Medical Office Buildings Post-COVID – Shaken but Still Strong

Originally published in PREA Quarterly Magazine

The US medical office building (MOB) sector has been a strong performer for several decades because of rising expenditures on health care and the cost advantage of MOBs versus hospitals. COVID-19 shook the health-care sector in 2020 as nonessential procedures and doctor visits effectively shut down for part of the year. After opening back up in the second half of 2020, health-care properties were compelled to add a wide range of safety features and protocols, including mask mandates, visitor restrictions, and pre-visit clearance procedures. Despite these disruptions, MOBs have emerged from the pandemic as an increasingly important venue for the delivery of health-care services and an attractive property type for real estate investors.

COVID-19 Impacts

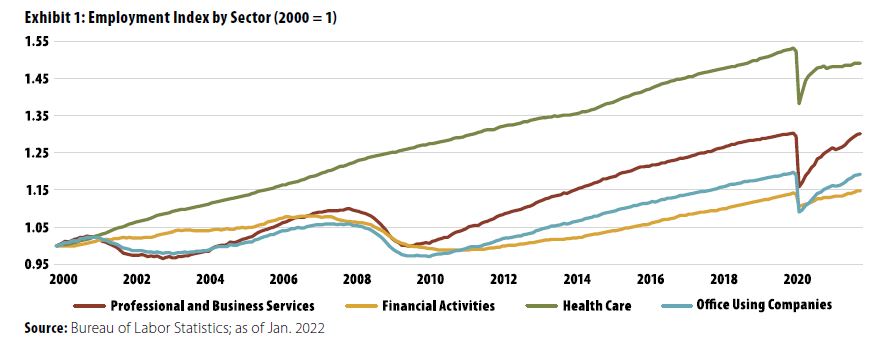

COVID-19 affected the MOB sector in numerous ways, some short term and some long term. At the onset of COVID-19, governments ordered health-care providers to curtail most nonessential services, both to maintain capacity to treat those infected and to stop the spread of the coronavirus through interactions with health-care workers and other patients. Although most health-care providers were able to keep their staffs employed throughout the lockdown, some organizations were not and some workers may have quit because of COVID or other concerns. As a result, health-care employment fell by 1.6 million jobs, or 10% of the workforce, from February 2020 to April 2020. As shown in Exhibit 1, this was an unprecedented development; the sector had grown at a steady pace for the prior 19 years, with no employment declines during previous recessions.

Rapid and steady growth in employment (and real estate requirements) had been one of the key positive attributes of health-care real estate, including MOBs, for the prior two decades. As Exhibit 1 shows, other sectors, such as professional and business services and office-using companies, exhibited both slower and more volatile growth, with declines in employment during recessions.

Although health-care employment declined rapidly in early 2020, it recovered more quickly than employment in most sectors. Within six months, health-care employers restored more than one million jobs, bringing the six-month decline to 4% (from the prior peak). This was a more rapid recovery than that of the economy as a whole, which had a deficit of 7% as of August 2020.

Although health-care employment growth picked up in mid-2020, it did so at a much slower pace than in prior periods, as some health-care workers reportedly left the industry because of the risks and burnout of dealing with COVID patients. Job growth slowed to 0.4% for all of 2021, the lowest rate in more than 30 years (not including COVID shutdowns). Employment growth will likely improve when COVID subsides; many hospitals are reporting a large backlog of unfilled jobs, particularly nurses.

