May 29, 2025

In a recent RCLCO Advisory, my colleagues Adam Ducker and Taylor Mammen noted that despite rising concerns tied to the Trump administration’s tariff policies and growing fears of a slowdown, RCLCO remains cautiously optimistic about U.S. real estate. Market fundamentals remain sound, and for disciplined investors, opportunities still exist, though the margin for error is narrower.

This Advisory focuses on the residential sector specifically, both in terms of current conditions, and, if a recession does materialize, how much impact it might have on new home sales, rental vacancies, and new for-sale and for-rent housing supply and demand. To gauge this, we reviewed how the residential market performed during the last eight U.S. recessions and compared those patterns to today’s fundamentals.

Key Takeaways

Demographics continue to drive long-term demand.

Millennials and Gen Z remain active forces in the housing market—Millennials in homeownership, and Gen Z in multifamily rentals—while Boomers sustain demand for second homes and active adult living.

Multifamily rental market shows resilience.

Slowing new supply and strong renter demand set the stage for tighter markets and rising rents in 2026 and beyond.

Recession risk remains, but fundamentals hold.

Despite rising concerns over tariffs, inflation, and elevated interest rates, housing market fundamentals remain relatively sound. RCLCO expects modest decline in supply and demand and little if any negative impacts on residential pricing in the event of a mild recession.

New home market is cooling.

Homebuyer confidence and builder sentiment have declined. If there is a recession, new home sales and permits could decline by 10% or less, with prices trending down slightly, especially if mortgage rates stay high.

Luxury and vacation home markets respond differently than the general market.

These segments are less vulnerable to recession due to their affluent buyer base—but they’re highly sensitive to stock market performance and investor confidence.

As of May 2025, both homebuyer confidence and homebuilder sentiment are weakening. Affordability remains a significant challenge for buyers, while builder sentiment is down. The NAHB/Wells Fargo Housing Market Index (HMI) dropped to 34 in May, down six points from April, marking the lowest level since November 2023. This decline reflects builder pessimism linked to elevated interest rates, U.S. tariff policies, and continued inflation in materials and labor. That said, builder sentiment remains above the historic lows of 2009.

With interest rates still elevated, inflation lingering, and both consumer spending and job growth losing momentum, the risk of a recession remains, though it’s not a given. Still, these conditions make it essential to closely examine how a potential downturn could affect the new home market.

