May 22, 2023

Originally published via UrbanLand

Prospects for the U.S. real estate market and economy changed little over the past six months, based on a survey of real estate economists. Broadly, the economy will slow in 2023 and 2024, with recovery expected to begin in 2025. The real estate market will follow suit, with flat to negative results over the next two years, followed by mostly positive news in 2025. The constancy of the forecasts can be attributed in part to the clear signaling of the Federal Reserve regarding interest rate increases, as well as the underlying strength of both the economy and real estate markets.

The Real Estate Economic Forecast, produced by the ULI Center for Real Estate Economics and Capital Markets, is based on a survey conducted in April 2023 of 41 economists and analysts at 37 leading real estate organizations. The forecast is based on the median responses gathered in the survey, which reflect a wide range of views both better and worse.

Although the overall sentiment of the Spring forecast changed little since the prior survey six months ago, in many cases minor improvements to the 2023 forecasts were offset or balanced by comparable downgrades in the 2024 predictions. For example, the 2023 GDP growth forecast improved to 0.9 percent from 0.5 percent, while the 2024 GDP forecast fell to 1.5 percent from 2.1percent, leaving the two-year average nearly the same. As with GDP, most of these changes are not dramatic, but do incorporate a shift in the predicted upcoming slowdown to later in 2023 and continuing into 2024.

Another conclusion for the Survey is that real estate economists expect that, after subpar performance this year and next, the economy will approach normal growth patterns in 2025, with real estate slightly lagging, depending on property type. Some of the key 2025 forecasts that are favorable compared to long-term averages include GDP and employment growth, the unemployment rate, single family starts, and rent growth forecasts for apartments, industrial, and retail.

Secure your seat for our most highly anticipated webinar of the year – the ULI Real Estate Economic Forecast! Complimentary and available to ULI members only, this lively debate features insights from the industry’s leading economists and analysts. Register Now

Key Findings for Commercial Real Estate

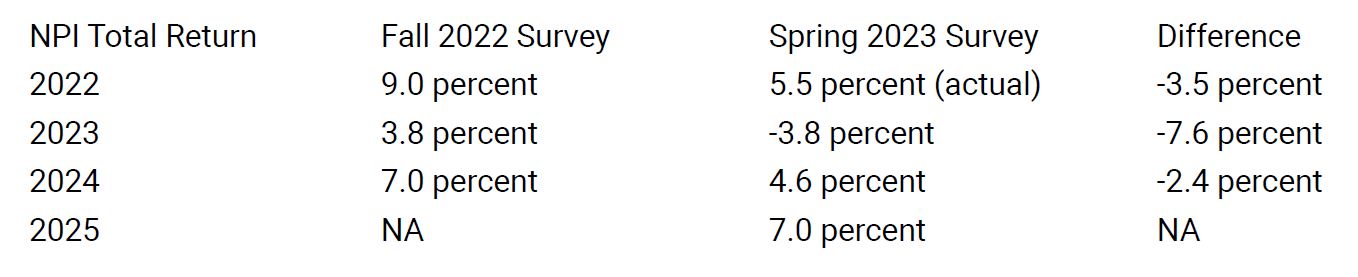

One forecast that did meaningfully change was total return from unleveraged core real estate (NCREIF Property Index or NPI),which fell relative to six months ago. Compared to the 2022 to 2024 period from Fall 2022, the current return forecasts (plus the2022 actual results) are 4.5 percent lower on average (see below), with the greatest difference in 2023. While investors will likely be disappointed by these lower returns, they are much higher than those posted during the GFC.

One positive likely to result from low returns is that capitalization rates or income yields, which have fallen to all-time lows, will move closer to long-term averages. This is due to predicted rent growth, which should lead to increases in Net Operating Income(NOI). Economists predict that the overall NPI capitalization rate will increase to 4.8 percent by 2025, up from 4.0 percent in 2022,the lowest capitalization rate on record. This is still below the long-term average of 5.5 percent, but a reasonable level given the forecast 10 Year Treasury rate of 3.15 percent in 2025.

Survey respondents forecast that U.S. real estate transaction volumes will fall to $425 billion in 2023 (from $730 billion in 2022), the lowest year since 2013. Transactions will rise to $525 and $695 billion in 2024 and 2025, respectively. The 2023 and 2024 forecasts are down from six months ago but well above the long-term average of $445 billion. CMBS debt issuance is predicted at below average levels for the forecast period. Issuance is projected to be $50 billion in 2023, $64 billion in 2023 and $83 billion in 2024. In addition to reduced CMBS availability, recent problems at some regional banks have raised concerns about both the cost and availability of real estate debt over the next several years.

Commercial real estate prices, as measured by the MSCI Real Assets Commercial Property Price Index (CPPI) are projected to fall by 8.0 percent in 2023 (the first decline since 2010) and increase by 2.6 percent in 2024 and 5.0 percent in 2025.

