Sentiment Survey Mid-Year 2016: Part 2

Brexit, Schmexit? But, Dust Off Your Cycle Strategy Just in Case…

Stock markets around the globe seem to have largely shrugged off the effects of last week’s Brexit vote, recovering most of the losses experienced in the immediate aftermath of the “out” vote in Great Britain. However, this event should serve as a stark reminder for everyone involved in the real estate industry that cycles are alive and well, and more than ever, now is the time to make sure that you have a well-defined cycle strategy in place for your real estate investments/assets, your portfolio(s), and your entire enterprise.

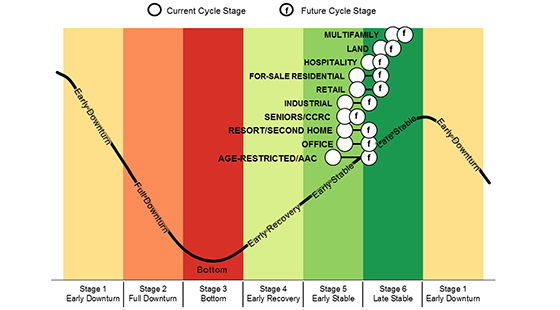

According to the Midyear 2016 RCLCO Sentiment Survey, most real estate product types are either firmly planted in, or will soon enter, the “Late Stable” stage of the cycle. Industrial, land, and hospitality have now joined apartments in the Late Stable stage, and respondents predict that most other product types will enter this stage by this time next year. Such sentiment suggests that peak conditions may be in sight for many real estate segments.

As markets shift from the Early Stable stage to the latter portion of the expansionary phase, market participants should begin to shift their strategy to a more defensive posture and be prepared to go on the offensive at the appropriate time.

RCLCO Real Estate Cycle Chart

SOURCE: RCLCO

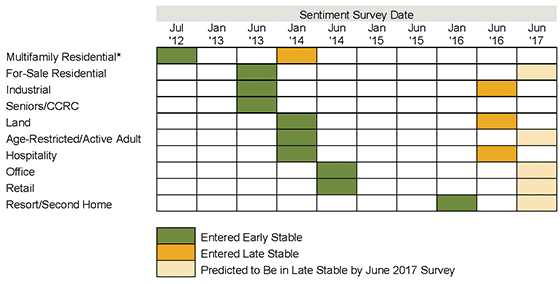

Last Call Already?

We know that different segments and markets have their own cycle timing driven by their unique supply-demand equilibrium. However, capital markets are increasingly national and global, with the effect that otherwise healthy markets or segments can get caught up in a downdraft. For some real estate segments that were late to the recovery, including office, retail, and resort/second home communities, this may mean a relatively short stay on the uphill slope of the expansionary phase of the cycle. These products may not have the chance to truly “peak” before the next cyclical downturn.

Timing of Early Stable and Late Stable Cycle Stage by Product Type

* RCLCO started tracking product cycle stages in July 2012. Apartments may have already been in the Early Stable stage prior to the July 2012 survey.

SOURCE: RCLCO

Storm Clouds on the Horizon?

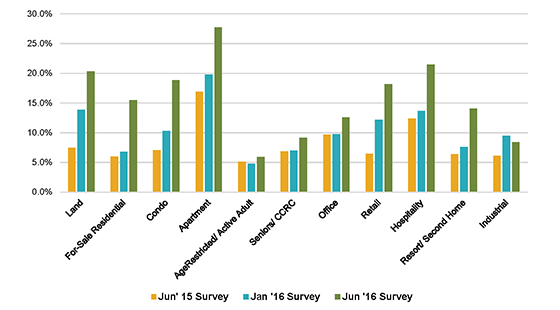

The majority of respondents to the Midyear RCLCO Sentiment Survey continue to report experiencing current positive economic and real estate market conditions. Even so, the share of respondents predicting looming Early Downturn conditions has spiked. For example, 28% of respondents are now predicting a downturn for the multifamily rental segment sometime over the next 12 months—this is up from 20% from predictions made six months ago, and up from 17% from predictions made this time last year.

Share of Respondents Predicting Early Downturn

Conditions Over Next 12-Month Period

SOURCE: RCLCO

Rental apartments continue to be on the leading edge of this trend, but hospitality, land, condo, and retail segments have all seen a big increase in Early Downturn projections, with the percentage of respondents predicting a downturn entering the high teens and low 20 percent range for the first time. For-sale residential and hospitality saw the biggest increase in downturn risk assessment, increasing 870 basis points each. Active adult remains the category with the lowest near-term downturn risk at only 5.9%, and industrial actually saw its risk assessment go down 100 basis points to 8.5%.

