December 18th, 2025

By Charles Hewlett, Managing Director; Kelly Mangold, Principal; Kaity Molito, Associate

The 2025 Year-End RCLCO Sentiment Survey depicts an economy and real estate market still navigating a challenging environment, with current conditions remaining at stressed levels but expectations beginning to improve. While risks remain evident, sentiment suggests a shift toward stabilization and growth in the year ahead.

Key Takeaways

- The RCLCO Real Estate Market Index (RMI) has remained relatively flat since mid-year, rising four points to 41, and remains towards the top of a range historically linked to economic and real estate market stress.

- Despite tepid current sentiment, market participants are increasingly optimistic about the future, with half anticipating moderately or significantly improved market conditions. The Future RMI reflecting expectations about the next 12 months has rebounded nearly 15 points to 63, showing optimism about the future.

- Recession fears have subsided significantly with only 29% of respondents expecting a recession within the next year – this is down more than 10 points from the RCLCO Mid-Year survey when 44% of respondents expected a recession within 12 months.

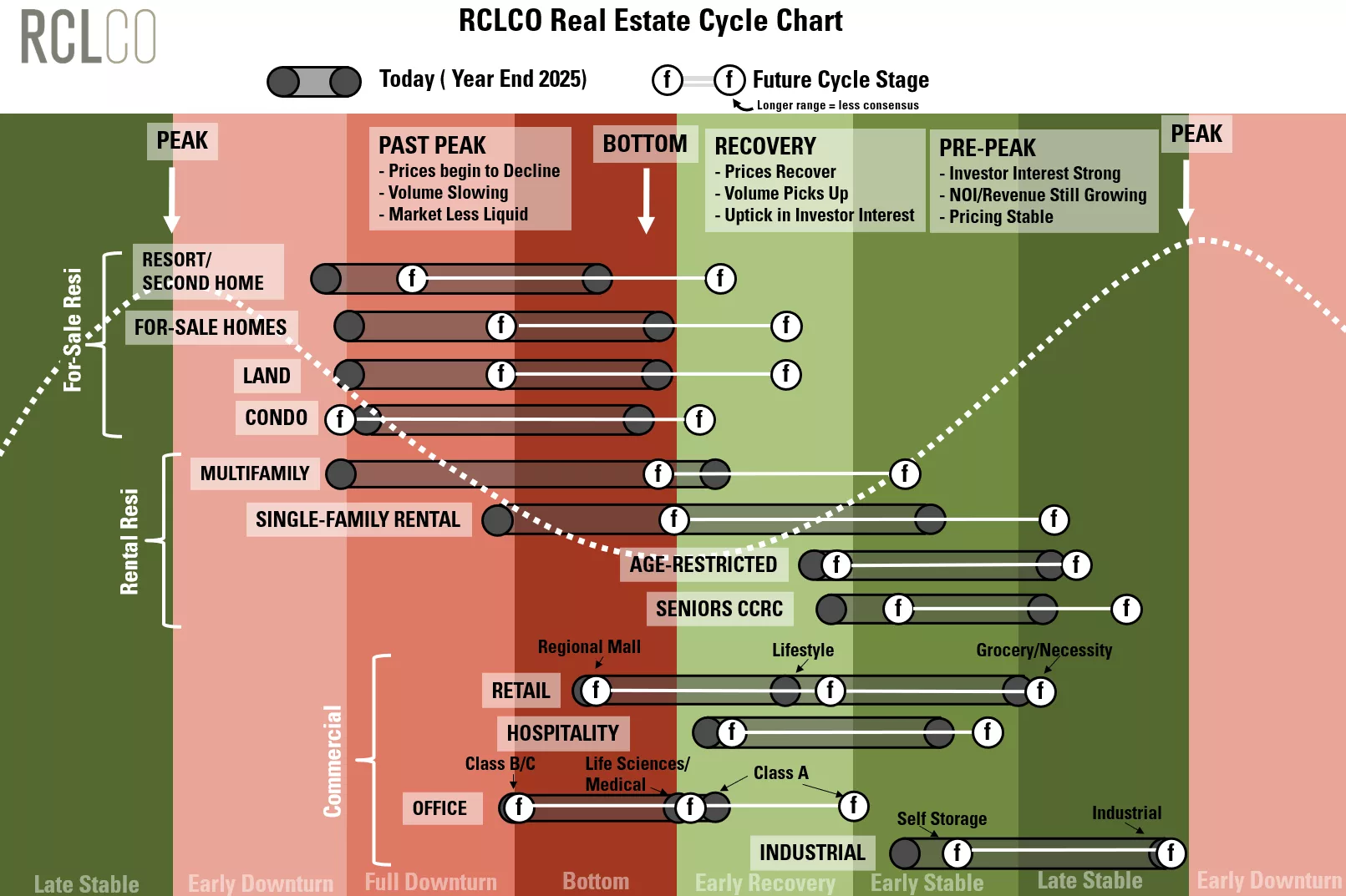

- Most market participants believe that the for-sale and rental housing sectors are currently still in downturn mode, or bumping along the bottom, while industrial, self-storage, senior housing, and lifestyle and necessity retail are experiencing some growth. However, respondents are expecting nearly every real estate sector to be in growth mode once again over the next 12 months. The exceptions to this are Class B/C office and regional malls, which are expected to continue to experience stress.

- With all of the hype around AI and associated demand for data centers, we asked market participants whether there was a risk of a bubble in this niche sector, and nearly two-thirds responded in the affirmative, with most respondents indicating that they thought power and energy availability could be a limiting factor on future development of data centers.

More Sticks and Bricks in 2026?

By Year-End 2025, the RMI[1] shows a market still in the doldrums. After dipping to 37.2 at mid-year, sentiment has improved slightly to 40.95, suggesting modest stabilization but not a material positive shift in momentum. While this is better than some of the more challenging moments in recent history, it remains below the long-term average since 2011 and still in the range historically linked to economic and real estate market stress. Overall, the responses reflect a real estate market that is steadying, but still contending with low levels of activity and macroeconomic uncertainty.

