COVID-19 Real Estate Sentiment Survey and the Truncated V-Curve, with a Tail…

As the current coronavirus pandemic reaches a (hopefully) peak in the U.S. and the extent of the devastation to the economy comes into focus – 22 million unemployed, thus far, with downstream impacts to everything from retail sales, sporting events, the price of oil, and the stock market (regardless of a mini bull market in the past week or so) – we have begun to think about what the recovery is going to look like, which real estate segments will be the winners and losers in the “Great Lockdown,” and what is happening in the real estate capital markets? And so we asked our client base of real estate market professionals to tell us what they thought, in this special edition COVID-19 Real Estate Sentiment Survey.

Survey responses were solicited the week of April 13-17, and we expect this sentiment to continue to evolve as we gain a line of sight to a possible flattening of the curve and a return to normal life and commerce – probably in a rolling fashion, and possibly with variation across the country. We will conduct the survey again in two weeks and track the progression of the sentiment.

Survey participants were asked three questions:

- There is little doubt that we are now in, or soon heading for, a recession in the U.S., and so the question is, which scenario, ranging from a relatively quick recovery to a more prolonged downturn, do you believe is most likely for a recovery?

- What impact will the scenario you have selected have on various real estate segments, ranging from no impact though dramatic impact on prices, revenues and/or values?

- What impact do you believe the downturn scenario you have selected will have on the ability to secure capital for your real estate activities, including continued funding for projects under construction, to refinancings, to debt and equity capital for new projects?

Here’s what we learned.

