November 25, 2020

In this article, we examine some of the housing market influences of the coronavirus pandemic in the context of a strong housing market and consider which trends are truly related to the pandemic as opposed to being more a continuation of established patterns. We are certainly experiencing a robust single-family housing market (both new and resale), and much of the activity is in the suburbs. Rental housing occupancies and rent growth have also been stronger recently in some suburban market areas as compared to urban areas. Do these trends represent a significant shift in market preferences for the suburbs?

Key Points Discussed in this Article

- We’re currently experiencing some of the strongest new home sales activity since the mid-2000s; how long with this last?

- While fear of Covid-19 has been a motivating factor behind some moves this year, high demand for new homes appears to be an acceleration of longer-term trends, not an entirely new trend.

- The strong housing market is being driven by historically low-interest rates and longer-term demographic trends.

- The Covid-19 crisis has likely influenced some buyers to move sooner than they might have otherwise and caused some younger renters to double up or move home.

- The increase in teleworking, home learning, and desire to keep more provisions on hand, is altering how and where some households choose to live and work, and homebuilders are responding.

- Many of the most “moved out of cities” this past year are also among the most expensive places to live.

New home sales activity in January and February of this year quickly surpassed levels experienced in late 2019, and despite a brief pause due to the coronavirus shutdowns in March and April, the resumption of strong new home sales over the summer represent some of the strongest new home sales activity since the mid-2000s. RCLCO’s mid-year report on the Top-Selling Master-Planned Communities shows MPC’s having some of their best years in terms of sales ever. It’s hard to say exactly how much of this activity is related to a Covid-19 induced “flight to the suburbs” versus trends that were already underway, but there is evidence that the pandemic and the associated economic turbulence have had both short term and potentially longer-term influences on the housing market.

It’s been surprising to many that high demand for new homes is occurring in the midst of a global pandemic. In some respects, this strong demand is an acceleration of longer-term trends, rather than an entirely new trend. While it’s true that the pandemic has motivated many people to move this past year, our 2016 report published with the Urban Land Institute, Housing in the Evolving American Suburb, found that suburban growth has been responsible for driving metropolitan growth for many years. That report concluded that following the Great Financial Crisis, the suburbs are where the majority of new household growth occurred, and where employment growth was the greatest.

More recently the impact of housing preferences influenced by the coronavirus appears to have at least temporarily accelerated growth in the suburbs that was already being driven by historically low-interest rates and long-term demographic shifts.

For many home buyers the pandemic has created economic and lifestyle changes that have influenced people to make moves sooner than they otherwise may have:

- Working and learning remotely

- Not being able to capitalize on urban amenities due to partial or complete shutdowns, and the need for social distancing, have made living in urban areas temporarily less important for many people

- Having the home transformed from a place they spend some of their time, to a place they most of their time, with a greater need for home offices, homeschooling, home exercise, etc. has accelerated many households’ desires for more space or at least differently configured space.

- Tight resale and new home inventories are keeping prices high, impacting for-sale housing affordability, and many households seeking more space are reportedly finding the suburbs (and exurbs) are where they can afford that new or resale house.

- Working from home means commute times are a less significant factor, it’s been reported that people are looking further out from job centers for more space and greater affordability.

Long-term demographic shifts are of course playing a role in a renewed demand for single-family homes, both for for-sale and for-rent. For years new Millennial household formations had been inhibited by DAS (Delayed Adult Syndrome), with young potential householders living at home, delaying marriage and kids to later in life, due to higher student debt and other factors. Despite high unemployment in some sectors of the economy many of those Millennials now in their mid to late 30’s, especially those with some accumulated savings, and at a stage in life where people often move toward single-family housing and homeownership, have been more active in the housing market. Of course, rising Covid-19 cases and potential shutdowns early next year could put a pause on that activity. That remains to be seen but the potential is there, although long-term fundamentals look good.

