RCLCO futuRE Series: A Driverless Vehicle Roadmap for the Real Estate Practitioner – Part 2

Introduction

As highlighted in part one of this series, fully autonomous, or “driverless,” vehicles (AVs) are going to become a reality within the next two decades and have the potential to bring about sweeping and transformative changes to society generally and real estate specifically. Every facet of the real estate industry, from land values and development costs to the very existence of certain asset types, stands to be affected. Investors, developers, and other real estate professionals who have the vision and foresight to plan accordingly will be able to capitalize on new opportunities as the landscape changes. Though some implications may come to bear too far in the future to be relevant to today’s practitioners, others, particularly for those planning or investing for the long term, are comparatively around the corner, requiring the industry’s attention within the near term.

This second part of the article applies RCLCO’s market perspective and knowledge of historical and current preferences and behaviors to the implications of this new technology. We specifically attempt to address how and when AVs could impact real estate, with the aim to spur broader discussion among our clients and the industry regarding what we can do to plan and prepare for their arrival.

How AVs Could Affect Real Estate

As autonomous vehicles begin to enter the market, they have the potential to affect real estate by influencing car ownership, commuting patterns, public transit use, consumer preferences, and parking demand.

Car Ownership

Over time, AVs should drive lower car ownership rates as people increasingly opt to share vehicles and trips.

The cost of owning and maintaining an autonomous vehicle likely keeps personal AV ownership out of reach for most households for the foreseeable future. Autonomous vehicles’ impacts on lifestyles are therefore likely to begin by contributing to the trend away from car ownership that has been facilitated by the rise of car and ride sharing (Zipcar, Uber, Lyft, etc.). These “”shared AV” fleets will most effectively serve urban areas, where many households have already spurned car ownership due to the costs and inconveniences associated with it. Shared AVs should be even less expensive than existing services given dramatically lower labor costs, further increasing the desirability of going carless.

For the same reasons that car sharing has failed to catch on in suburban and exurban areas, shared AV fleets may not initially be as economically feasible in these areas due to the challenges of scaling fleets in lower-density environments. Car ownership rates, even of AVs, may therefore continue to be higher in the suburbs, but could still be significantly reduced given the higher price tag and much more efficient asset utilization of AVs. Autonomous vehicles may serve as essentially personal family chauffeurs, shuttling family members around throughout different times of the day to the extent this works for the family’s schedule, rather than sitting unused in a parking stall. Car sharing among family members may be the norm in the suburbs, and AVs may facilitate much more efficient carpooling among either friends or strangers. AVs will also add considerably to the mobility of seniors who can no longer drive, people who never learned to drive or who have disabilities that prevent them from driving, and children.

Commuting Patterns

The potential of autonomous vehicles to ease traffic congestion, as well as to enable commuters to spend time engaging in more enjoyable or productive activities than driving, will likely make commuting less of a burden. This trend has significance for real estate because inconvenient commutes often lead people to live in locations that are more proximate to their employment, schooling, or other amenities, even though that may mean higher costs and less space. However, AVs’ anticipated efficiencies in time may entice many people to move farther from city centers to more affordable, less dense locations. Land that is currently perceived as too far away from employment cores to be developed could become more attractive as AVs contribute to more convenient commutes.

This trend could jumpstart development towards the outer edges of metropolitan areas. The current arbitrage between “close-in” desirable neighborhoods and more distant suburbs may decrease as desirability and land values increase for more distant locations. Longer term, depending on how AVs are introduced and what policies are in place, AVs may accelerate suburban and exurban growth and development.

Public Transit Use

People frequently choose public transportation over other modes because of perceived savings in terms of cost and/or time. However, the rise of cost-friendly and convenient autonomous vehicles could negatively affect the value proposition presented by mass transit. Any substantial reduction in demand for public transit would have significant ramifications for the real estate located near and around existing routes. AVs may therefore undermine the premiums associated with transit-oriented development today unless the public and private sectors effectively integrate AVs into existing systems and facilitate multimodal transportation solutions, or planners and developers identify other benefits or amenities to justify their density and premiums.

