February 17, 2026

By William Maher, Director of Strategy and Research, RFA; Scot Bommarito, Vice President, Research, RFA; Andrew Janko, Managing Director, RFA; Amber Hughes, Senior Associate, RFA

Many data center investors have gotten comfortable that demand will continue to grow at a rapid pace in the age of AI. While that may be true, the dramatic supply response taking shape calls for more measured analysis.

Originally published via AFIRE

Data centers have emerged as a preferred property type among commercial real estate investors in the digital age, especially since the release of ChatGPT in 2022 inaugurated the AI race[1]. Conventional wisdom held that demand tailwinds would keep the sector flying high for years to come, and capital rapidly poured into the space in response. Meteoric demand led to ballooning construction pipelines.

Recently, focus has begun to shift from the attractive demand story to concerns about overinvestment and oversupply. The Wall Street Journal, New York Times, Economist, and Financial Times all featured headlines throughout the second half of 2025 questioning whether the data center boom is actually a bubble, akin to the telecom infrastructure bubble of the late 1990s.

This article adds some context to that conversation, estimating the size of the data center supply pipeline and situating it within the broader universe of commercial real estate investment. It finds that the stabilized real estate value of the current US data center supply pipeline is enormous, at roughly $1.8 trillion in our base case, with a wide potential range from $1-$3 trillion. In addition, technology companies will spend an additional $1-$2 trillion on servers and other computing equipment.

There are multiple risk factors associated with raising and spending this enormous pool of capital. The three main ones that we focus on include:

- Real estate capital markets may face challenges in securing sufficient capital to fund the data center pipeline and absorb its stabilized value at today’s market expectations.

- Tech companies forecast aggressive capital expenditures on data center infrastructure, but it is uncertain how much of that spending is for the real estate itself and whether companies can maintain their recent spending paces.

- AI does not generate meaningful revenues today. If revenue growth remains slow, tech stock prices may fall, leaving companies overextended on their data center commitments and leading to a wave of sublease space.

Given these risks, data center investors should exercise caution in their development strategies and investment assumptions, particularly on expected exit valuations and timing.

Sizing the Supply Pipeline

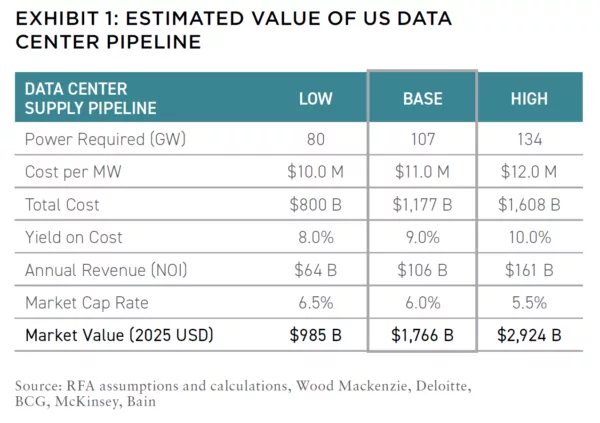

As a relatively new property type, information on the data center sector is still limited. Because of this, estimates of the existing data center inventory in the US vary, but they are generally around 40 gigawatts (GW) [2], including both colocation and hyperscale segments[3].

There is much less certainty about the future supply pipeline. Wood Mackenzie, a global research and consultancy group, reported tracking 134 GW of proposed data centers in the US in mid-2025. This represents a staggering 3.3x the existing inventory. The entirety of that pipeline is unlikely to deliver over the next several years due in large part to power constraints. Also, most data center development is built to suit, limited supply to actual tenant demand. As such, 134 GW serves as our high scenario for data center supply expansion. For our low scenario, we use the average new demand forecast for data centers through 2030[4]. This comes to 80 GW of supply to meet new demand. Our base case data center supply outlook is the midpoint of 107 GW.

A global research and consultancy group, reported tracking 134 GW of proposed data centers in the US in mid-2025.

