A Lighthearted Look at Which of the Quarterfinal Teams’ Base Camps Might be the Best Market for Real Estate Investment

July 9, 2026

By Evan Farrar, Senior Associate; Reilly Eagan, Associate

One of the more unexpected storylines of this World Cup has unfolded far from the stadiums. When national teams arrived at their base camps to prepare for the tournament, media attention followed them, and cities that rarely surface in international sports coverage suddenly found themselves under the lights.

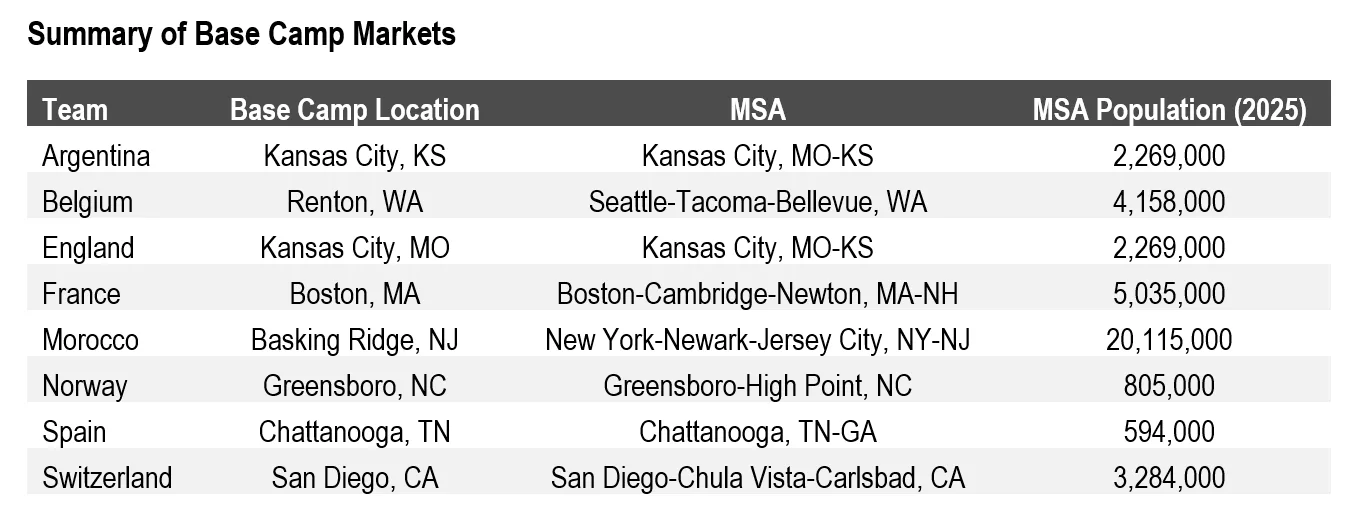

Where the teams chose to settle varied widely. A few teams gravitated toward the suburbs of major gateway markets, setting up outside New York and Seattle. Others made their way to smaller Southeastern cities like Chattanooga and Greensboro, drawn by quieter surroundings and a distinct local character. What followed produced some of the tournament’s best off-pitch moments. Communities adopted visiting squads as their own, open training sessions became local events, and players found themselves cheered on by a new hometown crowd thousands of miles from home.

Memorable as these moments are, they raise the obvious question. What if we treated the base camp map as a bracket, one where each team is represented by its chosen base camp, and cities advanced according to the strength of their conditions for real estate investment rather than the strength of their squads? We ran that exercise, comparing base camps across three rounds and judging each on a different criterion.

The quarterfinals turn on growth potential, measuring which markets are attracting new residents and expanding their economies. The semifinals raise the bar to pricing and liquidity, asking which cities offer the depth and availability of capital that mitigates investment risk. The final comes down to supply-demand balance and regulatory risk, the factors that shape whether a market can produce outsized NOI growth.

As the quarterfinals kick off this afternoon, here’s how we think the real estate bracket might play out. Consider it our tongue-in-cheek tribute to the tournament.

