Condos: What’s Working Now

Market Segmentation Strategies that Connect with Customers

Introduction

As RCLCO hypothesized in this space last fall, market conditions increasingly suggest that the cyclical shift from apartment development (increasingly well supplied) to condo delivery (still largely undersupplied) is underway, and we expect that this market will mature quickly. Last time (September 12, 2013, “Condo Recovery Underway and Likely to Accelerate”) we focused on market timing and suggested strategies available to developers and investors to best position themselves for success and to manage downside within the risky and limited window of opportunity to deliver for-sale condo product.

If market timing is a gateway factor for a successful condominium project, laser-like alignment between product and potential customer is what actually sells units. So what will the next wave of condo buyers look like and how can we better understand which market audiences are active and what products make them move?

Condominiums appeal to a broad and varied range of consumer types (no, it’s not a value product) up and down the age/lifestage and income spectrum. If there is a unifying characteristic, it’s the lack of children living at home that allows for the higher density lifestyle, and openness to urban areas where schools and other services might not be as robust. This article discusses the composition of condominium buyers in America today and what they are buying. Next time in this space we will discuss how to quantify the depth of each market segment in your geographic marketplace.

Buyer Composition Overview

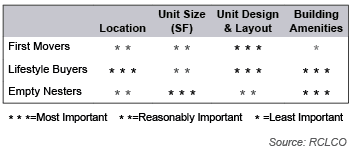

We observe in our work in most major metropolitan markets, and even in many re-urbanizing smaller markets, that there are three distinct segments, or cohorts, of condominium buyers: “First Movers,” the so-called young professionals; “Lifestyle Buyers,” singles or couples, sometimes referred to as “Never Nesters” in their 30s, 40s, and 50s; and “Empty Nesters.”

As in any for-sale housing type, each unique customer brings their own personal decision “algorithm.” However, RCLCO’s analysis of what’s working in condominium development now demonstrates a similar willingness within each cohort to trade off key factors when identifying a home that will serve their lifestyle and prove reasonable within their economic realities. These priorities are summarized in the table below:

Of course, most buyers want everything and resist sacrifices unless their own purchase economics require it. In A+ locations supporting top-of-the-market pricing, all of the above factors may be absolute requirements.

The challenge of development or repositioning, however, is to craft a project that reflects the realities of location and economics, and connects a defined customer with an offering that serves enough of their needs at a price they can afford to pay. At this stage of redevelopment in many American cities, the challenge is making projects work for the heart of the market in terms of purchasing power, or in locations that are less established. Discussed below are strategies for targeting the full spectrum of potential condominium customers, including in less-than-A locations.

First Movers

First Movers are younger households currently in the rental market, but motivated to purchase by the financial appeal of ownership. To a significant extent, the most appealing product and location may be something that is relatively similar to their current apartment and in a comparable, if not the same, neighborhood. These buyers are least likely to compromise on unit layout/design and most likely to sacrifice building amenities—the city itself being the primary amenity, offering most of the needed facilities and services on an “a la carte” basis. This demographic will increasingly choose to purchase over renting, RCLCO’s research suggests, when their economic confidence is sufficient to maintain their current lifestyle, and so condo conversions also offer a compelling “value proposition” to this target market.

Locations that attract first movers are typically A-/B+ locations with strong livability factors such as basic neighborhood retail (i.e., grocery, restaurants, fitness facility, cleaners), good multimodal access to employment cores, a unique/authentic identity, and considerable upwards momentum. This demographic demonstrates the greatest potential to anticipate (and price in) the evolution of a pioneering neighborhood. As they have demonstrated in rental apartments during the past few years, this group is highly prone to accept smaller unit sizes in exchange for a better or better-located apartment. And for sure “cool,” “stylish,” and “interesting” have shown themselves highly powerful in compelling young buyers to accept a smaller unit in a secondary location.

The Linea in San Francisco typifies successful First Mover projects. The project is located at the intersection of several transitional but central neighborhoods in the heart of San Francisco, between Hayes Valley and Duboce Triangle. The Linea is also in close proximity to other neighborhoods that are known for their nightlife, which bodes well for attracting First Movers. With regard to the unit program, The Linea offers smaller, one- and two-bedroom floor plans, and provides few common amenities—effectively reducing the entry price and ongoing association fees. The reduced upfront costs of ownership are pivotal for First Movers, as many prospective buyers within this market segment cannot afford lofty down payments. Therefore, projects that steer clear of excessive amenity packages but are located in improving areas with strong neighborhood retail can compete effectively with older, better-located resale alternatives for First Mover buyers.

