November 1, 2024

Data Centers: Navigating Power Constraints and Skyrocketing Demand

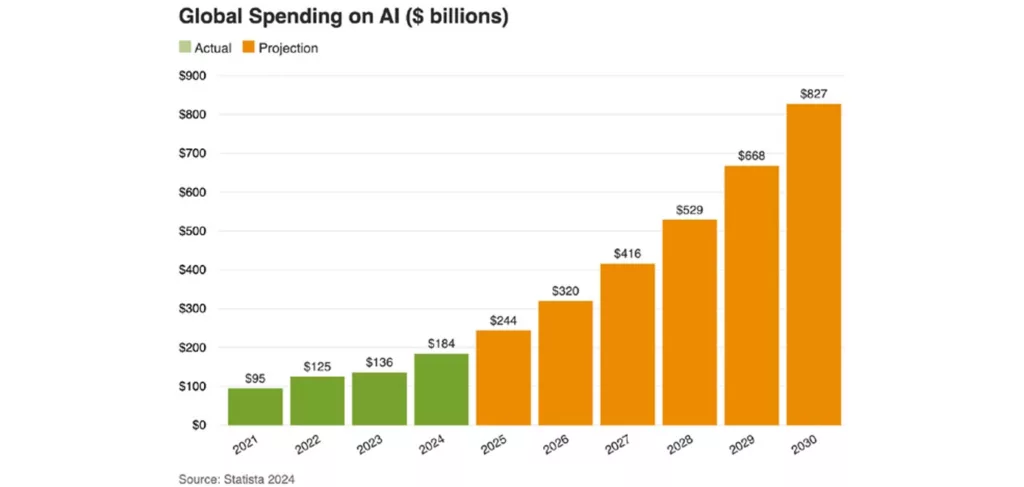

Data centers are a relatively new major property type with ties to both infrastructure and net-lease, and they are on a path to be one of the largest property types in the country over the next 10 years. Demand is being fueled by numerous drivers, including cloud storage, mobile data traffic, overall internet traffic, and artificial intelligence (AI), among other new and growing uses (e.g., autonomous vehicles). The surge in AI is notably driving a significant increase in the need for data centers and computing capacity.

While demand for data centers is skyrocketing, new supply is facing severe constraints mainly due to limits on electric power transmission capabilities. The mismatch between constrained supply and strong demand, which is likely to persist for the next five years or more, has resulted in virtually no vacant space in the major data center markets, rapidly rising rents, and super-charged profits for developers that can secure access to guaranteed power sources.

There are certainly downsides to the rapid expansion of data centers. The pressing need for electricity is causing utilities to prolong the use of coal and other carbon-intense power plants. New transmission lines are needed in many cases, with public opposition a risk. Data center equipment needs to be constantly cooled, often with water that is increasingly scarce in many parts of the country.

They tend to be noisy and visually unappealing, making them unsuitable as neighbors. Data center operators hope to re-open decommissioned nuclear power plants to secure long-term power, raising concerns about safety and spent fuel disposal. Further, certain counties with high concentrations of data centers (e.g., Loudoun County, Virginia) have begun to discuss legislation that would make new development more difficult, potentially even doing away with any by-right development of land into data centers and requiring discretionary approval.

All in all, the strong business case for data usage (AI is forecast to annually generate hundreds of billions in revenue) and the potential societal gains (e.g., greater productivity, lower fatalities due to autonomous vehicles) mean that data centers will likely continue to expand as fast as power sources can be procured for the next five to 10 years.

Data Center Typology

There are three primary types of data centers:

- Enterprise facilities are wholly built, maintained, operated, and managed by companies for the optimal operation of their own information technology equipment.

- Cloud or hyper-scale facilities are built to accommodate the scalable applications revolving around the cloud, big data, or distributed storage. They are typically single-tenant facilities and/or campuses. Increasingly large, hyper-scale tenants are using these facilities for AI purposes (e.g., large language model training, inferencing).

- Multitenant/colocation/network-dense facilities are built to accommodate multiple companies that lease space within the data center. Network-dense facilities allow users to interconnect to many different network service providers, enhancing the interconnectivity of the user to other facilities within a market and outside that market.

A very limited well-known group of hyper-scale tenants make up the bulk of current demand and are projecting continued and expanded capital spending. Unlike other real estate sectors, data center revenue is usually linked to power capacity (kilowatts per month) rather than the size of the building.