Historical Perspective

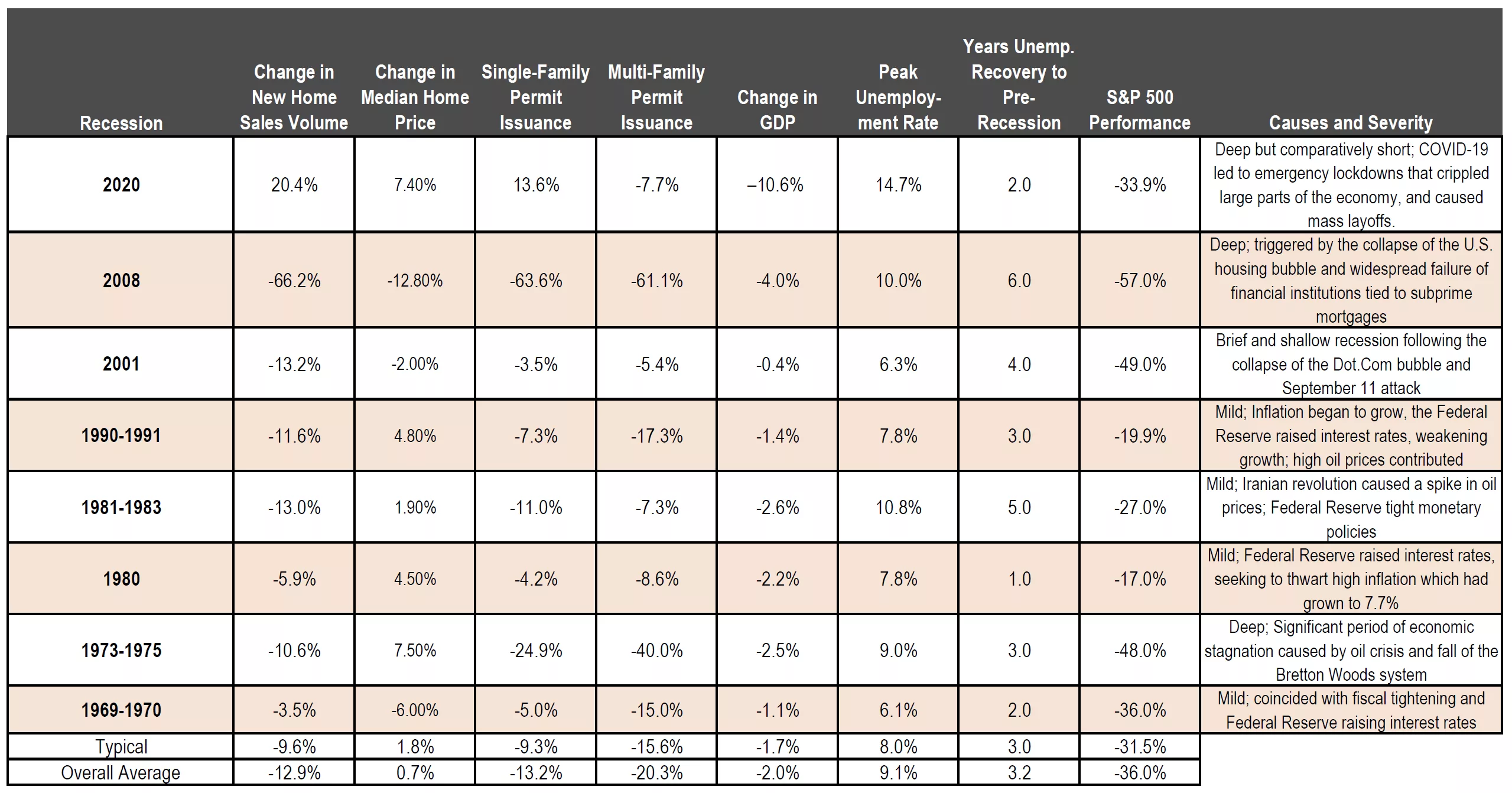

In past recessions, new home sales volume has declined by anywhere from -3.5% to -66.2%. The worst-case scenario, the 2008 financial crisis, is unlikely to be repeated this time around. Excluding both the Great Financial Crisis and the 2020 pandemic recession (when new home sales rose), the typical decline in sales volume during a recession has been under 10%. Recovery of employment levels has historically taken about three years.

Based on current conditions, a mild recession would likely lead to:

- A decline of less than 10% in new home sales and permits.

- Modest downward pressure on prices.

- Limited long-term disruption, with gradual improvement possible in 2026 if mortgage rates ease.

