September 25, 2025

By Derek Wyatt, Managing Director; Dana Schoewe, Principal; Scott Cottier, Associate

The vacation and investment home market is undergoing a noticeable evolution, driven by the shifting preferences and lifestyle needs of today’s buyers. In light of these changes, RCLCO conducted the 2025 version of its Vacation/Investment Home Survey (previously conducted in 2020, 2021, and 2023), to better understand the investment and ownership preferences of over 1,000 individuals with a net worth of over $1 million across the United States. By focusing on motivations for purchasing, renting, and amenity selection, RCLCO can apply these insights to help inform industry professionals designing, developing, and marketing new vacation and investment properties.

Four Key Takeaways from the 2025 Vacation/Investment Home Survey:

- Rising Interest in Investment-Oriented Vacation Homes

- Growing Attention & Awareness of Branded Residential

- Pent-up Demand & Opportunity at Lower Price Points

- Amenities Drive Purchase Motivations, with a Resurgence of Golf

1. Rising Interest in Investment-Oriented Vacation Homes

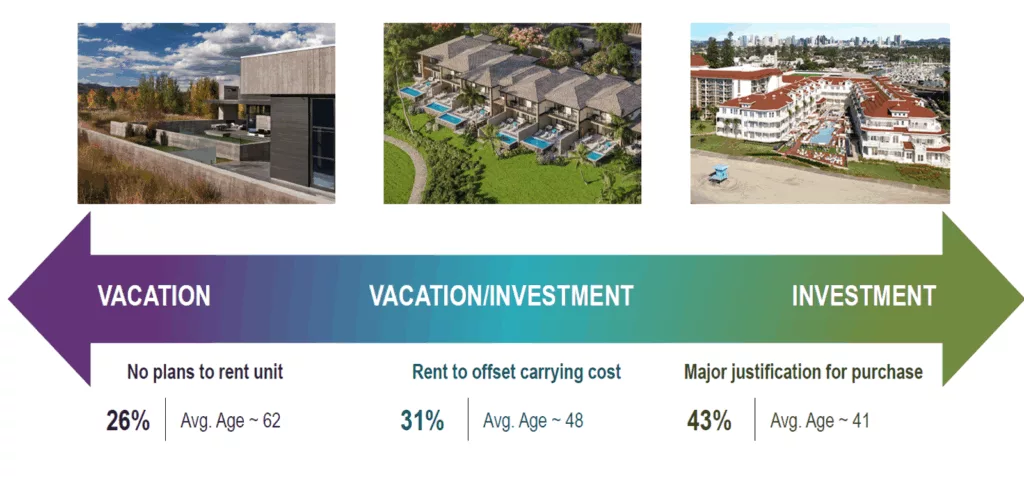

One of the clearest findings of the survey is the growing willingness of buyers across wealth levels to place their vacation homes into structured rental pools and utilize short-term rental platforms. Historically, many luxury buyers considered vacation properties as purely private retreats, but attitudes are shifting. Roughly 42% of qualified respondents in 2025 indicate that generating investment income is a major justification for their purchase, up from 33% when RCLCO last conducted the survey in 2023. This shift is likely driven by the abundance of professional rental management services, as well as a generational divide; younger buyers are more inclined to view rental participation as essential, while older buyers, who tend to be wealthier and can spend more time at their second homes, lean toward exclusive use. As new vacation and investment home development expands, turn-key rental management has become a critical decision factor for buyers. Even amongst the highest-net worth respondents, generating rental income has strong appeal; 73% of buyers with over $10M in net worth cited that generating investment income is a major justification for their purchase. Across wealth levels, short-term renting helps offset carrying costs and improves investment appeal without compromising on value.

