June 26th, 2025

The past several years have brought unprecedented volatility to the RCLCO Real Estate Market Index (RMI)[1] – driven by dramatic shifts in market sentiment. After a short-lived boost at the end of 2024, sentiment has taken a dive back into the zone of real estate stress, with heightened uncertainty around tariffs, interest rates, and geopolitical stability.

Key Takeaways

- The RCLCO Real Estate Market Index (RMI) has declined over the past six months, ending at 37 in the mid-year 2025 survey, a decrease of 28 points since year end 2024. The index has now returned to challenging territory – an RMI below 30-40 is typically coincident with periods of economic and real estate market stress/recession.

- The survey reflects the prevailing market uncertainty, with respondents evenly divided on whether conditions will improve or worsen over the next 6 to 12 months. Despite this split, the Future RMI is projected to rise to 50 within the next year, suggesting a potential gradual return to expansion.

- Following a period in which recession concerns had largely subsided, nearly two-thirds of respondents (63%) now anticipate a recession within the next 12 months.

- Tariffs and labor availability have emerged as major concerns, with 85% of respondents expecting rising costs due to tariffs, and 71% expecting cost increases due to labor availability.

- Sentiment has softened across most land uses, with increasing concern regarding conditions in the for-sale residential markets. Rental housing and commercial land uses have shown relative resilience with sentiment remaining more optimistic, especially in certain high performing commercial sectors such as industrial, grocery/necessity retail, and hospitality. However, the outlook for a majority of the sectors is anticipated to improve over the next year.

From Resilience to Risk: Sentiment Slumps on Economic Jitters

The RMI Index has experienced a series of dramatic swings over the past several years. Following a strong but short-lived recovery at the end of 2024, sentiment has once again declined sharply by mid-2025, driven by mounting economic uncertainty. Concerns over rising costs stemming from tariffs, inflation, labor shortages, and geopolitical instability have all contributed to this downturn. The current RMI has fallen to 37.2, reflecting a market in which respondents are increasingly cautious and adjusting to a continuously shifting economic environment.

RCLCO National Real Estate Market Index

Source: RCLCO

Browse Past Sentiment Surveys

The outlook for the year ahead mirrors the broader market uncertainty, with an equal share of respondents believing conditions will improve as those expecting them to deteriorate.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Recession Fears Resurface

After closing the year with recession fears largely subdued, sentiment has shifted noticeably toward greater concern. Currently, 63% of respondents anticipate a recession within the next 12 months, including those who believe one is already underway, while 12% expect a recession to occur beyond the one-year mark. Just 25% consider a recession unlikely within the next two years. This represents a significant shift from a year ago, when only 43% predicted a near-term recession and 39% believed a downturn could be avoided in the next two years.

When Will the Next U.S. Recession Occur?

Source: RCLCO

Tariffs, Immigration Policy, and Concerns about Global Unrest

Tariffs, especially on key construction materials such as steel, aluminum, lumber, and other imported fixtures, appliances, and equipment have the potential to influence the real estate industry as a key component in rising construction costs. The level of announced tariffs has changed over time, but the impact on the industry is already being felt, with 70% of respondents already noticing an increase in costs due to tariffs. Labor is the other part of the construction cost equation, and while estimates vary by geography and specific construction trade, somewhere in the range of a quarter of all construction workers are foreign-born, with certain trades (drywall, roofers, painters, etc.) comprised of 50% or more immigrant labor.[2] Over half (53%) of respondents have already experienced increasing labor costs, and the impacts of both tariffs and labor costs are expected to rise over the next six months. Additionally, recent events in the Middle East have heightened geopolitical instability, posing potential risks to the global economy and real estate markets.

Tariffs Have or Will Cause:

Source: RCLCO

Immigration Policy/Labor Availability Has or Will Cause:

Source: RCLCO

Sentiment Falters at Mid-Year, But Conditions are Expected to Improve

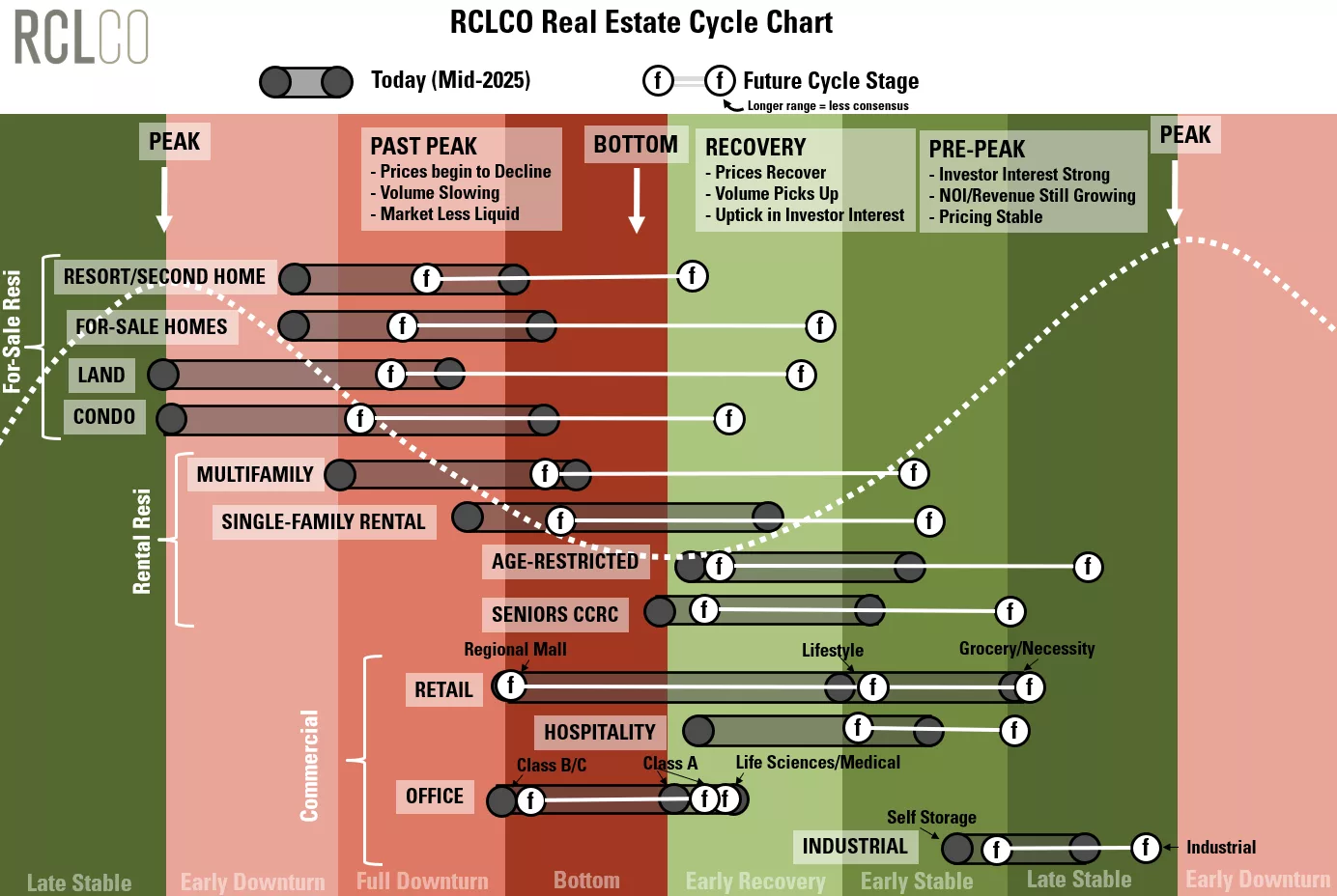

While many sectors appeared to be entering recovery at the close of 2024, sentiment has deteriorated in mid-2025, with several land uses once again showing signs of distress. Survey respondents indicated increasing concern regarding conditions in the for-sale residential markets, driven by a mix of continued high mortgage rates and broader economic uncertainty. In contrast, the rental residential market has proven more resilient, with age-restricted and seniors housing performing particularly well amid recent challenges.

In the commercial realm, sentiment has held steady relative to year-end 2024. Struggling segments such as regional malls and Class B/C office space remain firmly in downturn, while high-performing sectors such as grocery/necessity retail, hospitality, and industrial continue to exhibit expansionary conditions. Looking ahead, respondents generally expect improvement across most land uses over the next 12 months. Despite current softness in sentiment, the broader outlook remains optimistic.