Expected NPI returns are closely aligned for all property types with the exception of office. From 2023 to 2025, economists estimate that total returns will average 4.2 percent for retail, 4.1 percent for apartments and 4.0 percent for industrial. Forecasts for 2023 and 2024 are all down from the prior survey. The fact that retail is expected to lead all property types may be surprising, but prior write-downs have positioned retail with the highest income returns of all property types—5.1 percent as of the first quarter of 2023. Prospects are much less sanguine for the office sector – total returns are expected to average -2.2 percent over the same timeframe, following a -3.4 percent return in 2022.

Returns for equity real estate investment trusts (REITs) are predicted to rebound from the -24.4 percent return in 2022, with forecasts of 4.0 percent in 2023 and 10.0 percent in 2024 and 2025, close to the 20 year average of 11.3 percent. Despite slower economic growth, industrial, apartment and retail rent growth is forecast to be positive and generally favorable relative to long term averages. From 2023 to 2025, average rents are forecast to average 4.7 percent, 2.8 percent and 2.1 percent for industrial, apartment and retail, respectively. These compare to long-term averages of 2.6 percent, 2.6 percent and 1.2 percent, respectively. Office will continue to under-perform, with average rent growth of -1.6 percent, reflecting record high vacancy rates.

The industrial availability rate will increase to 5.6 percent in 2025 from 4.9 percent in 2022, both well below the long term average of 9.7percent. Prospects for the apartment sector softened since the prior survey. Expected vacancy rates in both 2023 and 2024 increased by 160 basis points over the past six months. On a positive note, the forecast 2025 apartment vacancy rate of 5.1 percent is equal to the long-term average.

The availability rate forecast for neighborhood and community centers was lowered to 6.9 percent in 2023 and 2024 and 6.8 percent in 2025. The 2023 and 2024 forecasts are 80 basis points lower than those of last Fall and well below the long-term average of 9.8 percent. Economists downgraded the office sector further compared to six months ago, as reduced office usage appears more likely going forward. Office vacancy rates will reach 18.7 percent in 2023 and 19.0 percent in 2024 and 2025, all well above the long-term average of 14.6 percent.

Prospects for the hotel sector have improved over the past six months, as leisure travel has been particularly strong. The national occupancy rate is expected to average 63.5 percent in 2023, climbing to 64.8 percent in 2025. Forecast occupancy rates are higher than the prior forecast and above the long-term average of 61.1 percent (but lower than the 2019 pre-COVID level of 65.9 percent). Hotel revenue per available room (RevPAR), will increase by 7.0 percent in 2022, and 6.2 percent and 5.0 percent in subsequent years.

The outlook for the single-family housing sector calls for a sharp decline in starts in 2023, followed by increases in 2024 and 2025. Economists are forecasting 850,000 new housing starts in 2023, up from 800,000 predicted six months ago. Starts will rebound to 950,000 in 2024 and 1.1 million in 2025, both above the long-term average of 917,000. Average home prices will fall by 4.6 percent in 2023, but are predicted to stabilize in 2024 and 2025, averaging 2.6 percent.

More Urbanland ULI Forecasts

- ULI Forecast: Forecasters Downgrade Prospects for U.S. Real Estate Sector and Economy

- ULI Forecast: Positive for U.S. Real Estate Despite Higher Inflation, Interest Rates

- ULI Forecast: Increased Inflation, Slower Growth in Coming Years

- ULI Forecast: Employment Growth, Rebounding GDP for U.S. Economy

Key Findings for Major Economic Indicators

The ULI Real Estate Economic Forecast continues to support the likelihood of the U.S. entering into an economic slowdown and possible recession over the next 12-24 months. Annual GDP is projected to grow by 0.9 percent in 2023, 1.5 percent in 2024 and 2.5 percent in 2025.

Economists predict that the economy will generate 1.5 million net new jobs during 2023, up from 0.6 million in the prior forecast. (Over 1 million jobs have been added as of March.) Job growth will decelerate to 0.8 million in 2024, but rebound to 1.8 million in 2025, well ahead of the long-term average of 1.2 million.

The forecast calls for the U.S. unemployment rate to end 2023 at 4.0 percent, up from the 2022 rate of 3.5 percent. The unemployment rate is predicted to rise to 4.6 percent in 2024 before moderating to 4.2 percent in 2025, all well below the long-term average of 5.8 percent.

Inflation expectations are similar to the prior forecast. Economists forecast that the Consumer Price Index (CPI) will rise by 4.1 percent in 2023, down from 6.5 percent in 2022. The CPI is expected to rise by 2.8 percent in 2024 and 2.5 percent in 2025, close to the twenty-year average of 2.5 percent.

Survey participants forecast that long-term interest rates will moderate through 2025 as inflationary pressures recede and the Federal Reserve reduces short term interest rates. Responding economists predict that the 10-year U.S. Treasury (UST) note will end 2023 at 3.5 percent (close to the rate in early May), end 2024 at 3.3 percent, and end 2025 at 3.15 percent, above the 20 year average rate of 2.9 percent.

Summary

Respondents to the spring ULI Real Estate Economic Forecasts made relatively minor changes to economic and real estate forecasts over the next three years compared to the prior forecast (Fall 2022), with a modest upgrade to 2023 performance, coupled with slightly lower estimates for 2024. The Spring 2023 forecast added 2025 as a forecast year, and real estate economists are predicting a solid recovery to both the economy and real estate markets in that year.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.