September 16, 2023

Originally published in PREA Quarterly Magazine

Data centers are specialized buildings used to house computer systems and associated components, such as telecommunications and storage systems. Data centers have one of the strongest demand profiles in the entire real estate sector, with much of the demand targeting a small number of markets. Returns have been strong for the past decade, and institutional investors are increasingly looking at data centers as a way to earn outsized returns, albeit with meaningful risk.

Types of Data Centers

Enterprise: Facilities are wholly built, maintained, operated, and managed by companies for the optimal operation of their own IT equipment. Examples of large enterprise users include banks, brokerage firms, insurance companies, and other large corporations.

Cloud/Hyper-Scale: Facilities are built to accommodate the scalable applications revolving around the cloud, big data, and distributed storage. Large hyper-scale users include Amazon, Google, Microsoft, and Salesforce.

Multitenant/Colocation: Facilities are built with the aim of accommodating multiple companies that lease space within the data center. Generally, a data center operator maintains the building and critical power systems, provides security, and leases rack space to end users, which maintain their own equipment (servers).

Building requirements include an uninterruptible power supply, redundant communications connections, environmental controls (air conditioning, fire suppression, etc.), cooling systems (including chiller units and water-cooling systems), and high security. Data centers are often in stand-alone, industrial-style buildings, but they can also be in mixed-use properties, including office buildings.

More PREA Articles

Demand Drivers

One of the most compelling reasons to consider investing in data centers is the very rapid growth in underlying demand. Demand for data storage is growing at an estimated 20% per year through 2026 and will likely remain high for the foreseeable future. Some reasons for the high sustained growth in demand include the following:

Cloud Computing: Data storage is rapidly moving from hard drives and personal devices to cloud-based storage, exponentially increasing demand for data storage.

IoT and 5G: The growth of both the Internet of Things (IoT) and 5G technology will require cloud providers to lease data center space near large population centers to make accessing data-heavy content simpler for end users. Mobile device internet traffic has more than doubled since 2016 and is projected to continue to increase.

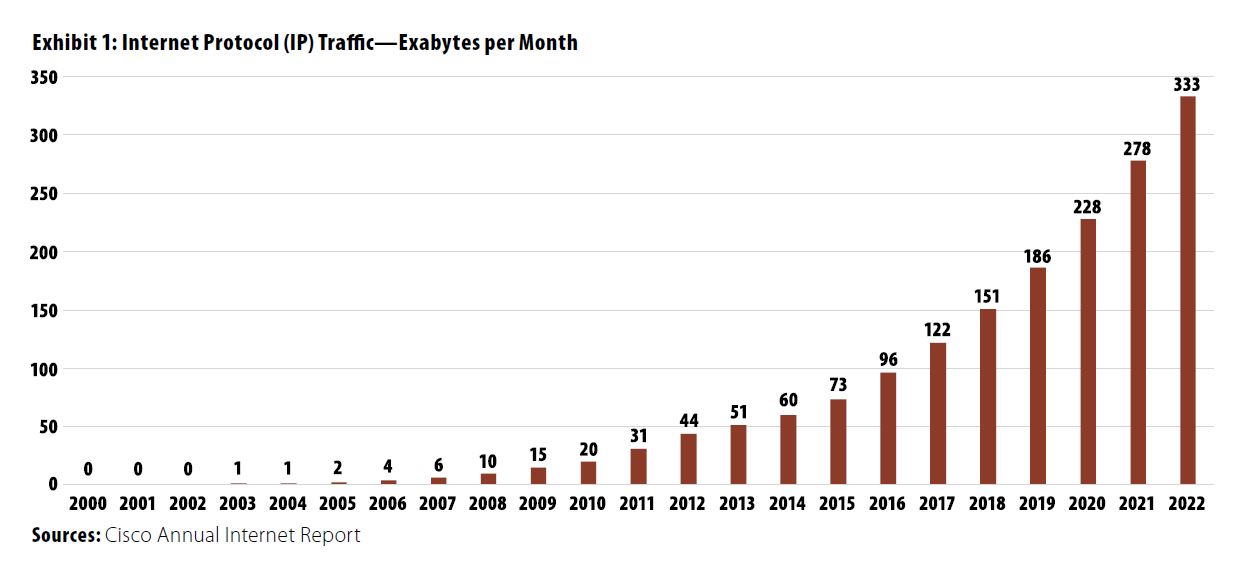

Consumer Proliferation: The number of IPv6 (the most recent version of the internet protocol, or IP) smartphones and tablets is expected to grow by 21% per year through the end of 2027, fueling demand for resilient, low-latency IP and cloud infrastructure (Exhibit 1).