RCLCO National Real Estate Market Index

Source: RCLCO

Detailed Results

Current National Sentiment Over Time

Source: RCLCO

National sentiment over time reflects a market that has moved away from the most severe pessimism observed in 2022 and 2023. Conditions improved tentatively in 2024, marked by a notable rise in respondents describing conditions as moderately better and a sharp decline in those reporting significantly worse conditions. By Year-End 2025, sentiment has settled into a more mixed and tempered state: while negative views still outweigh positive ones, they are driven primarily by moderate pessimism (44%), with only a small share (3%) characterizing conditions as significantly worse. At the same time, nearly 30% of respondents view conditions as moderately better and more than 20% see no change, indicating a market that remains in distress but is not dominated by expectations of further decline.

Browse Past Sentiment Surveys

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Looking forward, expectations for 2026 are markedly more positive than the present sentiment. Notably, more than twice as many respondents anticipate moderate to significant improvement as those expecting conditions to worsen, underscoring a shift toward optimism.

Risk of a Recession Receding?

When Will the Next U.S. Recession Occur?

Source: RCLCO

Expectations around the timing of the next U.S. recession are dispersed, with no single outcome dominating responses. Roughly one third (30%) of respondents believe a recession is likely within the next 12 months, and an equal share view a recession as unlikely within the next 24 months. The lack of consensus suggests elevated uncertainty around recession timing, with respondents split between near-term concern and expectations that an economic downturn remains further out.

Data Center Growth: Bubble or Balance?

To What Extent Do You Think Data Center Demand and Development is a Bubble?

Source: RCLCO

Perceptions of data center demand and development skew toward measured concern rather than alarm. A majority of respondents view current demand and development as at least somewhat overheated, with roughly one-third characterizing it as slightly a bubble and a similar share seeing it as moderately a bubble. Overall, the responses suggest that while many participants acknowledge signs of unsustainable levels of demand and development, most do not currently see the risk as extreme.