Recovery Scenarios

The recovery will take some time

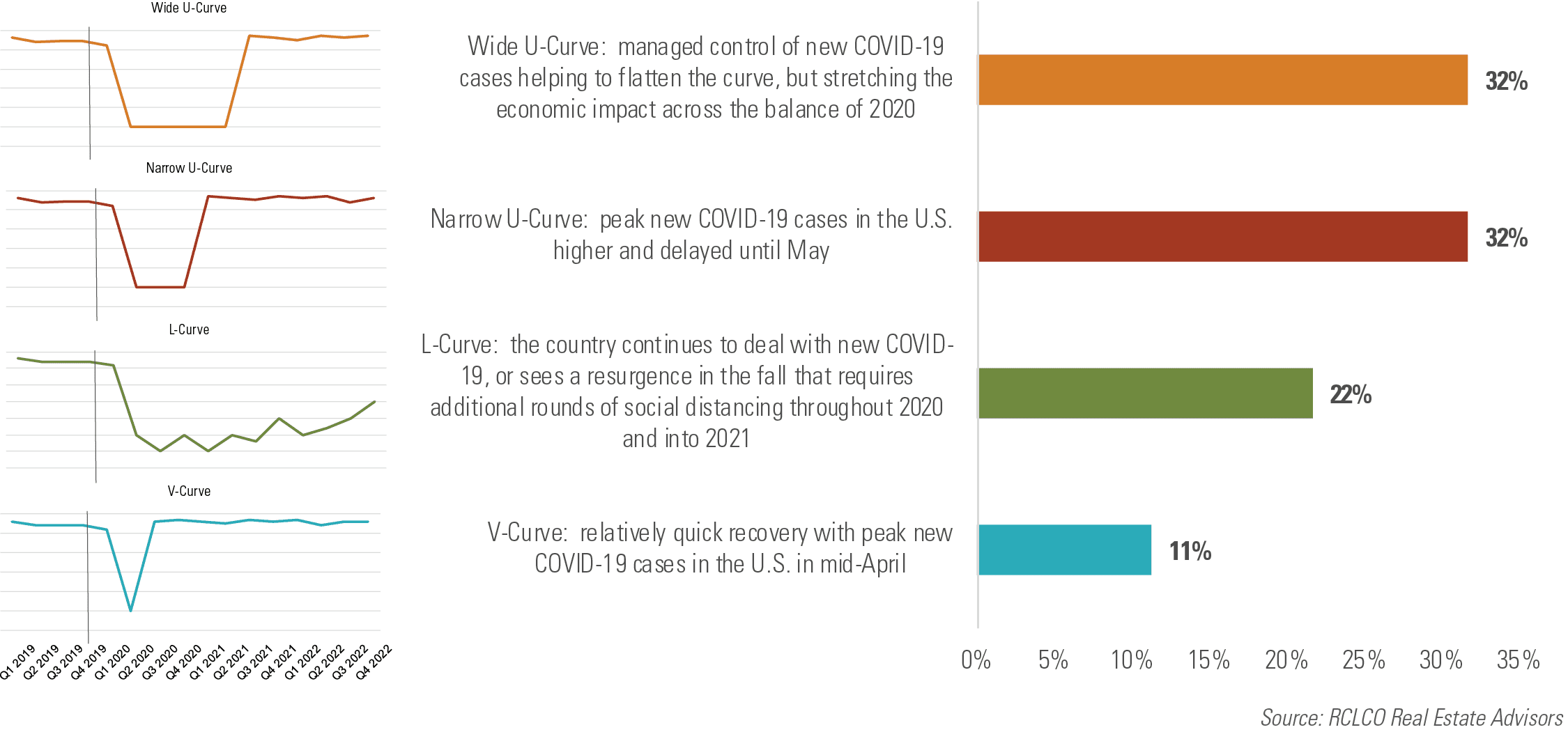

V-Curve – Not Likely

Very few survey respondents expect to see a rapid snapback of the economy, with peak new COVID-19 cases in the U.S. by mid-April – only 11% indicating that we can expect a “V-Curve.”

Prolonged Downturn, But Robust Return to Growth – Pretty Likely

Rather, the majority expect to see either more a prolonged downturn with 32% calling for a “Wide U-Curve” with managed control of new COVID-19 cases helping to flatten the curve, but stretching the economic impact across the balance of 2020; and the same 32% calling for a “Narrow U-Curve” with peak cases occurring in May 2020; but in both cases a fairly robust return to growth once the economy opens up again for business.

Long Slog – Can’t Rule It Out

Finally, a not insignificant percentage (22%) believe that the effects of the coronavirus pandemic will have deep and longer-term impacts on the U.S. economy. In this scenario, respondents expect that the country will be dealing with new COVID-19 cases, or possibly see a resurgence in the fall that requires additional rounds of social distancing throughout 2020 and into 2021.

We would expect the number of respondents gravitating towards a more pessimistic outlook for the economy to increase as the extent of the damage becomes more evident.

