Part 2 of RCLCO Forecast: Understanding the Demand for New Housing

This is the second installment in a series examining New US Housing Demand, relative to underlying demand drivers.

Part 2: Generation Y and New Housing Demand

As job growth continues to slowly improve, the 85 million Generation Y’s impact on the housing market will steadily increase, and not just for rental housing. They will have a transformative impact, one that’s already being felt in the multifamily sector. This is the generation whose economic prospects were hit the hardest by the downturn, but they already comprise the biggest share of new household for- mations. Just think what they could do in a better economy.

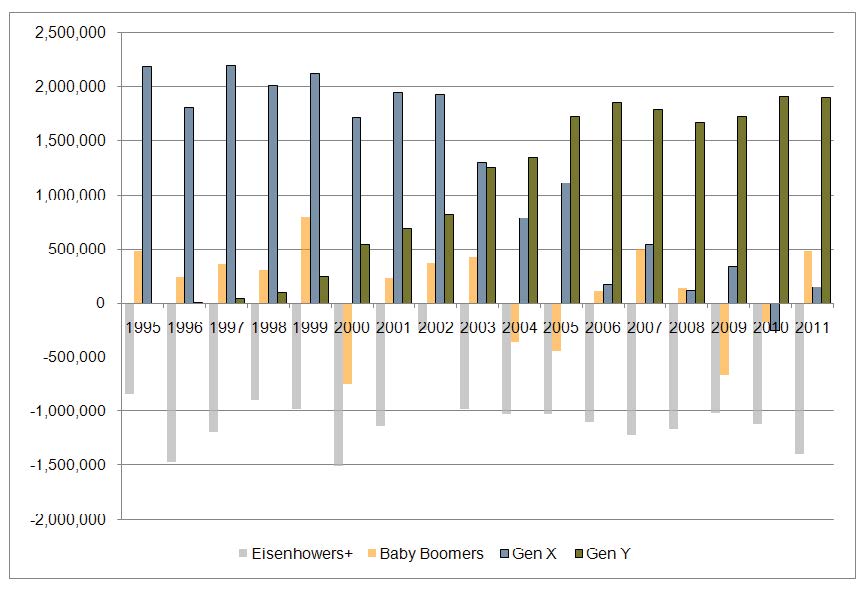

Total Net Household Formation United States, 1995 – 2011:

The rate at which Generation Y is forming new households is currently lower than Generation X before them, as young people in their early 20’s today have found themselves in a tougher job market, contend- ing with higher unemployment at a point in time where they would traditionally be seeking their economic independence. This has temporarily depressed their impact on housing demand, but as the economy con- tinues to recover during the next two years there will be significant “unbundling” that’s likely to create a surge in demand.

A recent Pew Research Center survey indicates that about 24% of Gen Y’s had to move back in with their parents after having lived on their own. Others that remained out on their own have postponed getting married and having children, or made other lifestyle compromises. As the economy continues to improve, these younger households will be able to exercise their preference to live on their own. While much of the focus has been on their potential to impact the rental market, just slightly more Generation Y’s currently rent homes than own homes (not including those still living at home). Although they’ll continue to have a positive impact on the demand for rentals, about two-thirds say that they’d like to eventually own a home. Their current impact on rental housing is as much driven by their lifestage, and economic conditions, as by permanent preference.

