October 27, 2025

Originally published via PREA

US pension funds have been investing in real estate for decades with mixed results to date. Numerous studies have shown that, on average, pension funds have historically underperformed their benchmarks net of investment costs, while taking greater risk than the underlying benchmarks. In our view, the main reasons for underperformance are straightforward:

- Overreliance on closed-end, non-core, commingled funds with mediocre performance and high fee loads

- Property-type allocations based on historical investment patterns (e.g., ODCE) that don’t reflect future demand and performance trends

- Lack of control over major investment decisions such as pacing, risk, leverage, and dispositions

Following up on past PREA Quarterly Points of View,[1] this article presents strategies that, if implemented, we believe will help institutional investors achieve better outcomes from their real estate portfolios

First, Some Good News

Despite overall long-term underperformance, some real estate investment strategies have been successful over the past several decades and should continue to outperform going forward.

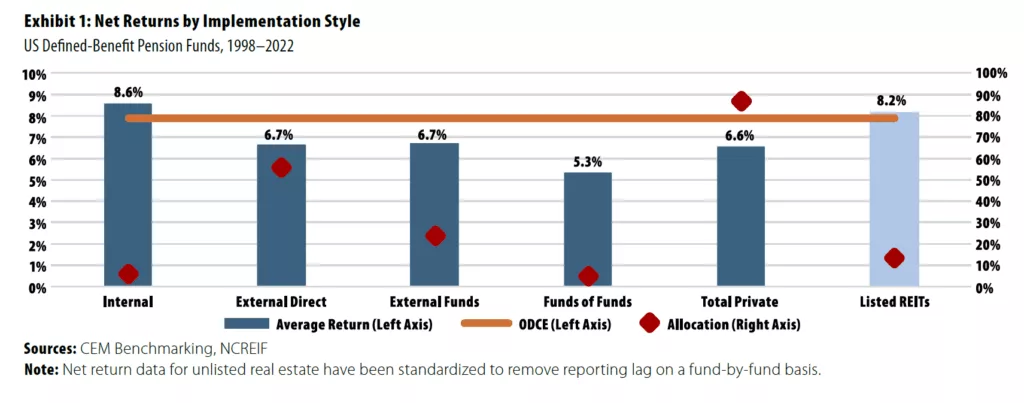

First, internally managed real estate investments have outperformed the ODCE (and closed-end funds) over the past 25 years. As shown in Exhibit 1, self-managed investments outperformed the ODCE by 80 basis points (bps) per annum from 1998 to 2022.[2] Direct investing usually results in lower fees and costs, better allocations, active portfolio management, and in some cases, greater leverage. Although internal management requires a sizable staff and therefore makes sense only for larger funds or real estate allocations, all funds can benefit from some of the strategies and techniques larger investors use.

Second, publicly listed REITs have also outperformed the ODCE over most time frames because of both greater exposure to better-performing property sectors (particularly so-called niche sectors) and lower fees and investment costs and slightly higher leverage. Average investment costs for active REIT portfolios were 49 bps (per annum) versus 117 bps for private vehicles.

Finally, larger pension funds have on average outperformed smaller funds. Funds with more than $10 billion in total assets under management have consistently outperformed smaller funds, while taking on less active risk.[3] The biggest advantage of scale is the ability to invest in private assets (including real estate) internally, resulting in lower asset management costs. However, while scale can be an advantage, there are many things that small and medium-size investors can do to improve performance, as discussed below

A Better Approach

Still, the overall performance picture is not good. As discussed above, most pension funds do not meet their real estate benchmarks over time. The ODCE (or ODCE plus a premium) is the most used benchmark among US institutional investors, but as a core index, it does not reflect the actual risk level of most plans. CEM reports that US defined-benefit pension funds allocated 32% to non-core private vehicles in 2021,[4] the latest year available.

Looking ahead, IREI reports that US investors plan to target 44% of their real estate portfolios to value-added and opportunistic strategies in 2025,[5] indicating that investors are taking on extra risk in vehicles that have historically not met or exceeded core benchmark returns. Based on our observations working with a range of investors, improved performance is most likely achieved when adhering to the following principles:

- Invest in property sectors and geographies that are most likely to benefit from observable demographic, economic, and technological demand and supply trends.