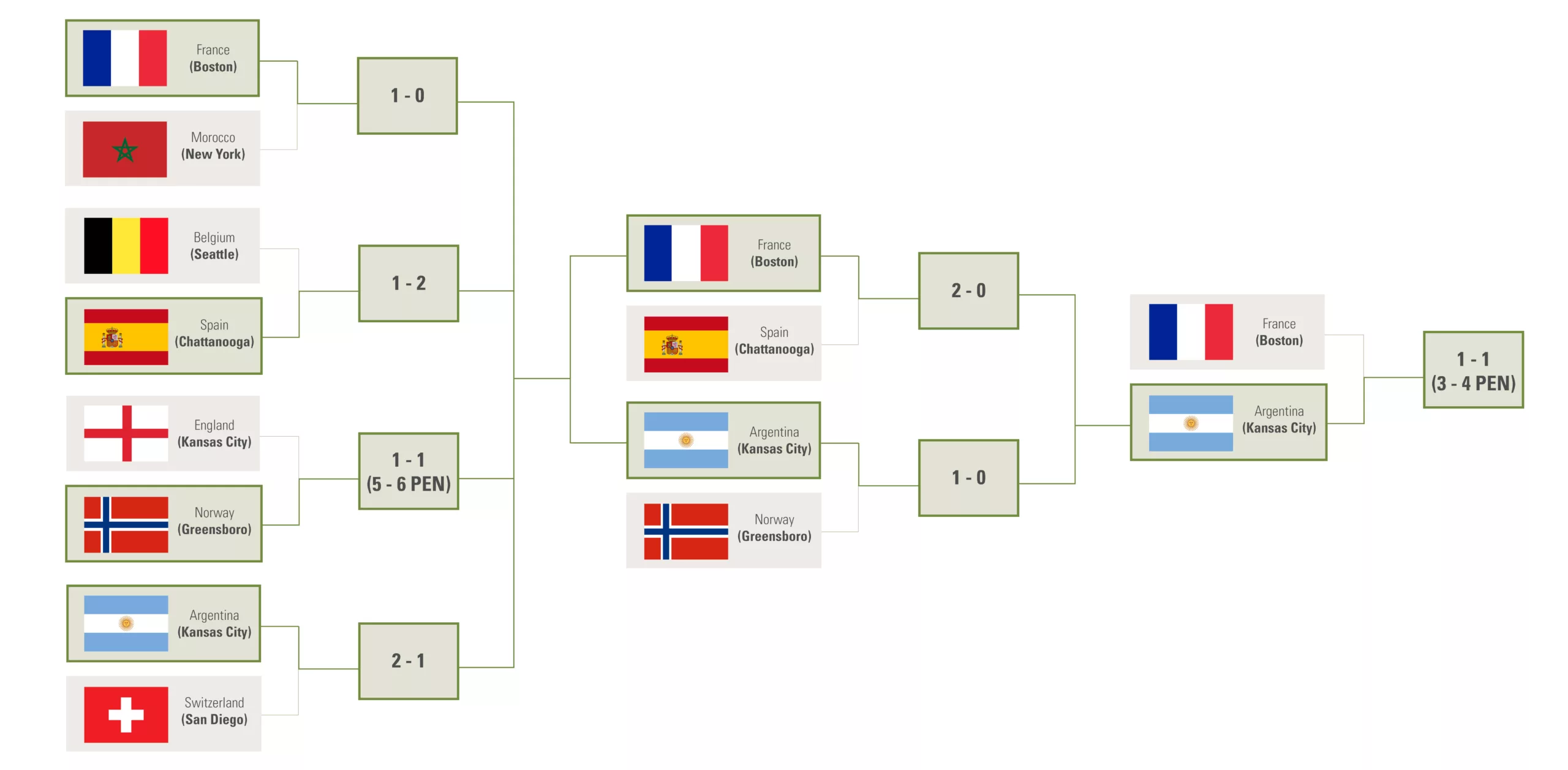

The Quarterfinals: Growth Fundamentals

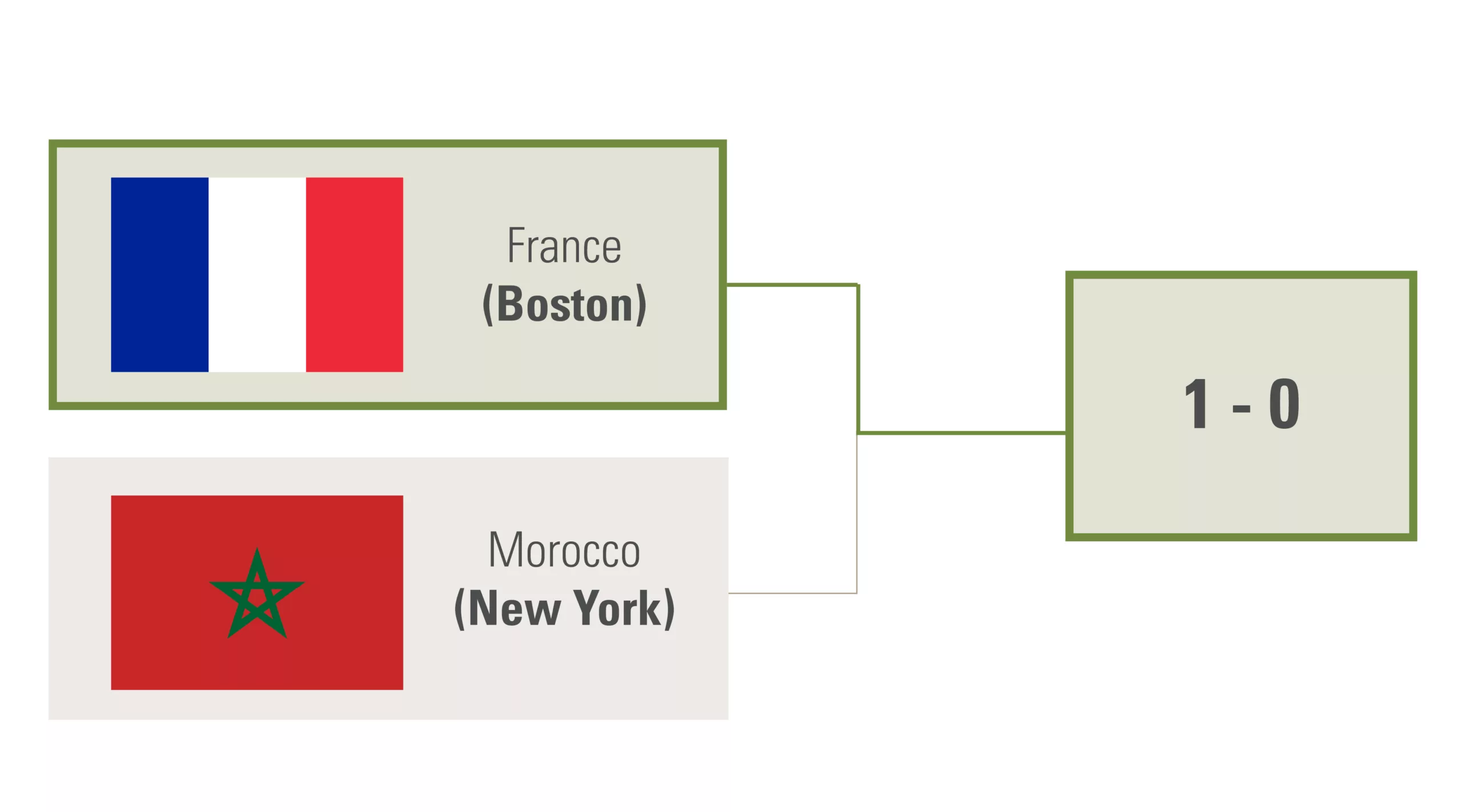

Boston finds the net late in the second half, fueled by modest post-pandemic population growth, while New York has a tougher time defending its position as steady out-migration presents complicated headwinds. Boston’s deep bench of highly-educated talent maintains possession, turning a low-scoring match into a controlled win.

