May 16, 2024

By Derek Wyatt, Managing Director, RCLCO; Patricia Bacalao, Vice President, RCLCO; Nicholas Stefanoni, Senior Associate, RCLCO

Introduction

Across the country, both urban centers and established suburbs have contended with a mismatch between the desire to densify with contemporary mixed-use development and their existing land use patterns of single-use, low-density development. In particular, many grocery stores were built as sprawling, low-density stores in central locations that today present an inefficient use of valuable land, one that in many cases is no longer the highest and best use of a desirable site.

As a solution to this land use problem, many owners and developers have identified the opportunity to transform low-density grocery sites into higher-value development by delivering new multifamily communities with ground-floor grocery stores. RCLCO’s research into the impact of ground-floor grocers, initially completed in 2016, updated in 2020, and revisited in this new analysis, demonstrates the meaningful competitive advantages that these projects gain over nearby competitors. Based on our analysis of Whole Foods, Trader Joe’s, and other premium grocers, the presence of a ground-floor grocer typically results in meaningful rent premiums over competitive communities and generates overall positive project outcomes.

Grocery Site Redevelopment Strategies

Single-land-use retail centers are a common but often overlooked part of our built environment. Typically the result of outdated single-use zoning and minimum parking requirements, a surface-parked retail center may be almost as American as the cheeseburger and fries served up in a center’s fast-food drive-thru. In North America, there are nearly 140,000 neighborhood and community centers, comprising a total of 4.4 billion square feet of retail space, according to CoStar. Of these, around 8,350 properties are listed as anchored by a supermarket, featuring nearly 700 million square feet total at an average rentable building area of 83,500 square feet per retail center. Approximately 75% of the supermarket-anchored centers were built before 2000, an indication of not only the age and quality of these assets but also the scale of the redevelopment opportunity.

As a strategy to procure these sites in visible and desirable locations, many developers and grocers have started to partner to redevelop existing grocery stores into multifamily housing anchored by the same grocery store on the ground floor. Related California struck an agreement with Vons (owned by Albertsons) to redevelop the existing store into multifamily housing, with 30% of the 280 units dedicated to low- and middle-income households. Vons will become the anchor retail tenant of the new development, now called 710 Broadway, and will be afforded a state-of-the-art 53,000 SF store in exchange for selling the land to Related California.

Source: Related California

Source: Foulger Pratt

Similarly, Foulger-Pratt collaborated with Albertsons to build The Exchange and Beckert’s Park, two apartment communities anchored by Safeway grocery stores in the Washington, D.C. area. Delivered in 2013, The Exchange marked Foulger-Pratt and Albertsons’ first collaboration, which replaced a smaller and aging Safeway store with a 17-story mixed-use development that takes advantage of a Metro-adjacent site by offering 486 rental units and a new 58,000 SF Safeway, an expanded store right-sized to meet the needs of a growing suburb. Following the success of The Exchange, Foulger-Pratt and Albertsons teamed up again in 2020 to deliver Beckert’s Park, providing 325 units and a new 60,000 SF Safeway store. In addition to expanding the size of the original Safeway by 10,000 SF, the overall mixed-use development marks the significant value transformation of a prime, urban site in Washington D.C.

Concurrent with these emerging trends at the property level, there is also an opportunity to integrate grocery/retail redevelopment into a more comprehensive, enterprise-level strategy. Notably, Kimco Realty, the country’s largest publicly traded real estate investment trust (REIT) focusing on grocery-anchored shopping centers, has recently been reimagining its retail properties, often aging or underperforming assets in prime locations, into new mixed-use centers. With the 2021 merger with Weingarten Realty and the recent acquisition of RPT Realty, Kimco greatly enhanced its ability to implement this strategy nationwide across its nearly 600-property portfolio, including high-profile projects at the Pentagon Centre in Virginia, Lincoln Square in Philadelphia, and the River Oaks Shopping Center in Houston.

In its most recent annual financial filings, Kimco described its strategy as such:

“[Kimco’s] focus on high-quality locations has led to significant opportunities for value creation through the reinvestment in its assets to add density, replace outdated shopping center concepts, and better meet changing consumer demands…[Kimco] continues to place strategic emphasis on live/work/play environments and in reinvesting in its existing assets, while building shareholder value.”

In order to implement this intentional strategy, Kimco has secured entitlements for 9,945 multifamily units, of which 3,157 units have been built as of year-end 2023. With a focus on key value creation projects, community enhancement, and achieving the highest and best use of real estate, Kimco is a compelling case study for building a company strategy around the evolution of shopping centers into dynamic, mixed-use hubs, integrating housing and grocery anchors, in response to shifting consumer preferences.

Source: Kimco

Methodology

Overall Framework

In order to adequately measure the impacts of a ground-floor premium grocer on apartment performance, RCLCO relied on apartment performance data from Axiometrics for 90 apartment communities across 28 different MSAs, each of which offer an integrated grocer on the ground-floor. Each case study project’s performance was individually compared to the performance of two to five comparable apartment communities, which—barring the presence of a ground-floor grocer—represent the most comparable apartment product in terms of age, scale, quality of execution, and market positioning within the immediate local neighborhood of each case study.

