September 10, 2020

By Derek Wyatt, Managing Director , Vahe Avagyan, Vice President , Nicholas Stefanoni, Senior Associate

Over the past two decades, the presence of Whole Foods in a neighborhood has functioned as an unmistakable cultural signifier, reflecting an area’s affluence, lifestyle preferences, and evolution. Much like other premium “lifestyle” brands including SoulCycle, Lululemon, and Equinox, Whole Foods has found success by combining high-quality products and service (and prices) with a perceived ethos of wellness, health, and self-care. This product offering has strongly resonated with affluent audiences, from Millennial urbanites to Gen X suburbanites, driving Whole Foods’ proliferation into every up-and-coming neighborhood (urban or suburban) in America.

The impact that a well-known grocer like Whole Foods can have on a neighborhood—what we refer to as the “Premium Grocer Effect”—had, until RCLCO’s analysis, only been studied from relatively narrow perspectives. Much has been written about the sociological and cultural implications surrounding the brand, while economic and quantitative analyses of Whole Foods’ impacts have been limited to neighborhood-level phenomena, such as changes in surrounding land values or home prices. In 2016, RCLCO sought to understand what effect the presence of a Whole Foods has on the value of an individual real estate investment from the perspective of the owner or developer—questions that had, until our analysis, largely gone unanswered. In RCLCO’s quantitative 2016 analysis, we found that ground-floor Whole Foods add value to apartments within the same development by driving rental premiums, enhanced absorption, and accelerated rent growth in comparison to other nearby properties.

Since our analysis in 2016, the high-end grocer market has changed in ways small and large, including Amazon’s $13.7 billion acquisition of Whole Foods in 2017, along with the proliferation of other premium grocers beyond just Whole Foods.[1] In light of these changes, two important questions emerged: first, has Whole Foods’ impact on apartment performance changed in recent years? And second, are other premium grocers, including up-and-coming or regional brands, able to replicate the success of Whole Foods as ground-floor tenants and drive similar premiums for apartment communities?

Our revised analytical effort sought to answer the following key questions:

- What premium on rental rates, if any, does a ground-floor Whole Foods, Trader Joe’s, or Other Premium Grocer generate for the apartment community within which it is located?

- How does these properties’ premium positioning relate to their rent growth over time?

- When a new apartment community with a ground-floor premium grocer delivers, does it capture above its fair share of demand during lease-up?

Key Findings

Rental Rate Premium

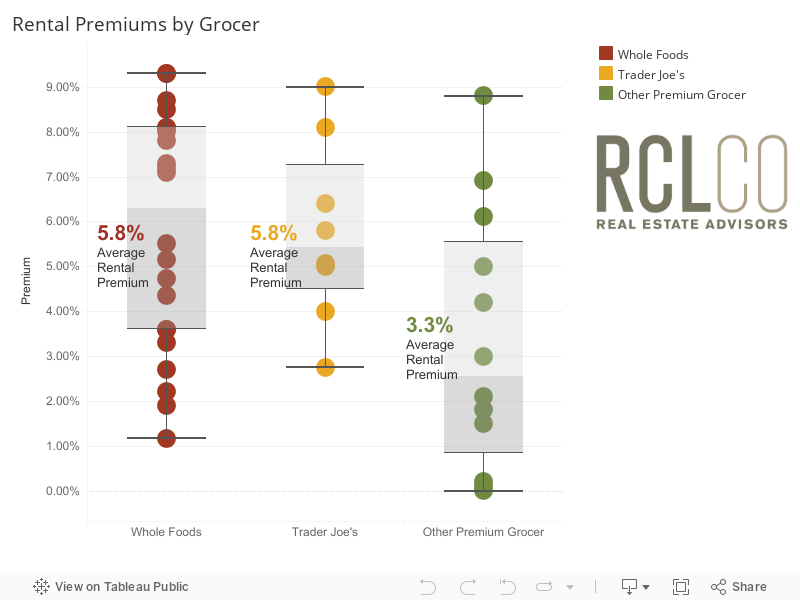

Whole Foods & Trader Joe’s buildings both earn 5.8% premium

Other premium grocers achieve smaller, but still significant, 3.3% premium

Apartment communities with a Whole Foods on the ground floor achieve, on average, a rental rate premium of 5.8% above comparable apartment communities in the immediate local area, after adjusting for qualitative and quantitative differences among these communities. This represents an increase of 1.5 percentage points relative to our findings in 2016, when we found that Whole Foods buildings earned only a 4.3% premium.