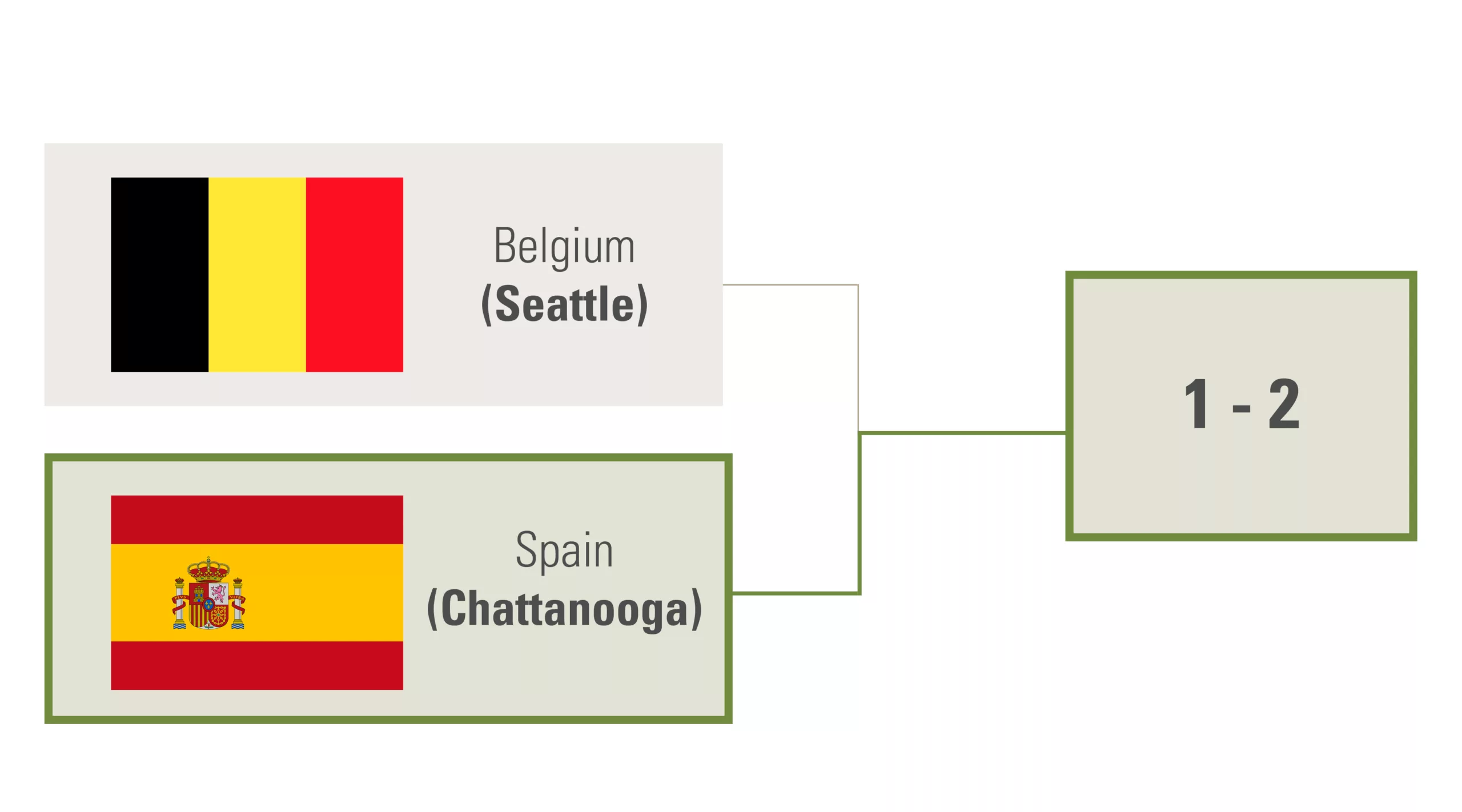

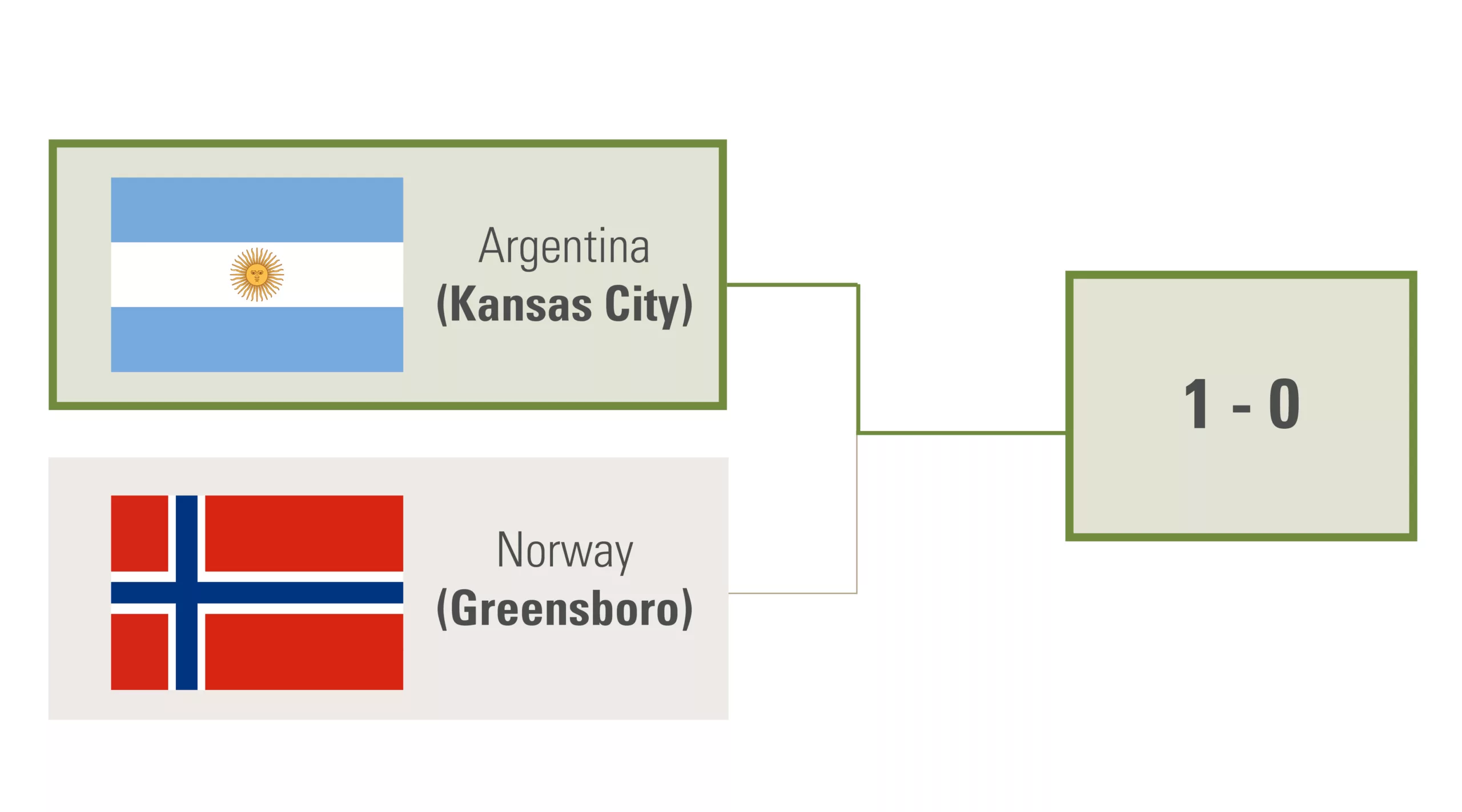

Chattanooga comes out pressing, riding a wave of in-migration and cost-of-living tailwinds to an early lead. Seattle attempts a spirited second-half comeback on the strength of its tech engine, but a slower job expansion leave it just one goal behind at the final whistle.