Much has been made of the change of address data collected from the United States Postal Service (USPS) indicating that slightly more people moved in the first half of 2020 than in 2019, with some suggesting this shows an exodus from urban areas likely due to the coronavirus pandemic. It’s true that the change of address requests increased year over year by about 3.9%. A moving services website, MyMove.com, prepared a report summarizing these data, suggesting there is a substantial movement of households fleeing cities for the suburbs. The data show the most significant increase in change of address requests was among those requesting a temporary change. If there is a substantial flight from cities we’d expect the data to show a sustained increase in changes-of-address in 2020 as compared to 2019, but what the data show (so far) is a spike in the first months of the coronavirus pandemic, followed by a decline in May and June compared to the same months in 2019. While it appears likely that the pandemic has accelerated some moves, we’ll need year-end data to truly know how much of an increase there’s been overall.

In a survey conducted by the Pew Research Center, many people said fear of Covid-19 was a motivating factor behind their move this year, and for younger households, college closures and financial reasons such as job loss were more frequently mentioned. Since Covid-19 spreads from person to person there has been some fear of density, and it’s been suggested that is part of the reason for the exodus from cities such as New York to the surrounding suburbs. According to the USPS move data, larger cities lost the most movers (in absolute numbers) during the first half of 2020. This includes areas such as Manhattan, Brooklyn, Chicago, and San Francisco. But people move out of big cities all the time, and migration from New York City for example is a long-term trend. Many of the most “moved out of cities” this past year are also among the most expensive places to live, so moves may be motivated as much by low affordability as fear of Covid-19.

With the above in mind, we are cautious about using these reported short term move trends to infer long term trends, particularly given demographic shifts already influencing suburban demand, including growth in households headed by people in their mid-thirties to mid-forties, age ranges where people often are in the life stage where they’ve outgrown apartment living and seek a single-family home in the suburbs. According to Zillow, about 64% of the users on its website are looking at suburban areas, which is similar to what it’s been in 2019 and 2018. At the beginning of the summer (June 2020) Zillow data showed more people looking at larger homes as compared to a year earlier, which lends credence to the idea that families cooped up together as a result of the pandemic are seeking more space. While it’s true that for-sale suburban homes attract more traffic on Zillow than urban listings do, that was already the case in 2019 pre-pandemic. Interest in detached single-family homes on Zillow has not seen a marked increase compared to previous years.

Some of the influences of the coronavirus pandemic on the housing market may be too subtle to show up dramatically in the data. We believe that the strong housing market is more the result of historically low-interest rates and longer-term demographic trends, though the Covid-19 crisis may have influenced buyers to move sooner than they might have otherwise, while also temporarily causing some younger renters to double up or move home.

New Home Sales, 2019-2020

Source: U.S. Census

As shown on the chart above sales of new single-family homes are well up over the 2019 pace, although the increase in year over year pace that began in May leveled off in the late summer and fall. Sales of new single-family houses in October 2020 were at a seasonally adjusted annual rate of 999,000, according to estimates released jointly on November 25, 2020, by the U.S. Census Bureau and the Department of Housing and Urban Development. Strong housing demand, and low housing supply, are impacting affordability, although historically low-interest rates continue to drive demand. Regionally, the greatest growth in activity has been in the South, followed by the West, with at least half of the activity in lower-density suburban areas.

2020 New Home Sales by Region

Source: U.S. Census

While single-family homes in the suburbs have been in high demand, suburban rents are also growing, while growth in urban rents and occupancies have not been as strong overall. Some have suggested that this also reflects a substantial shift away from cities.

- In a survey conducted by Pew Research Center earlier this year about 3% of U.S. adults said they moved permanently or temporarily due to the pandemic, and young adults were the most likely to say they’d moved, with 9% of those aged 18 to 29 saying they’d moved due to the coronavirus outbreak.

- Economically related moves due to the coronavirus have had an impact on urban rental housing markets, with suburban rent growth surpassing that of many urban areas, but other factors, such as higher absolute rents in urban areas (affordability) and the pace of urban apartment deliveries are also at play.