Communities with a ground-floor Trader Joe’s earn the same premium—5.8%—as those that contain a Whole Foods. In 2016, we found the gap between buildings with Trader Joe’s and Whole Foods to be significantly wider—Whole Foods buildings achieved a 4.3% premium, which is one percentage point higher than the 3.2% achieved by Trader Joe’s buildings. However, over the past several years, that gap has diminished, with Trader Joe’s conferring a comparable premium to apartment rents as Whole Foods.

Other Premium Grocers, which were not included in our 2016 analysis, drive a lower—but still meaningful—premium of approximately 3.3%.

Rental Growth

Communities that achieve the highest premiums also experience the strongest rent growth, yet the presence of a premium grocer is no guarantee of higher rent growth

When comparing the relationship between average rent premium and average rent growth for 2018 to 2019, Whole Foods properties that achieved the highest premiums also experienced the strongest rent growth, reflecting a positive linear relationship between rent premium and rent growth. Buildings with Trader Joe’s experienced a flat relationship, meaning that higher premiums did not necessarily correlate with stronger rent growth.

Note: in this chart, bubble size is reflective of the rent per square foot for each community.

Absorption Pace

Premium rents do not inhibit the absorption of premium grocer buildings—in many cases, they capture more than their fair share of market demand

We profiled the absorption performance of eight of the case studies with ground-floor premium grocers. A new building with a ground-floor, premium grocer can expect to lease-up units at a pace at least on par with—but frequently above—its fair share capture of submarket absorption during the lease up period. When these grocer-anchored buildings first open, their capture rates tend to exceed their fair share of submarket demand, but stabilize to approximately fair share levels over time.

“The Premium Grocer Effect” is Coming to a Town Near You

The presence of a ground-floor premium grocer has a meaningful impact on apartment performance, measured in terms of rental rates and lease-up pace. Brand cachet, particularly among Millennials who have been the primary target market for most new apartment buildings, is clearly important, as properties containing a Whole Foods or Trader Joe’s on the ground floor are able to achieve the highest rental rate premiums. The increase in the rental rate premium for Whole Foods, and especially for Trader Joe’s, relative to the prior analysis, highlights the growing importance of convenient access to high-quality, wellness-oriented grocers to renters, particularly affluent renters in major metropolitan areas. Moreover, the emergence of other premium grocers with a similar orientation—but less established brand power—as Whole Foods and Trader Joe’s shows that other brands are also able to capitalize on this trend, conferring a smaller, but still substantial, premium to rental rates in the communities within which they are located.

It is important to note that this analysis does not take into account the impacts of COVID-19, which continue to unfold daily, as the rental data was collected in April 2020. While the staying power of the impacts of COVID-19 on consumer behavior and spending cannot yet be discerned, there is a possibility that increased consumer spending at grocery stores—and an accelerating focus on health and wellness—could drive further increases in the premiums that communities with premium grocers are able to achieve in the future.

Methodology

Overall Framework

In order to adequately measure the impacts of a ground-floor premium grocer on apartment performance, RCLCO relied on apartment performance data from Axiometrics for 64 apartment communities across 20 different MSAs, each of which contain a premium grocer on the ground-floor.[2] Each case study project’s performance was individually compared to the performance of two to five comparable apartment communities, which—barring the presence of a ground-floor grocer—represent the most comparable apartment product in terms of age, scale, quality of execution, and market positioning within the immediate local neighborhood of each case study.

This analysis sought to isolate the premium that is derived from the presence of a ground-floor premium grocer. In reality, many apartment communities that contain a ground-floor premium grocer earn a noticeably higher premium relative to local comps. However, a meaningful share of this premium is due to the higher-quality execution and amenitization that tends to characterize communities that attract ground-floor premium grocers, rather than the impact of the grocer itself.

