Headlines from this article:

- The RCLCO Current Real Estate Market Sentiment Index (RMI)[1], which measures sentiment on a 100-point scale, has increased 57.5 points over the past six months, from 31.6 at YE 2020 to 89.1 at Mid-2021, returning to a high not seen since Mid-2015.

- Respondents predict that real estate market conditions will remain largely consistent in the near future, with the RMI anticipated to drop only 7.8 points to 81.3 over the next 12 months. This is still well above the long term (since 2011) average of 68.8.

- Approximately three quarters of survey respondents (75%) believe real estate conditions will be moderately or significantly better in the next 12 months.

- 7 out of 10 respondents indicate that rising construction costs are having a significant impact on the real estate market. Going forward, higher costs are likely to temper somewhat, though still remain a factor in 12 months.

- Respondents indicate that most product types have moved from contractionary phases to expansionary phases in the real estate cycle since the YE 2020 survey. Retail and office remain at the bottom of the cycle, and hospitality has reached early expansion. However, all three sectors are expected to return to Early Recovery within the next 12 months.

- Looking ahead a year, a majority of respondents expect interest rates to rise, capital flows to increase to real estate, and homeownership rates to rise. However, there was less consensus over the expected performance of cap rates over the next 12 months.

RCLCO’s Real Estate Market Sentiment Survey has tracked confidence in U.S. real estate market conditions for the past 10 years. The overall index took a dramatic dive in Mid-2020 due to the speed and intensity of the economic downturn sparked by COVID-19, hitting its lowest level in the history of the series (9.2). The prior survey at YE 2020 showed the beginning signs of recovery but overall sentiment was still below the long term average. The Mid-2021 result reflects strong optimism as vaccination rates approach herd immunity levels, business restrictions have been lifted, and a drop in cases nationally spurs the economy and real estate markets toward recovery.

Overall Sentiment Has Quickly Rebounded from Historic Lows in Mid-2020 to an Optimistic Level On-Par with 2015 Sentiment Levels

Sentiment about the health of the economy and real estate markets was overwhelmingly positive in Mid-2021, increasing dramatically from COVID-19 downturn lows recorded in 2020. The precipitous drop in 2020 reflected the disarray of the markets and economy in reaction to the global pandemic. Since the end of 2020, the RMI index increased to 89.1, consistent with sentiment levels in 2015, and close to the highest levels ever seen. The strong and quick rebound is partially the result of the robust housing market over the past year; as households spent more time at home and therefore prioritized spending on their place of residence. The downturn’s uneven impact left many middle-income and affluent households relatively unscathed, while those in lower paying service-sector industries bore the brunt of the financial hardship. This left many higher income households (who are often the target of new real estate developments) in a position to purchase, rent, or invest.

The high current index level portrays a sense of optimism that surpasses the also-strong YE 2020 predicted RMI of 81.3, which is typically indicative of strong market conditions. The forward outlook indicates that the market index is likely to stay at a high level, though dropping slightly over the next 12 months, perhaps a reflection of fading stimulus spending.

RCLCO National Real Estate Market Index

Source: RCLCO

The high current index level portrays a sense of optimism that surpasses the also-strong YE 2020 predicted RMI of 81.3, which is typically indicative of strong market conditions. The forward outlook indicates that the market index is likely to stay at a high level, though dropping slightly over the next 12 months, perhaps a reflection of fading stimulus spending.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

The majority (88%) of respondents indicated that national real estate conditions were moderately or significantly better when compared with one year ago. A meaningful 50% of respondents predicted that real estate market conditions are significantly better than last year. This is a marked improvement from the nearly two-thirds of respondents who claimed worsened conditions at YE 2020, and signals that the market is well on the way to recovery.

The outlook for the upcoming year is also bullish. Approximately 75% of respondents predicted that national real estate market conditions would be “moderately” or “significantly” better in the next year. The remainder of the survey respondents were equally split between unchanged or worse conditions.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Construction Costs Could Cause Market Headwinds

There is a clear consensus that increased construction costs is having an impact on the real estate industry, presumably a negative one. 7 out of 10 respondents (70%) indicated that rising construction costs are having a significant impact on the real estate market where they are active, with another 24% indicating a moderate impact, and 4% indicating a slight impact. It should be noted that the survey was conducted close to the recent high point of lumber prices, which have traded down in recent weeks. Still, construction cost pressures are widespread, and this is an important issue to watch over the rest of the year.

Construction Cost Impact on Real Estate Markets Today

Source: RCLCO

Encouragingly, when asked to look 12 months out, the concerns over construction costs are less significant, with only 36% believing construction costs will continue to have a significant impact, with 61% predicting that the impact would be moderate or slight.

