RCLCO National Real Estate Sentiment Survey

Broad-Based, but Guarded, Optimism

Guarded Optimism…

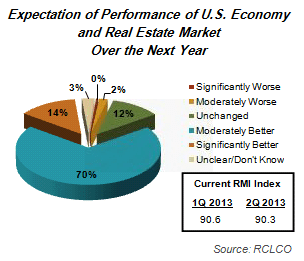

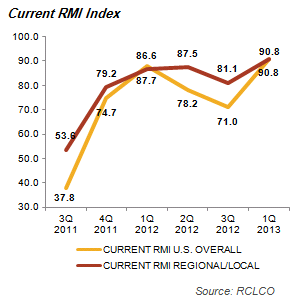

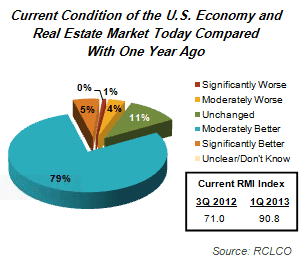

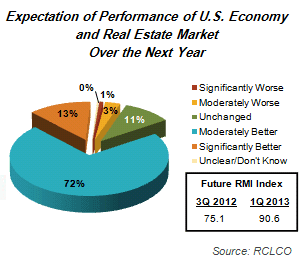

After another slight hesitation in the third quarter of last year, most likely due to uncertainty surrounding the fiscal cliff debate and the election, sentiments regarding the current state and likely future trajectory of the U.S. economy and real estate markets reflect a high degree of optimism, albeit of the “moderate” variety. The Current Real Estate Market Index (RMI1), for both the U.S. overall and Local/Regional markets, broke the 90 mark, up from 71.0 and 81.1 respectively in 3Q 2012. This is the highest level since we began the survey in 2009. Nearly 80% of respondents said that the U.S. economy and real estate markets were Moderately Better than 12 months ago, plus an additional 5% who reported that they were Significantly Better.

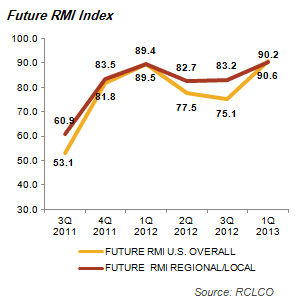

Looking forward over the next year, the sentiment is equally optimistic, with both the U.S. and Regional/Local markets posting Future RMIs above 90. And perhaps most encouraging is that few respondents report that their markets are Worse today than they were a year ago, and only 5.6% of respondents expect their markets to decline over the next 12 months. Furthermore, 13% expect the U.S. economy and real estate market to perform Significantly Better over the next 12 months. Break out the moderately-priced Chablis?

Regional Outlook—Dead Cat Bounce?

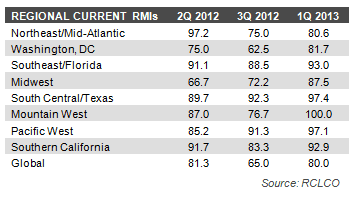

No, we think this kitty is alive and kicking, and the real estate markets are on a healthy and sustained path towards recovery and growth. After several quarters of growing optimism about the strength of the recovery in the second half of 2011 and into the first half of 2012, many market participants expressed concern leading up to the 2012 election. RMI metrics declined across the country in 3Q 2012—most sharply down 17% in the Washington, D.C., region and 23% in the Northeast/Mid-Atlantic. Notable exceptions included the Midwest, where the auto business was roaring back, and the South Central/Texas region, driven largely by a surge in the energy sector.

No, we think this kitty is alive and kicking, and the real estate markets are on a healthy and sustained path towards recovery and growth. After several quarters of growing optimism about the strength of the recovery in the second half of 2011 and into the first half of 2012, many market participants expressed concern leading up to the 2012 election. RMI metrics declined across the country in 3Q 2012—most sharply down 17% in the Washington, D.C., region and 23% in the Northeast/Mid-Atlantic. Notable exceptions included the Midwest, where the auto business was roaring back, and the South Central/Texas region, driven largely by a surge in the energy sector.

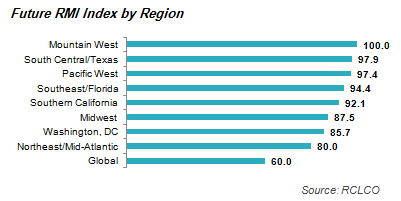

Fast forward to 1Q 2013, and nearly every market has bounced back to the lofty heights experienced back in 2Q 2012. The outlook for the next 12 months by region reflects continued optimism, with Future domestic RMI indices all above 80, and five out of eight above 90. The Mountain West region, which includes Great Recession poster children Phoenix and Las Vegas, has a Future index of 100, reflecting the near universal belief that these markets will experience continued significant improvement. Even in the D.C. area, where debt ceiling and sequester debates continue to be a main topic of cocktail party chatter, respondents recorded the highest Future RMI since we have been conducting the sentiment survey. Optimists around the Capital Beltway are arguing that the next round of cuts is likely to affect entitlement programs and will not hit the Washington region in a disproportionate way.

The one exception to the unbridled enthusiasm is respondents who are active globally—here the Future RMI dropped down to 60, which presumably reflects perceived risks associated with the continuing malaise in the Eurozone.

RCLCO Outlook

We believe the survey respondents have got it basically right. We anticipate that demand for real estate will continue to improve in 2013, but at a moderate pace relative to previous recoveries. We expect the second half of 2013 to usher in better job growth, higher consumer confidence, and less volatility, particularly as the market gains better clarity on the direction of the debate regarding the debt ceiling and sequestration. This should all translate into a robust, healthy real estate development and investment environment in 2013 and beyond.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us