2. Growing Attention & Awareness of Branded Residential

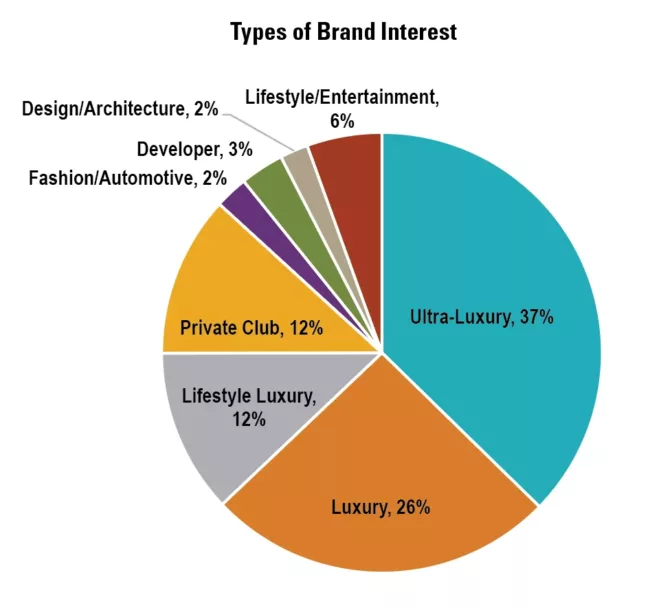

The latest survey also reveals growing enthusiasm for and awareness of branded residences. These projects bring established hotel, lifestyle, fashion, and entertainment brands into the residential space, applying their name, service standards, and operational expertise. Roughly 80% of qualified respondents said they are interested in branded residences, up from 75% in 2023. Respondents show they would pay a premium for a vacation home affiliated with a recognized luxury brand, citing key reasons such as improved investment security (especially in international destinations), elevated service and amenity packages, name recognition, quality assurance, and overall prestige and exclusivity. Driven by these advantages, branded residences are often priced at the very top of the market. A large share of respondents indicated they would pay a 20% to 30% premium for the services and investment security these residences provide. As these developments have continued to command meaningful premiums, the geographic footprint of branded residences has also expanded. While ultra-luxury hospitality brands are still the most desired type of branded residences, the field is expanding into more moderately priced options. Various fashion and even automotive companies have recently entered the branded residential sector, suggesting that brand loyalty and identity will continue to influence real estate purchasing behavior.