Construction Cost Impact on Real Estate Markets in 12 Months

Source: RCLCO

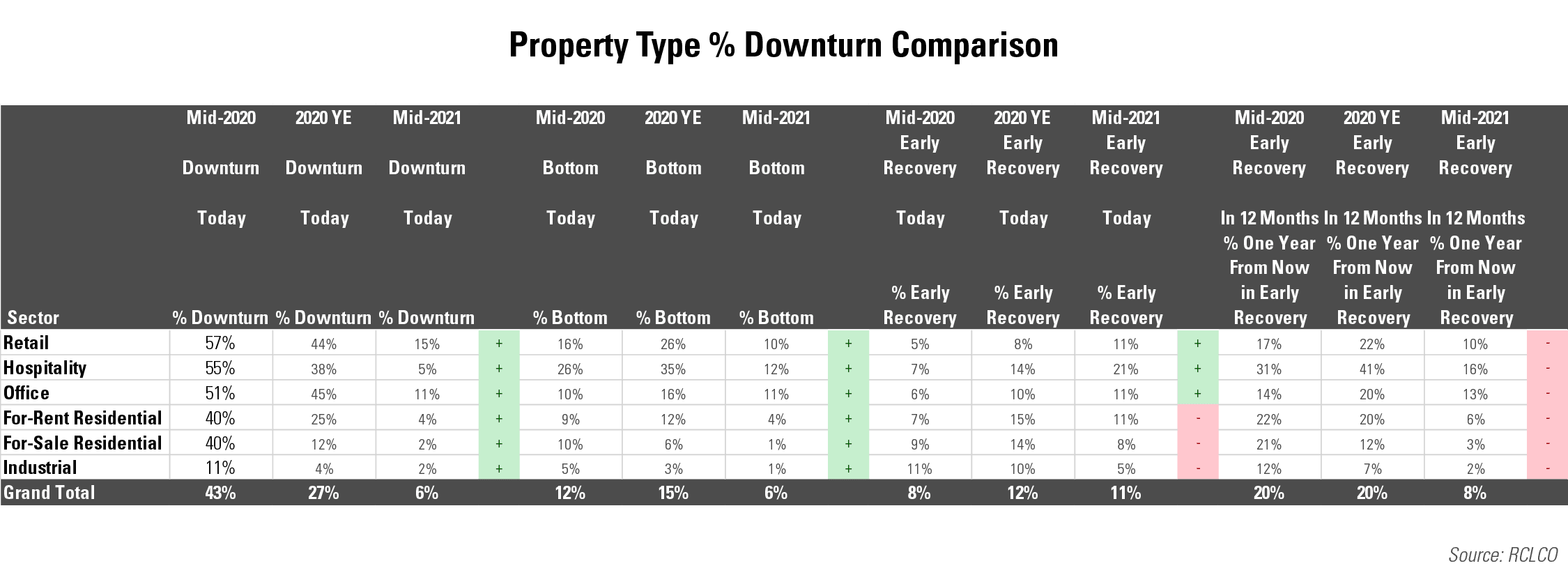

Fewer Product Types in Downturn over the Past Six Months

RCLCO’s Real Estate Market Sentiment Survey captures a snapshot of where respondents thought each major real estate sector was on the real estate cycle, the downturn-related stages are detailed in the chart above and the full cycle is shown below. Consistent with the broad recovery of the overall market, respondents told us that only 6% of the overall real estate market was in a downturn by Mid-2021. This is a sharp improvement from 43% and 27% that was registered in Mid-Year 2020 and Year End 2020, respectively. Retail and office remain towards the bottom of the market cycle, and a consistent share of respondents expect each of these sectors to move to early recovery a year from now compared to the survey six months ago. Since December, retail switched with hospitality yet again to become the sector with the worst conditions (downturn + bottom), likely due to the continuing long-term impacts of online shopping outpacing gains seen in experiential retail as the nation reopens. The industrial sector continues to be a bright spot in real estate and for-sale housing emerges as another strong performer, with only 3% of respondents for each use stating that it was in a downturn or at the bottom of the cycle.