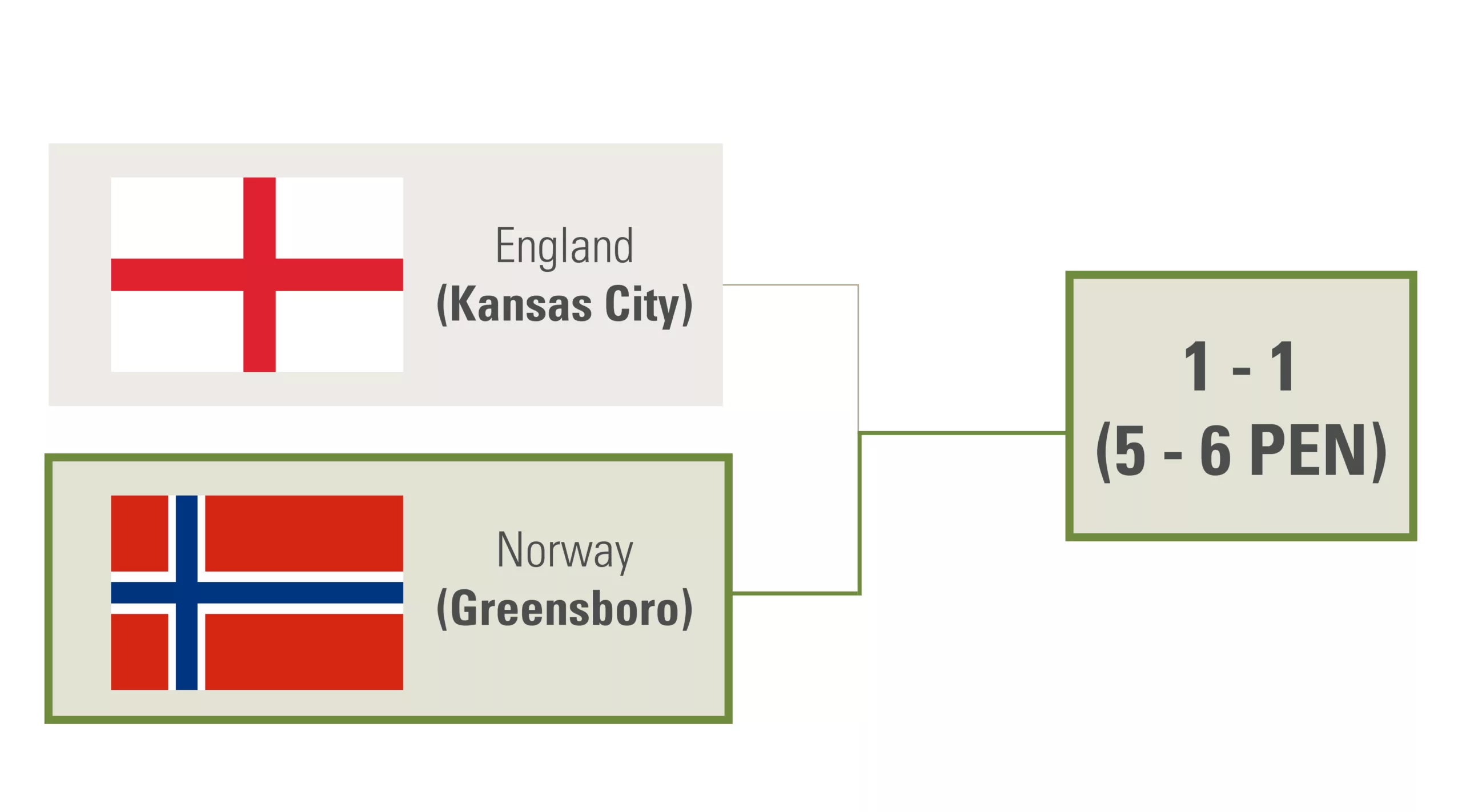

A genuine end-to-end battle that neither side could settle in regulation or extra time, finishing level at 1-1. It comes down to penalties, and after both teams trade blows deep into the shootout, Greensboro converts to win 6-5, with the Triad’s stronger relative domestic in-migration burying the decisive shot.