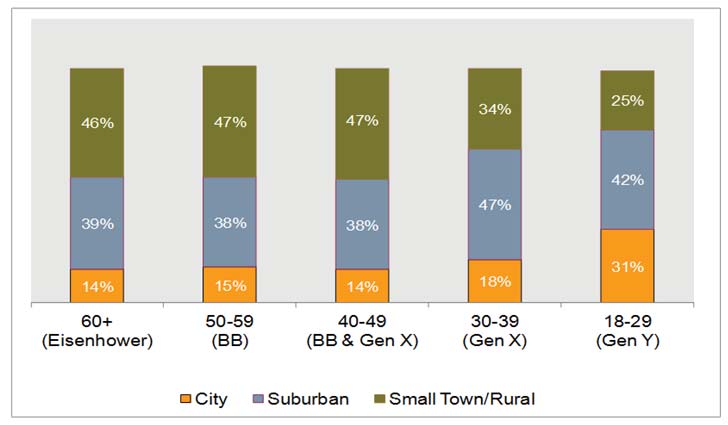

Based on stated preference, Gen Y’s are 1.7x more likely to choose to live in a City than the youngest Generation X’s, and 2x more likely to choose to live in a City than older Generation X’s and Baby Boom- ers. This appears to be a major shift in preference, but that doesn’t tell the whole story. In considering their current preferences, we should bear in mind where they are in their lifestage: young and single (and some couples), and largely “pre-family”. They will get older, marry, and some will have kids. They will ob- tain more resources, their needs will evolve, and they’ll likely make different housing choices. And by the way, more of them prefer the Suburbs than the City. The 2011 National Community Preference Survey by the National Association of Realtors shows a broad range of location preferences across all generations including Gen Y.

Where People Want To Live by Generation:

It’s true that young Gen Y renter and first time buyer households have a stronger interest in urban areas relative to other generations, but their preferences are not exclusively urban. At this stage in their lives they value convenience, in terms of proximity to work, shopping, services, and fun. RCLCO’s own con- sumer research shows that Gen Y renters have a stronger city preference than Gen Y buyers, but 44% prefer close-in suburban areas to the City (37%).

Are Generation Y’s really behaving that differently than Generation X that preceded them? After adjusting for their different economic circumstances, their behavior is fairly similar. And what we know about Gen X is that as they moved through various life stages, they made different housing and location choices.

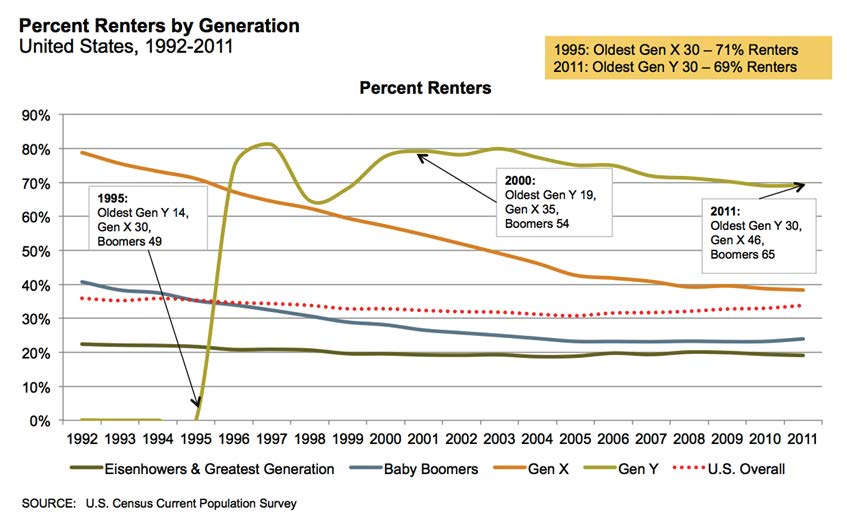

The chart below shows that when the oldest Generation Y’s hit age 30, the difference between their pro- pensity to rent and that of Generation X before them at the same age is statistically insignificant. In other words, at age 30 Gen Y’s were just as likely, not more likely, to be renters than Gen X was.

Gen Y’s renter propensity to rent has actually been declining, just as Gen X’s declined as they got older and bought homes. The rate of decline has been slower for Gen Y, but that’s largely due to economic con- ditions, not underlying preference. So we don’t want to simply straight line these trends into the future. As the market recovers, with more Gen Y’s able to find jobs and move out from Mom and Dad’s, with an opportunity to save a down-payment, two-thirds indicate they will opt for for-sale housing. Access to credit could depress that, of course. And they will hit that buyer life stage a bit later than the Gen X’s due to the economic conditions at the point they entered the market. Gen Y’s impact to the rental market will continue to be significant, and their impact on the for-sale market will be substantial as well.

Part 3: Geography of New Housing Demand

The third installment in our series examining New US Housing Demand, will focus on the locations where the greatest demand for new rental and for-sale housing will be, by generation.

RCLCO provides real estate economics, strategic planning, management consulting and implementation services to real estate investors, developers, financial institutions, public agencies, and anchor institutions. Our real estate advisors help clients make the best decisions about real estate investment, repositioning, planning and development.

We are organized into specific practice areas that allow us to provide market driven, analytically based, and financially sound solutions.

For more information, please contact Gregg Logan at glogan@rclco.com or at (407) 515-4999.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us