The Linea in San Francisco typifies successful First Mover projects. The project is located at the intersection of several transitional but central neighborhoods in the heart of San Francisco, between Hayes Valley and Duboce Triangle. The Linea is also in close proximity to other neighborhoods that are known for their nightlife, which bodes well for attracting First Movers. With regard to the unit program, The Linea offers smaller, one- and two-bedroom floor plans, and provides few common amenities—effectively reducing the entry price and ongoing association fees. The reduced upfront costs of ownership are pivotal for First Movers, as many prospective buyers within this market segment cannot afford lofty down payments. Therefore, projects that steer clear of excessive amenity packages but are located in improving areas with strong neighborhood retail can compete effectively with older, better-located resale alternatives for First Mover buyers.

Lifestyle Buyers

Interestingly, Lifestyle Buyers can be the most unforgiving and thus the hardest to service with new product, but are very active in the market today and too often overlooked. These buyers are in many instances moving up from an existing condominium and thus can be enticed to move only with something very special. These households are typically more mature (often 40s and 50s), high-income professionals without children (or whose children live with another parent) with strong purchasing power. This market segment understands the economic benefits of ownership, has ample disposable income and/or home equity, and seeks a home that facilitates their lifestyle and provides a sense of “identity refreshment” or prestige.

This market segment typically has a strong desire to maintain an urbane lifestyle (even if in a suburban setting), and Lifestyle Buyers expect high service and convenience in exchange for higher prices. More specifically, Lifestyle Buyers are willing to exchange smaller unit size for an A+ location, compelling amenity package, and high design—but are most likely to require the total package of location, amenities, and design to justify a move.

Successful Lifestyle Buyer projects are located in the CBD or 100% high-density suburban or other “name brand” neighborhoods, and typical floor plans consist of modestly sized, one-/one-bedroom plus den and two-bedroom units (800-1,300 square feet) that provide top-of-market appliances, finishes, and compelling (often highly contemporary) design. Exclusive social spaces and service-oriented building amenities play into the prospective buyer’s perception of exclusivity and status—such as indoor swimming pools, open-air terraces, and top-of-market fitness facilities.

A prime example of a successful Lifestyle Buyer project is The Legacy at Millennium Park in Downtown Chicago. This high-rise project, which overlooks Millennium Park, primarily appeals to experienced homebuyers who enjoy being close to their places of employment and cultural amenities. The Legacy at Millennium Park also has floor-to-ceiling windows, which allow for excellent views, and the top-of-market unit finishes are consistent with the standard of living that buyers are seeking. As a unique offering, this project enjoys an affiliation with an adjacent private downtown club, allowing homeowners to take advantage of the club’s hotel-like services as well as other lifestyle amenities.

A prime example of a successful Lifestyle Buyer project is The Legacy at Millennium Park in Downtown Chicago. This high-rise project, which overlooks Millennium Park, primarily appeals to experienced homebuyers who enjoy being close to their places of employment and cultural amenities. The Legacy at Millennium Park also has floor-to-ceiling windows, which allow for excellent views, and the top-of-market unit finishes are consistent with the standard of living that buyers are seeking. As a unique offering, this project enjoys an affiliation with an adjacent private downtown club, allowing homeowners to take advantage of the club’s hotel-like services as well as other lifestyle amenities.

Insignia, a Seattle-based project that is currently being developed by Bosa Development, is another high-rise condo venture that is targeting Lifestyle Buyers. Insignia is anticipated to enter the market in 2015, and boasts an A+ location that overlooks Puget Sound. The project offers one- and two-bedroom floor plans (most units ranging between 700 and 1,500 square feet) that will be priced between $400,000 and the high $600,000s. Insignia offers great unit finishes, along with community green spaces that leverage the development’s superior views. Insignia has already received considerable interest from prospective buyers. These buyers are required to put at least 10% down—which effectively prices out First Movers, and speaks directly to the Lifestyle Buyer market segment.

Insignia, a Seattle-based project that is currently being developed by Bosa Development, is another high-rise condo venture that is targeting Lifestyle Buyers. Insignia is anticipated to enter the market in 2015, and boasts an A+ location that overlooks Puget Sound. The project offers one- and two-bedroom floor plans (most units ranging between 700 and 1,500 square feet) that will be priced between $400,000 and the high $600,000s. Insignia offers great unit finishes, along with community green spaces that leverage the development’s superior views. Insignia has already received considerable interest from prospective buyers. These buyers are required to put at least 10% down—which effectively prices out First Movers, and speaks directly to the Lifestyle Buyer market segment.