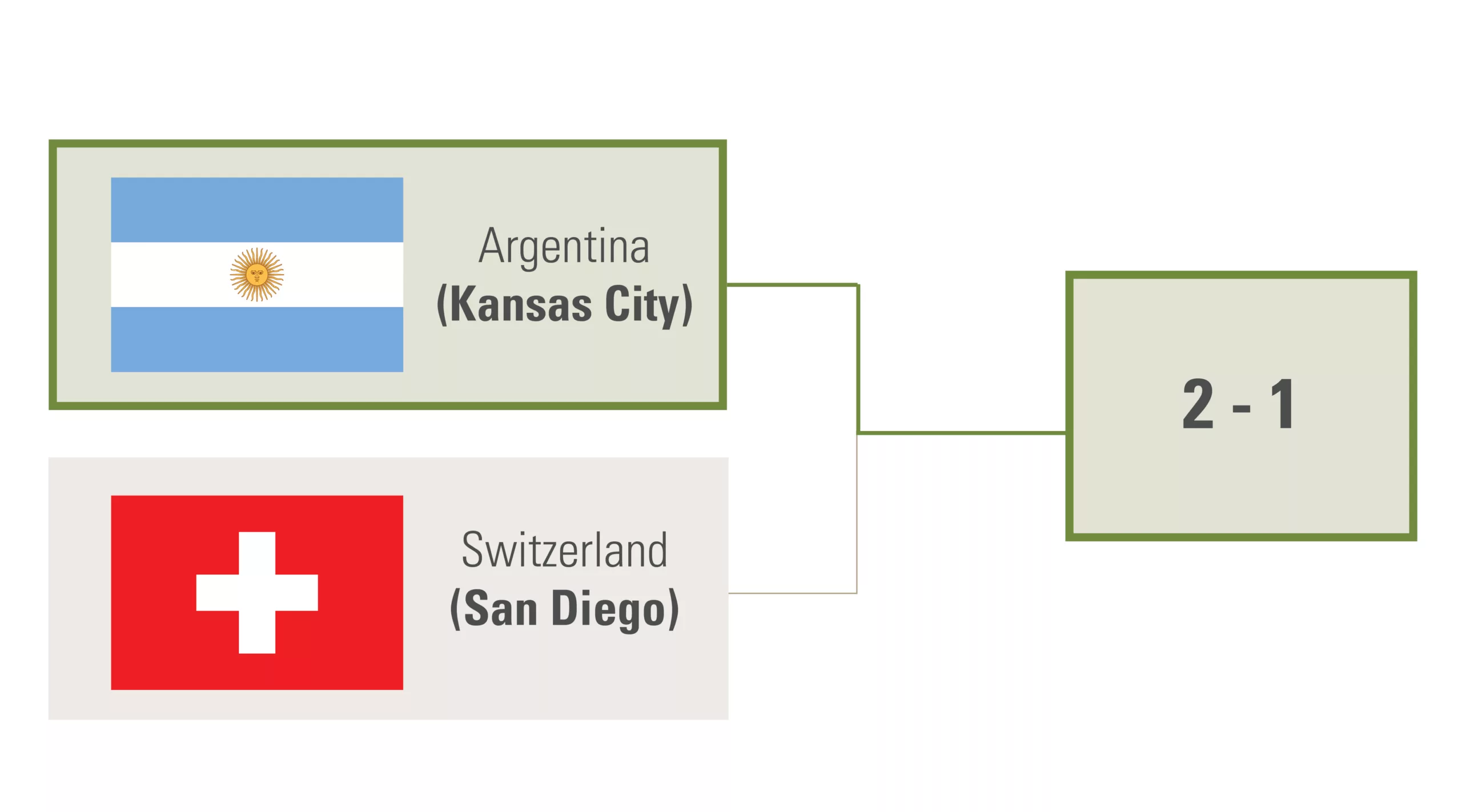

Kansas City turns in a commanding performance, its affordability and below-the-radar employment growth proving too much for a San Diego side weighed down by high costs and constrained supply. San Diego flashes quality on the counter, but Kansas City’s Midwestern engine can’t be overcome.