- Be “cycle aware” when committing capital for long periods of time.

- Select partners that pursue a disciplined, strategic approach to investing alongside strong operational skills to drive net operating income growth.

- Invest through structures (e.g., joint ventures, separately managed accounts, and real estate operating companies [REOCs]) that enable active management input by limited partners (LPs) and mitigate the potential misalignment between general partners (GPs) and LPs.

- When investing in funds, favor operators over allocators and select funds/managers with LP-friendly fee structures and governance, clear strategies, and coinvestment opportunities, if applicable.

- Proactively review asset and portfolio optimization and recycling of capital.

Investing according to these principles requires organizing internal and external resources to facilitate portfolio oversight and capital deployment. In our view, many plan sponsors have historically underinvested in these “must have” resources, and we offer suggestions for how they can be accessed despite scale and governance constraints.

Property Type and Geographic Selection

Optimal portfolio composition (property type and markets) changes materially over time as a result of shifts in economic growth as well as property and capital market drivers. US investors have been slow to shift property-type and geographic allocations as the relative attractiveness shifts and new property types enter the potential universe. A good example was the continued prevalence of the office sector, which was more than 40% of the ODCE as recently as 2015. Most investors were slow to notice deteriorating market fundamentals (higher structural vacancy and capital requirements, even prior to the COVID-19 pandemic) and maintained high exposure to the sector.

Some things to consider in crafting portfolios:

- Invest in high-conviction sectors irrespective of the index. Investors that attempt to mimic benchmark allocations tend to underperform, as property performance shifts with changing demand and supply trends. We recommend overweighting property types with strong long-term demand drivers, irrespective of the index.

- Evaluate evolving demand drivers, technological change, and market fundamentals for potential future opportunities and disruption. In recent decades, e-commerce, remote work, and the fast growth of Sunbelt markets have had big impacts on performance. Looking ahead, artificial intelligence, autonomous vehicles, and industrial reshoring are just a few of the potential macro shifts that will likely influence real estate demand drivers and returns.

- Alternative or niche property types are becoming an increasing share of institutional portfolios. Many of these property types have strong demand drivers (e.g., data centers, seniors housing, and health-care real estate) and are less impacted by recessions.

- Although there are clear differences in growth trends among US regions and metro areas, supply constraints in older established markets can frequently offset the effects of demand growth in new markets (often in the Sunbelt). Differences in returns by metropolitan statistical area are therefore more muted than differences in returns based on property types.

Investment Timing

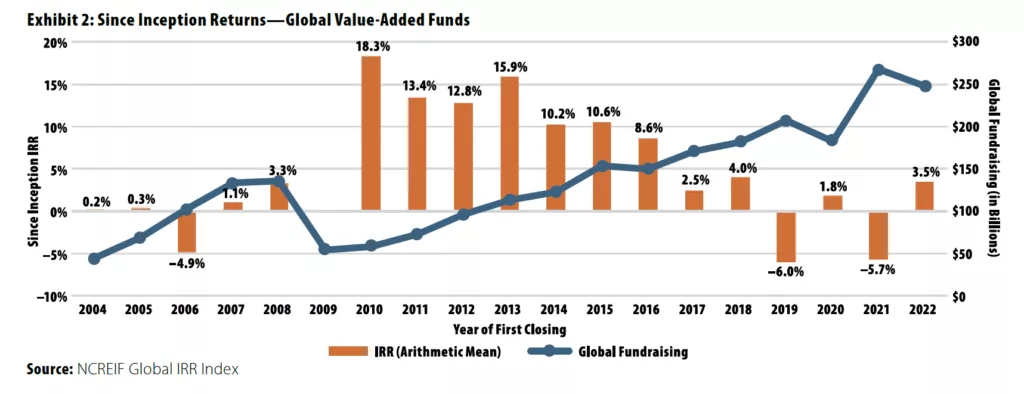

Many investors proclaim not to be market timers and aim to achieve exposure to most or all vintage years. We sympathize with this approach but would argue that real estate moves in long cycles that can inform when to overweight or underweight the asset class and varying strategies. As shown in Exhibit 2, fund performance varies widely by vintage years, with the best performance coming after steep downturns, such as the global financial crisis. There is also a noticeable pattern of low IRR vintage years occurrence when fundraising volumes are high.

