Leveraging Control – LPS and Real Estate Leverage

Originally published via AFIRE

Though leverage is an important part of capital funding, it’s important to ask LPs if (and how) they should take control of their real estate leverage.

Leverage is widely used in real estate as an important part of the capital funding, and real estate and leverage have gone hand-in-hand since mortgages originated in England in the Middle Ages. When used wisely, it can enhance returns and provide other portfolio benefits. Institutional investors manage real estate leverage in a variety of ways, but typically utilize relatively low levels of leverage for low-risk investments and higher levels of leverage for higher risk investments. In general, this has worked out in terms of overall returns, but may not be the most efficient strategy.

Institutional investors should continue to use moderate levels of leverage on a portfolio-wide basis but also explore ways to minimize the cost and maximize the flexibility of real estate leverage. In particular, overall fund-level leverage can offer investors lower interest rates while not encumbering specific properties held in their portfolios.

Owners of residential and commercial properties typically use mortgage loans tied to specific properties (collateral) as an important source of capital to make real estate purchases. In most cases, repayment of a mortgage is limited to the cash flow and potential value of the property itself. In some cases, personal or corporate guarantees can provide additional repayment support. Not all real estate loans are mortgages – lines of credit and unsecured debt are also used, without a specific property (or properties) designated as collateral.

This article examines the pros and cons of leverage in general, explores the unique aspects of real estate leverage, looks at the way that leverage is used in an institutional real estate setting, and offers options for institutions to consider in managing real estate leverage.

Does leverage add value?

Despite some arguments to the contrary, the majority of investors believe that leverage adds value when applied to real estate assets or portfolios. The use of leverage generally enhances returns (when property or portfolio returns are in excess of the cost of leverage), allows for greater diversity in a portfolio, and in some cases, provides a free put option when the value of a property is less than the mortgage amount.

The biggest argument against using leverage stems from work done by economists Modigliani and Miller in the 1950’s. They argued that the value of a firm (and by extension, a property) is independent of its capital structure. Adding leverage can boost returns but comes with an offsetting amount of risk. Plus, investors have the ability to adjust leverage through investor-level borrowing or by offsetting firm (or property) leverage with risk-free bonds, so there was no apparent need for firms to utilize leverage.

This initial finding was influential in corporate finance circles but was based on crucial simplifying assumptions, such as no taxes or bankruptcy costs, and did not account for differences in the cost of debt by firm (property) and over time. Later versions of the theory took into account those and other factors and determined that there is an optimal level of debt for each firm based on its riskiness, with lower leverage recommended for riskier firms and industries.

Real estate tends to use more debt than other sectors. Some real-estate specific attributes that support borrowing include yields (either income or cash yields) in excess of borrowing costs; long leases with creditworthy tenants (depending on property type); relative resilience to technological and other changes; and collateral values that are typically independent of ownership, resulting in relatively low loss rates in the event of default. Over time, leverage has had a beneficial impact on returns. For example, properties with leverage in the NCREIF Property Index (NPI) have out-performed unleveraged properties by 150 and 110 BPS over the past 10 and 20 years, respectively. Of course, there have been periods of low or negative returns when leverage had a negative impact on returns.

For most private investors, the answer to how much leverage is optimal is: “As much as one can get at a reasonable interest rate.” Institutional investors need to view this question differently. Pension funds generally have a lower tolerance for risk than most private investors, particularly when underfunded relative to expected liabilities. Also, most asset allocation analyses are based on the returns and volatility of unleveraged core real estate, creating a potential mismatch between target and actual portfolio impacts. Finally, adding leverage to a real estate portfolio effectively offsets investments in similar duration bonds. For example, a US$1 billion real estate portfolio with 50% leverage would effectively offset US$500 million of an institution’s bond portfolio.

For most private investors, the answer to how much leverage is optimal is: “As much as one can get at a reasonable interest rate.” Institutional investors need to view this question differently. Pension funds generally have a lower tolerance for risk than most private investors, particularly when underfunded relative to expected liabilities. Also, most asset allocation analyses are based on the returns and volatility of unleveraged core real estate, creating a potential mismatch between target and actual portfolio impacts. Finally, adding leverage to a real estate portfolio effectively offsets investments in similar duration bonds. For example, a US$1 billion real estate portfolio with 50% leverage would effectively offset US$500 million of an institution’s bond portfolio.

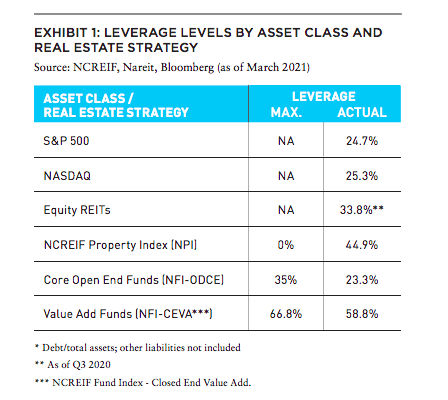

Leverage levels for real estate strategies and other asset classes are fairly stable over time, with fluctuations due to changes in market values. Real estate stands out with a relatively wide range of leverage levels, as shown in Exhibit 1. The NPI reports returns on an unleveraged basis, but many properties in that index utilize some leverage. As also detailed in Exhibit 1, NPI properties actual leverage is about 45%, indicating leverage is generally accepted by many institutional investors. The ODCE Index limits overall fund leverage to 35%, with the current average much lower at 23%. There are some who suggest that ODCE funds should use greater leverage given the low-risk nature of those funds. Equity REITs utilize about 34% leverage, with notable differences by property type. Finally, value-add real estate funds utilize the highest leverage levels—an average of 67% allowed and 59% in practice.