The Semifinals: Pricing and Liquidity

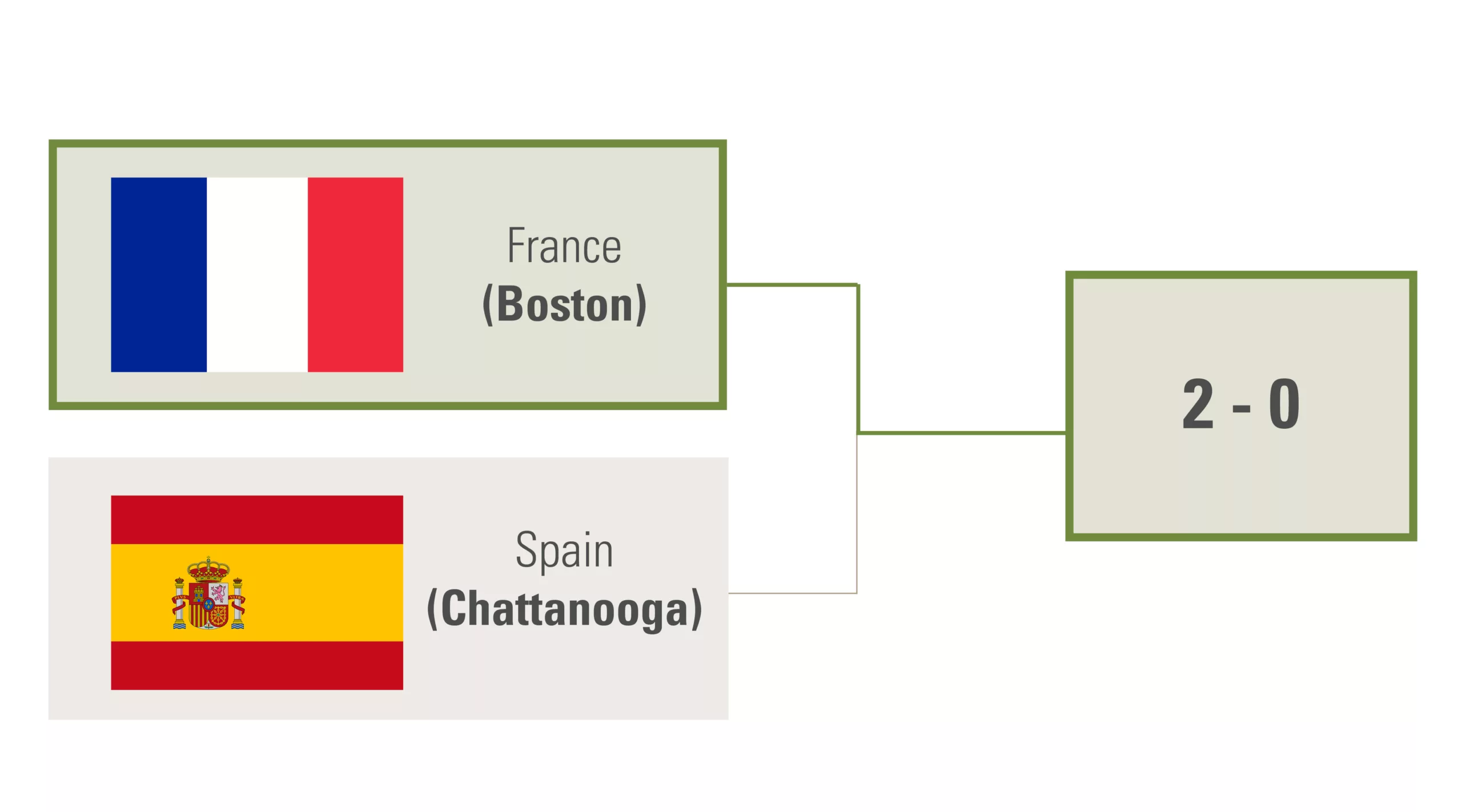

The match turns on liquidity, and Boston simply has too much depth on the ball as an established, heavily traded market. Chattanooga’s Cinderella run meets a firmer defense here; as a smaller, thinner market, it struggles to generate the transaction velocity needed to break through.