Parking Demand

As car ownership drops, the demand for parking follows suit. According to some estimates, there are around 500 million, and as many as 2 billion, parking spaces in the United States that occupy anywhere from 4,000 to 16,000 square miles (the equivalent of all the land in Connecticut and Vermont combined). Furthermore, it is estimated that around 1/3 of the land area in some U.S. cities is dedicated exclusively to parking.1 With so much land set aside for the storage of vehicles in lots, driveways, and garages, any reduction in demand for parking will have drastic impacts on land that is currently being used to accommodate it. Many downtown parking structures could become obsolete and minimum parking requirements could drop precipitously.

Depending on how quickly AVs are adopted, the net result of this “influx” of land and space previously dedicated to parking would be a in cities with a significant amount of space dedicated to parking. The reduction in parking requirements could also make development of dense projects in the urban core more feasible as burdensome subterranean or structured parking elements of developments are minimized or eliminated. Drops in land values and development costs could lead to increased housing affordability, potentially shifting the make-up of our cities. Parking in immediate proximity to homes and other destinations may become less crucial, allowing parking (and charging) lots to move to lower cost, less desirable locations, and requiring less space per car considering no people will be entering/exiting the vehicles in the lot.

Suburban areas may also see significant drops in demand for driveways, parking lots, and streets currently set aside to park vehicles. The sea of surface parking that traditionally surrounds suburban office parks or shopping centers could become unnecessary as people opt to share vehicles or have their cars spend the idle parts of the day shuttling people around or recharging at home. Less parking demand could affect suburban real estate by creating redevelopment opportunities and contributing to lower infrastructure costs for new developments.

Consumer Preferences

Household decisions regarding where to live, work, and play are as much influenced by preference as they are by convenience. In recent years, lifestyle choices, particularly among young consumers, have driven a resurgence in urbanization. Dense walkable environments have become favored areas of living relative to quieter suburban communities. AVs likely won’t alter preferences, but should serve to significantly enhance households’ ability to achieve them; they are an enabling technology that may allow households to live according to their wishes and not just because of convenience. Those who prefer urban living may find it easier and more affordable, while those preferring suburban or rural lifestyles may not have to sacrifice as much convenience as they currently do.

AVs’ Potential Specific Impacts

Anticipated Timing

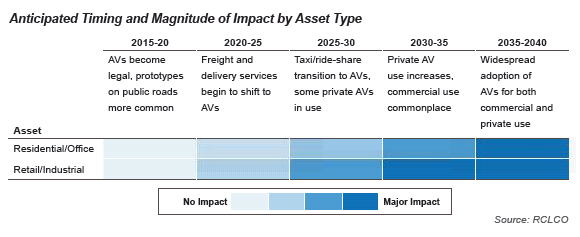

Although it is impossible to predict exactly when and how autonomous vehicles will enter our lives and become commonplace, observers anticipate their gradual introduction over the next 20 to 30 years. AVs in commercial freight and delivery services will likely be the first to be introduced, as private sector companies are especially motivated to find new ways to cut costs and enhance supply chains. The transition to autonomous commercial vehicles is already underway as evidenced by Nevada’s licensing of the world’s first officially recognized self-driving truck earlier this year. Autonomous taxis and shared fleets will likely follow suit with major transitions occurring sometime between 2025 and 2030. Around the same time, we expect affluent individuals to own and commute via their own private AVs, but the majority of consumers will likely still be priced out. Widespread adoption of AVs for both commercial and private use likely won’t happen until around 2035 to 2040.

The magnitude and timing of impacts on real estate vary greatly by product type, with retail and industrial affected the earliest by the rise of autonomous commercial vehicles. Residential and office properties will likely experience a much more gradual shift as commuting patterns and car ownership change incrementally. The sections below outline how we think each asset type could be affected by AVs over time.