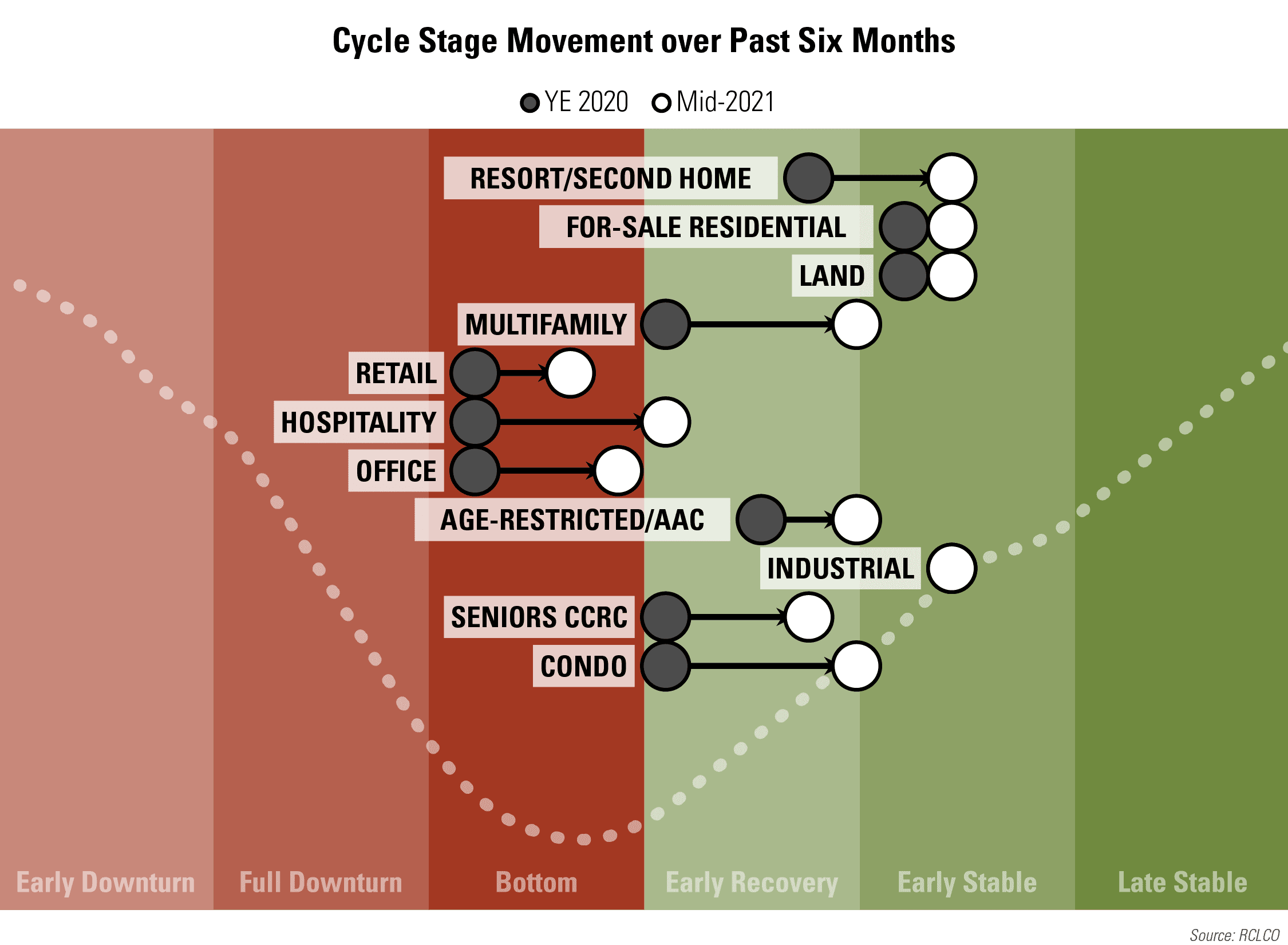

Survey respondents believed that most of the major real estate sectors moved from bottom or early recovery to expansion in mid-2021.

- The industrial sector continued its exceptionally strong performance due to increasing e-commerce penetration and home delivery surges throughout the year.

- Retail and office improved over the past six months but remain in the bottom part of the cycle, while hospitality moves into early recovery.

- All of these sectors were the hardest hit by COVID-19 shutdowns, stay-at-home orders, travel restrictions, and increased teleworking.

- Within these sectors, there were occasional bright spots – for example, more than 70% of respondents categorizing Medical Office and Grocery-Anchored Community/Neighborhood Centers in the healthy expansionary phase of the cycle, consistent with EY 2020 Sentiment.

Hospitality was bolstered in the past 6 months by strong sentiment in the Home Sharing/Airbnb/VRBO and in Extended Stay product, though there are indications of other sectors recovering as travel resumes.

