January 21, 2022

RCLCO’s Real Estate Market Sentiment Survey has tracked confidence in U.S. real estate market conditions for the past 10 years. The overall index took a dramatic dive in Mid-2020 due to the speed and intensity of the economic downturn sparked by COVID-19, hitting its lowest level in the history of the series (9.2). After a big drop in 2020 due to COVID-19, market sentiment spiked to 89.1 in mid-year 2021, as vaccination rates rose, new cased dropped, business restrictions were lifted and the economy and real estate markets started to recover. The Year-End 2021 result shows a more tempered sentiment of 82.1 as new variants have emerged in the second half of the year that are more transmittable and vaccine-resistant and as concern about inflation increases.

Key Takeaways

- The RCLCO Current Real Estate Market Sentiment Index (RMI)[1], which measures sentiment on a 100-point scale, has decreased 7.0 points over the past six months, from 89.1 at MY 2021 to 82.1 at YE 2021, still well above the long term (since 2011) average of 69.4.

- Respondents predict that real estate market conditions will continue this gradual decline, with the RMI anticipated to drop 13.1 points to 69.0 over the next 12 months. This would bring sentiment in line with average levels over the past 10 years.

- Just over half of survey respondents (57%) believe real estate conditions will remain moderately or significantly better in the next 12 months.

- A majority of respondents believe Covid-19 will cause a reduction in long-term office demand compared to pre-Covid estimates, with 41% predicting a 10-20% reduction, followed by 36% predicting a slight 0-10% reduction.

- The apartment market boom will continue for at least another year – nearly half of the respondents indicated apartment rent growth would remain somewhat above historical levels (5% to 8% growth) in 2022.