There have been numerous studies and analyses on the advisability and proper level of debt for an institutional real estate portfolio. Most of them are focused on private real estate funds and not on core strategies, including separate accounts with low levels of leverage.

Some recent examples include:

- Alcock, Baum, et al. found that, based on analyzing a large sample of global private equity real estate investment funds, leverage-related strategies, such as adding leverage or tactically changing leverage levels in an attempt to time the market, do not reliably generate excess fund returns.

- Bollinger and Pagliari examined the risk-adjusted, net-of-fee performance of non-core funds and generally found that investors would have been better served by placing additional leverage on their core investments rather than investing in non-core assets. Looking at a range of funds over the 2000–2017 timeframe, a leveraged core strategy would have produced higher returns with lower fees than a value-add or opportunistic fund.

- Green Street, a real estate advisory firm that focuses on publicly traded real estate companies, noted that “Preserving financial flexibility and avoiding both direct costs of financial distress and indirect costs, such as not being able to pursue attractive investments at opportune times, is important. There is not a one-size-fits all approach, but . . . key ingredients to a healthy balance sheet should include comprehensive leverage of 30% or less, debt-to-EBITDA of 5X or less, access to a wide menu of capital sources, well-laddered debt maturities, and a thoughtful stance on the mix of recourse/non-recourse debt.”

Interest rate trends and timing considerations

Real estate income yields, or cap rates, reflect many factors, including risk-free rates, growth projections, riskiness as indicated by lease length and tenant credit, among others. The availability, cost, and benefits of leverage vary over time, as both base lending rates and risk spreads vary. The following chart shows how the cost of debt can vary over time. The implication is that there are certain times when real estate borrowing is more beneficial than other times, although leverage has been accretive for core strategies over most long-term hold periods. As of Q4 2020, the steep drop in Treasury rates due to COVID-19 has created favorable borrowing conditions—a signal to consider higher leverage levels.

How should LPs manage real estate leverage?

Institutional investors currently manage real estate leverage in a number of different ways. Many have overall portfolio guidelines, with some extending restrictions by investment style, typically allowing lower leverage for core strategies and higher leverage for riskier strategies. For fund investments, institutional investors largely delegate leverage decisions and execution to managers, although most funds have explicit limits for individual assets as well as overall fund leverage. As shown in Exhibit 2, funds that qualify to be included in the NFI-ODCE must maintain leverage levels below 35%, while value-add funds have leverage levels restrict leverage to around 60-70%.

In many ways, the general practice of using higher leverage for higher risk strategies and lower leverage for lower risk strategies is counterintuitive. Core strategies often consist of properties with longer-term leases and fewer needs for capital expenditures— typically conditions that allow for greater leverage. Value-add and opportunistic investments often involve properties that have lower occupancy rates and require extensive capital improvements, resulting in greater uncertainty regarding future cash flow and values. By comparison, many sectors with volatile cash flows and uncertainty about future market conditions, such as technology companies, employ low levels of debt/leverage.

Some potential implications:

- Use more debt for lower risk strategies, and less debt for higher risk strategies. Debt for higher risk strategies and with higher loan-to-value ratios typically comes with higher interest rates and more onerous terms than debt for lower risk strategies. This would argue for utilizing more debt for core strategies (particularly apartments) and less debt for higher risk strategies. In practice, most higher risk strategies are executed through private closed-end funds commingled with many investors and in some cases, track records of strong performance using high leverage levels. Changing general partner terms and practices may be difficult to achieve, particularly for those with good track records.

- Consider ways to lower the cost and increase the flexibility of real estate debt. For mortgage debt, the least expensive and most flexible financing typically is available for low-leverage loans on “core” stabilized properties. The tipping point where lenders charge higher interest rates varies over time and by property type, but has typically been in the 50–70% range. In addition, interest rates for multifamily apartments are often lower than for other property types if originated by government-sponsored entities such as Fannie Mae and Freddie Mac.

Plan-level financing

An innovative way to minimize the costs of debt and maximize flexibility is using overall fund level assets (e.g., cash, securities, etc.) as collateral for real estate portfolio debt. Secured, fund level borrowing rates are almost always lower than mortgage interest rates, even for low leverage core properties. Fund level debt also reduces the use of asset-level mortgage debt that can sometimes reduce the potential buyer pool when selling an asset. Finally, fund-level leverage can be structured with a range of maturities that act as a partial hedge if interest rates rise and property values increase.

At least one state pension plan, Massachusetts Pension Reserve Investment Management, has utilized this structure since 2013. According to their 2020 Annual Report, “By utilizing the securities lending financing capabilities, the LLC is able to achieve lower borrowing costs for the Real Estate Portfolio and allow more flexibility within the real estate debt program.”7 Other institutional investors have executed or evaluated this approach.

There are both positive and negative implications of fund level real estate debt, as shown in Exhibit 3 (above).

In conclusion, leverage is an important part of the real estate capital stack. Used wisely, it can enhance returns and provide other portfolio benefits. Academicians have raised questions about the value of leverage as deployed by private equity funds using relatively high (>65%) leverage ratios, although there many managers that have added value with leverage. Institutional investors should continue to use moderate levels of leverage but also explore ways to minimize the cost and maximize the flexibility of real estate leverage.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us