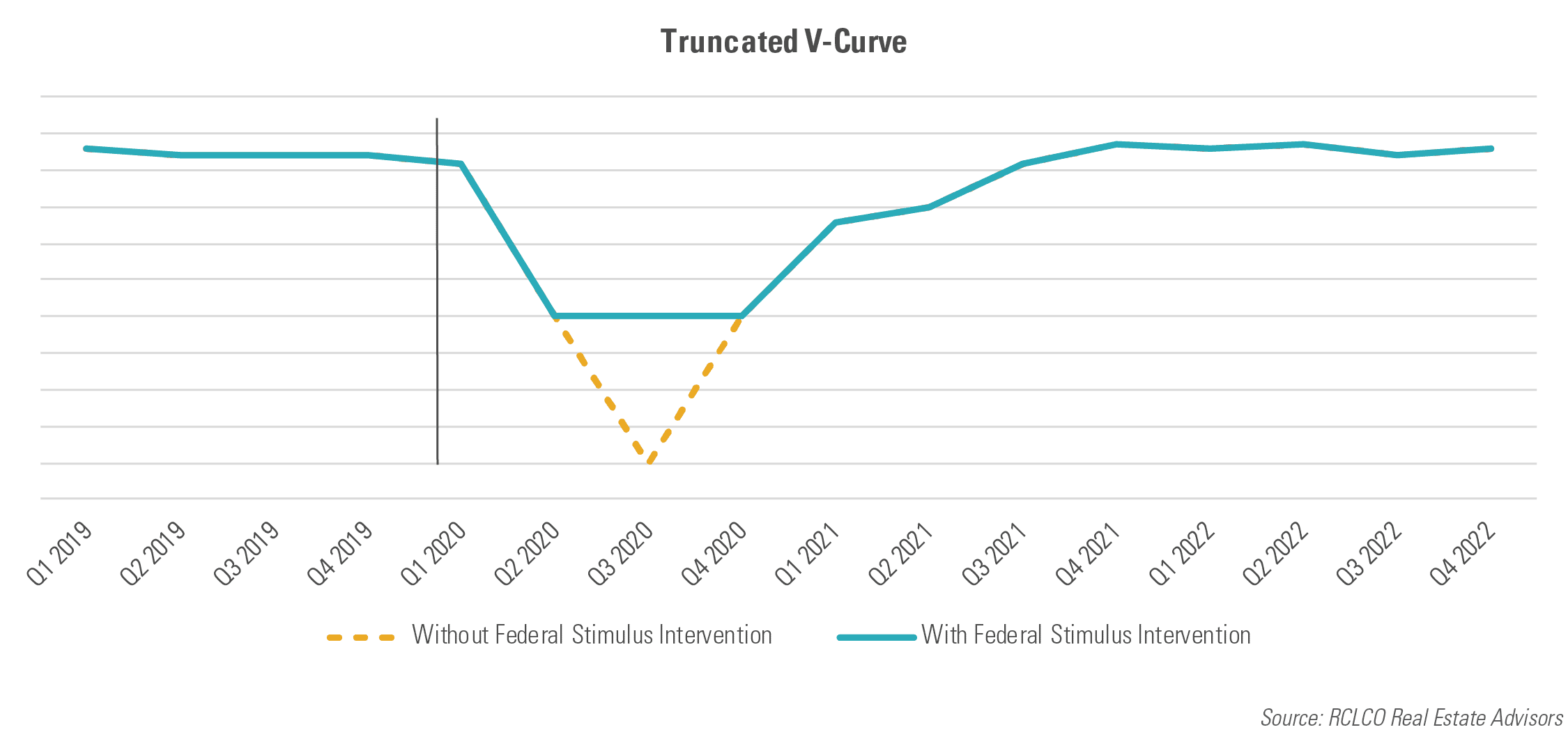

Truncated V-Curve, With a Tail

Here at RCLCO we believe that a “Truncated V-Curve” with a slightly longer tail is the most likely outcome for the shape of the recovery.

| Stage | Indicators | Timing |

|---|---|---|

| Stage 1 | Flattened Curve | Late April/Early May 2020 |

| Stage 2 | Declining Cases | Mid-June 2020 |

| Stage 3 | Healthcare Breakthrough | Q4 2020 |

- 2020 GDP -5% to -6%

- 2021 GDP +5% to +7%

This curve, intended for illustrative purposes only, envisions an economy that, but for federal stimulus intervention, was likely headed for a much deeper and pronounced crash, from which it may have recovered quite quickly upon reopening of the economy. The stimulus created somewhat of a floor and is helping us avoid the pointy and decidedly unpleasant bottom of what could have otherwise been something even worse.

We believe there will be a relatively robust initial recovery as many of jobs lost were merely deferred and many can be rehired from a state of suspended animation without too much time or friction. However, given the magnitude of the disruption, it will likely take some time to regain all of the lost ground – reemerging from this crisis is not going to be an “event,” rather it will be a “process” – and we will likely see elevated unemployment rates for the balance of 2020 and into the first half of 2021 above the long-term average of 5.7%.

So bumping along this floor, what does a recovery look like? We see a three-stage process to extricating ourselves from this disaster.

Stage 1: Flatten the Curve – Late April/Early May

With evidence from China, South Korea, and other places around the globe as possible guides, there is a reasonable case to be made that once we begin to see a flattening in the curve of new COVID-19 cases in the U.S., hopefully in late April to early May, we can begin the process of adding to the list of “essential services,” and begin to see improvements in consumer confidence that will lead to more spending. The economic impacts from the first confirmed case to this flattening of the curve are likely to be unprecedented, with -20% to -25% declines in GDP and over 30 million Americans unemployed. During the one- to two-month “flattening” period, we expect to see a healthy expansion with +/- 5% GDP growth as a sizeable portion of the “essential” economy gets back to work.

Stage 2: Declining Cases – Mid-June/Early July

With significantly improved testing and more focused quarantining leading to more recovered than active cases over a two- to three-month period, many more will go back to work, but the situation will still be very far from normal, with schools still closed, hesitation to travel, dine in restaurants, attend sporting events, etc., and still a significant amount of teleworking taking place. In this stage, half of the GDP loss is regained and begins to grow from here. Assuming this stage continues through Q3 2020, and gains steam through the end of the year, the U.S. economy will still likely be in the red for the year 2020, with year over year GDP declines of between -5% and -6%. Unemployment by the end of the year, while improving, will still likely be in the low double or high single digits.