The Case for MOB Investing

Accounting for about 10% of the total office space in the US, MOBs have been a strong and steady performer for many years, particularly when compared to traditional office properties. The reasons for historical (and likely future) strong performance include these:

- Strong space demand because of increasing expenditures on health care in general, a trend that will be supported by an aging population and biotech innovation over the next decade

- An ongoing shift in medical service delivery from hospital-based care to medical-office-based treatment, resulting in significant cost savings

- Limited new construction because of a small and distinct tenant base, resulting in lower and more stable vacancy rates compared to traditional office

- Much higher tenant retention (renewal rates are as high as 80% to 90%) because of patient preferences and synergies that develop within MOBs, reducing both downtime and capital expenditures compared to those of traditional office

Rising Health-Care Expenditures

Despite efforts to rein in costs, US spending on health care continues to grow at a rapid pace. According to the Centers for Medicaid and Medicare Services, US health-care spending grew by 9.7% in 2020, reaching $4.1 trillion, or $12,530 per person. This represented 19.7% of US GDP. The 2020 GDP share was elevated by COVID-related costs as well as a decline in GDP but is consistent with recent trends.

The share of the economy devoted to health care will likely continue to rise rapidly over the next decade as a result of many factors, including technology advances and the aging of the baby boomer generation. Congressional Budget Office projections suggest that, in the absence of changes in federal law, total spending on health care will rise to 25% of GDP in 2025 and 37% in 2050.

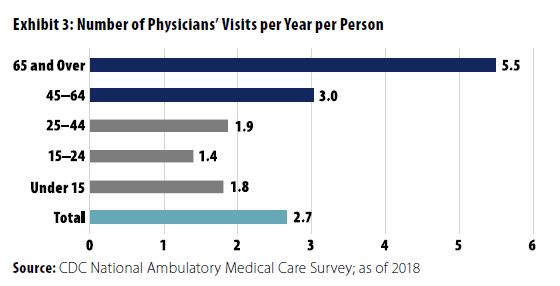

Exhibits 2 and 3 show that the senior population is growing rapidly and that visits to doctors and clinics increase with age. The population over age 65 will increase by 33% over the next decade (2.9% average annual growth), according to the US Census Bureau. This compares to 9.5% growth (0.9% annually) for the US population as a whole. Seniors are much greater consumers of health care than the overall population, visiting doctors twice as often as the overall population.

As the population ages across the US, growth in population and health services demand will be greatest in Sunbelt states. Texas, Florida, Nevada, Arizona, and Utah will lead the country in senior population growth over the next ten years, rising by more than 3% annually, according to the University of Virginia.

Medical Office Building Advantages

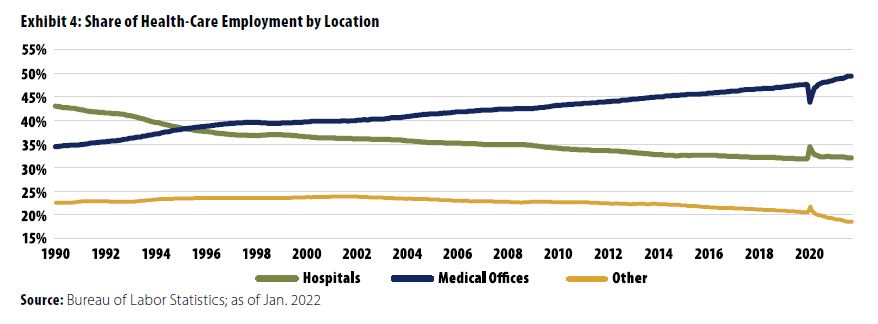

Rising health-care costs have pushed insurers and health-care providers to develop strategies to limit health expenditure increases. An important tool in that process is to move some patient care from hospitals to MOBs, where treatment is often less expensive. Technological advances have enabled many more procedures (including surgeries) to take place in outpatient clinics and/or physicians’ offices. As more procedures have migrated out of hospitals, the MOB share of health-care employment has been rising for more than 20 years and now comprises close to 50% of total health-care employment (Exhibit 4). There is little reason to expect this trend to change.