Urban/Suburban Housing and Employment

Large urban areas will likely be the earliest to adopt AVs and subsequently experience their impacts. While programming AVs to correctly function in dense urban agglomerations has proved to be challenging, urban areas also offer the lowest barriers to the transition due to existing physical and wireless infrastructure, combined with population size and concentration, and the greatest overall consumer need.

We anticipate two potential phases of impacts on suburban development. In the earlier phase, likely as soon as the 2020s, the most desirable suburbs and rural areas may experience growing demand as some consumers, who previously chose smaller, higher density living to avoid long commutes, purchase AVs to make their commutes less arduous. Next, as autonomous vehicles become more affordable, suburban and exurban areas could experience more of a mass in-migration. At the same time, as urban living becomes more affordable many people may continue to prefer living in cities. Tracking how consumer preferences change over the next several decades will be crucial to understanding how AVs might ultimately affect housing.

AVs will likely further contribute to the trends enhancing the desirability and performance of CBDs and other high-quality regional employment cores. As they do today, firms will continue to favor areas with high concentrations of employers and employees so they can generate business, interact with clients and contractors, attract new employees, and exchange ideas. Demand for office space in the most dynamic cores as AVs make them more accessible, and create new opportunities for development as parking requirements decline.

To the extent that AVs make it possible for more seniors to continue living in their homes, AVs may reduce the demand for seniors housing such as independent living.

Retail and Industrial

Autonomous vehicles stand to greatly affect the demand for and value of industrial and retail properties. In conjunction with other technological trends, including the rise of e-commerce and same-day delivery, , assuming future innovations in autonomous delivery to customers’ homes and businesses. This trend is already gaining traction, as evidenced by Amazon’s “Prime Now” program (free two-hour delivery on certain items in participating cities) and plans for deliveries by drone, and will likely be accelerated by AVs in the future if logistics costs continue to decline by reducing labor costs and if AVs can serve as delivery vehicles when not being used to transport people.

This type of retail depends on last-mile industrial warehouses near major population centers that facilitate automated logistics chains for speedy fulfillment. As industrial properties become the “new retail,” and as people become more disengaged with their surroundings when they transition from drivers to full-time passengers, much of the functional retail like service stations or convenience stores will slowly become obsolete as demand withers. Even grocery-anchored centers, which have thus far largely avoided the relentless competition from e-commerce, could be disrupted by AVs that facilitate cheaper, faster, and more effective on-demand retail purchasing.

In the midst of the decline of functional retail, experiential retail—including entertainment, shopping for fine goods, dining, “seeing and being seen,” etc.—will likely continue to be relevant. Desirable destinations that feature consumer-oriented retail are likely to be much less susceptible to disruption than retail that exists purely to provide convenient access to goods. Industrial properties, especially those located close to population centers, will likely become increasingly valuable as they continue to facilitate e-commerce, while obsolete retail centers transition to look much more like industrial space.

Conclusion

As the transition to autonomous vehicles continues to take shape, and the implications become more certain, real estate and land use players should begin to take AVs into account in their decision making. Investors and other real estate practitioners should monitor the progress of AV technology and evaluate its potential timing to determine how much they should emphasize the impact of driverless cars in their planning and underwriting. While near-term opportunities to capitalize on the impending arrival of AVs are limited, we expect to see them factored into the real estate industry’s decision making within the next 10 years.

In spite of the many differing opinions about what the advent of AVs will bring and when they will arrive, society continues to progress towards an autonomous future that has major ramifications for the real estate industry. Consequently, real estate practitioners who are proactive and patient will be well-positioned to capitalize on this new technological trend rather than be disrupted by it.

1 Michael Kimmelman, “Paved, But Still Alive,” New York Times, January 6, 2012, accessed December 15, 2015, http://www.nytimes.com/2012/01/08/arts/design/taking-parking-lots-seriously-as-public-spaces.html

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us