Given this, here are some timing strategies to consider:

- Utilize different strategies based on property type, geographies, and cycle positioning (Exhibit 3).

- Sell at opportune times to maximize returns. Capital structures should allow for both short and long holds, depending on market conditions.

- Contrarian investing is crucial but difficult to execute. The best vintage years are after corrections, often accompanied by limited fund distributions and denominator effects. However, the worst vintage years are usually when values, debt availability, and transaction volumes are at their peak. Investors should be very cautious during those periods.

Structure and Partner Selection

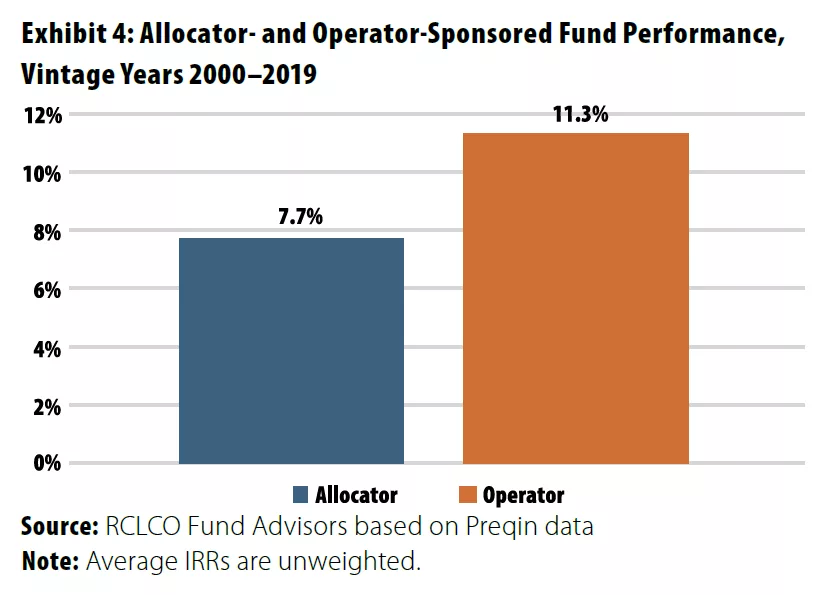

US real estate investment management is dominated by managers whose main areas of expertise are allocation and capital markets rather than operations; 18 of the largest 20 US investment managers are capital allocators rather than operators.[6] Allocators typically leverage operational partners to source and operate property-level investments, resulting in two layers of fees, dragging down net investment performance.

Although they tend to be smaller, funds sponsored by operators have outperformed those sponsored by allocators by an average of 360 bps per annum since 2000 (Exhibit 4). Operator-sponsored funds are also more likely to be in the top quartile (by vintage) than allocator-led funds, indicating that fee-mitigation and property-specific expertise is generally more valuable than property-type selection.

Preferred Structures

US real estate capital markets offer a range of investment approaches, including public securities (REITs), open- and closed-end commingled funds, joint ventures, separate accounts, operating companies, and direct ownership.

Over time, we have observed that the segments of institutional investors’ portfolios offering greater control—such as joint ventures, separate accounts, and REOCs—have consistently outperformed those with limited control, such as commingled funds.

For small and medium-size investors, achieving control is more difficult, particularly if staff and resources are limited. Fund selection is also more difficult, particularly considering that most funds do not generate alpha. One alternative strategy is to focus on low-fee and liquid products, such as REITs and open-end funds. Higher returns can also be generated by using internal leverage on core investments (albeit not without increased volatility).