Land Use Cycle Stage Today and Looking Ahead 12 Months

Economic Indicator Predictions for the Next Year

Generally speaking, respondents expect key indicators that have an impact on real estate to worsen somewhat over the next year, as uncertainty causes sentiment to falter.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

- Nearly an equal share (~40%) think interest rates will decrease as those who feel they will stay the same, and the remaining 20% think they will increase. This is a decline in sentiment from mid-year.

- Respondents feel cap rates will stay the same (40%) and the remainder are split between increasing and decreasing rates. There is less consensus than at year end when a larger share believed cap rates would decrease.

- The inflation outlook has less variation than at year end – with half believing it will increase, and 29% predicting that it will stay the same.

- 43% of respondents now believe that capital flows to real estate will increase over the next year, down from 68% at year end.

- Views on construction costs were more pessimistic than at year end with 65% predicting an increase.

- The homeownership rate was predicted to decrease by 35% of respondents, a larger share than at year end.

- There was a wide range of forecasted 10-year treasury yields, although 67% predicted it to be between 3.5% and 4.5% in 24 months.

Because it has a big impact on real estate valuation and debt costs, where do you think the 10-year treasury will be 24 months from now?

Source: RCLCO

RCLCO POV

Q2 2025 – Increased Economic and Market Uncertainty Could Slow Growth in 2025

Recent developments in U.S. trade policy as well as geopolitical events have introduced a higher level of uncertainty that could weigh on economic growth and real estate market activity in 2025. Many economists have lowered near-term growth projections and increased the likelihood of a recession within the next 12 months.

It appears increasingly likely that tariffs are part of a short-term negotiating strategy, yet the uncertainty surrounding these policies has caused hesitation among real estate investors and capital markets participants. At last year’s end, RCLCO expressed optimism that 2025 could mark the beginning of a gradual recovery in real estate fundamentals. While that scenario remains possible in the mid-term, today’s rapidly changing environment makes forecasting more difficult and makes current conditions rocky. We continue to monitor developments closely.

The risk of a trade war has introduced a new layer of unpredictability to the economic outlook, though long-term sectors like real estate may be better positioned to weather near-term market fluctuations. A number of economic indicators are now signaling increased risk: consumer confidence has declined, inflation expectations have risen, and economists have raised the probability of a recession in the coming year.

The Conference Board’s Expectations Index recently fell to its lowest level in over a decade, and the Federal Reserve has revised down its 2025 growth forecast while signaling fewer rate cuts than previously expected. Major financial institutions have also adjusted their forecasts, citing slower growth, rising inflation, and an uptick in expected unemployment.

While changes in regulatory and tax policies could provide some upside for real estate, higher inflation and trade-related challenges may offset those potential gains. RCLCO’s overall outlook for the real estate sector has become somewhat less optimistic, as consensus forecasts for real GDP growth in 2025 and 2026 have recently dropped from around 2% to the mid 1% range annually—raising the likelihood of a recession among other possible outcomes. Long-term NOI growth projections remain unchanged for now, as it is still too early to assess whether the structural risks posed by tariffs will have a lasting impact on fundamental demand drivers.

Despite current headwinds, RCLCO’s base case remains cautiously optimistic, projecting that the U.S. real estate market will benefit from relatively favorable investment dynamics, limited downside risk, and attractive opportunities as conditions stabilize in the coming weeks and months. While the proposed trade policy changes present real and significant risks to the global economy, a worst-case scenario appears less likely amid growing political consensus favoring economic growth and backlash against the April 2nd tariffs. Investors should remain vigilant as volatility may complicate decision-making, but long-term demand fundamentals and continued capital flows into real estate support a positive outlook, with potential for opportunity amid the uncertainty.

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. A majority (74%) of respondents have worked in the real estate industry for 20 years or more, with an average respondent tenure of approximately 27 years, and 84% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Type of Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 41% of the sample. Another 19% are investors or capital allocators, followed by 5% in design or architecture firms. The remaining 35% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Primary Region/Market

Source: RCLCO

The respondent mix is representative of the U.S. as a whole: however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Sentiment Survey article and research prepared by Charles Hewlett, Managing Director; and Kelly Mangold, Principal.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

[2] National Association of Home Builders. Concentration of Immigration in Construction Trades. Accessed June 23, 2025. https://www.nahb.org/advocacy/industry-issues/labor-and-employment/immigration-reform-is-key-to-building-a-skilled-workforce/concentration-of-immigration-in-construction-trades

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Copyright ©️ 2025 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.