Rental Premium

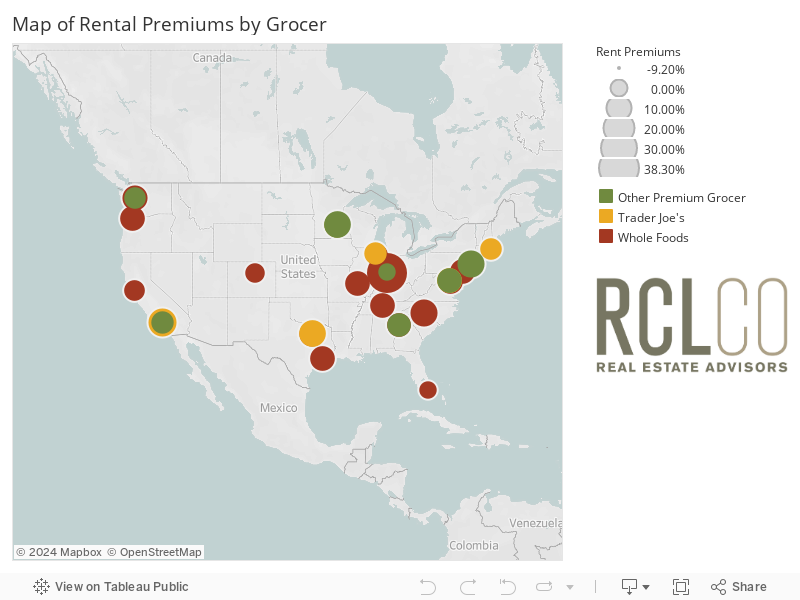

RCLCO analyzed 31 apartment communities with a ground-floor Whole Foods tenant, 15 with Trader Joe’s, and 18 with Other Premium Grocers, located in 20 different MSA’s and 50 submarkets across the nation.

After identifying each case study, we then selected between two and five nearby buildings within each local neighborhood that were similar in terms of age, scale, type of construction (i.e. low-, mid-, and high-rise), quality of execution, and overall market positioning. We collected the average asking rents for each case study and comparable community in April 2020. The rents at each comparable community were then adjusted for size (to allow apples-to-apples comparisons of rents), and further adjusted to control for other qualitative and quantitative differences between properties, such as building age, quality of location (measured using Walk Score and Transit Score), in-unit finishes and features, and quality and quantity of community amenities. The resulting adjusted rents for the comparable properties were then compared to the average rent in the grocer-anchored case study building. This methodology allowed us to make an apples-to-apples rent comparison, meaning that the resulting difference in rents between each case study and its comparable communities can be attributed to the impact of a ground-floor premium grocer tenant.

Rental Growth

RCLCO investigated the relationship between average rent premiums and rent growth to understand if the premium conferred by a ground-floor retailer also contributed to enhanced rent growth. Due to the impacts of COVID-19 on rent growth in 2020, our analysis focused on rent growth during more stable market conditions in 2018 and 2019.

RCLCO evaluated a rolling three-month average rent growth among each case study with available data for 2018 and 2019. We then compared the average rent growth of these case studies in 2018 and 2019 with the average rental premium they achieved, to understand the relationship between rent premiums and rent growth.

Absorption Pace

RCLCO analyzed the lease-up performance of two Whole Foods buildings, three Trader Joe’s buildings, and three other premium grocer buildings that had adequate monthly data available on lease-up rates. RCLCO compared each case study’s actual capture rate of submarket net absorption with its expected, or “fair share,” capture of the submarket’s net absorption relative to other newly delivered buildings in lease-up each month. This “fair share” capture rate estimate was calculated based on the overall number of new units leasing up in each submarket at the respective point in time. For example, if 1,000 units (including the case study building) were in lease-up at the same time, the “fair share” capture rate for a case study building of 200 units would be 20%. Buildings that capture more units than their “fair share” can be said to be outperforming the submarket, compared with those buildings absorbing units in-line or below their “fair share” of demand. In order to account for reporting inconsistencies, we employed a rolling three-month average for these calculations.

Article and research prepared by Derek Wyatt, Managing Director; Vahe Avagyan, Vice President; and Nicholas Stefanoni, Intern.

References

Thumbnail and header images courtesy of Eighth & Grand

[1] Due to differences in sample sizes across different grocers, we grouped these grocery stores into three categories: Whole Foods, Trader Joe’s, and “Other Premium Grocer” (which includes such brands as Sprouts Farmers Market, Fresh Thyme, Harris Teeter, Fairway Market, and Safeway).

[2] RCLCO’s analysis considered all potential properties with ground-floor premium grocers. This set was narrowed to 64 case study properties, which had relevant comparable communities against which their performance could be measured. While the analysis measured the performance of all 64 case study properties, those that represent statistically significant outliers—or had insufficient or incomplete data—for each metric analyzed (rent premium, rent growth, or absorption) are excluded from the averages presented in this report.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.