Stage 3: Healthcare Breakthrough – Q4 2020

With a potential breakthroughs in more effective and widespread testing and therapies to reduce mortality rates of those infected (all of which is being pursued vigorously across the globe), but prior to a true vaccine being developed, which could take 12 to 18 months, the U.S. economy is poised to get back to a “new normal.” Under this scenario, people are back to work, social gathering, traveling, and spending money. The rapid pace of GDP growth begun in the second half of 2020 will continue into 2021, and this year could see most of the losses recouped. However, it will still take some time, perhaps the balance of 2021, to regain all of the jobs lost and get back to pre-COVID-19 levels of employment, and some economic sectors, and likely some real estate segments, may never fully recover.

Downside Scenario

There is of course a chance that the curve does not flatten as hoped/expected, or that there is a resurgence, or possibly regional waves and hotspots, that continue to course over the U.S., and/or that the healthcare breakthrough does not come until later which results in a longer and slower recovery. In this case, there could be an additional -3% decline by some estimates in 2020 GDP, and the beginning of the recovery could stretch into the latter half of 2021.

Impact on Real Estate

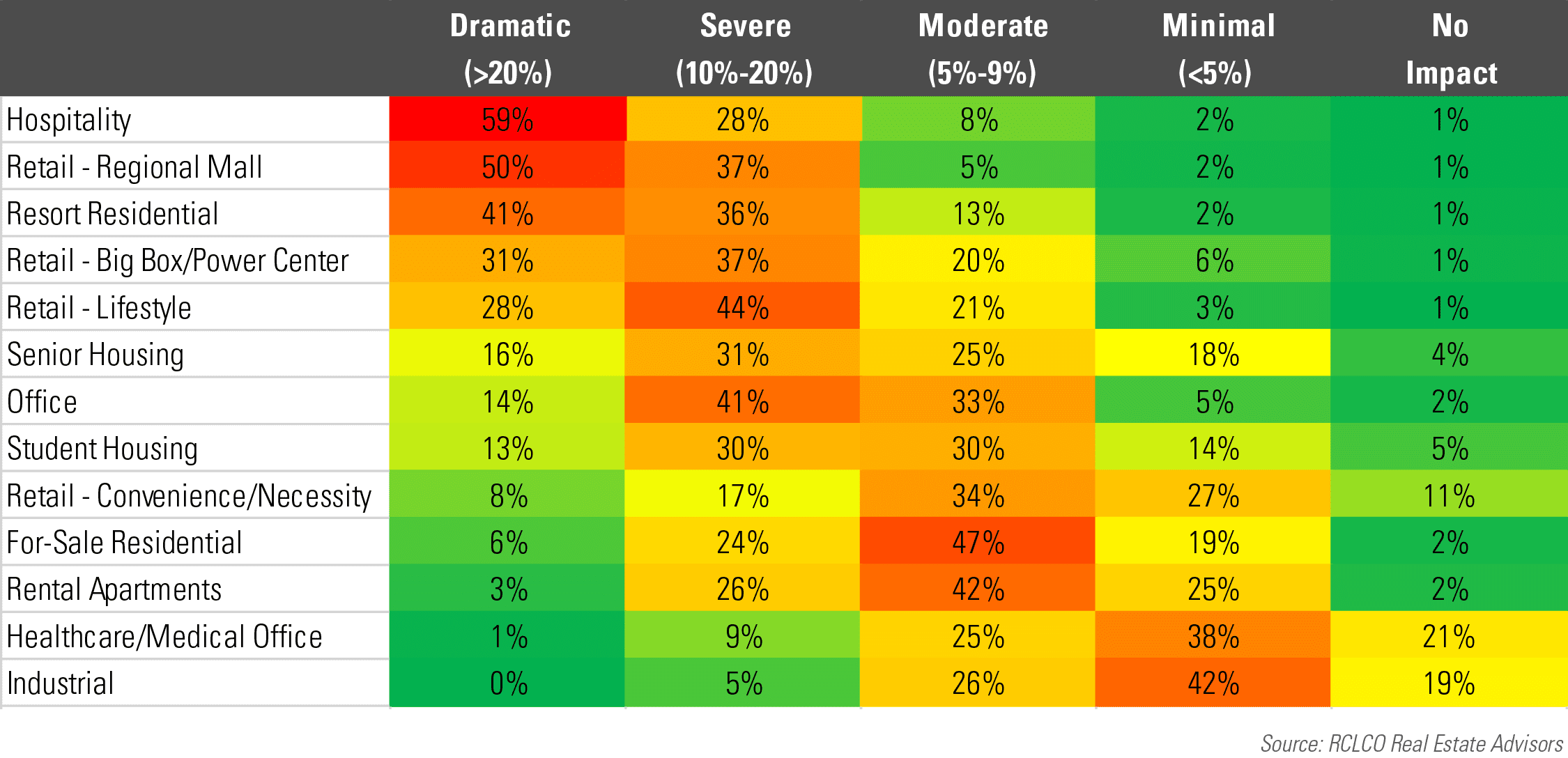

So what impact will this downturn and likely recovery scenario have on various real estate sectors and segments? Survey respondents to the RCLCO COVID-19 Real Estate Sentiment Survey believe that hotel, retail (particularly destination, lifestyle, and entertainment retail that depend upon more than 10 people gathering closer than six feet apart), and resort residential are the segments that are getting hammered now, and likely will take some time to recover. Nearly 90% indicated that hotels and regional malls would experience “severe” (10%-20% declines in revenues/values) or “dramatic” (>20% declines in revenues/values) impacts.

Lifestyle and big box/power center retail, senior housing, and office are likely to experience “severe” impacts, equating to between 10% and 20% decline in revenues/values.

Convenience/necessity retail will fare much better, with only “moderate” (5%-9% declines) or “minimal” (<5% declines) impact. Perhaps not surprisingly, in many of our conversations with owners and operators of grocery-anchored neighborhood shopping centers, the grocery stores have been experiencing 20%+ increase in sales, while sales in the balance of the centers are down more than 50%. Collections in these types of centers range widely between 50% and 80%, and many tenants are reaching out to landlords seeking primarily deferment, but also forbearance.

