October 9, 2025

By Eric Willett, Managing Director; Kelsey Padgham, Vice President; Isaac Gershberg, Associate

CRE C-Suite Outlook

The commercial real estate industry is navigating an environment marked by capital scarcity, evolving risk appetites, and shifting operating models. To bring some clarity to this moment, RCLCO Management Consulting launched its inaugural CRE C-Suite Outlook, a survey designed to surface the trends shaping the strategic agendas of real estate leaders across the United States.

The survey responses deliver a collective snapshot of how the industry’s senior decision-makers are thinking about capital, talent, innovation, organizational structure, and risk. The results serve as both a benchmark and a sounding board for executives seeking to evaluate their strategies against broader industry dynamics.

This report synthesizes insights from 80+ survey respondents who currently hold senior leadership roles at CRE firms that, combined, represent a reported $39 billion dollars in real estate investment volume in 2024. RCLCO also conducted follow-up interviews with participants to gather additional feedback on survey themes. Our hope is that findings from the CRE C-Suite Outlook help inform boardroom conversations, capital planning, and long-term vision-setting across the real estate landscape.

Key Takeaways

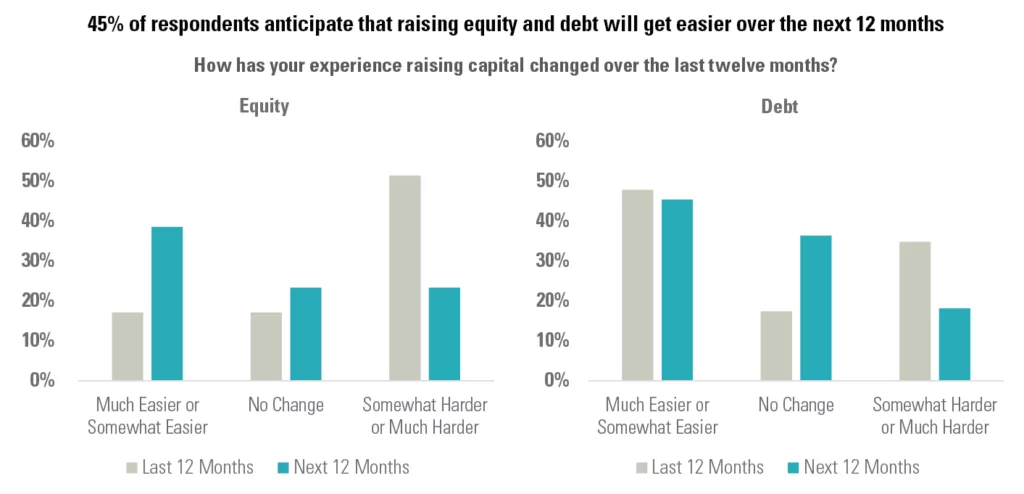

- Capital Markets: Sixty percent of executives report tougher equity raises and one-third see harder debt conditions than last year, yet nearly half expect ease of fundraising to improve in the next year as sentiment surveys point to gradual market stabilization

- Investment Strategy: Average development allocations dropped from 60% to 54% in 2025 while core/core-plus and value-add acquisitions rose, reflecting high construction costs and a shift toward buying assets as pricing for many segments remains at or below replacement cost

- Profit Margins: Two-thirds of firms maintain operating margins above 10%, but 39% experienced year-over-year compression as rising operating costs and slower deal flow erode profits

- Team Continuity and Retention: Nearly three-quarters of executives report stable or improving ability to attract and retain talent, and most focus on developing existing leaders rather than external hiring amid tight budgets and cautiousness around headcount expansion

- M&A and Ownership Changes: Close to 60% of companies say a merger or acquisition is somewhat or very likely within 12–18 months, with many eyeing new investors or ownership changes to gain scale and liquidity

- Technology: Roughly 90% of firms are testing AI tools, concentrating first on property management, underwriting, and other high-volume functions while broader integration remains in pilot stages

Capital Markets: Scarcity Persists, with Signs of Thaw

Raising capital over the past year remained a grind for most real estate firms, with equity proving especially difficult. Sixty percent of executives said sourcing equity was harder than a year ago, and 40% described it as “much harder.” Only 20% experienced any easing in their access to equity capital. Debt capital was a somewhat different story: while the lending environment was far from easy, it showed more balance. Roughly one-third of respondents said borrowing had become somewhat or much easier, but an almost equal share experienced greater difficulty or no change.

“Equity capital raising? We’ve been in the desert for three years.”

CEO | Vertically Integrated Multifamily Developer

The view forward is cautiously more upbeat. Nearly half of respondents (45%) expect equity fundraising to become somewhat easier in the next twelve months, while about one-third (27%) still anticipate further tightening. Expectations for debt are similarly constructive: about 45% foresee easier borrowing conditions in the year ahead, while only 19% predict that debt markets will become more challenging. Together these figures suggest that while capital remains scarce today, CRE executives sense that the worst of the dislocation may be past.

This cautious optimism echoes RCLCO’s Mid-Year 2025 Real Estate Sentiment Survey, which found that overall market sentiment, while softening, points to gradual improvement ahead. The RCLCO Real Estate Market Index (RMI) fell back to 37 at mid-year after a year-end bounce, yet the Future RMI is projected to rise to 50 within the next 12 months, signaling expectations for a slow return to expansion despite current uncertainty. In that survey, 40% of respondents predicted moderately or significantly better conditions over the next year, roughly matching the share who anticipated continued weakness, highlighting a market that is stabilizing but still feeling the effects of elevated rates and geopolitical tension.

Where firms find their equity underscores the importance of trusted networks, especially as certain segments of the capital landscape are less active. High-net-worth individuals and family offices are the dominant source of new capital supporting recent investments, cited by 73% of respondents and reflecting their relative resilience and willingness to invest through cycles. Half of companies also tap pension funds or endowments, and more than one-third are funding projects solely with internal capital.