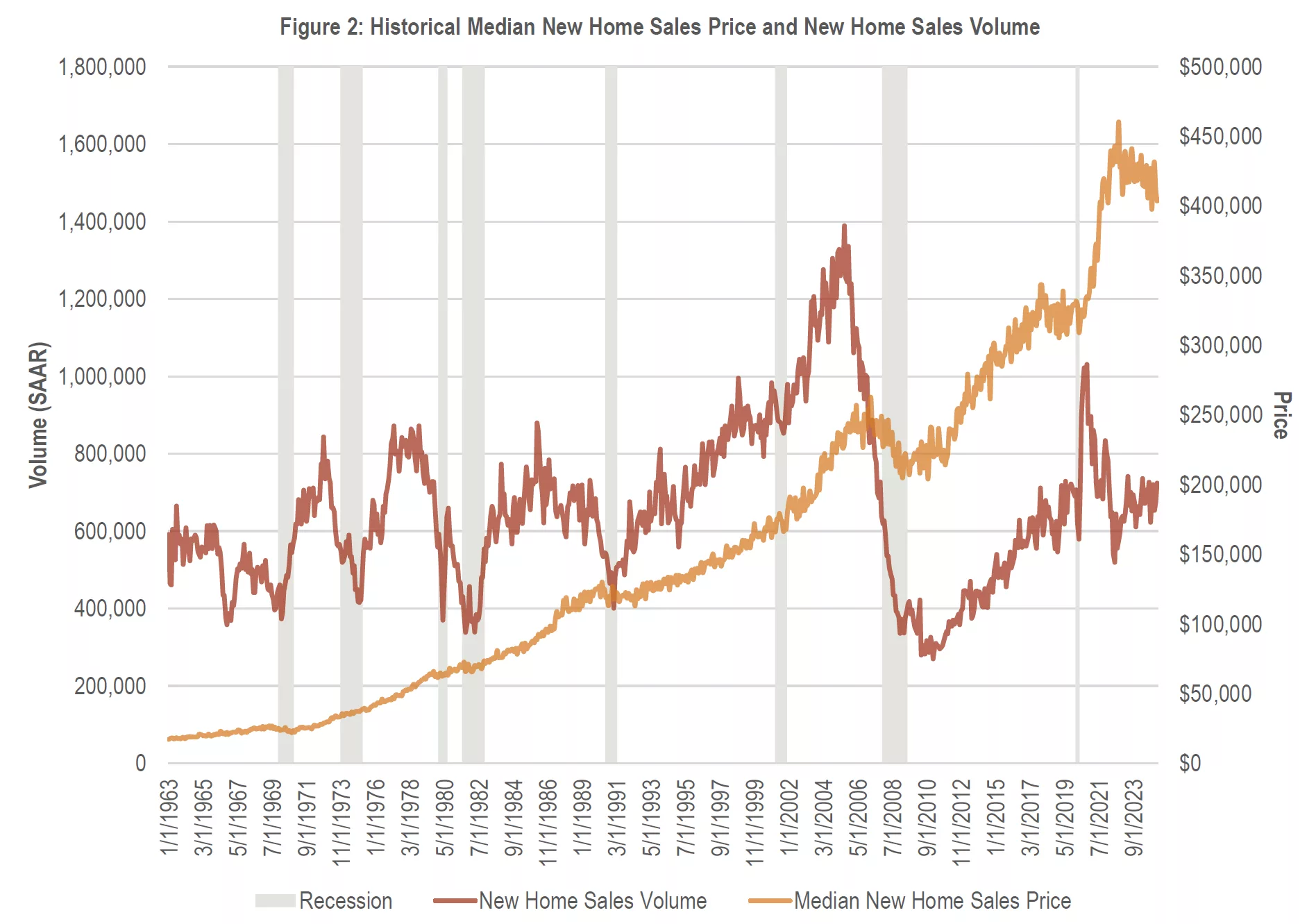

Evidence of home price softening is already visible. While there was a notable peak in median new home prices at the beginning of 2025, subsequent months have seen a downward trend, bringing prices below 2024 levels. In April 2025, the U.S. Census Bureau reported that the median sales price of new single-family homes was $407,200, a 2.0% decrease compared to April 2024, when the median price stood at $415,300. Around 20% of resale listings have seen price reductions, the highest share since 2016. Builders continue to respond with incentives; roughly 60% are offering concessions to close deals. Yet elevated mortgage rates continue to weigh on affordability, especially for first-time buyers.

Luxury and Vacation Home Markets

The luxury and vacation home end of the market, while similarly exposed to recession, is not equally vulnerable. While it can be more cyclical and discretionary than the primary home market, because it caters to wealthy home buyers it can also be more resilient. Of course, that partially depends on what happens in the stock market. Luxury and vacation home buyers are more exposed to equities and financial assets. During periods of stock market downturns or wealth contraction (e.g. 2008), discretionary purchases like vacation and second homes often get delayed. There is a strong relationship between the stock market and second home/vacation home purchases, especially at the higher end of the market. The key link is that discretionary housing demand rises and falls with household wealth and investor confidence, both of which are heavily influenced by equity market performance. Affluent households feel richer when their portfolio values rise, leading them to consider big-ticket purchases like second homes. When markets are strong, buyers prioritize quality of life, retreats, and status, driving demand for homes in resort destinations like Palm Springs, Aspen, or coastal Florida.