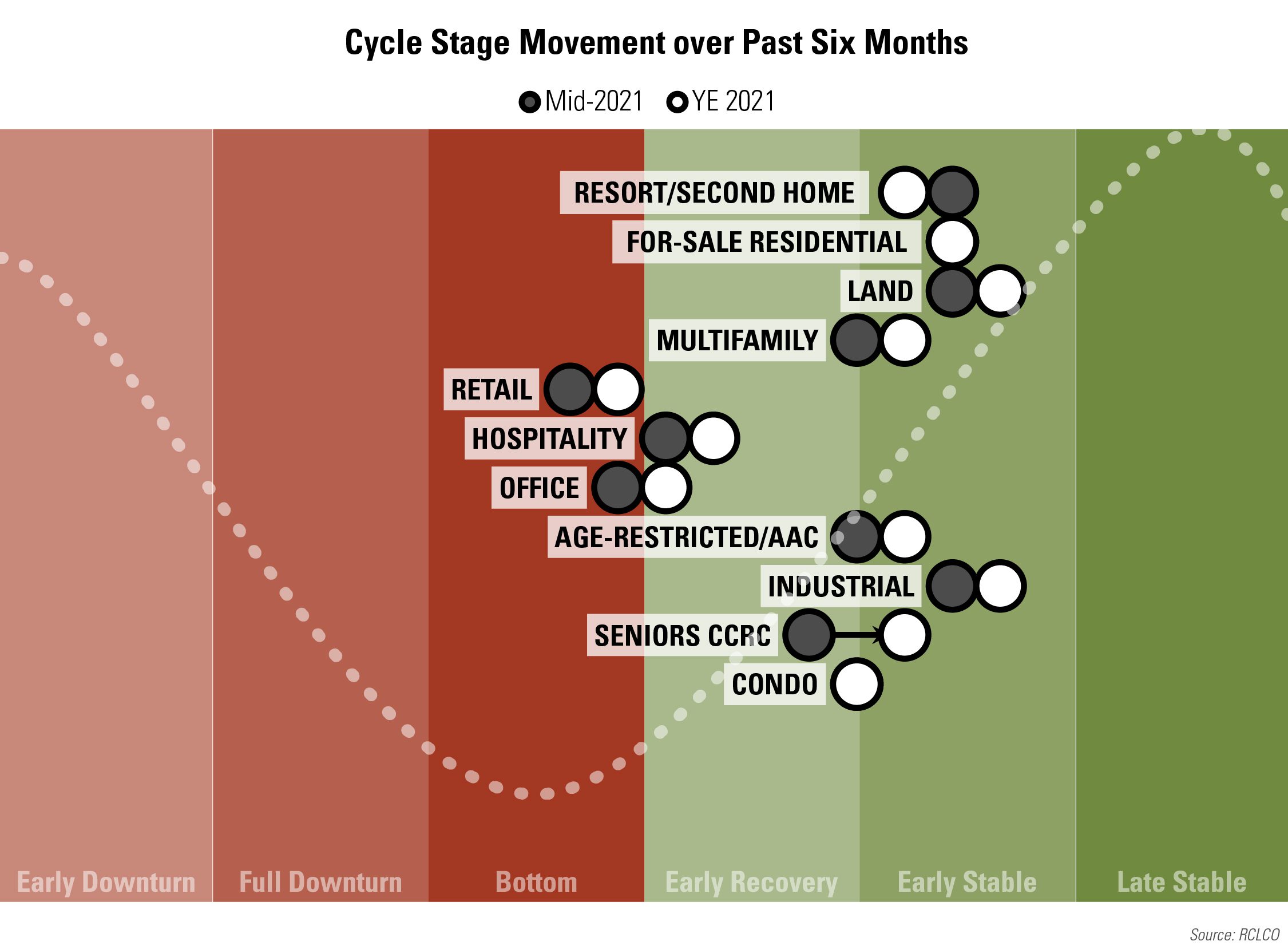

- Respondents indicate that many product types have moved from Early Recovery to Early Stable phases since the MY 2021 survey. Retail still remains at the bottom of the cycle due to ongoing disruption from Covid-19, though both office and hospitality have reached early expansion. Encouragingly, retail is expected to return to Early Recovery within the next 12 months.

- Looking ahead a year, a majority of respondents expect interest rates to rise, inflation to increase, and capital flows to increase to real estate. Respondents were split about homeownership rising or remaining constant. The was also less consensus over the expected performance of cap rates over the next 12 months, though slightly more predicted an increase than at mid-year.

Sentiment has Moderated since the Mid-2021 High – Though Remains Strong

Sentiment about the health of the economy and real estate markets declined somewhat at Year-End 2021 when compared to the exceptionally optimistic sentiment at mid-year 2021. Summer of 2021 reflected the first wave of optimism in what has been an inconsistent recovery. Since mid-2021, the RMI index decreased 7.0 points to 82.1, yet remains well above the long-term (since 2011) average of 69.4. The slight decline is due in part to supply-chain concerns and a recent surge in cases due to the Omicron variant. Despite these factors, the housing market, in particular, remains strong, and both the for-sale and for-rent sectors have had a record-breaking year in 2021 due to robust demand. Covid-19 had a disproportionate impact on service-sector and retail workers and left many middle-income and affluent households relatively unscathed. With a strong stock market and less money spent on travel in 2020 and 2021, many higher-income households found themselves flush with cash and in the position to upgrade their housing situation.

RCLCO National Real Estate Market Index

Source: RCLCO

The current index at 82.1 remains high, as values above 60 are typically indicative of strong market conditions, and is well above the long-term average. However, this value is slightly below the predicted year-end value of 85.2, which shows that the market softened faster than was anticipated in the summer of 2021. The forward outlook predicts the index will decline by 13.1 points over the next 12 months, a slightly pessimistic reaction to the new variants, vaccine hesitancy and breakthrough infections, inflation concerns, and supply-chain woes. However, just as this pandemic has not been predictable, it will be interesting to track sentiment over the next six months as there is much in the real estate industry to remain optimistic about.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

The majority (75%) of respondents indicated that national real estate conditions were moderately or significantly better when compared with one year ago. While 36% of respondents predicted that real estate market conditions are significantly better than last year, this is a marked decline from mid-2021. This signals that while the recovery was initially strong in mid-2021, there have been several hiccups in the recovery which have caused sentiment to temper at year-end 2021.

Browse Past Sentiment Surveys

The outlook for the upcoming year remains strong, though more subdued than at mid-year. Approximately 57% of respondents predicted that national real estate market conditions would be “moderately” or “significantly” better in the next year. The remainder of the survey respondents were equally split between unchanged or worse conditions.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Covid-19 Impacts on Office Space Demand

The pandemic has accelerated the acceptance of remote work, with many companies instituting a hybrid work policy or allowing their employees to work remotely indefinitely. While many offices have welcomed back employees in the past year, the ever-changing Covid-19 landscape has made planning for the future challenging.