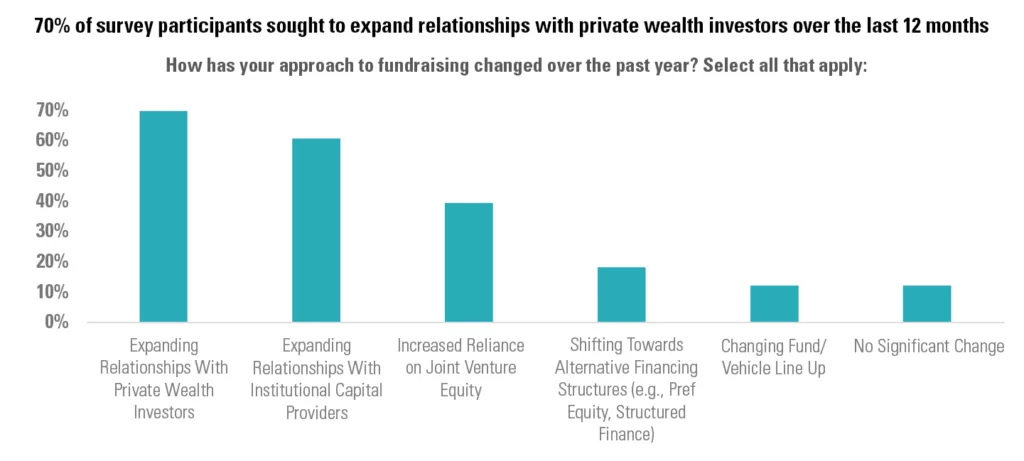

Fundraising tactics have evolved to match the environment. Seven in ten firms expanded relationships with private-wealth investors over the past year, and six in ten deepened ties to institutional capital providers. The secular rise of private equity and real asset investing among HNWIs has been a tailwind for the CRE space, and the survey data highlight the investments groups are making in tapping into this growing segment. Said one CEO, “We value the discretion that our HNWIs offer, and we’re proud of the investor pool we’ve cultivated. It’s a focus of ours to continue expanding our private capital relationships.” Nearly 40% increased their reliance on joint-venture equity, and roughly one-fifth experimented with alternative structures such as preferred equity or structured finance. Very few reported shrinking investor relationships or reducing their JV activity, reflecting an industry bias toward broadening capital relationships, regardless of target investor type.

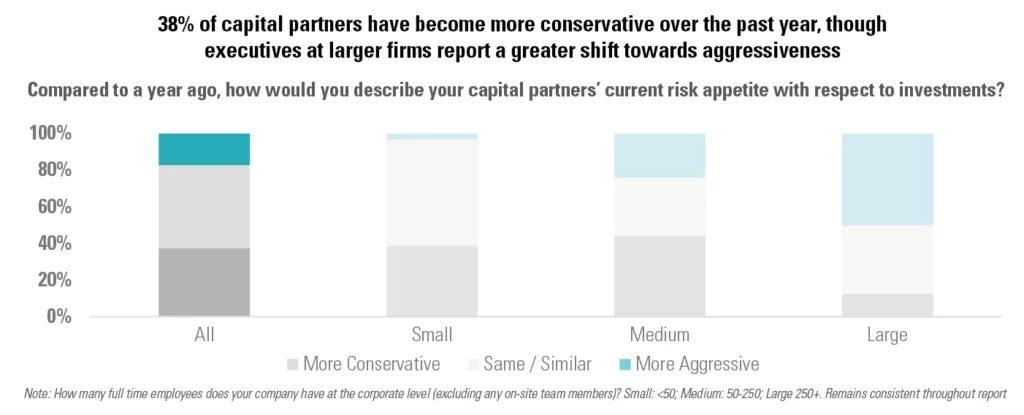

Executives also report a measured stance from their capital partners. Almost half perceive investor risk appetite as unchanged, while 38% say partners have become more conservative and only 17% see a shift toward greater aggressiveness. This aligns with the broader narrative of a market that remains disciplined and selective even as it begins to thaw. As one executive explained, “Investors are still showing up, but they’re asking tougher questions and want to see us prove the downside is protected before they commit.”

Notably, these patterns hold across company size and business model. Whether small, mid-sized, or large, firms are encountering similar obstacles and expressing comparable optimism for modest improvement ahead.

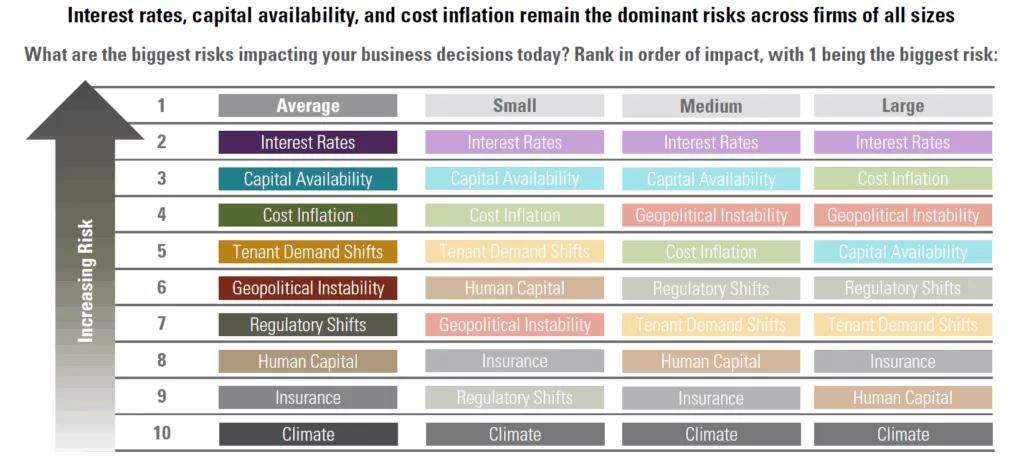

That cautious capital markets optimism is shaped by a clear hierarchy of risks. When asked to rank the forces most affecting their decisions today, executives placed interest-rate volatility at the top, followed closely by capital availability and cost inflation. The paramount focus on elevated interest rates was undoubtedly influenced by the challenging macroeconomic environment faced by the Federal Reserve throughout 2025 to-date as it navigates deteriorating labor market conditions and sustained, elevated inflation. Anticipation for cuts in the Federal Funds rate (ultimately realized in September) was top of mind for the executive respondents looking for signs of the market “opening back up.”