Resilience of the Rental Housing Market

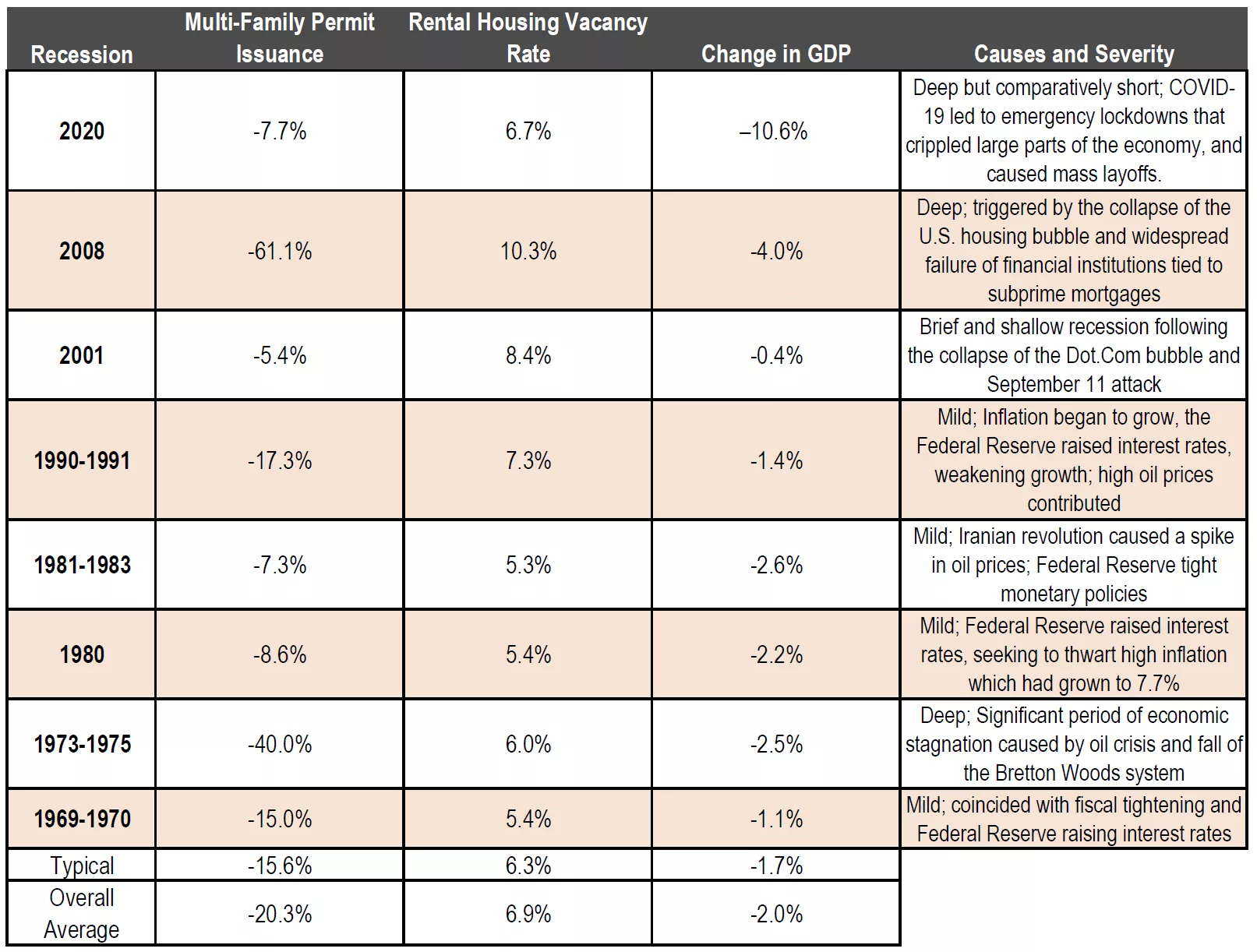

Rental housing has historically weathered recessions more effectively than the for-sale market. In past recessions, overall rental vacancy rates have rarely exceeded 7%, and permit issuance for new units typically declined by 7% to 15%. Excluding the 2008 and 2020 recessions, multifamily vacancy rate increases during recessions have typically ranged from 0.5% to 1.2%. These modest rises reflect the sector’s resilience, as the demand for rental housing often remains relatively stable even during economic downturns. Now, following a period of rapid new deliveries, the multifamily market is moving toward stabilization as demand remains strong and the influx of new supply diminishes. We expect continued improvements in occupancy rates and gradual rent growth throughout 2025 and into 2026, though of course regional disparities will persist, influenced by local supply dynamics and economic conditions.

Given the on-going shift in the rental market from a period of rapid growth in supply to a potential future undersupply, permitting is likely to remain more stable if there is in fact a recession. The most recent data show multifamily permitting activity declining to an annualized pace of 438,000 units, significantly below the post pandemic boom (651,300 units in 2022, 536,400 in 2023 and 441,600 in 2024). The current slowing in new construction is expected to lead to tighter rental market conditions, exerting upward pressure on rents in 2026 and 2027. Following a peak of 591,700 units delivered in 2024, multifamily deliveries are projected to decrease to approximately 525,000 units in 2025 and further to 414,000 units in 2026. Looking ahead, these dynamics will likely result in a much more competitive rental market.

In summary, Gen Z is fueling strong interest in multifamily housing including that for build-to-rent communities that offer flexibility and lifestyle appeal, supporting a cautiously optimistic outlook towards stabilization of the rental housing market in 2026, with a tightening supply-demand balance in metros with good population and job growth. For for-sale housing, despite short-term headwinds like elevated interest rates and waning buyer confidence, strong demographic fundamentals continue to support the demand for new housing. If a recession does occur, this underlying demand suggests the impact on new home sales and pricing will likely be moderate and relatively short-lived. Millennials remain a strong force behind new home demand, especially in high-growth Sun Belt and Western metros. Baby Boomers remain active in the market, fueling demand for single-level homes, active adult communities, and second homes. Our thesis continues to be that market fundamentals are sound.

Eric Whinnen, Senior Associate, and Jameson Logan, Analyst, contributed research to this article.