At the other end of the spectrum, industrial is expected to have minimal impact, with nearly 20% of survey respondents anticipating that this segment will experience no impacts at all, and another 42% expecting only minimal (<5%) impact. Similarly, the healthcare and medical office segments are expected to experience only minimal or no impacts.

In the for-sale housing space, builders and land developers are seeing traffic drop off precipitously, with most converting to virtual or limited scheduled sales operations. Prices seem to be holding for the time being, but cancellations have increased, and many builders and community developers are pulling back on spec home and land development activities.

Finally, in the rental apartment space, the majority of survey respondents expect moderate impacts to revenues and/or values. Owners and operators report to us that most stabilized apartment communities have collected low to mid-90% of rents for April, but they expect May to be worse. Occupancies are holding as few residents are electing to move in this environment, with most residents renewing or extending. Lease-up pace of communities is 20% to 50% of pre-COVID levels. Concessions, while not discernable in the data yet, are in the works.

Based on RCLCO’s extensive interviews and conversations with real estate executives across the country in just the past week, property-/project-level revenues during the “shut down” period for selected real estate sectors could vary significantly:

| Segment | Revenue Variation |

|---|---|

| Industrial | -0% to -5% |

| Multifamily | -5% to -15% |

| For-Sale | -50% to -80% |

| Retail | -50% to -90% |

| Hospitality | -80% to -100% |

As the Stage 1 Flattening Curve evolves into the Stage 2 Declining Cases condition, we expect industrial will snap back to trend line. Multifamily and office collections will resume and improve, but still below pre-COVID-19 levels. Retail is likely to continue to suffer, and may gain half of its losses over time – COVID-19 is likely to accelerate the trend already in place pushing marginal operators and those subject to increasing e-commerce competition to go under. Hospitality will be one of the last real estate segments to recover, and may only make it back to 25% of pre-COVID-19 performance in 2020.

As the recovery gains steam, industrial will continue to be the “hot” sector as businesses fortify supply chains, businesses increase inventories, and some manufacturing is repatriated. Collections at high quality multifamily and office assets start to match or exceed pre-COVID-19 levels. Expect all type of retail to lag, but steadily improve as the consumer reengages. Hospitality will also lag in the recovery, but will steadily improve as more essential businesses are activated, and fears of travel and convening subside.