Empty Nesters

Empty Nesters, a segment we believe will drive growth of the condominium market, are increasingly considering downsizing from their suburban, single-family detached homes, with an urban environment proving an alluring lifestyle option.

Empty Nester condominium buyers are the subset of post-family households that are willing to trade some of the space of their current home (likely in a suburban location) for the walkable, low-maintenance lifestyle of a more urbane environment. The dilemma the industry struggles with is that the personal space this customer often believes they need, and the cost of acquiring it, has made the transition to urban living challenging for all but the most affluent. Successful projects often provide a large percentage of one-story, two-bedroom floor plans of at least 1,500 square feet, with some projects offering units topping 3,000 square feet. The one-story units allow for greater mobility, and the larger floor plans make it easier for Empty Nesters to still entertain family and guests.

Empty Nester condominium buyers are the subset of post-family households that are willing to trade some of the space of their current home (likely in a suburban location) for the walkable, low-maintenance lifestyle of a more urbane environment. The dilemma the industry struggles with is that the personal space this customer often believes they need, and the cost of acquiring it, has made the transition to urban living challenging for all but the most affluent. Successful projects often provide a large percentage of one-story, two-bedroom floor plans of at least 1,500 square feet, with some projects offering units topping 3,000 square feet. The one-story units allow for greater mobility, and the larger floor plans make it easier for Empty Nesters to still entertain family and guests.

For the most affluent, five-star features and amenities allow for a “standard of living” similar to the level provided by a high-end single-family home. But the broader market, whose economic considerations require making product trade-offs, do seem to be willing to sacrifice features, amenities, and even location to some degree, if they can find a unit of appropriate size. Some recent projects have found success (sometimes accidental success) in attracting this customer on the periphery of more established downtown districts, where the retail is interesting and transit service is rich, or in walkable suburban locations.

The Rosewood, located southeast of Downtown Charlotte, is a prominent example of a well-executed Empty Nester project. The Rosewood offers units in excess of 2,000 square feet, a robust amenity package, within 10 minutes from downtown. The combination of large floor plans and multiple acres of green space offers similar living to a single-family home, without the maintenance and upkeep. Familiar outdoor and community amenities offer buyers additional lifestyle and convenience, including: a large pool area, tennis courts, walking trails, a fitness center, communal lounge spaces, private parking, multiple elevators, and 24-hour security.

The Rosewood, located southeast of Downtown Charlotte, is a prominent example of a well-executed Empty Nester project. The Rosewood offers units in excess of 2,000 square feet, a robust amenity package, within 10 minutes from downtown. The combination of large floor plans and multiple acres of green space offers similar living to a single-family home, without the maintenance and upkeep. Familiar outdoor and community amenities offer buyers additional lifestyle and convenience, including: a large pool area, tennis courts, walking trails, a fitness center, communal lounge spaces, private parking, multiple elevators, and 24-hour security.

Stonebridge Lofts in Minneapolis is another good example of a recently-developed condo project that attracts a large share of Empty Nesters. Similarly to Rosewood, the project is located on the edge of downtown, and offers large floor plans. Although this project does not offer as much green space as Rosewood, each unit includes a balcony or patio, many with views overlooking the nearby river and downtown Minneapolis. Stonebridge Lofts also provides a compelling but not over-the-top mix of community amenities that are attractive to Empty Nesters, including a large community room with a full kitchen and grill, swimming pool and hot tub, and exercise room.

Although most Empty Nesters have not yet proved willing to compromise very much on unit size, this cohort is far more diverse in economics and housing requirements than conventional wisdom believes. There will increasingly be an opportunity to serve this market with a broad range of unit sizes, level of amenities, and locations. But the key to success is defining the potential customers’ desired lifestyles and crafting products that respond to them.

Article and research prepared by Adam Ducker, Managing Director, and Erin Talkington, Vice President.

RCLCO provides real estate economics and market analysis, strategic planning, management consulting, litigation support, fiscal and economic impact analysis, investment analysis, portfolio structuring, and monitoring services to real estate investors, developers, home builders, financial institutions, and public agencies. Our real estate consultants help clients make the best decisions about real estate investment, repositioning, planning, and development.

RCLCO’s advisory groups provide market-driven, analytically based, and financially sound solutions. RCLCO’s Urban Real Estate Group produced this newsletter. Interested in learning more about RCLCO’s services? Please visit us at www.rclco.com/urban-real-estate.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us