- We found that when asked to predict Covid-19’s long-term impact on office demand compared to pre-Covid estimates, 76% felt that they would be a decrease of up to 20% in office space demand.

- Nearly 15% believed office demand would decrease by more than 20%.

- This metric will be interesting to track as more companies have leases expiring to see what decisions are made about the overall amount of office space and/or the layout of the space that makes the most sense moving forward.

Covid-19’s Impact on Office Demand

Source: RCLCO

Apartment Market Boom – Temporary or Lasting?

2021 has been a strong year for apartment rent growth in many markets. National effective rent growth was up 12.6% at the time of the survey (in 4Q 2021). Historical average annual rent increases tend to average between 2% to 5%, so 2021 YTD growth was significant. With this as context, we asked what rent growth might look like in 2022, and nearly half of respondents believed that growth would remain somewhat above historical levels (5% to 8%), indicating that the apartment market boom may continue into 2022. However, opinions on this were somewhat mixed, and while a smaller share believed growth may be even higher than 8%, a significant share 27.5% believed rent growth will moderate to historical levels. It still remains seen if this level of growth is sustainable in the longer term, or if a reset to historical levels will happen in 2023 or beyond.

Apartment Market Rent Predictions for 2022

Source: RCLCO

Survey respondents believed that most of the major real estate sectors were entering early recovery or early stable phases by YE 2021.

- The industrial sector continued its exceptionally strong performance due to increasing e-commerce penetration and home delivery surges throughout the year.

- Office has moved into early recovery and hospitality also continues to progress within early recovery stages. While these sectors were hard hit by Covid-19, the ability to return to the office and travel over the past year has given the sectors a boost.

- Retail remains at the bottom but is also showing signs of moving into early recovery. The acceleration of trends toward e-commerce that existed before the pandemic have made lasting changes to the retail landscape, and the sector is evolving to adapt to new market conditions.

- Within these sectors, there continued to be bright spots in essential uses– for example, more than 58% of respondents categorized Medical Office and Grocery-Anchored Community/Neighborhood Centers in the healthy expansionary phase of the cycle, consistent with MY 2021 Sentiment.

- Hospitality was bolstered in the past year by continually strong sentiment in the Home Sharing/Airbnb/VRBO, Budget, and Extended Stay product. In the past six months, Resort sentiment has significantly improved as leisure travel has resumed.