Proximity to End Users: The rising mobile workforce and demand for increased data and application availability with low latency requires additional data centers in smaller markets.

Other: Autonomous vehicles and artificial intelligence will require large amounts of quickly accessed data.

Risks

As a specialized property type, data centers present numerous risks, many of which are unique to the sector.

- Obsolescence might result from advancements in technology.

- Scalability could reach a level at which it is more cost effective for hyper-scalers to own everything, eliminating the need for many data centers and data center operators and making the industry function as a public utility, with hyper-scale cloud providers (such as Amazon and Google) dominating the space.

- The IoT may enable connected devices to replicate the functionality of data centers. This is highly unlikely over the near to mid term.

- Capital expenditures can be quite high depending on the level of services provided. The capex burden is approximately 25% of NOI, compared to 15% for all real estate and approximately 30% for hotel and office properties.1 In some cases, capex is the responsibility of the tenant as opposed to the property owner.

- Sourcing power for data center developments has become a timely and difficult proposition in certain infill data center markets. Most notably, northern Virginia, the world’s largest data center market, is experiencing significant delays in power procurement for newly constructed and under-construction facilities.

- Greenhouse gas emissions from data centers are significant, exceeding the emissions from airliners. Data center owners are exploring clean energy, fuel-cell storage, and recycling of data, but regulatory actions are possible.

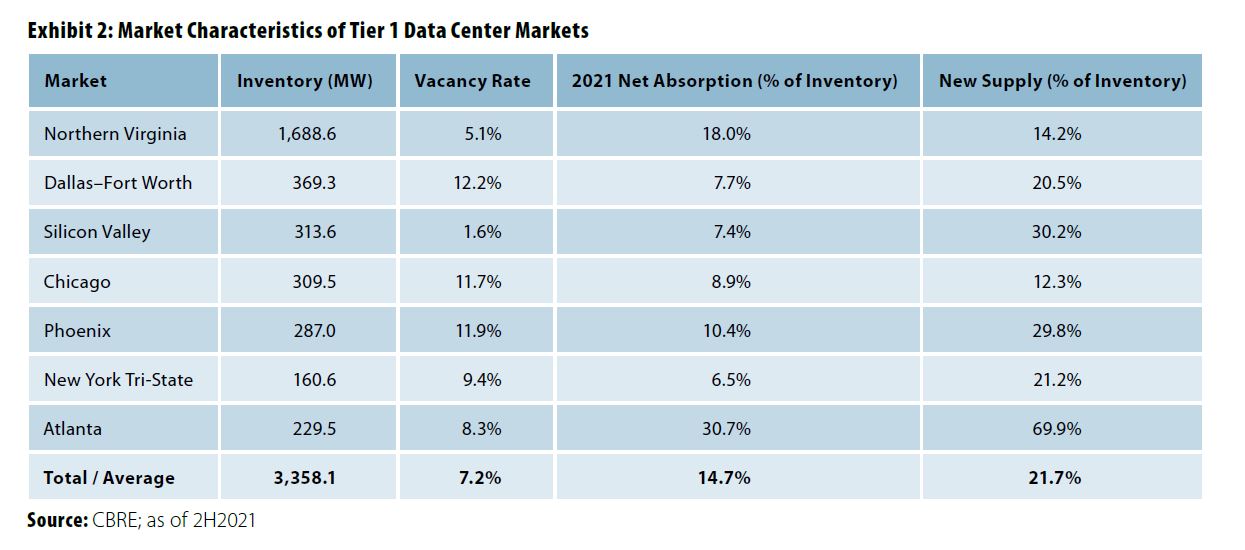

Approximately 728 megawatts (MW)2 of new supply was under construction within primary markets at the end of 2021, according to CBRE, representing 21.7% of the current supply. More than 320 MW of this pipeline is pre-leased, however, signaling strong tenant demand and market fundamentals.