Tenant-demand shifts and geopolitical instability formed a secondary tier of concern, while regulatory changes and human-capital issues trailed further back. Climate risk ranked lowest. These priorities cut across company sizes and margin profiles, underscoring that the capital discipline evident in the market is grounded in broad macroeconomic pressures rather than firm-specific challenges.

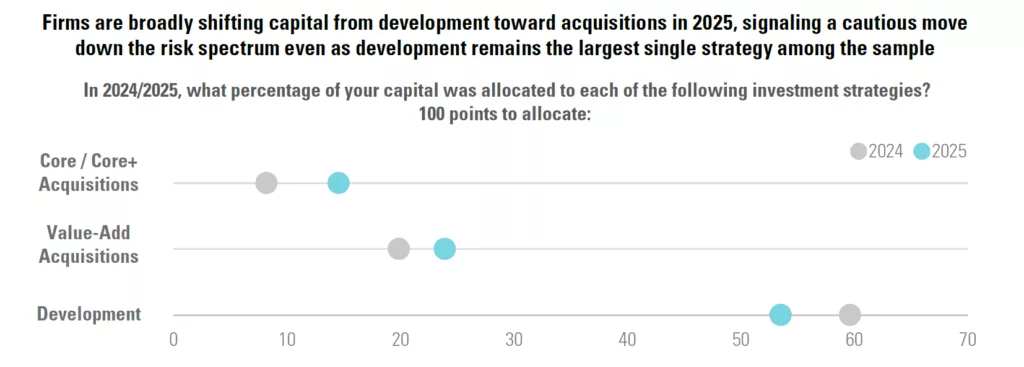

Investment Strategy: Development Leads, but Acquisitions Are Gaining Ground

Survey data reveal a market that is slowly re-opening to acquisitions while ground-up development remains historically difficult. In 2024 respondents devoted an average of 60% of their capital to development, reflecting the survey group’s historical focus on development activity. But that share is projected to drop to roughly 54% in 2025, while core/core-plus acquisitions rise to 15% and value-add climbs to about 24%.

This reallocation is not just a tactical tweak; it reflects today’s macro reality. With construction loans expensive and economic uncertainty still high, ground-up development carries outsized risk. Even well-capitalized groups acknowledge that starting a new project in this environment is challenging, which has slowed development activity across the market despite many groups maintaining conviction in the long-term opportunity.

At the same time, pricing dynamics have shifted. Survey participants highlighted recent transactions demonstrating that some assets can now be purchased below replacement cost or even at distressed prices. These conditions allow investors to buy high-quality, stabilized (“core” or “core-plus”) properties at discounts that can deliver value-add-level returns, the kind of upside that typically requires heavy renovation or redevelopment. As one respondent explained in a follow-up interview, “We’re buying core-plus assets today at prices where we can achieve the same returns we used to underwrite for value-add plays.”

The result is a broad move “down the risk spectrum.” Instead of pursuing riskier ground-up development, many firms are channeling more capital into acquisitions where they can earn attractive returns with less execution risk.

These shifts cut across company size and business model, signaling an industry-wide recalibration.

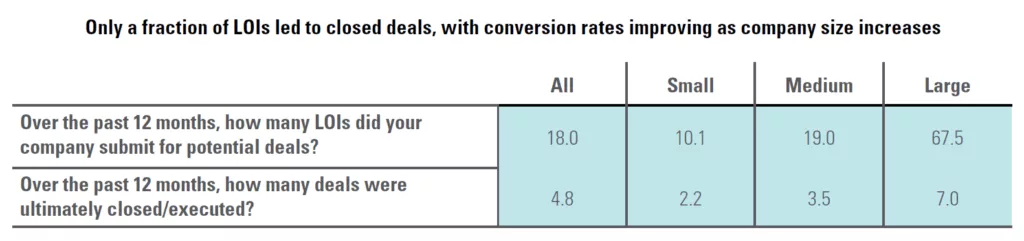

In terms of transaction activity, across the sample, companies submitted an average of 18 letters of intent over the past year but closed fewer than five transactions. Large operators were more active, submitting dozens of LOIs and closing several deals, while smaller and mid-sized firms pursued only a handful of prospects. The gap between offers and closings highlights both the competitive nature of the market and the strict underwriting discipline that has characterized this cycle, reinforcing how challenging it remains to convert acquisition opportunities into executed deals even as pricing adjusts.

The survey signals a modest shift, but not a full pivot. The developer-heavy sample set still allocates most capital to new construction, but national data show development starts at multi-year lows and financing costs remain high. Viewed against that backdrop, these results reflect cautious diversification more than renewed development momentum.