To What Extent Do You Think That Power and Energy Availability will Limit Future Growth in U.S. Industrial, Manufacturing, and Data Center Development?

Source: RCLCO

Respondents largely view power and energy availability as a meaningful constraint on future growth across U.S. industrial, manufacturing, and data center development. 34% percent of respondents characterize factors as moderately limiting, with nearly as many (32%) citing them as very limiting; 27% consider them only slightly limiting, and only a small minority believe these constraints are not limiting at all. The distribution suggests broad agreement that power and energy availability are no longer peripheral considerations, but rather central factors shaping the pace and feasibility of future development in these sectors.

In combination, the responses around data centers point to a market that is expanding rapidly but constrained by real-world limits. While many respondents see signs of overextension in data center demand, concern is measured rather than alarmist, and views on power and energy availability suggest that infrastructure constraints, rather than demand alone, are likely to be a defining factor shaping the sector’s growth trajectory.

Return to Growth Mode in 2026?

By Year-End 2025, sentiment across land uses reflects a market that remains selectively challenged rather than uniformly distressed. Several for-sale residential segments, including land, condominiums, and resort/second homes, continue to be viewed as operating in downturn phases, underscoring ongoing affordability constraints and sensitivity to mortgage rates. In contrast, some rental residential sectors have demonstrated comparatively greater resilience, with age-restricted and seniors housing in particular being predominantly characterized as stable or recovering amid demographic tailwinds and steady demand.

Within the commercial landscape, sentiment remains divergent across land uses. Regional malls and Class B/C offices continue to be viewed as firmly entrenched in downturn conditions, while grocery-anchored/lifestyle retail, industrial, and hospitality are more commonly positioned in stable or late-stable phases of the cycle. Looking ahead, respondents anticipate gradual improvement across most land uses over the next 12 months, with future expectations shifting modestly toward recovery and stability even where current conditions remain constrained. Collectively, the results suggest a market still working through cyclical challenges today, but with growing confidence that conditions may improve incrementally rather than move deeper into distress.

Land Use Cycle Stage Today and Looking Ahead 12 Months

Signs of Relief: Selective Improvement Ahead

When asked what they expect to happen with a set of key economic indicators over the next 6 to 12 months nationally, respondents generally point to a market anticipating some easing in financial conditions while continuing to grapple with operational constraints. Improvements in rates and capital availability are tempered by ongoing challenges related to costs, labor availability, and housing dynamics, suggesting selective improvement rather than a full return to favorable market conditions.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

- Interest rate expectations lean decisively toward easing in the next 6-12 months, with 77% of respondents anticipating a moderate decrease. This marks a departure from mid-year 2025, when expectations for interest rates to remain stable and for rates to decline were evenly balanced, at roughly 39% each.

- Predominant cap rate expectations did not majorly differ from those of Mid-Year 2025, in that 47% of respondents anticipate conditions to remain the same. Year-End 2025 expectations do favor moderate rate decreases over increases by a margin of roughly 10 percentage points, which is a slight departure from the evenly split outlook at Mid-Year 2025.

- Sentiment regarding capital flows to real estate clusters around both expansion and stasis, with 45% of respondents anticipating a moderate increase and 34% expecting no change, similar to sentiment at mid-year.

- Consistent with Mid-Year 2025 sentiment, most respondents do not expect the homeownership rate to improve in the next 6-12 months; 33% foresee a moderate decline and 44% expect the rate to remain unchanged.

- Equal shares of respondents expect inflation to remain unchanged (39%) or increase moderately (39%), with a smaller but notable group (16.04%) anticipating a moderate decrease.

- Respondents largely expect construction costs to continue rising. Nearly half (49%) anticipate a moderate increase, with an additional 6% expecting a significant increase, reaffirming continued pressure on development feasibility.

- Expectations for labor availability remain consistent with mid-year sentiment, with the largest share of respondents (43%) continuing to anticipate a moderate decrease.

