May 9, 2025

The Trump administration’s approach to tariffs and its rollout have spooked investors and consumers with good reason, with slower growth or even a recession increasingly possible. Still, RCLCO’s base case is that U.S. real estate benefits from favorable investment dynamics with limited downside in valuation and compelling opportunities for cash flow as markets settle down in the weeks and months ahead.

Eyes Wide Open About Macro-Economic Risks

As of April 25, 2025

We may not be able to entirely avoid an economic slowdown resulting from 1) the economy-wide “tapping of the brakes” relative to new investments that has taken place since April 2 and/or 2) a trading regime that, even as bilateral deals are made, will likely feature higher tariffs than we’ve seen since WWII. But we think it’s becoming increasingly clear that the worst case scenario is unlikely as a political consensus that favors economic growth is emerges in response to the broad and deep unpopularity of the April 2 tariffs. Further, real estate investors will again focus on the fundamentals, which we believe are in aggregate positive, and a growth trajectory will again emerge.

Trade War Avoided?

Radical trade policy changes would cause genuine shocks to the economy. Even during the tumultuous last few weeks the evidence suggests that political leadership will fall on the side of reason and that worse case scenarios (which are real and very scary) are unlikely to be the result. Our base case is that a complex network of negotiated compromises, probably with a base layer of higher tariffs, but generally more consistent with decades of economic theory and practice will emerge during the remainder of 2025.

Foreign Investors Do Not Abandon the U.S.

The last few weeks have also underscored the very real threat that global financial markets could sour on the American economy and that the impact would be disastrous. In the past few weeks, we’ve spoken to investors around the world and recognize that they are taking stock of the potential for economic weakness in the U.S., and some may choose no action for a period of time. Assuming the avoidance of calamity as suggested above, however, it is also apparent that U.S real estate, in particular, will again be too compelling to ignore.

Rates Settle Down but Don’t Decline Much.

Inflation appears to be sticky, plus foreign investors in Treasuries may go on strike, keeping rate volatility elevated in the near term. The Fed is demonstrating commitment to move rates cautiously if at all, and we suspect that 10-year rates will remain between 4.0% and 4.5% through the second half of the year.

Real Estate Capital Markets on Stand By

While there is, unsurprisingly, much watchful waiting at the moment, we continue to observe ample dry powder and investor interest in taking advantage of the otherwise strong and improving investment fundamentals. Public markets illustrate this state of anxious stasis and daily volatility, but anecdotal evidence suggests an immediate-term pull back, not a retreat, by both debt and equity providers for real estate. Overseas investors—often reflecting national politics—are more explicit regarding their pause.

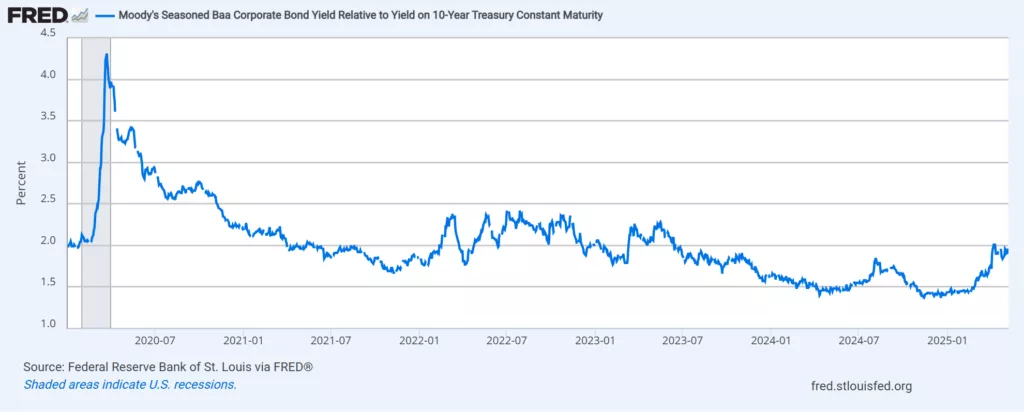

Looking more quantitatively, RCLCO closely monitors the Baa bond rate to 10-Year Treasury spread, which research suggests has been the best indicator of troubled times ahead for the economy and real estate. The spread has widened rapidly in the last week, though does not yet exceed 300 basis points, which in the past has signaled crisis for real estate capital markets, but should be monitored carefully.

Buyers’ expectations for a risk premium to transact amid current turmoil could lead to short-term asset repricing—which had appeared to be behind us at the beginning of 2025. We expect, though, buyers’ hopes will largely be disappointed: like in 2023 and 2024, sellers will be patient and give way only under duress. REITs already provide evidence of valuation stickiness, showing meaningfully lower declines than broader public equities.

Real Estate Fundamentals Largely Outweigh Tariff Turmoil

Underwriting new investments in 2025 will be challenging. Costs of both construction and operations will be hard to forecast, and we may not escape recession. While history tells us that higher costs can usually be passed along to consumers of real estate, just how much tenants will bear is uncertain. The potential for slower job growth, compounded with higher inflation, could also temporarily interrupt growth in demand.

But strong long-term fundamentals remain in place for real estate based on broad-based balance in supply and demand and a meaningful pullback in construction over the last 18-24 months, in many markets and property types from already low levels of the last decade.

Higher materials costs—even in lower tariff scenarios—and tighter labor pools make new development appear particularly infeasible. This will clearly benefit owners of existing properties, but investors in development can look beyond the uninspiring and unsupportive recent data to tight property markets in the medium term.

Implications of a tariff-driven slowdown vary by property type:

- Poor consumer confidence and/or slower job growth could negatively affect residential real estate, although the pullback in new supply in 2025 and 2026 will put a floor under rents and occupancy. Discretionary moves could be deferred, perhaps creating a pullback in luxury housing performance, and renters subject to economic pain may look for ways to reduce costs by moving down or doubling up.

- Long-term demand, namely e-commerce, driving the logistics market should not fundamentally change, but it will experience shocks as the global economy reorganizes; coastal port markets will be significantly impacted.

- Office fundamentals were just appearing to reach bottom and an economic slowdown would frustrate further recovery as leasing decisions are deferred. But job losses could finally give employers leverage to enforce greater in-office attendance, putting a floor underneath office demand.

- Neighborhood retail will remain mostly protected from the impact of higher costs but regional malls may suffer for a time as customers defer purchasing. Hospitality, particularly resort, could see similar impacts.

- “Niche” or specialty sectors which rely on need-driven demand (e.g., seniors housing, medical office) or shifts in structural demand (e.g., data centers) may continue to be relative bright spots in the real estate market.

Use Extreme Caution, But Too Soon to Change Strategy

The risks of the proposed change in trade policy and their negative impacts on the global economy are real and significant. Investors should monitor them closely, and volatility will challenge decision making, but our base case assumes long-term demand trends and the flow of capital to real estate will remain healthy—suggesting a period in which investors will find attractive opportunities amid the uncertainty.

As of April 24, 2025