One of the big questions about data centers is whether there will be enough capital to fund future development and absorb stabilized values. To estimate the market value of the data center pipeline, we assume construction costs ranging from $10 million/MW to $12 million/MW, development yields-on-cost of 8-10%, and valuation cap rates of 5.5-6.5%, as shown in Exhibit 1 below. Yields and cap rates vary between hyperscale and colocation data centers, but the above figures are reasonable estimates for the overall sector. These assumptions imply a roughly $1.8 trillion stabilized valuation of the current data center pipeline in our base case, ranging from $1-$3 trillion in our low and high scenarios.

Real Estate Capital

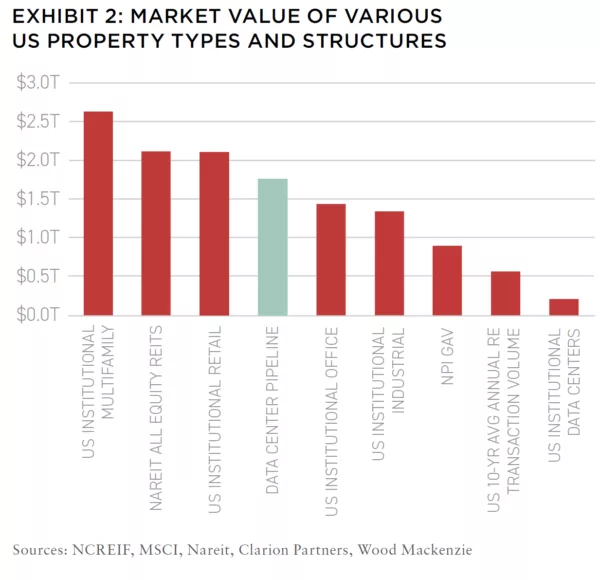

To put the estimated total market value into perspective, Nareit estimates that the enterprise value of the entire publicly traded REIT universe is $2.1 trillion (see Exhibit 2). The total market value of the NCREIF Property Index (NPI), a widely used commercial real estate benchmark focused on traditional property types, is just over $900 billion. Clearly, the large size of the US data center pipeline raises the question of whether the institutional real estate market will be able to absorb the projected stabilized value.

We recognize that data centers will appeal to other investors besides real estate-oriented groups.

Triple net lease and infrastructure investors will likely be attracted to what are often long-term leases with credit tenants. With this diversified investor base, it remains to be seen where average leverage ratios settle for data centers.

Core real estate investors typically utilize about 25-30% loan-to value financing while net lease and infrastructure investors typically

use greater leverage[5].

In the public markets, REIT LTVs have been fairly stable in the low 30% range over the last decade, averaging 33%. In 2025, the two publicly traded data center REITs averaged slightly lower LTVs of 25-30%, while net lease REITs had 35-40% leverage. Finally, non-traded REITs generally use about 50% leverage. LTVs of 25-50% on the data center pipeline would imply $0.9-$1.3 trillion of equity needed in our base case. In practice, it will likely be a range of investors that participate in data center investments, but the availability of sufficient equity remains unclear.

Tech Capital

In addition to real estate capital requirements, tech companies will also need to spend an enormous amount of capital to develop their data center infrastructure. Morgan Stanley estimates that Big Tech companies will spend around $1.4 trillion on data centers through 2029, representing an annual pace of $350 billion. Recent earnings reports provide some support for that estimate[6].

In the first three quarters of 2025, capital expenditures totaled approximately $280 billion across Amazon, Microsoft, Alphabet, and Meta, on track to reach $370 billion for the year. Still, questions remain about whether this pace of capex is sustainable, particularly if stock prices fall or earnings outlooks decline. It is also uncertain how much of this data center spending is destined for investment in the physical plant of the real estate compared to other costly network infrastructure (e.g., servers, semiconductors, power generation, and other networking equipment). The main point is that the huge amount of capital required to fund the data center pipeline may not be readily available from data center tenants.