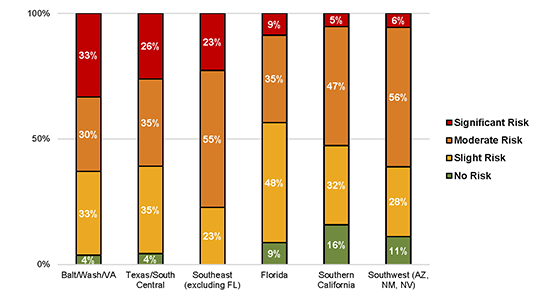

California Dreaming?

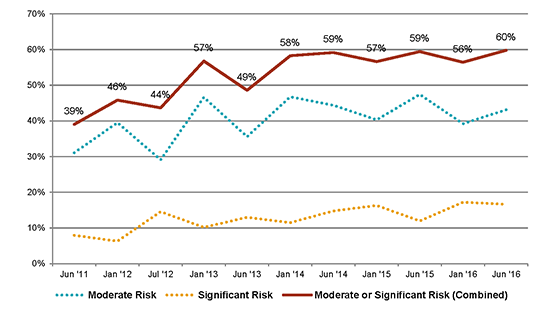

The percentage of respondents reporting a risk of an apartment bubble in the U.S. overall continues to hover around the 60% mark. However, it is a dramatically different story as we travel around the country. Only 5% and 6% of respondents in California and the Southwest, respectively, believe there is a significant risk of an apartment bubble, and a full 16% of those active in California say there is “no risk” of a bubble.

Share of Respondents Reporting Moderate or Significant

Apartment Bubble Risk in their Market

SOURCE: RCLCO

In stark contrast, a full one-third of respondents active in the greater Washington-Baltimore region believe there is a significant risk of an apartment bubble, up from 17% in the RCLCO Sentiment Survey that was conducted just six months ago. A similar trend emerges in the Texas/South Central region, where 26% believe there is a significant apartment bubble risk, compared to 0% of respondents six months ago.

Risk of Apartment Bubble by Region

SOURCE: RCLCO

RCLCO’s Point of View

The most recent Sentiment Survey seems to confirm the RCLCO view that most real estate markets and product segments are entering a late cycle phase.

During this stage of the cycle, real estate investors are generally looking to take less risk and are making more bets on stable cash-flowing assets, rather than searching for real estate investments that promise a big lift in value or operating fundamentals. During this stage of the cycle, value is typically more difficult to find, so investors are becoming much more selective. Those that buy now are taking on a certain amount of vintage risk. Further, while “core” investing is thought of as lower risk, buying core properties at this stage of the cycle has significant cap rate expansion risk. As such, value-add and opportunistic strategies with a specific plan for increasing net operating income and less reliance on cap rates staying low may actually be less risky than core investments at this point in time. Time will tell.

With that said, investors with dollar-cost averaging strategies will continue to invest through the late cycle, though should consider doing relatively less.

For-Sale Housing

The for-sale housing market is still catching up to what should be the fundamental underpinnings of demand. The current for-sale housing market is relatively stable, and even a bit undersupplied—particularly in high-growth and large in-migration markets. Moreover, as Millennials mature over the next several years and begin to enter the key family formation stage of their lifecycle, they will become a major driving force in the for-sale housing business. These trends lead us to conclude that even in the late stages of the cycle, when appropriately market-driven, new homebuilding still probably makes sense.

Multifamily Rental Housing

The rental apartment business continues to benefit from strong demographic tailwinds. Some markets and submarkets may have some potential indigestion absorbing inventory for the next couple years, but other markets are still catching up. Projects in urban locations, close-in urbanizing suburban locations, and strategic suburban submarkets are still good bets where demand exceeds supply as measured by rent growth and strong occupancy. But again, investors should be more careful and more selective in this Late Stable stage of the cycle.

Office

Commercial property markets have been improving significantly over the past several quarters, and, except for some CBD office submarkets that are getting overbuilt, operating fundamentals are still generally very strong. Late cycle conditions, however, suggest that investors should proceed with new development only when assets are significantly pre-leased. Stabilized asset acquisitions may continue to make sense when reasonable, market-driven underwriting argues in favor of near-term increases in income. However, it’s important to conduct proper due diligence against a backdrop where prices are very rich for finished product. We advise clients to be careful in making assumptions about where prices are going in the mid- to long-term.

Retail

Retail continues to experience the status quo—only in retail, that means constant change. Consolidation in the industry, changing consumer patterns, threats from e-commerce, and the emerging significance of omni-channel retailers will place significant pressures on the industry, not just over the next few years, but in the coming decades. Convenience and necessity retail in superior locations with the ability to adapt to this changing retail and consumer landscape, whatever that may be, will continue to do well.