Top Markets

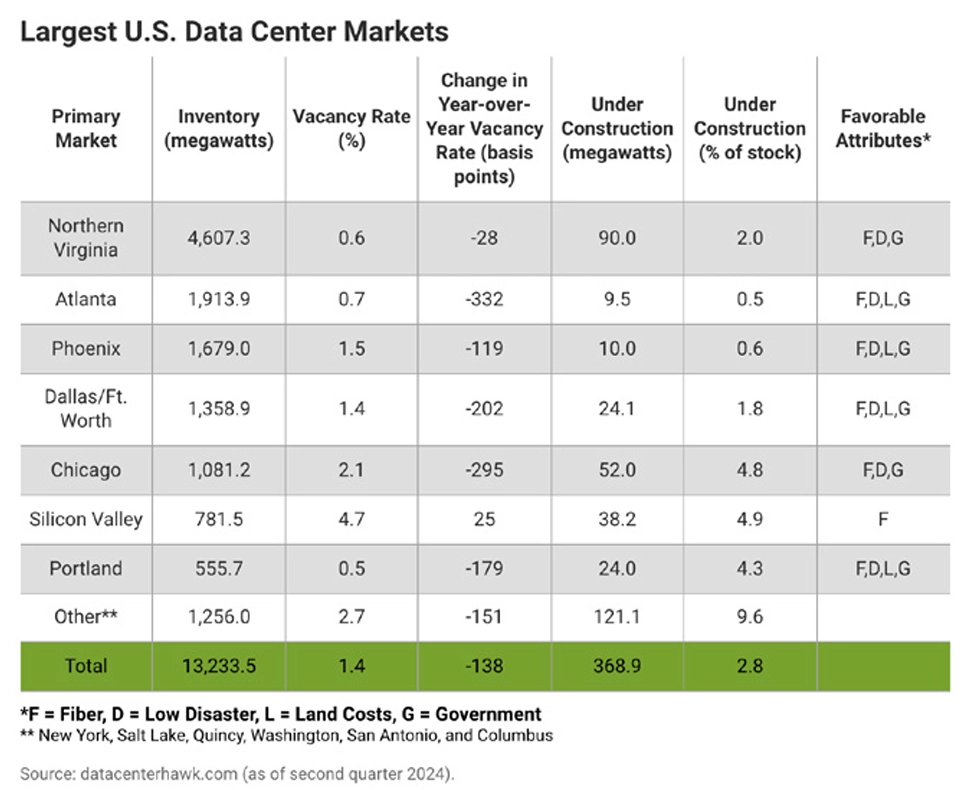

Data centers have historically clustered in areas with good connectivity to fiber and near major population centers. Northern Virginia is the leading global data center market mainly because it was one of the earliest locations of the internet ecosystem, having proximity to government and military-focused users, deep fiber optic connectivity, a relative availability of land, and a low risk of natural disasters. Today, approximately 70 percent of world internet traffic passes through data centers in the Northern Virginia region. The figure outlines the primary reasons for the extremely low vacancy rates and very limited supply pipeline, particularly in the largest markets. The primary markets vary in terms of their relative attractiveness. The key qualities of an attractive data center market include the following:

- Fiber connectivity

- Proximity to a major population base

- Government support, such as tax incentives

- Power availability and cost

- Low risk of disaster or disruption

- Low land costs

Risks

In addition to the specialized skills needed to develop and operate data centers, additional risks include the following:

- Obsolescence due to advancements in technology is always a possibility. For example, one interviewee suggested that “there is a 25 percent chance of commercially viable and disruptive quantum computing breakthroughs in the next decade.”

- Economies of scale could reach a level such that hyper-scalers find it more cost effective to own their own facilities. The current risk is tenant concentration.

- Capital expenditures can be quite high depending on the level of services provided, although most such expenses are the responsibility of the tenant. Overall the burden of capital expenditures for this property type is generally less than that of other types.

- Electric power for new developments will be constrained for the foreseeable future. Northern Virginia and Silicon Valley are two of the most constrained, but many other top tier markets are experiencing power constraints that are leading to wait times of five or more years.

- Environmental impacts such as greenhouse gas emissions and water usage will grow rapidly as the sector expands. The industry is exploring clean energy (including nuclear), fuel cell storage, and recycling data center equipment, but greater local restrictions are possible.

- Small markets will come into play as data centers increasingly locate near large power sources- some of which are outside of major population centers. For example, a large software firm has signed an agreement to purchase 835 megawatts (MW) of power for 20 years at the to-be-reopened Three Mile Island nuclear power plant, to meet its carbon-free energy goals at its nearby data centers. The power plant is in Harrisburg, Pennsylvania, a metro area with 570,000 people. Other small markets are similarly being explored due to the availability of power.

Capital Markets

The capital requirements for future data centers are likely to be immense. Moody’s estimates that global data center capacity will double over the next five years. Considering the addition of 15 MW of new capacity at a rate of $12.5 million per MW, the cost of this growth will amount to $188 billion, while their market value is estimated at approximately $281 billion, both in present-day dollars. By comparison, the two publicly traded data center REITs have a total estimated value of $190 billion, as of early October 2024.

Fortunately, institutional investors have expressed great interest in data centers. CBRE reports that 97 percent of investors plan to allocate more funding to data centers in 2024. REITs will continue to be a major source of capital, particularly with institutional investors as capital partners. Data centers also work well for private investors: Development is highly profitable compared to other forms of real estate and long leases with credit tenants support high loan to value ratios.

In summary, data centers are currently highly profitable for both tenants and developers/owners. Power procurement difficulties will keep supply below demand for the near- to mid-term, ensuring that sites with power access will lease up quickly at high rates. Of course, if supply constraints were to materially ease, new construction would spike and rental rates and returns would likely decline. The outcome is not likely anytime soon.