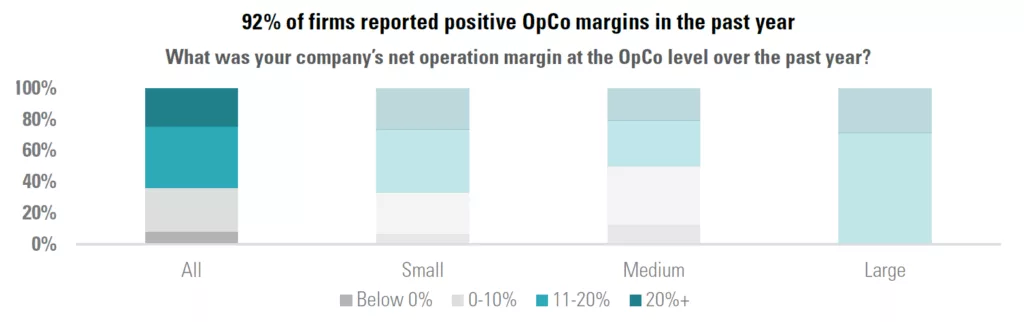

Profit Margins: Resilient but Under Pressure

Operating profitability across companies remains generally healthy, but signs of strain are present. Two-thirds of respondents reported net operating margins above 10% in 2024, with the largest single group (39%) falling in the 11–20% range and another 25% earning margins above 20%. A small minority, 8%, operated below breakeven, underscoring that most firms are still running profitable core businesses despite a challenging capital environment and decreased investment activity.

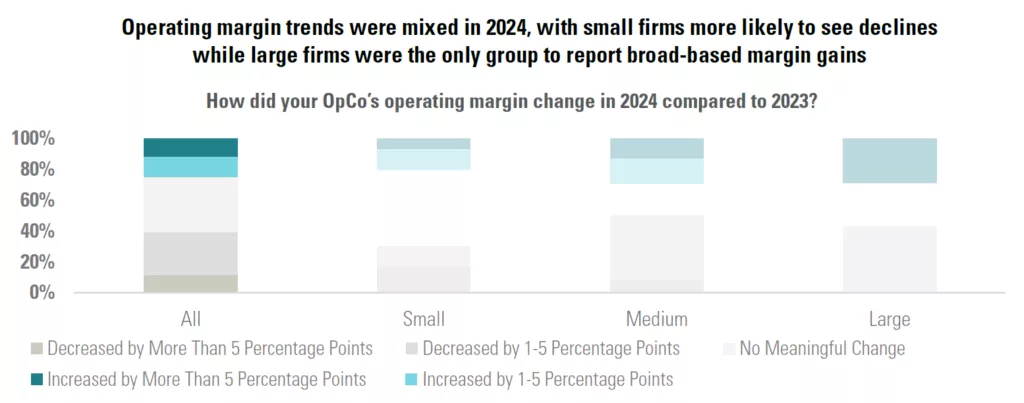

Year-over-year trends reveal a more cautious story. Thirty-nine percent of companies experienced operating margin compression compared with 2023, including 11% that saw declines of more than five percentage points. By contrast, only about a quarter reported any improvement, and 11% achieved gains greater than five points. The remainder, roughly one-third, reported no meaningful change. This pattern suggests that while firms have maintained profitability, rising costs and slower transaction activity are beginning to erode operating profits. As one CFO explained, “We’re still making money, but every deal takes longer and every expense line is higher… Holding margins flat feels like a win right now.”

Overall, operating companies remain profitable, but many are absorbing cost pressures and reduced fee income that narrow the cushion. Maintaining current margins, or even a modest decline, appears to be the baseline expectation as executives wait for clearer signals of sustained market recovery.

Team Continuity and Retention: Stability First, Evolution Where Needed

Despite a turbulent capital environment, executive teams remain stable, with most firms focused on nurturing existing leadership rather than recruiting externally.

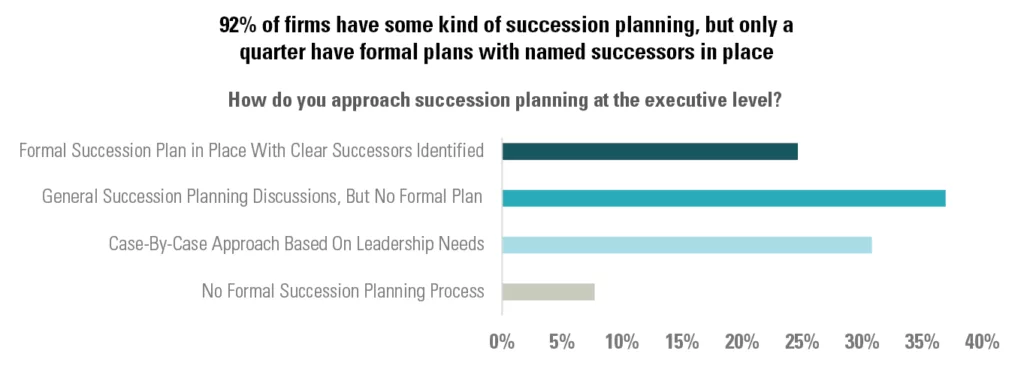

Succession planning illustrates this measured approach. Only one-quarter of respondents have a formal plan with named successors, while the majority rely on lighter frameworks: 37% have held informal discussions, and 31% address succession on a case-by-case basis. Just 8% report no planning at all. Many organizations appear to recognize the need for leadership continuity but are still maturing their succession planning processes. Formal succession planning remains a gap industry-wide, with some firms facing acute challenges as executives look toward retirement.

“Succession is keeping me up at night. We’ve relied on finding young people and training them up, but I need a successor and hiring senior talent is hard.”