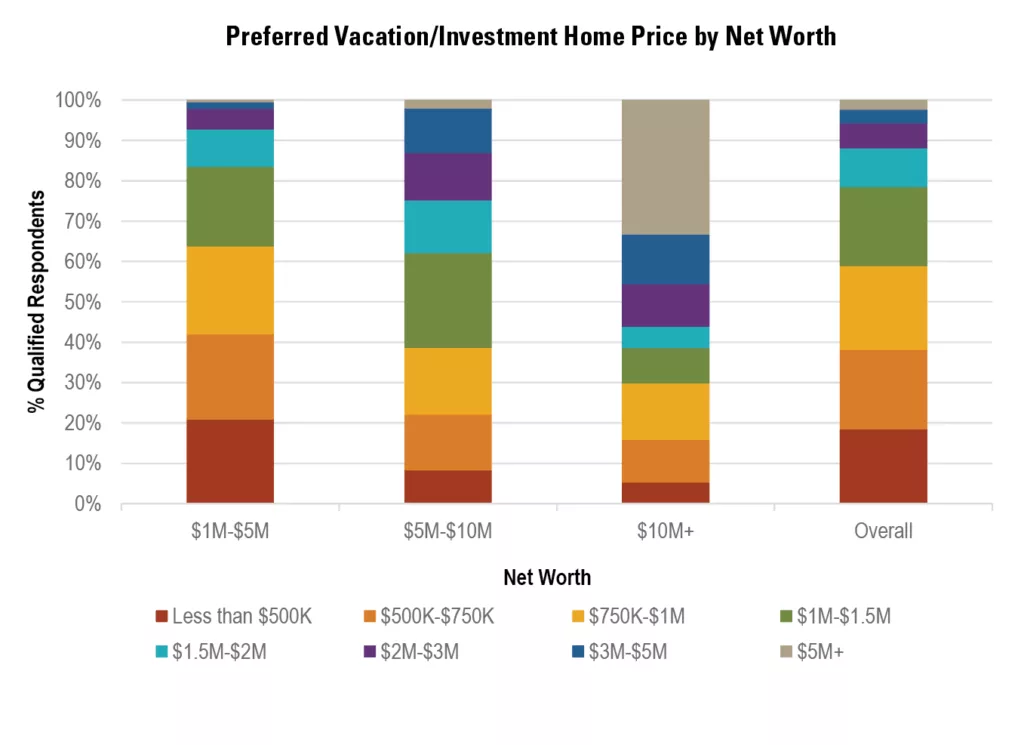

3. Pent-up Demand & Opportunity at Lower Price Points

While the increased prevalence of branded and ultra-luxury developments has been successful in addressing the wealthiest segment of vacation and investment buyers, this trend has not addressed the growing demand for vacation and investment units priced under $1 million. Roughly 60% of qualified survey respondents are searching for product under $1 million; for buyers with $1 to $5 million in net worth, smaller, more affordable units with lock-and-leave convenience and investment income potential are high-priority. However, there is a supply mismatch; as an example, in key mountain resort markets, only about 30% of sales have fallen below this price threshold in recent years. By addressing this demand with efficiently designed, service-enhanced communities, developers have the potential to broaden absorption and capture buyers who may, over time, trade up into higher tiers. Furthermore, offering innovative ownership structures and appealing investment opportunities may help unlock this constrained demand in established vacation markets.

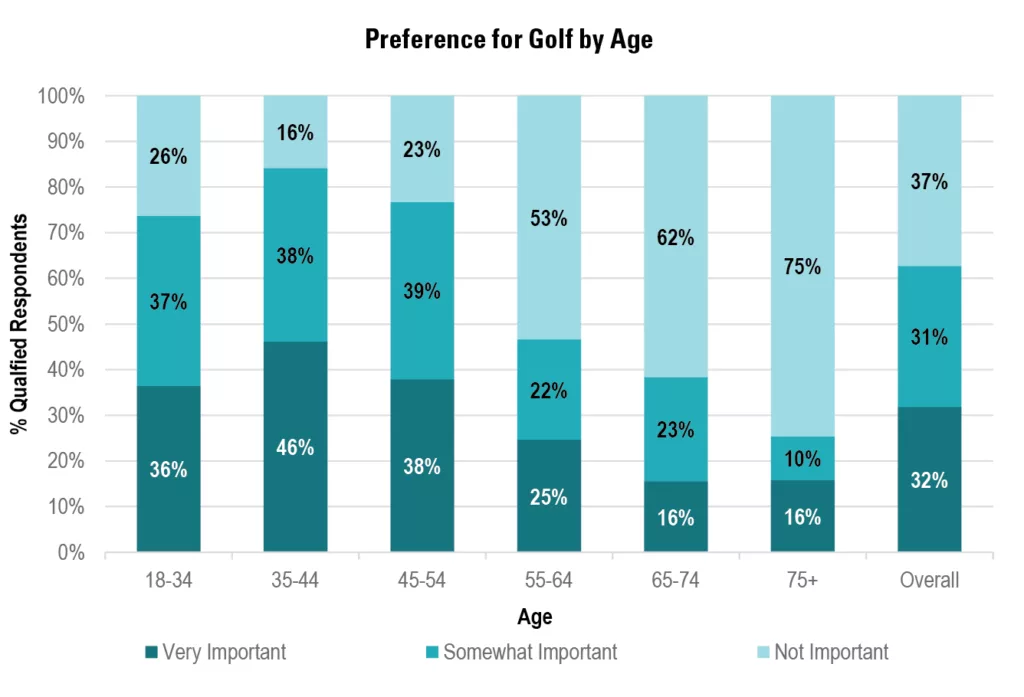

4. Amenities Drive Purchase Motivations, with a Resurgence of Golf

Amenities are a key value driver in vacation and investment home product, which directly influences design, programming, and pricing decisions. Developers and operators who anticipate evolving amenity priorities can create properties that resonate more deeply with target audiences, improving marketability as well as long-term absorption and price appreciation. Across age groups, access to shopping and dining outposts continues to dominate the amenity landscape, along with access to outdoor activities like swimming (particularly in beach locations), walking and biking trails, and other recreational amenities. Another top amenity sought out by potential buyers is access to golf. A noticeable trend in RCLCO’s 2025 survey was increased interest in golf among younger buyers (age 44 and under); 79% percent of younger buyers indicate golf was either “very” or “somewhat” important, compared to 63% of respondents overall. Developers are often faced with key decisions regarding whether to include a golf course in a resort community due to its high land consumption and operating costs. However, demonstrated interest among high-net worth buyers, combined with the opportunity to use the course as a recreational and aesthetic anchor, makes it a compelling selling point. Partnerships with nearby clubs or the integration of smaller-scale golf amenities (such as practice facilities, short courses, and simulators) can deliver a golf experience without requiring the level of investment commanded by a full 18-hole course.