MOB Market Fundamentals

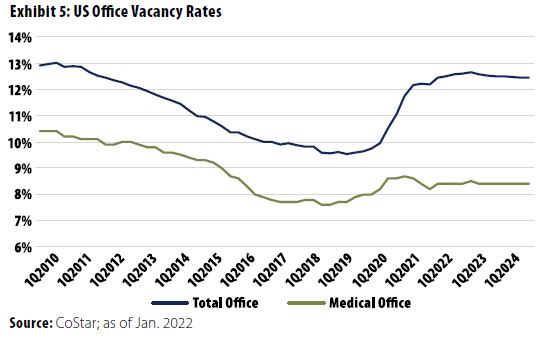

Strong employment growth and limited construction have resulted in MOB vacancy rates that are lower and less volatile than those in the rest of the office sector. Exhibit 5 shows that the national MOB vacancy rate averaged 220 basis points (bps) lower than the overall office vacancy rate over the 2010–2021 period. That difference has widened during COVID, standing at 400 bps as of the fourth quarter of 2021, and is expected stay at widened levels through 2024, according to CoStar.

MOB Capital Markets

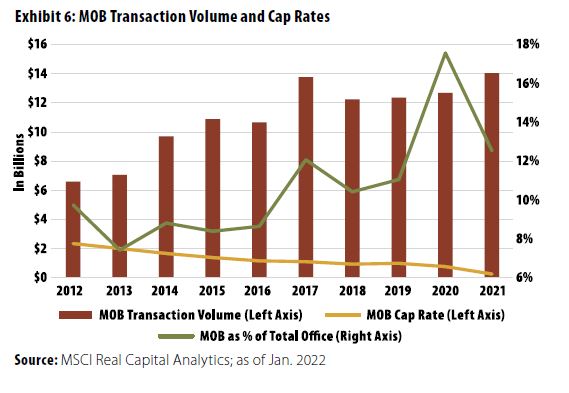

Over the past several decades, investors have shown increased interest in medical office properties. Transaction volumes have been growing for the past decade, and the 2021 total of $14 billion represents an all-time high, according to MSCI Real Capital Analytics (Exhibit 6). Investment in MOBs as a percentage of overall office transactions has been rising, reaching close to 18% of volume in 2020 before falling to a still-strong 12.5% in 2021. Rising investor interest has led to lower cap rates for MOBs. Average cap rates declined to 6.2% in 2021 from 7.5% in 2012. Significantly, the spread between MOBs and the overall office market went from a positive 36 bps from 2012–2014 (average) to negative 37 bps in the fourth quarter of 2021. The decline in cap rates and the rising share of the office transaction market may be because investors are developing a better understanding of MOB demand drivers and returns, as well as potential issues with traditional office, such as obsolescence and the impact of work-from-home policies.

Looking Ahead

MOBs continue to prove their ability to weather negative economic conditions, even one as extreme as the pandemic-induced recession of 2021. Despite the fact that many MOB tenants had to cease operations and in some cases lay off workers, vacancy stayed low and rent growth was very strong. The cost argument for shifting services from expensive hospitals continues to support increasing demand for MOBs. COVID has introduced a new reason to accelerate this shift—keeping healthy individuals away from potentially infectious hospital patients.

The COVID pandemic will likely result in some changes to the health-care sector that will ultimately affect MOBs. Tighter controls over patient health and exposures will likely be ongoing, as will some guest restrictions. Telemedicine and at-home technologies advanced during the COVID lockdown will continue to grow going forward, possibly dampening MOB demand. However, these changes look to be very much at the margin and are not likely to derail the ongoing importance of MOBs in health-care delivery.

Medical office properties have long been an attractive investment opportunity because of the size and strength of the health-care industry and the disciplined introduction of new supply. Ongoing efforts to reduce the cost of medical care and to cater to patient desires to have more convenient and less stressful health-care experiences will increasingly shift health-care services from hospitals to MOBs. Despite a few inevitable dislocations, the demand for medical office space will continue its strong growth.

Growing demand and controlled supply is likely to produce consistent long-term rent and income growth at MOBs. The sector’s resilience during recessions limits downside risk compared to the general office sector and other property types. Future COVID-like disruptions are possible but unlikely to be long lived. Because of these factors, MOBs will likely continue to attract institutional investors for the foreseeable future.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us