This analysis sought to isolate the premium that is derived from the presence of a ground-floor premium grocer. Many apartment communities that contain a ground-floor premium grocer earn a noticeably higher premium relative to local comps. However, a meaningful share of this premium is due to the higher-quality unit finishes and amenities, rather than the impact of the grocer itself. By quantifying the premium for each unit finish and amenity, we were able to isolate the premium earned directly by the ground-floor grocer.

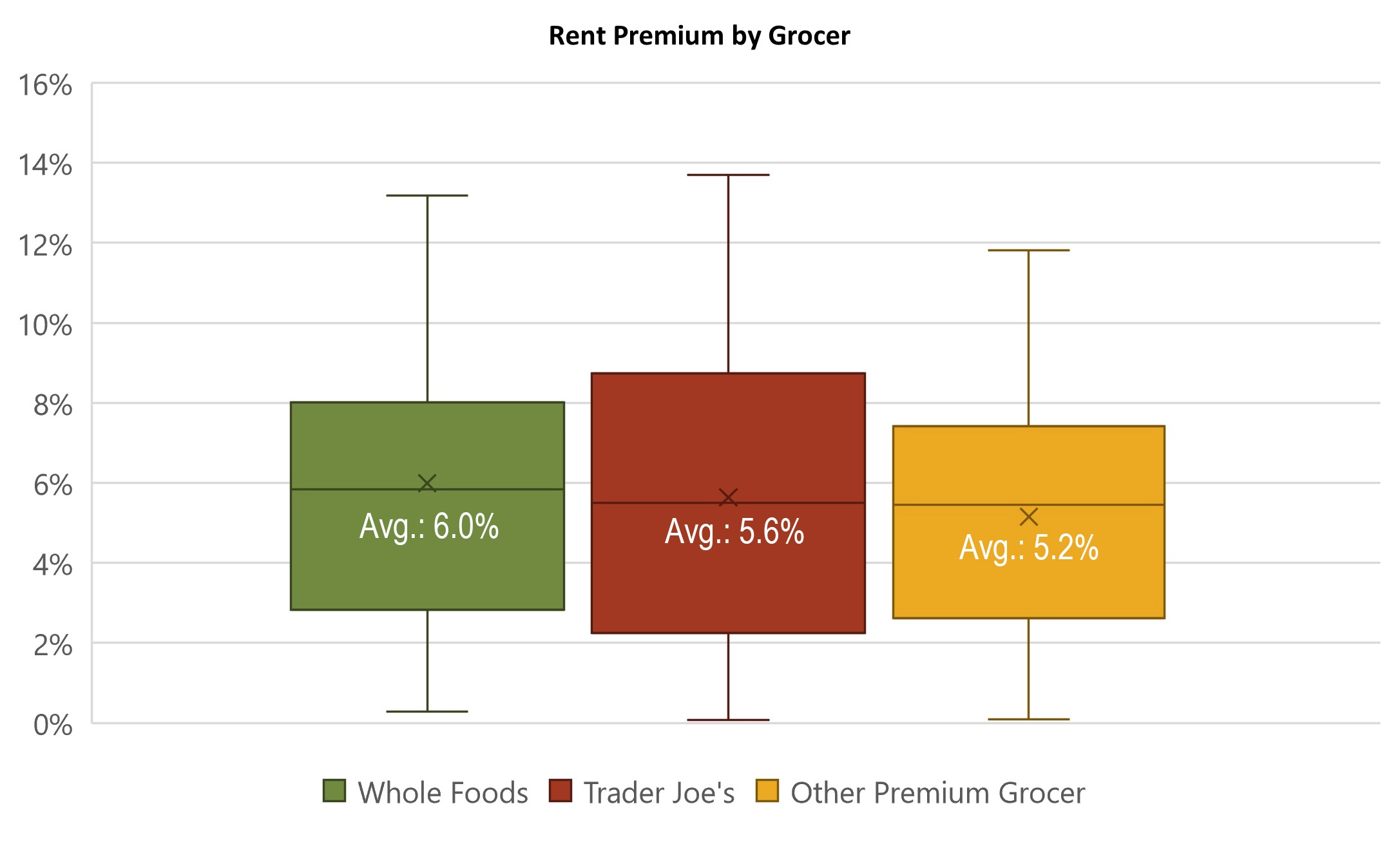

Rental Premium

RCLCO analyzed 37 apartment communities with a ground-floor Whole Foods tenant, 21 with Trader Joe’s, and 30 with Other Premium Grocers, located in 29 different MSAs and 71 submarkets across the nation.

After identifying each case study, RCLCO then selected between two and five nearby apartment buildings within each local neighborhood that were similar in terms of age, scale, type of construction (i.e. low-, mid-, and high-rise), quality of execution, and overall market positioning. We collected the average asking rents for each case study and comparable community. The rents at each comparable community were then adjusted for size (to allow apples-to-apples comparisons of rents), and further adjusted to control for other qualitative and quantitative differences between properties, such as building age, quality of location (measured using Walk Score and Transit Score), in-unit finishes and features, and quality and quantity of community amenities. The resulting adjusted rents for the comparable properties were then compared to the average rent in the grocer-anchored case study building. This methodology allowed us to make a quality-adjusted comparison, meaning that the resulting difference in rents between each case study and its comparable communities can be likely attributed to the impact of a ground-floor premium grocer tenant.