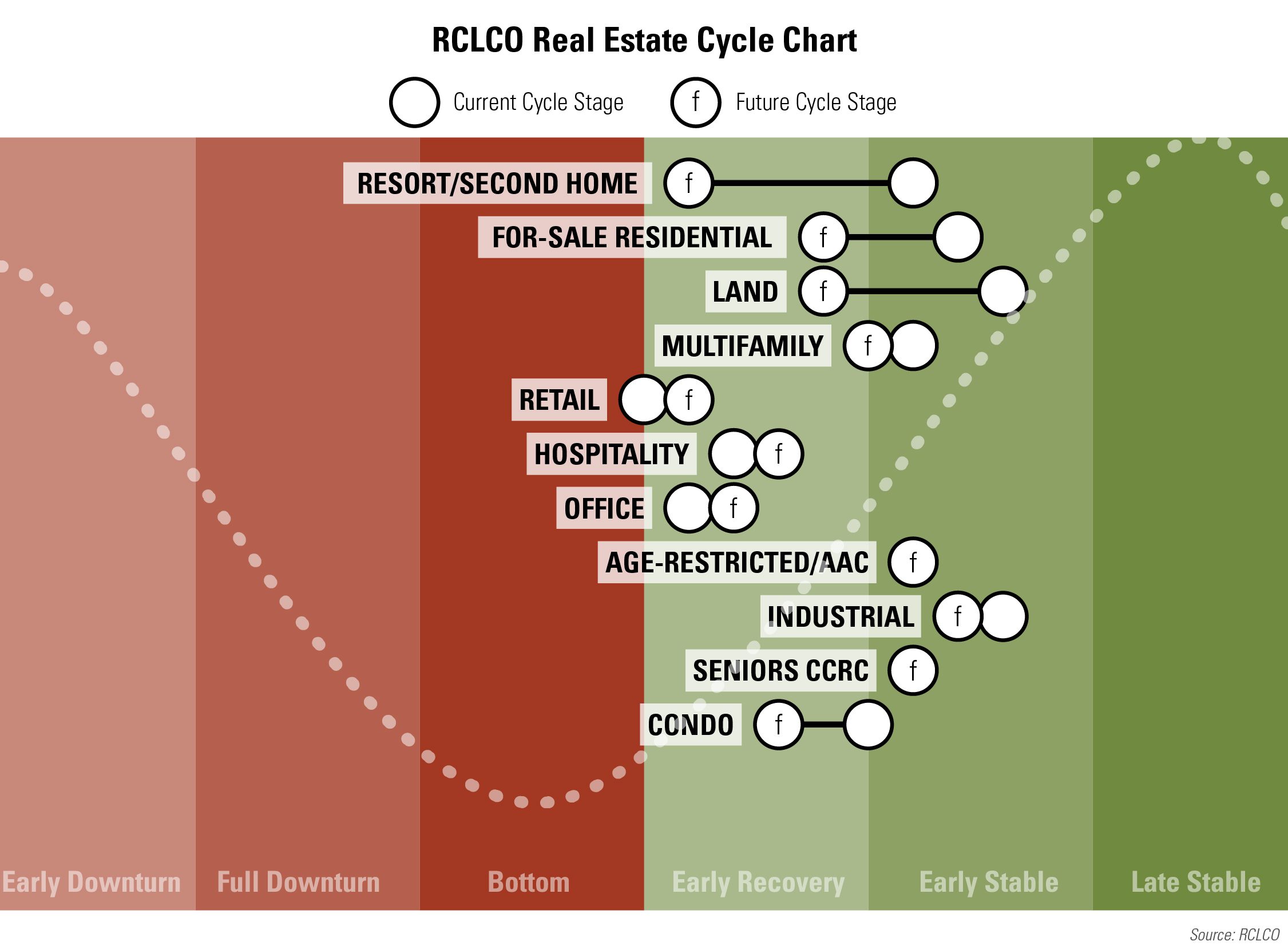

Expansion of most product types in the upcoming year

Looking forward, all sectors are predicted to move into recovery or stable phases, with many moving to a more favorable stage. Retail is expected to attain Early Recovery in the next 12 months, while hospitality and office are expected to move further into Early Recovery as office workers partially return and travel resumes, enabling the economy to become more fully engaged. Industrial continues its strong performance, moving further into the Early Stable stage. For-sale residential (including resort/second home) and land outperformed significantly in the downturn as buyers took advantage of historically low mortgage interest rates and were looking for more space; the for-sale sectors are currently pegged as Early Stable, though due to recent supply chain issues the forward-looking predictions for these uses are somewhat more tempered.

Economic Indicator Predictions for the Next Year

While interest rates have increased from lows earlier in the year, 77% of respondents predict that interest rates will continue to increase moderately for the next year. Inflation is predicted to increase by over 87% of respondents, with a relatively even split between those who expected a moderate or a significant increase. Over half (57%) of respondents also felt that capital flows to real estate would increase over the coming year, a positive prediction but a decline from the two-thirds of respondents who felt this way at mid-year. While the for-sale market sentiment is strong overall, respondents were somewhat split about the homeownership rate with 43% of respondents believing it will continue to rise while 39% believe it will stay the same. While there was relative agreement around increasing inflation, increasing interest rates, and increasing flows of capital to real estate, and somewhat of a consensus around a rising homeownership rate, there was less consensus around future cap rate levels. Of the respondents to this survey, 16% believe they will decrease moderately, 36% predict no change, and 41% predict a moderate increase. However, the number of respondents who believe rates will go up has increased slightly since mid-year (36%).

Predicted Economic Indicators over the Next Year

Source: RCLCO

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. Approximately two-thirds (72%) of respondents have worked in the real estate industry for 20 years or more, and 83% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 45% of the sample. Another 19% are investors or capital allocators, followed by 7% in design or architecture firms. The remaining 29% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

For management consulting services or more information about our strategic planning group contact Joshua A. Boren.

Sentiment Survey article and research prepared by William Maher, Director of Strategy and Research; Kelly Mangold, Vice President; and Grace Amoh, Associate.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.