Data Center Markets

Seven markets are generally considered to be Tier I, or primary, markets, based on size and connectivity. Of the Tier I markets, northern Virginia is by far the largest because of its proximity to fiber lines, which were initially built for military and government usage in the Washington, DC, area. Northern Virginia is more than four times larger than the Dallas–Fort Worth market, the second largest data center hub.

The primary markets (shown in Exhibit 2) vary in terms of their size, market fundamentals, and relative attractiveness. In general, the most important qualities of an attractive data center market include these:

Proximity to a Major Population Base: All primary markets benefit from proximity to large population bases.

Fiber Connectivity: Fiber connectivity is relatively limited across the US; however, it is available across all the primary markets.

Tax Incentives: Tax incentives and political environments vary by market, with northern Virginia and Atlanta offering the highest incentives (e.g., exemptions from sales and use taxes).

Power Cost and Availability: Low power costs reduce the operating costs and increase attractiveness to tenants. Recently, power availability has become a major concern.

Disaster Risk: A low risk for natural disasters offers a lower probability of disruption.

Land Costs: Data centers tend to aggregate in areas where land is cheaper. Other markets that are growing, have strong supply-demand fundamentals, and could potentially turn into primary markets in the near to mid term include Hillsboro, OR; Columbus, OH; Salt Lake City, UT; Kansas City, MO; and Miami.

Institutional Investment Opportunities

The data center investment market is growing quickly, as public, private, and institutional investors are drawn to the sector. Since 2015, more than 700 data center transactions representing an aggregate value of $182 billion have closed. As of June 2022, there were 87 transactions valued at $24 billion.

Transaction activity has increased since 2015 at a compound annual growth rate of approximately 27% in number of transactions and 64% in aggregate capital, with private equity investment accounting for a larger portion of transaction activity than public REITs each year. Private equity firms accounted for approximately 42% of all data center acquisitions from 2015 through 2018, 65% from 2019 through 2021, and 90% in the first half of 2022.

Core cap rates and returns depend heavily on market (Tier I, II, III) and data center type (turnkey versus powered shell, enterprise versus colocation). For stabilized institutional-quality properties, cap rates typically range from 4.25%–6.25% with five-year unleveraged internal rates of return (IRRs) ranging from 7.0%–8.5% (lower for Tier I colocation or hyper-scale powered shells and higher for enterprise and turnkey facilities). Development opportunities often begin as speculative and rapidly turn into build-to-suit because of the high demand for space. For development, investors generally demand a stabilized yield premium of 75–150 basis points over prevailing market cap rates, depending on market and data center type. Developers target stabilized leveraged IRRs ranging from 12%–19% or more, depending on the risk profile of the opportunity.

Data center REITs have delivered stronger returns than the REIT average since 2014 (the first year Nareit tracked REIT returns for data centers). The current public data center REITs—Equinix, Inc. and Digital Realty—have a combined market capitalization of $112 billion (as of Sept. 30, 2022). Three former public REITs—CyrusOne Inc., CoreSite Realty Corporation, and QTS Realty Trust, Inc.—were acquired by KKR and Global Infrastructure Partners, American Tower Corp., and Blackstone Group, respectively.

Summary

Demand for data centers is growing faster than perhaps any other property type; data usage has grown and will likely continue to grow at exponential rates. Supply is growing rapidly as well, though it continues to be rapidly absorbed and now faces headwinds such as power procurement constraints that will likely keep the supply-demand fundamentals in balance. Data centers are a highly specialized building type with numerous features that may become obsolete and are not likely to have value to non–data center tenants if data center demand subsides. In addition, the sector has clustered in a handful of very competitive markets, although additional markets are increasingly attractive as proximity to end users has grown in importance. As with most alternative property types, specialized expertise is needed to develop and operate data centers. Despite all these concerns, with the right partners, data centers are likely to provide above-average returns going forward.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.