Asset and Portfolio Management

Active portfolio management requires diligent decision-making on both the acquisitions and dispositions. Managers and investors are typically careful about buying decisions but less rigorous in selling assets. This is not unique to real estate. A study on equities trading among institutional investment managers found that managers’ buying decisions consistently outperformed a random buy/sell benchmark, while selling decisions consistently underperformed.[7]

Managers often hold on to underperforming assets hoping that the property or market will improve, with asset management fees a meaningful incentive to hold.However, in many cases a quick sale and redeployment of proceeds will outperform a long hold. In a similar way, selling nonperforming funds on the secondary market (despite sizable liquidity discounts) and reinvesting in current opportunities can also be accretive in some cases.

Operational excellence occurs when managers/operators place as much (or more) emphasis on asset management and dispositions as they do on acquisitions. Great operators continuously improve processes in acquisitions, construction, property management, financing, etc., and collect and analyze both third-party and internal data.

This mind-set and skill base will become increasingly important as artificial intelligence improves as an analytical resource.

Resources

The vast majority of institutional investors have limited internal resources relative to the size of their portfolios and must use a combination of managers, advisors/consultants, and service providers to effectively manage investments.

The specific allocation of work and decision-making among internal staff, managers, advisors/consultants, and service providers is driven by governance, culture, and organizational expertise and capacity. Often, institutional investors outsource too many decisions and spend too much on investment managers, which research demonstrates does not deliver acceptable returns,[8] and too little on what actually generates alpha: internal teams[9] or outsourced or contracted staffing if in-house hiring is not possible.

In addition to sufficient staffing, investors need independent, relevant, and timely portfolio information to enable more-effective decision-making. Investors receive manager quarterly reports and standard books of record long after the information would be relevant. Fund-level information typically aggregates risk factors, property types, and geographies, limiting effective decision-making. Investors would benefit from their own third-party data sources and valuation resources that more effectively track market and portfolio information.

Ironically, many investors are far more constrained and cost/fee sensitive relative to internal hires or directly outsourced resources than they are in making commitments to managers charging meaningfully higher fees. Enhancing internal capabilities often requires changes in governance and procurement (or requires outsourced or contracted staffing) but would likely result in overall cost savings and better performance.

Summary

The long-term structural decline in interest and cap rates—which coincidentally or not overlaps with the growth of real estate in institutional portfolios—boosted returns and potentially covered up the sources of underperformance we’ve outlined here. With most observers anticipating a different, higher interest rate regime going forward, delivering acceptable, let alone superior, returns will require all participants to bring their A game. We observe that outperformance is achieved via the following:

- Management of property-sector risk and vintage exposure

- Investment supported by high-conviction demand drivers

- Management of supply risk (geographically and qualitatively)

- Alignment with best-in-class operating partners to mitigate risk and create value at the asset and portfolio level

- Utilization of LP-friendly structures that work within the LP’s resource constraints, which reduces misalignment and fee drag, and proactive management of investments throughout cycles to keep the portfolio relevant and performing

None of these steps are easy, but moving to adopt as many of them as possible can move the needle on investment returns and risk.

References

[1] William Maher, Taylor Mammen, and Ben Maslan, “Private Equity Real Estate Fees: A Modest Proposal,” PREA Quarterly, Fall 2024. William Maher and Taylor Mammen, “Academics Question the Value of Private Real Estate Funds: What’s an Investor to Do?” PREA Quarterly, Fall 2023.

[2] Pouya Behmaram, Chris Flynn, and Maaike van Bragt, “Asset Allocation and Fund Performance of Defined Benefit Pension Funds in the United States, 1998–2022,” CEM Benchmarking, November 2024.

[3] Alexander D. Beath, et al., “A Case for Scale: How the World’s Largest Institutional Investors Leverage Scale to Deliver Real Outperformance,” CEM Benchmarking, February 2022.

[4] Behmaram, “Asset Allocation.”

[5] 2025 Institutional Real Estate Investor Trends, IREI.

[6] Recognizing the value of operational resources, some allocators are acquiring or internally developing operating platforms.

[7] Klakow Akepanidtaworn, et al., “Selling Fast and Buying Slow: Heuristics and Trading Performance of Institutional Investors,” working paper, July 2021.

[8] Timothy J. Riddiough and Da Li, “Persistently Poor Performance in Private Equity Real Estate,” SSRN, May 3, 2023.

[9] Behmaram, “Asset Allocation.”

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.