Because it has a big impact on real estate valuation and debt costs, where do you think the 10-year treasury will be 24 months from now?

Source: RCLCO

Expectations for the 10-year Treasury 24 months out are concentrated in a relatively narrow range; the largest share of respondents (42%) expect the yield to settle between 3.5% and 4.0%, while about half as many expect rates to remain clustered in the 4.0%–4.5% range. Far fewer respondents (~4%) anticipate outcomes at the extremes, either below 3.0% or above 5.0%. Taken together, the responses suggest that most participants expect long-term rates to ease from recent levels but remain structurally elevated relative to the pre-pandemic period.

RCLCO POV

Q4 2025 – Moderate Growth Expected to Continue in 2026

Inflation and growth have cooled compared to 2022-2024 and the Fed has begun easing (policy rate trimmed another 25 bps in Dec 2025), which has contributed to improved financing sentiment and liquidity for real-estate investors, but financing costs remain above pre-pandemic norms. In recent quarters, macroeconomic forces and administration policies have caused uncertainty and stress in the real estate industry. After an extended period of elevated vacancy rates and tightening financing conditions, signs of stabilization have begun to emerge, with increased investor interest in select property types such as data centers, industrial/logistics, and, yes, office. Key risk factors to monitor include interest rate policy surprises – particularly slower-than-expected easing or renewed hawkishness if inflation increases; macroeconomic growth slowing that puts a dent in leasing, travel, and consumer expenditures; and localized supply-demand imbalances in selected sectors/markets (especially multifamily and industrial as deliveries begin to taper).

Despite recent economic and geopolitical uncertainty, the overall U.S. economy has remained relatively stable, with consumer spending, business investment, and capital markets activity continuing at sustainable levels. This stability has supported moderate overall economic growth and steady real estate activity throughout 2025, even as certain sectors have experienced uneven performance:

- Industrial/Logistics: Healthy demand with some weakness at port markets; growth moderates as new supply completes. Premium modern stock favored; secondary stock faces rising vacancy.

- Multifamily: Rent growth slowing; fundamentals stabilize as deliveries taper. NOI growth moderate; top-market/value-add opportunities attractive.

- Office: Weakest sector; gradual stabilization for prime, amenity-rich assets. Secondary/tertiary towers remain distressed.

- Retail: Bifurcated recovery; grocery-anchored/experiential strong; weaker corridors remain challenged.

- Hospitality: Recovery led by leisure and gateway markets; sensitive to consumer spending.

- Niche: Strong demand for data centers, self-storage, and senior housing; life sciences overbuilt.

Taken together, the current environment points to a potentially attractive period for disciplined acquisitions. Investment decisions should be grounded in conservative underwriting assumptions, including slower rent growth and tighter exit cap rates. Portfolio strategy should emphasize operational resilience and institutional-quality assets that can perform through modest volatility, while capital structures favor shorter debt maturities and flexible refinancing options. Ongoing monitoring of macroeconomic conditions, interest rates, and localized supply-demand dynamics will be essential to navigating near-term risks and preserving downside protection while positioning for the next phase of the cycle. Despite elevated uncertainty, we expect 2026 to bring improved real estate opportunities and activity, supported by strengthening property fundamentals and more constructive capital markets.

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and industry. A majority (75%) of respondents have worked in the real estate industry for 20 years or more, with an average respondent tenure of approximately 25 years. Moreover, 87% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Type of Organization

Source: RCLCO

Developers and builders represent the largest share of respondents at 44% of the sample. Another 22% are investors or capital allocators, followed by nearly 7% in design or architecture firms. The remaining 28% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Primary Region/Market

Source: RCLCO

The respondent base spans a broad geographic footprint, with the largest share (15.65%) identifying the primary focus of their role as national in scope. Beyond that, regional representation is strongest in growth markets, particularly the Sunbelt.

Sentiment Survey article and research prepared by Charles Hewlett, Managing Director; Kelly Mangold, Principal; and Kaity Molito, Associate

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Copyright ©️ 2025 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.