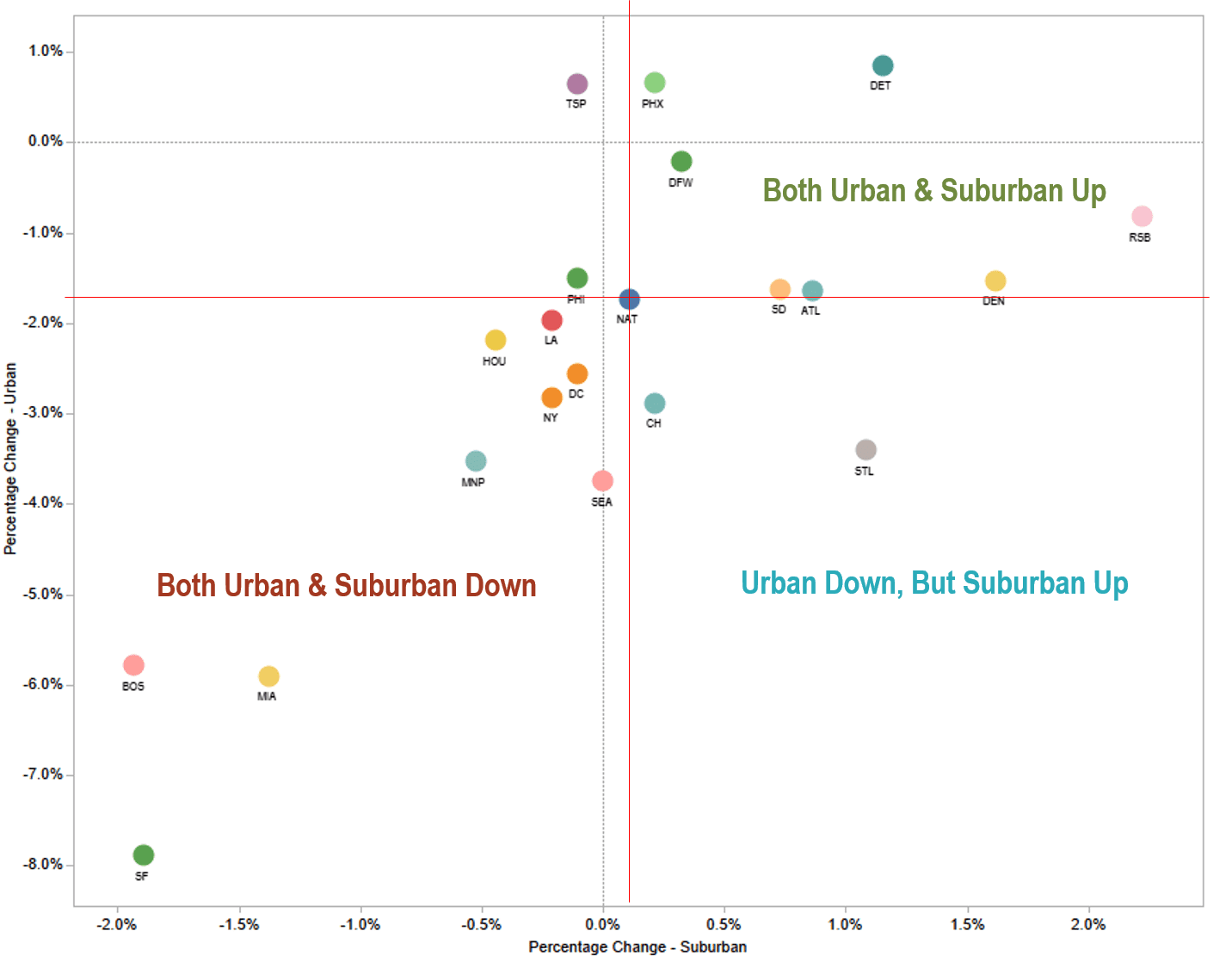

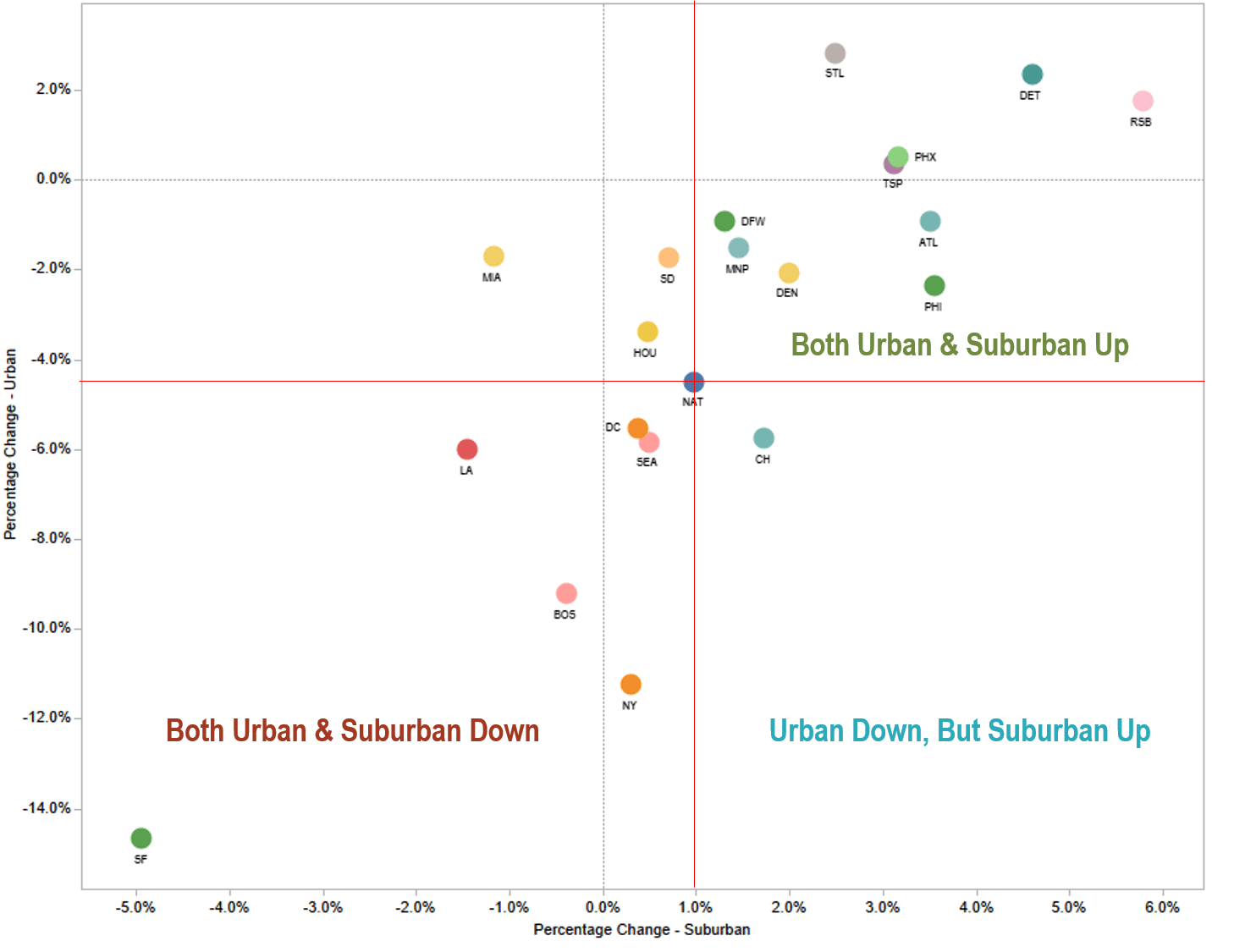

- When we look at the data across many different markets, what we see is that rental housing rent growth and vacancy trends vary from one location to another. What the data actually show is that in some markets, both urban and suburban occupancies and rents are up, while in other markets urban occupancies and rents are down, but the suburbs are performing better.