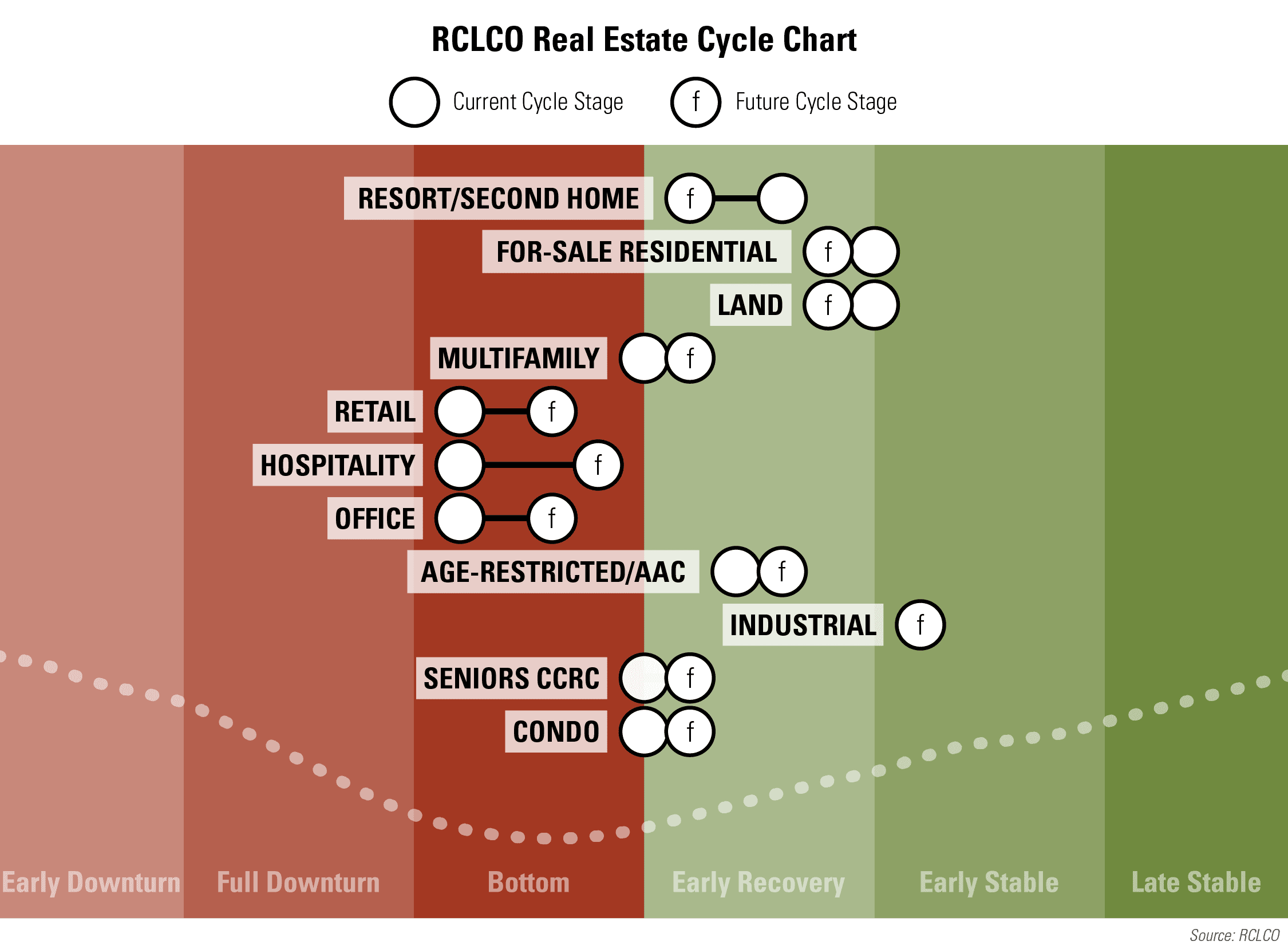

Expansion of most product types in the upcoming year

Looking forward, all sectors are predicted to improve, with many moving to a more favorable stage. Retail is expected to attain Early Recovery in the next 12 months, while hospitality and office are expected to move further into Early Recovery as office workers partially return and consumer confidence returns, enabling the economy to become more fully engaged. For-sale residential (including resort/second home) and land outperformed significantly in the downturn as buyers took advantage of historically low mortgage interest rates and were looking for more space; and not surprisingly, a significant share of respondents pegged these sectors to be in the Early Stable stage, indicative of healthy market conditions.

Economic Indicator Predictions for the Next Year

While interest rates have increased from lows earlier in the year, over 70% of respondents predict that interest rates will continue to increase moderately for the next year. A majority (68%) of respondents also felt that capital flows to real estate would increase over the coming year, echoing the positive real estate sentiment described in this article. Because interest rates still remain low and the for-sale residential market remains strong, nearly 60% of respondents predict that the homeownership rate will rise as first-time homebuyers purchase homes in increasing amounts. While there was relative agreement around increasing interest rates, increasing flows of capital to real estate, and a rising homeownership rate, there was less consensus around future cap rate levels. Of the respondents to this survey, 18% believe they will decrease moderately, 38% predict no change, and 34% predict a moderate increase.

Economic Indicators

Source: RCLCO

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and across the industry. Approximately two-thirds (72%) of respondents have worked in the real estate industry for 20 years or more, and 83% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 43% of the sample. Another 21% are investors or capital allocators, followed by 5% in design or architecture firms. The remaining 37% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

Sentiment Survey article and research prepared by William Maher, Director of Strategy and Research; Kelly Mangold, Vice President; and Grace Amoh, Associate.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at present compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.