President | Land Development Firm

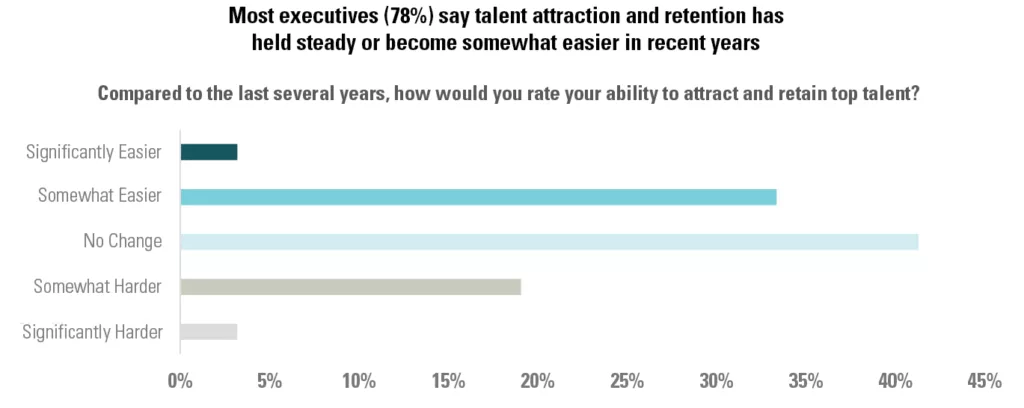

Talent conditions indicate an employer’s job market. Nearly three-quarters of executives say their ability to attract and retain top talent is unchanged or improving compared with recent years. One-third report that hiring has become somewhat easier, while only about one in five see greater difficulty. In a cycle defined by caution, the relative ease of retaining or hiring for key positions over the last few years reflects a marked shift from the pandemic period and has allowed firms to concentrate on growing internal talent while facing constraints on growth.

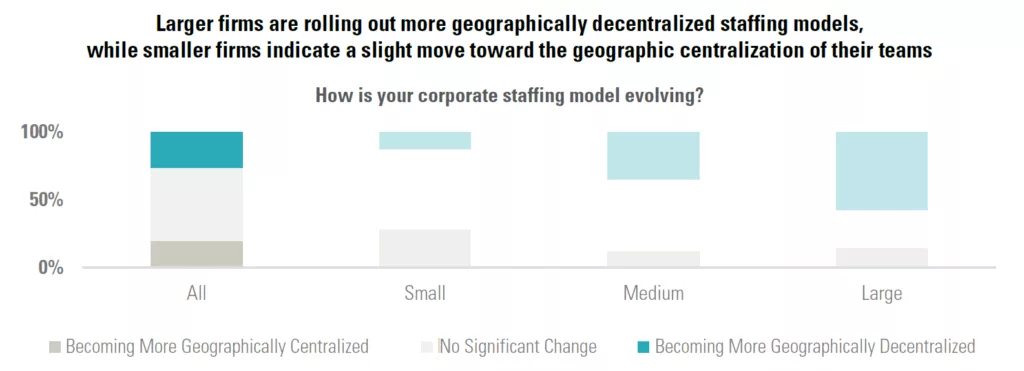

Corporate staffing remains steady overall, but over half of the firms making changes are moving toward a more distributed footprint. While 54% report no significant shift, the adjustments that are happening tilt toward decentralization: 26% are spreading functions across multiple markets versus 20% that are pulling teams back to headquarters. Larger platforms in particular are opting for a multi-market operating model, mirroring a wider real estate trend of regional hubs and satellite offices that bring decision-making closer to projects and talent pools.

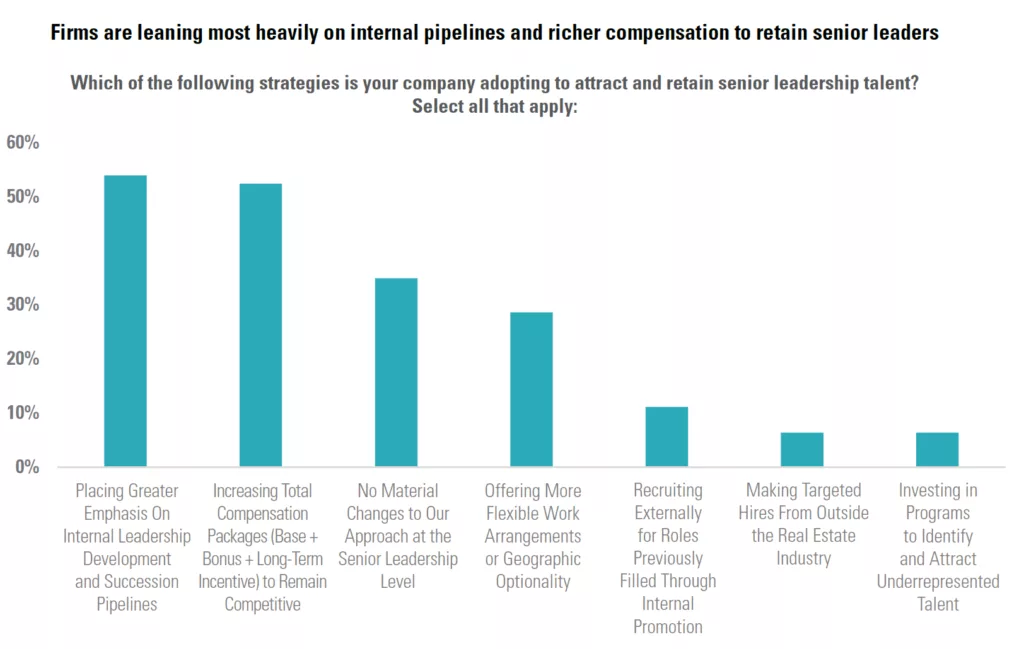

When it comes to attracting and retaining senior leaders, companies are relying on proven tools rather than radical moves. Internal leadership development and succession pipelines (54%) and enhanced total compensation packages (52%) top the list of retention strategies. Flexible work arrangements (29%) provide additional support even as the pandemic focus on remote work has waned.