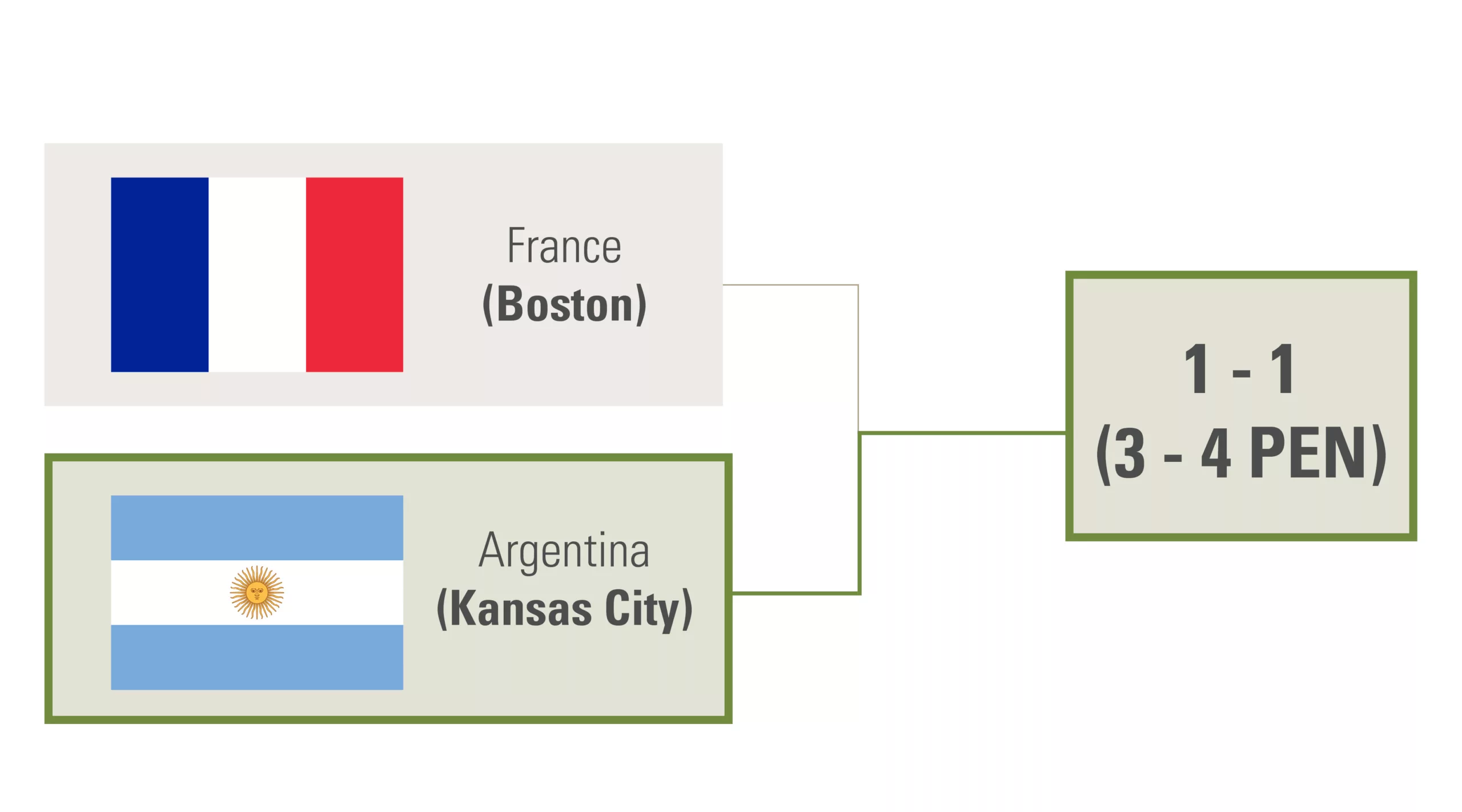

Greensboro’s growth carried it far, but the semifinal is decided on pricing, and that’s where Kansas City’s comparatively strong values win out; Greensboro also can’t match Kansas City’s multifamily and office transaction volume. Greensboro battles hard, but Kansas City grinds out a narrow win to reach the final.

The Final: Supply-Demand Balance and Regulatory Risk

In a final decided on supply and demand fundamentals, Kansas City pulls off a stunning upset—its elastic, builder- and owner-friendly environment producing moderate but consistent value growth and strong development opportunity. Boston takes an early lead on the strength of its fundamentals, with deep demand and real barriers to entry, but those same supply constraints and regulatory hurdles make it expensive, difficult to underwrite income expansion, and very hard for development to pencil. In a penalty kick showdown, a contrarian midwestern bet pays off.

Kansas City takes the bracket, defeating Boston in the final. That final matchup feels fitting to us, and while it may be unexpected, Kansas City’s win is emblematic of a broader shift we’re observing. A large but still-emerging Midwestern metro squaring off against an established coastal gateway mirrors what many of our gateway-based clients are grappling with today: high costs, constrained growth, and selective capital. Capital that once clustered almost exclusively in a handful of established markets is increasingly interested in following the fundamentals to a wider range of places, seeing careful, deliberate geographic diversification as a strength. The same emerging metros that drew national teams and camera crews this summer are turning up more often in those conversations.

While this is not meant to be investment advice, we hope it does reflect RCLCO’s observation that market selection frameworks are often too rigid and that it pays to try a contrarian approach from time to time. The lens we see the world through—or, in this case, the World Cup—is real estate, and every so often it’s worth having a little fun with it!

If you enjoyed the above and want to learn more about RCLCO’s sports-adjacent work, click here to learn more:

Disclaimer: This article has been prepared solely for informational purposes and is not to be construed as investment advice or an offer or a solicitation for the purchase or sale of any financial instrument, property, or investment. It is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein reflects the views of the author(s) at the time the article was prepared and will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing or changes occurring after the date the article was prepared.