Tech Revenue

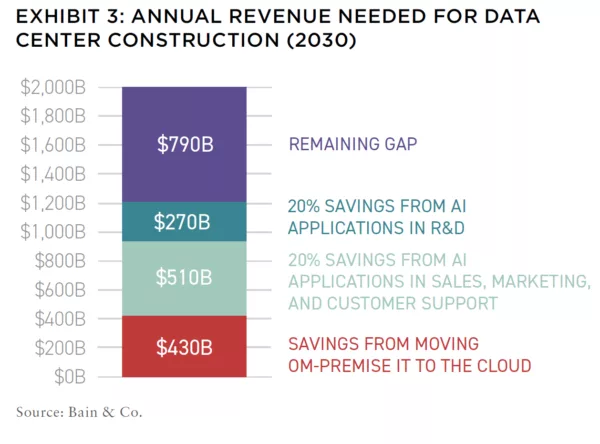

AI revenue limitations could also constrain the amount of capital tech companies have available for data center buildouts. Bain estimates that by 2030, $2 trillion in annual AI revenue will be required for AI infrastructure investments to pay off, assuming $500 billion of annual AI infrastructure spending.

According to their analysis (Exhibit 3), even after accounting for the cost savings likely to accrue from AI adoption, the global economy will be nearly $800 billion short of reaching that revenue target. Many AI services do not generate strong revenue streams today. Although most AI companies expect rapid revenue increases in coming years, it remains to be seen how sensitive users will be to the pricing of these services.

AI companies’ ability to demonstrate very rapid revenue growth will determine their ability to finance expansion of their data center infrastructure.

The outlook for data centers is closely tied to tech companies’ stock prices and earnings outlooks. If tech capital availability declines or revenue growth proves sluggish, the sector is likely to soften. The most acute risk is that hyperscalers’ stock prices decline, leaving them overextended on their data center commitments and forcing them to sublease their data center space.

Where Does It Go From Here?

Many data center investors have gotten comfortable that demand will continue to grow at a rapid pace in the age of AI. While that may be true, the dramatic supply response taking shape calls for more measured analysis. The sheer volume of capital required to finance data centers’ accelerated pipeline growth and absorb stabilized values at today’s market expectations presents meaningful capital risks to investors.

Having $1.8 trillion of data centers entering the market could weigh heavily on real estate equity capital’s ability to absorb the supply without activating some new sources of demand or compromising on price. Competition on development yields to win tenants and less attractive construction financing may lead to disappointing returns, as could meaningful cap rate expansion and timing delays. For the portion of the pipeline that does not deliver, some land investors may be left holding the bag.

It will likely take several years to know if we are in a data center boom or bubble. In the meantime, investors should focus on projects with near-term roadmaps to power and stabilization. Where possible, investors should seek to have forward sales at negotiated prices already in place to establish better certainty around residual values.

Finally, given the sheer size of the pipeline and the potential capital supply/demand imbalance, investors should be cautious in their expectation of exit valuations and timing on developments.

Having $1.8 trillion of data centers entering the market could weigh heavily on real estate equity capital’s ability to absorb the supply without activating some new sources of demand or compromising on price.

References

[1] See ULI’s Emerging Trends in Real Estate 2025 and IREI’s 2025 Institutional Real Estate Investor Trends report.

[2] See MSCI. Unlike other property types, data centers are sized by power not by square footage.

[3] Cloud / hyperscale data centers are single-tenant facilities that cater to the scalable applications revolving around the cloud, big data, or distributed storage; multitenant / colocation data centers accommodate multiple companies that lease space within the data center.

[4] New demand forecasts come from Deloitte, BCG, McKinsey, and Bain.

[5] As of 2025 Q3, LTVs in the NCREIF Fund Index – Open End Diversified Core Equity (NFI-ODCE), a commonly used industry benchmark among core real estate investors, averaged 26%.

[6] See “Big Tech has built the future. Now it has to deliver on the present” in Quartz, visited on 10/29/2025 and “When AI Hype Meets AI Reality: A Reckoning in 6 Charts” in The Wall Street Journal, visited on 12/1/2025.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.