In all, the data reveal talent strategies that prioritize continuity over disruption. Firms are shoring up existing teams, investing in internal growth, and making targeted structural adjustments. Rather than launching aggressive external searches, many leadership teams are concentrating on strengthening the bench they already have—in part because tighter capital markets and limited hiring budgets leave little room for big external hires. As one executive told us, “It’s not that we wouldn’t love to bring in new senior talent, it’s that every dollar is being scrutinized; we’re focusing on growing the people we’ve got.” The result is a cautious, inward-focused approach that preserves institutional knowledge while keeping organizations ready to scale when market conditions improve.

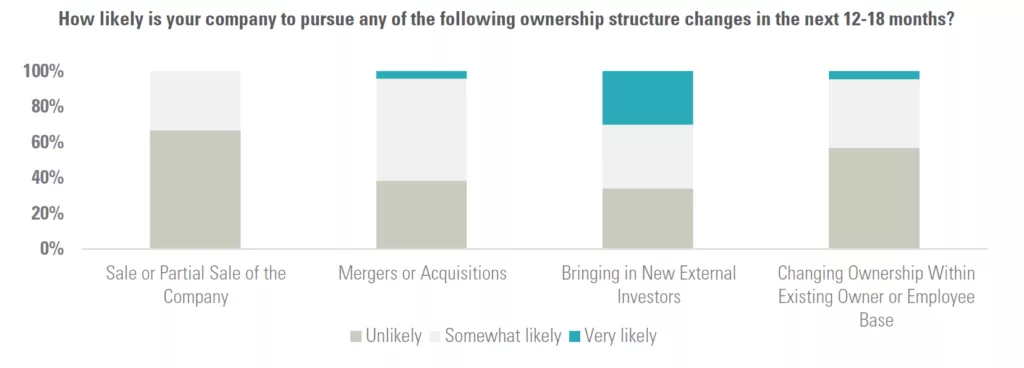

M&A and Ownership Changes: Interest Builds, but Execution Lags

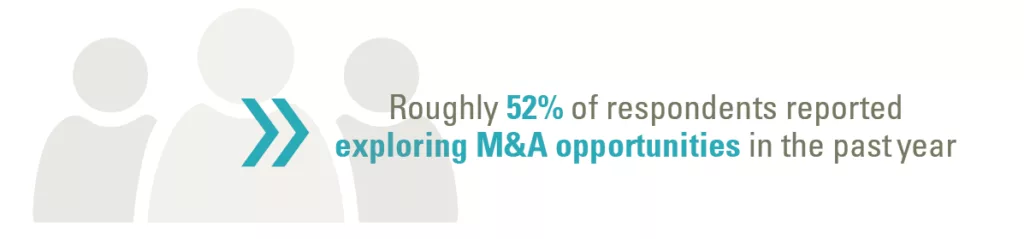

Commercial real estate firms are clearly thinking about inorganic growth, even if few have yet to act. Over the past year, nearly half of executives said they had at least considered a merger or acquisition, but the vast majority remain in the exploratory phase. Roughly one-third described their efforts as “somewhat” exploratory and another 17% as actively exploring, while almost half (48%) reported no activity at all. No respondent reported closing a transaction, underscoring that most of the movement so far has been preparatory rather than transactional.

The next 12 to 18 months may look different. Close to 60% of companies describe a merger or acquisition as somewhat or very likely, and about one-third say a partial or full sale of their company is at least somewhat likely. Appetite for new capital partners at the OpCo level is even broader: two-thirds of firms are at least somewhat likely to bring in new external investors, and roughly half are open to changing ownership within the existing employee or investor base. Interest in M&A and ownership changes is widespread across company sizes and performance profiles, suggesting that the industry is quietly preparing for a potential wave of partnerships and recapitalizations as firms respond to persistent capital scarcity, narrowing margins, and the recognition that scale and diversification may be necessary to weather prolonged uncertainty. One CEO stated, “At some point we expect that we’ll need new partners or a bigger platform to keep up.” With many platforms facing pressure to secure liquidity or attract fresh growth capital, consolidation is increasingly viewed not just as opportunistic, but as a defensive strategy.