Availability of Capital

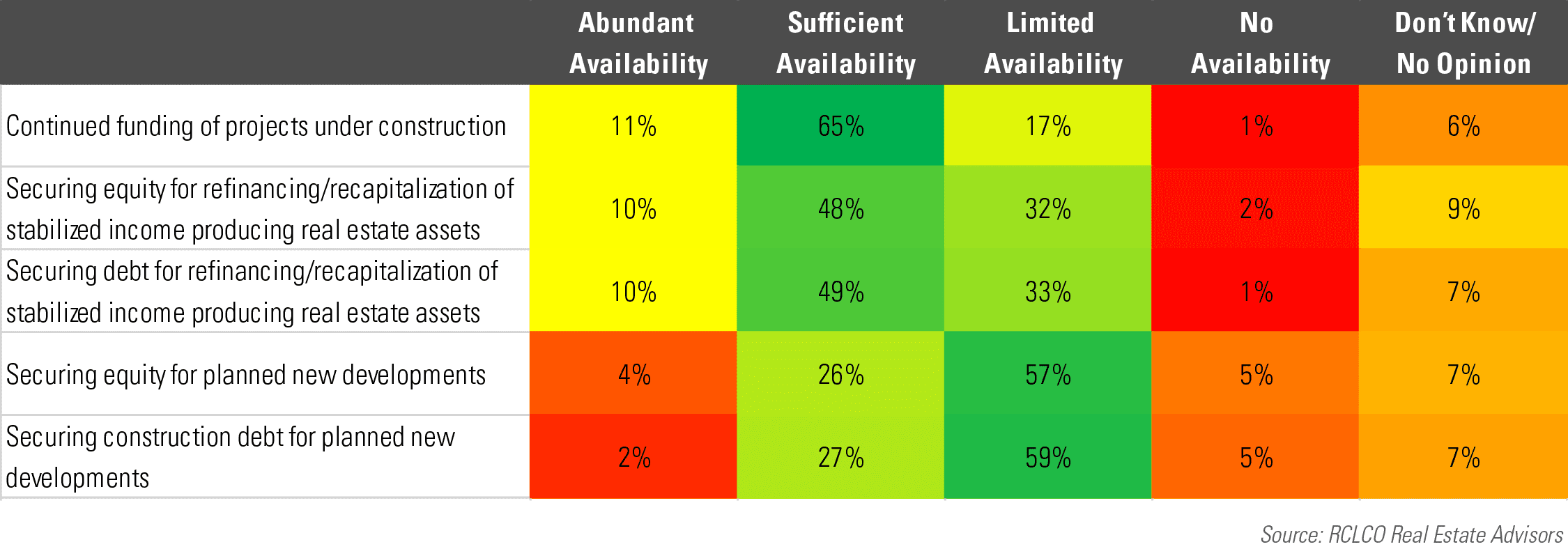

When asked about the impact that the recovery curve is likely to have on the ability to secure capital for various real estate investments and activities, the majority of survey respondents believe that projects currently under construction will continue to be able to draw down funds to continue making progress, particularly in places where residential construction has been deemed “essential.”

Similarly, a majority believe that there will be either sufficient or abundant availability of both equity and debt for refinancing/recapitalizing stabilized income-producing real estate assets. However, most expect that securing capital, either debt or equity, for new projects will be in limited supply.

These sentiments are consistent with what RCLCO is hearing from its clients. Most construction projects are indeed continuing as negotiated, with some changes around the edges with regard to LIBOR floors, etc. Strong sponsors with long-standing relationships with banks and other lenders continue to have access to capital, and most deals that were inked pre-COVID-19 are closing largely at the negotiated terms.

However, we are already seeing a steep drop in new transactions with only deep distress or long-term strategic investments taking place. New borrowers or new investments and new developments are largely on hold. Debt capital markets are particularly constrained as many lenders have been distracted by processing SBA and PPP loans. Some sponsors have dropped deals, but most have negotiated and received delays and deferrals, and many deals are, or soon will be, in the process of being renegotiated. Pricing discovery and valuation are impossible to determine, and this will likely continue to be the case until there is some better clarity on the shape of the recovery.

Truncated V-Curve anyone?!

Article and research prepared by Charles A. Hewlett, Managing Director and Taylor Mammen, Senior Managing Director.

RCLCO can help you make the most strategic, effective, and enduring decisions about real estate during this turbulent time – let us be a resource for you! To learn more about how you can leverage our strategic planning, investment strategy, and real estate economics expertise, please contact Charles A. Hewlett, Managing Director, at (240) 644-1006 or chewlett@rclco.com. Whether conducting valuation analyses or evaluating the highest and best use for development, investment, or disposition, for example, RCLCO can provide detailed and actionable recommendations related to your real estate needs. We have been a trusted industry partner for over 50 years, supporting our clients and the real estate community through other previous challenging times as well.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us