Regional and lifestyle destination retail that figures out how to deliver an engaging and entertaining “experience” for its patrons, and centers that succeed in blurring the lines between living, working, and playing, will likely outperform the sector overall.

Hotel

The U.S. hospitality markets across the spectrum—from select service to luxury—were among the latest to recover in terms of operating fundamentals but then moved quickly, with RevPAR now well above pre-recession levels in most segments and geographic markets. Perhaps more than any other real estate segment, the story in hospitality is market by market – some geographies have already seen deliveries spike, resulting in a decline in property level economics, and other markets still have not seen significant construction begin. The risk of obsolescence is also particularly high with hotels, so the best assets will continue to outperform the averages even in markets that have supply concerns, while dated assets will suffer more significantly in a declining market.

Industrial

Demand for industrial and logistics space is expected to moderate somewhat over the next 12 to 18 months, with net absorption falling below the high water mark set in 2015, but well above the long-term average. Steady, if moderate, employment and GDP growth coupled with strong consumer confidence is driving demand for imports and the need for additional bulk warehouse space. At the same time, e-commerce driven, same-day delivery strategies are increasing the demand for “last-mile” distribution space, typically of the flex warehouse variety, closer to households and job centers. The ability of developers to gear up (and down) development is much shorter in the industrial sector, so while this sector remains vulnerable to cycles, the time necessary for a correction is much less pronounced.

Capital Markets

With property values in most markets now at or above replacement cost, we can expect construction activity across product types to further accelerate, creating a need for construction financing to fill in the vacuum created by commercial banks’ limited capacity to originate much construction loan activity. The shortage of construction lending activity may help keep construction activity lower than it otherwise would have been, helping reduce the risk of overbuilding and helping to keep pricing power in the hands of property owners where demand exceeds supply.

In the equity markets, there is a large amount of capital available to be deployed. By some estimates, there is approximately $200 billion of dry powder in commingled funds alone. The U.S. continues to be a favored destination for off-shore capital, and we see no letup in this trend for the foreseeable future, particularly as the world works to fully process the implications of Brexit.

We may well be experiencing a pricing bubble in real assets, as well as equities, due to central banks’ low interest rate policies that have kept rates negative in the E.U. and Japan and near zero in the United States and elsewhere. Due to fear of driving the economy into recession, the Fed has relied on cautionary commentary rather than interest rate hikes to let some air out of the balloon. The flat stock market of the past 12 months indicates that the Fed may have had at least some success, but real estate prices seem to be unfazed, at least for now.

We do caution investors of the perils of borrowing at floating rates at this stage of the cycle. It may be a good idea to buy an interest rate cap for protection.

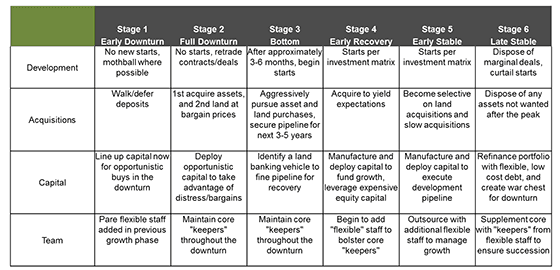

What Action Should You Be Taking?

Of course, real estate is local and every real estate investment opportunity is unique, so these national trends need to be applied to investment-specific, micro market dynamics. As the likelihood of a downturn increases over time, it is wise to be prepared. Tightening up underwriting criteria, shoring up the balance sheet, and creating flexibility to pursue opportunities during the inevitable downturn, when it does occur, should be priorities.

RCLCO Strategy Recommendations by Cycle Stage

SOURCE: RCLCO

Key strategies and actions that real estate market participants should be considering deploying in the Late Stable stage of the cycle include:

- Consider selling non-strategic assets and dispose of marginal deals, or assets not wanted after the peak;

- Negotiate lease extensions for leases due to expire between now and 2020;

- Refinance your portfolio with flexible, low-cost debt; optimize the debt side of the balance sheet; and lock in low rates and extend maturities to 2020 and beyond;

- Raise hurdle rates for new deals, and review and reconsider pending investments, including new acquisitions, planned construction and development projects, value-add investments, capex expenditures, and any other types of new initiatives;

- Become more selective with new investments, in part by building in a downturn to base underwriting models;

- Manage growth with flexible/outsourced overhead to avoid painful cuts in the downturn; and

- Create “dry powder” and conserve cash to weather the downturn and take advantage of opportunities presented as a result of the downturn.

We at RCLCO stand by to help any way we can to set up, implement, and advise your real estate organization regarding economic and real cycles, and strategies to prepare for and manage through these cycles.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us