Technology: Early Adoption, Growing Ambition

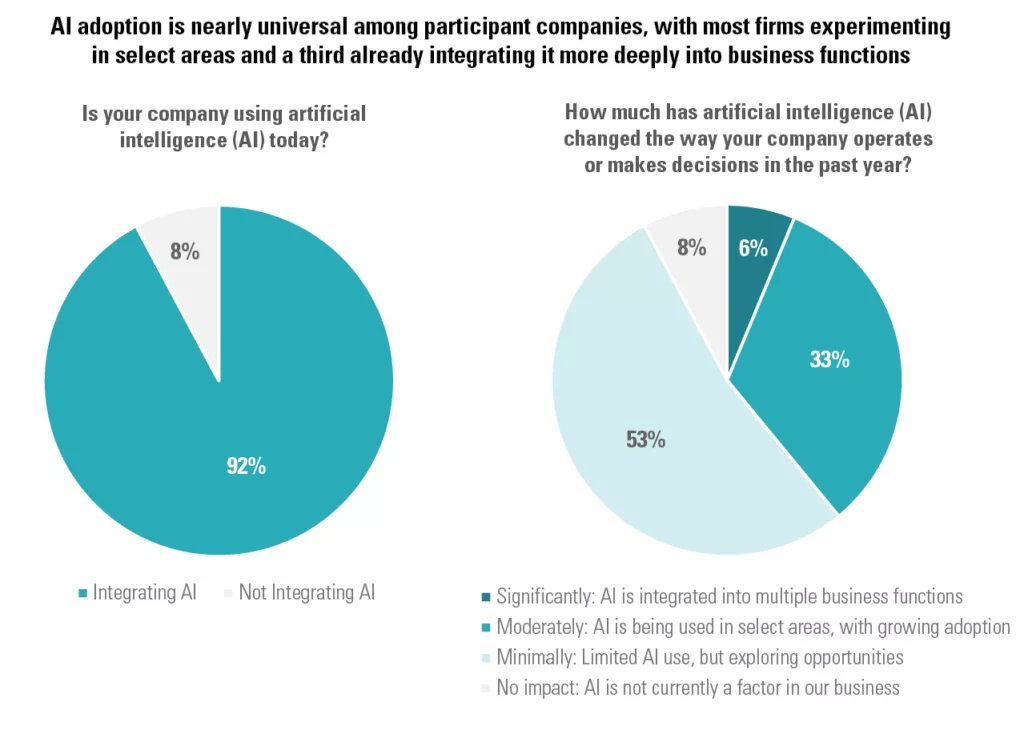

Commercial real estate firms are moving steadily toward technology-enabled operations. Artificial intelligence (AI) is at the center of the conversation, but broad deployment is still in its early stages.

Over the past year, nearly nine in ten companies report some level of AI activity, yet the depth of integration remains limited. Just 6% say AI is significantly embedded across multiple business functions. One-third describe moderate use in select areas with adoption expanding, while a majority (53%) are still experimenting and exploring opportunities. Only a small minority (8%) report no current AI impact. Alongside AI, firms are layering in complementary tools to support decision-making and reporting: 57% are actively integrating business intelligence (BI) platforms, and a handful are experimenting with blockchain or other emerging technologies.

“We’re focused on using AI and other tech to be more predictive in the business, especially as it relates to market selection.”

CIO | Vertically-Integrated Asset Manager

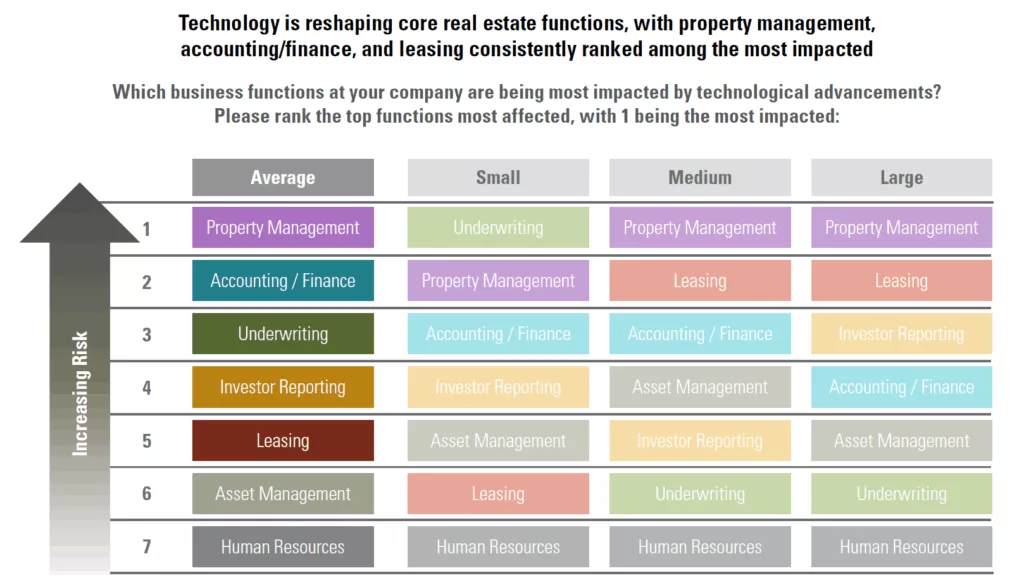

When asked where technology is having the greatest effect, property management ranks as the most impacted area, followed closely by accounting/finance, underwriting, investor reporting, and leasing. Human resources sits at the bottom of the list, underscoring that automation and data analytics are concentrating first where they can directly enhance revenue generation, risk management, and asset performance. This pattern may suggest that early adoption is focused on more repetitive, process-driven tasks, often those that are customer-facing or transactional, rather than functions tied to major strategic investment decisions.

Nearly every firm is testing AI or related analytics, but comprehensive transformation is still rare. Larger operators show somewhat greater momentum, with half reporting at least moderate AI adoption, yet the overall industry stance is deliberate: pilot projects today, broader rollout tomorrow. This measured approach allows companies to test efficiency gains and build institutional comfort while positioning themselves to scale technology adoption over time.

Continue the Conversation

RCLCO Management Consulting partners with owners, developers, and investors to translate market intelligence into actionable strategy. If you’d like to discuss these findings in the context of your own portfolio or strategy:

Stay Informed:

- Follow RCLCO on LinkedIn and subscribe to our newsletter for ongoing research and market commentary.

Explore More:

- Visit our website to learn how our advisory team helps clients navigate capital markets, organizational trans-formations, and strategic planning.

Appendix: Respondent Profiles

The findings in this report draw from a focused group of commercial real estate leaders, primarily operating in the United States and with a strong representation of CEOs, presidents, and senior investment officers.

Geography: Ninety-six percent of responses came from U.S.-based firms, with a small subset from Canada and Mexico.