Our analysis indicates caution is called for in interpreting the data as representing a single trend of “flight from urban areas”. There may indeed be a flight from high-cost coastal markets but that may be due as much to economic conditions and affordability as the pandemic, and it does not appear to be a universal trend.

Top 20 Rental Apartment Markets % Change in Occupancy, Urban vs. Suburban

Source: RCLCO Real Estate Advisors

Top 20 Rental Apartment Markets % Change in Rents, Urban vs. Suburban

Source: RCLCO Real Estate Advisors

Many younger renters who have been impacted by job losses or colleges and universities switching to remote learning have moved back home with mom and dad. In fact, age 18-to-29-year old’s living at home is at the highest levels since the Great Depression era. Much of that increase is among the youngest adults, not those older Millennials who are already active in the for-sale housing market. Historically periods of higher population growth relative to household growth negatively impact housing demand, but when the conditions inhibiting household growth are mitigated, pent-up demand may result. Once there is a vaccine, colleges and universities reopen, and job growth strengthens, urban rental housing markets should strengthen again.

Substantial new rental apartment activity over the past several years has been focused on urban locations, and it’s likely that the weaker rent growth and lower occupancy growth in urban areas have as much or more to do with the higher absolute urban rents as well as the pace of urban versus suburban deliveries, as the coronavirus pandemic. There has been much higher inventory growth in many urban areas for years, and that has inhibited rent growth in those markets and kept occupancies lower than in suburban apartment markets.

Historically urban core area real estate has seen much stronger value appreciation than the suburbs, although residential price growth has been more similar this past year. Once there are wide distribution and adoption of an effective vaccine(s) and people are once again confident in patronizing restaurants, theaters, and other cultural amenities, it’s likely that closer-in urban and urbanizing suburban locations will once again be able to command a premium. Many people are willing to pay a premium to be close to cultural amenities and live in walkable neighborhoods, more so when they can actually take advantage of those amenities.

The growing demand for single-family rental housing, filling in some of the affordable housing gap, is likely a long-term trend. While monthly costs to rent versus own may not make single-family rental homes appear that much more affordable than their for-sale counterparts, the fact that they don’t require tying up significant savings in a down payment is a big deal for many households.

Builders are responding to the current housing boom with new home layouts better suited for households living through a pandemic. New homes that better accommodate working from home, with built-in desks, better noise insulation, enhanced lighting, pre-wired Wi-Fi, built-in USB chargers, exterior entrances, and dual office set-ups are increasingly common. Home learning is also being better incorporated into new home designs, with “learn-in” kids’ bedrooms, school room loft designs, and basement study halls being offered as options. While many gyms remain shut down or only partially open, builders are offering dedicated space for at-home workouts, in the house, garage, or basement. Some plans offer larger pantry spaces to reflect the fact that households want to keep more provisions on hand than in the past. Outdoor environments for socially distanced gatherings, such as extended screened decks, enhanced patios, and porches are similarly attractive options.

Although we’re obviously concerned about rising Covid-19 cases nationally and the potential for temporary shutdowns in the next several months, underlying economic and demographic fundamentals have indicated that we should expect a strong 2021 new home market as long as interest rates remain low, and home prices stay in reach of homebuyers. Meanwhile, the rental housing market may see an uptick in activity in a post-covid economy as the rate of new household formations gets back to normal among younger households, many of whom have been more negatively impacted by Covid-19 related layoffs and college closings as compared to older households.

We all hope that once vaccines are readily available and implemented we’ll all be able to get back to “normal life”. However, it’s likely that at least some of the changes brought on by the pandemic will last, with an increase in teleworking, home learning, and desire to keep more provisions on hand being responsible for evolving, if not dramatic, changes to how and where we live.

Article and research prepared by Gregg Logan, Managing Director.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.