by then, it may be too late to do anything about it.

Those who will be better positioned to thrive from—and not merely survive—a downturn, particularly as a real estate market enters the “late stable” phase of the cyclical upturn and approaches a peak, are those who learn to (a) analyze and interpret signs that indicate the probability that a peak is imminent; and (b) take graduated actions in advance of the peak to mitigate risk, bolster the balance sheet, accumulate liquidity to protect the enterprise during the downturn, and position the enterprise to take advantage of the opportunities that will inevitably become available at the bottom of the cycle.

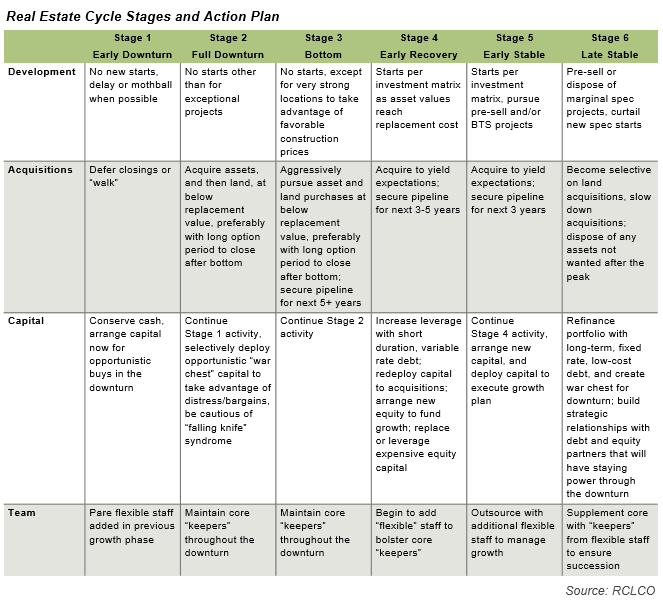

RCLCO Cycle Strategies for Real Estate Companies

Early planning and ongoing monitoring will help provide real estate executives with the tools necessary to navigate changing market conditions. The enterprise needs to: first, have a comprehensive strategy for all stages of the real estate cycle, then, be nimble as activities shift from one strategic initiative to the next—from growth to hesitation to rationalization strategies; and, finally, be able to anticipate and monitor the economy and the marketplace to be among the first to realize what is going on and do something about it before it is too late.

RCLCO’s Point of View and Advice to Clients

RCLCO believes that an appropriate “base case” for the next downturn is that it will be mild and of relatively short duration. This base case postulates that once the next downturn begins, markets may experience 12 to 18 months of declining revenues or, at best, weak or zero income growth and expanding cap rates (as suggested by the current forward curve pricing) until the next “bottom,” with healthy growth resuming thereafter. This scenario assumes that the period of weakness/decline will cause some market disruptions but not likely a systematic failure, and as such would be more akin to the economic and real estate market contraction experienced in 2001. Of course, all players will be wise to be prepared for a more significant downside as a “worse case” scenario.

Whether the next downturn reflects the base case or something more severe, our advice to clients ahead of the downturn is to:

- Consider selling non-strategic assets;

- Negotiate lease extensions for leases due to expire between now and 2020;

- Optimize the debt size of the balance sheet—lock in low rates and extend maturities to 2020 and beyond;

- Review and reconsider pending investments, including new acquisitions, planned construction and development projects, value-add investments, capex expenditures, and any other types of new initiatives;

- Become more selective with new investments, in part by building in a downturn to base underwriting models; and

- Create “dry powder” and conserve cash to weather the downturn and take advantage of opportunities presented as a result of the downturn.

We at RCLCO stand by to help any way we can to set up, implement, and advise regarding economic and real cycles, and strategies to prepare for and manage through these cycles.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us