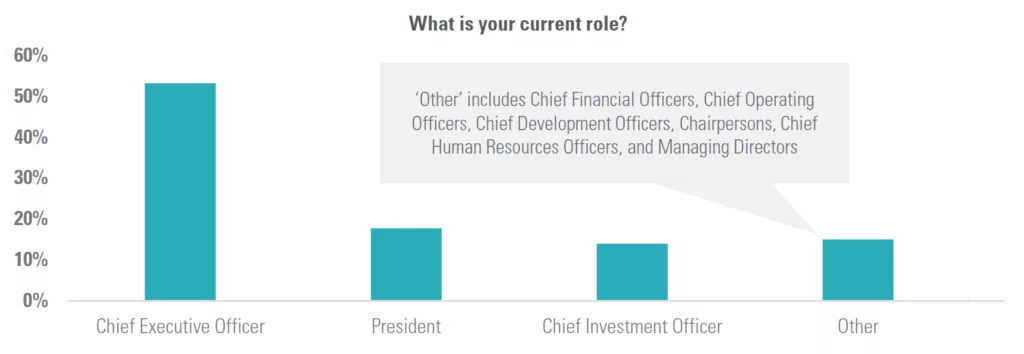

Executive Roles: The majority of respondents (53%) identified as Chief Executive Officers, with additional representation from Presidents (18%), Chief Investment Officers (14%), and other senior leadership roles such as CFOs, COOs, and Managing Directors.

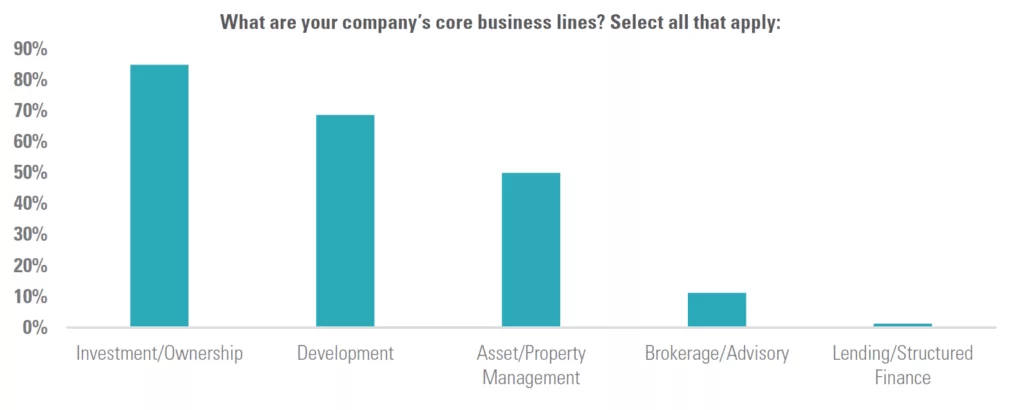

Business Lines: Most operate across multiple lines of business. Investment/Ownership was the most common focus (85%), followed by Development (69%) and Asset/Property Management (50%). Smaller shares cited Brokerage/Advisory (11%) or Lending/Structured Finance (1%) as core activities.

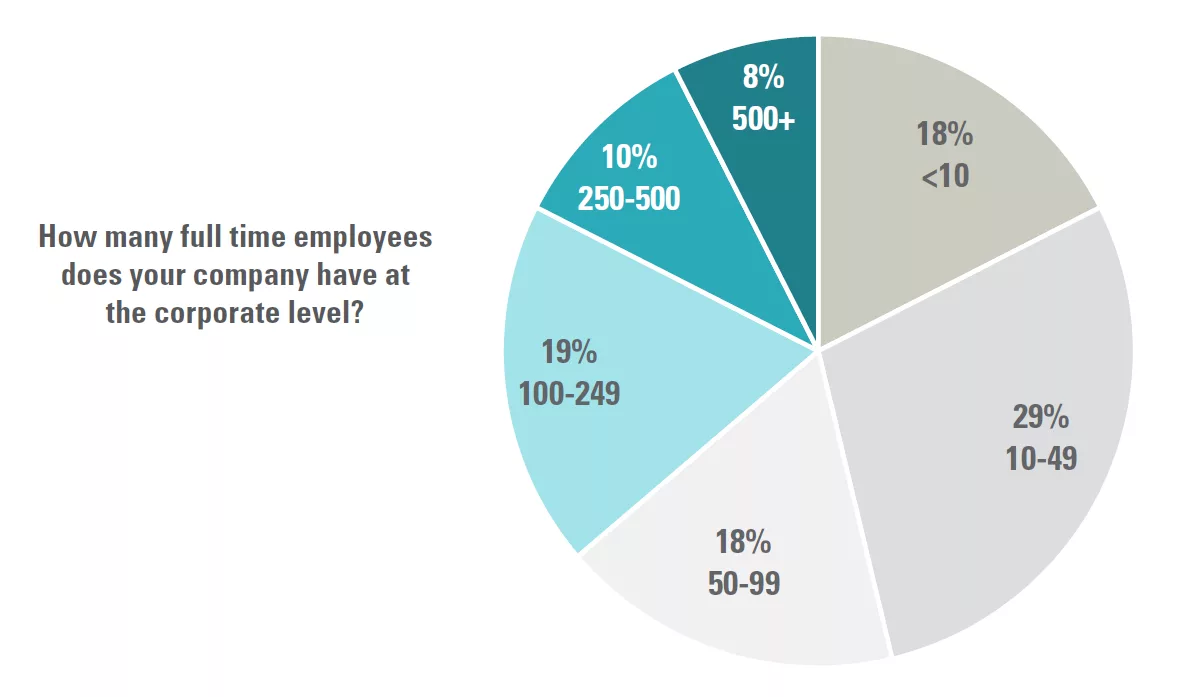

Company Size: Firms range widely in scale. Many respondents represent firms with a corporate headcount between 10 and 49 employees (29%), but the survey includes everything from boutique operators to enterprises with more than 500 employees at the corporate level.

Product Focus: The majority of respondents invest in, own, develop, and/or operate Multifamily Rental Housing (62.5%), reflecting the asset class’s prominence in recent cycles. Respondents also report exposure to Retail (24%), Office (23%), Industrial/Logistics (20%), Single-Family For-Sale (19%), and select niche sectors such as Hospitality and Senior Housing.

The survey was fielded in June and July 2025 with select interviews conducted in July.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Copyright © 2025 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.