The Monte Carlo Simulation: Contemplating Risk in Real Estate Investing

Real estate performance in the U.S. has been consistently cyclical throughout its history. The most recent economic recession and associated real estate downturn were exceptionally severe, and led to one of the slowest—and longest—expansion periods in recent U.S. history. As the current expansion continues, the probability of a downturn increases. It is therefore reasonable to assume that U.S. real estate markets, like the broader economy, will experience a contraction in the foreseeable future. Nevertheless, due in large part to its illiquidity and the resulting limitations on performance data, the real estate industry has historically lacked quantifiable assessments of risk as a tool to improve investment decision-making.

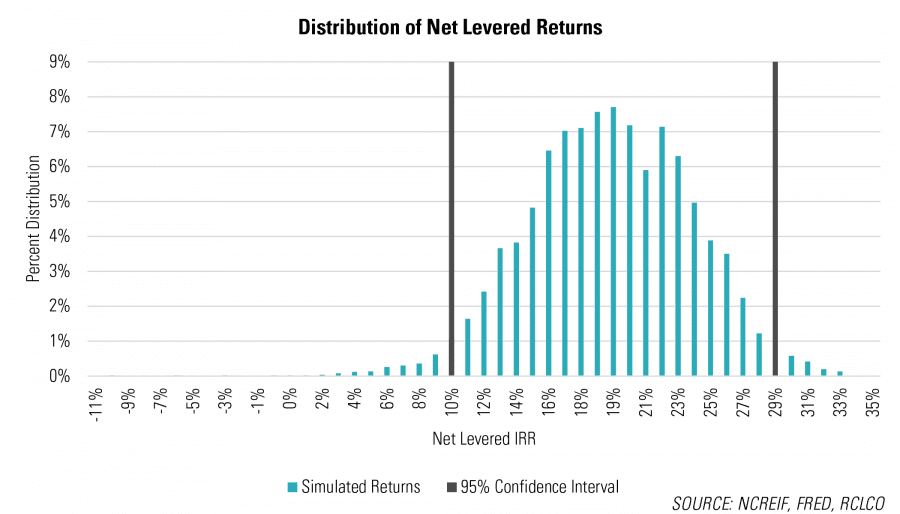

Given the above, the most common approach for real estate investors to evaluate risk is through a sensitivity analysis on returns from changes in select variables. For example, an investor may evaluate expected returns if cap rate expansion is greater than anticipated, or if vacancy rates increase unexpectedly. Such sensitivity analyses, while helpful, are limited in that they look at each variable in isolation, and ignore the actual probability distribution of each variable. The Monte Carlo method provides a much more robust approach for evaluating risk-adjusted returns by simulating performance volatility caused by variances in multiple components of the investment return, such as: cap rates, operating income (including rental rates, vacancy rates, and operating margin), capital expenditures, and interest rates. By generating thousands of potential outcomes based on the expected probability distributions for each variable, we are able to view a spectrum of returns as opposed to just a single outcome produced by traditional underwriting techniques. The result is an assessment of the likelihood (i.e., distribution), and therefore quality, of the projected investment returns, as illustrated in the example below.

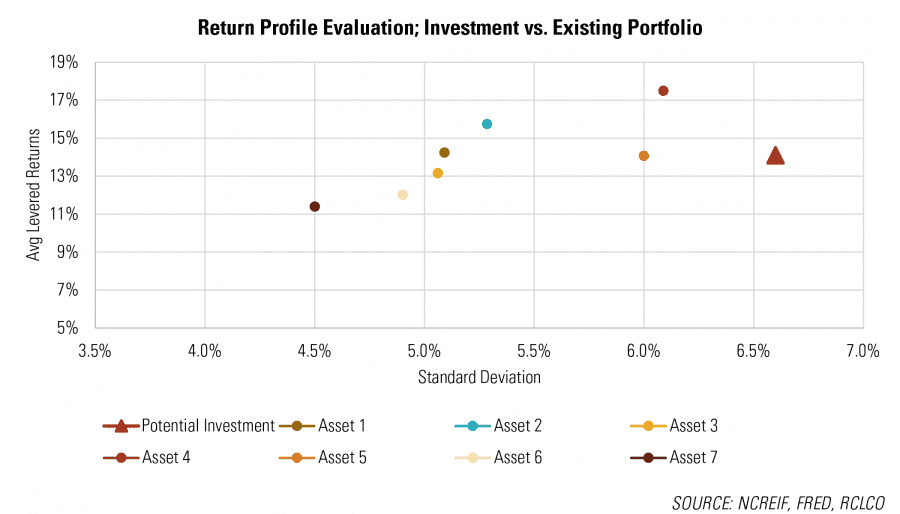

Monte Carlo simulation can be used to improve several common investment practices. Two that we would like to highlight here include: 1) comparing the return profile of an investment relative to an existing portfolio of assets; and 2) evaluating potential fee structures during partnership negotiations.

The figure below demonstrates the first point; the investment being evaluated (the “Potential Investment”) is projected to yield an average IRR of 14.1%, slightly above the portfolio average of 14.0%. However, because the standard deviation of returns for the Potential Investment exceeds the rest of the portfolio, its Sharpe ratio[1] (a measure of risk-adjusted returns, determined in this case through Monte Carlo simulation) is in fact lower than the existing assets. Therefore, while on the surface the investment seems attractive, it would dilute the risk-adjusted return profile of the portfolio if acquired. While traditional due diligence approaches will provide an expected return, and will typically provide insight regarding the risks associated with any investment, they tend to lack a standardized metric that can be used as a means of comparison.

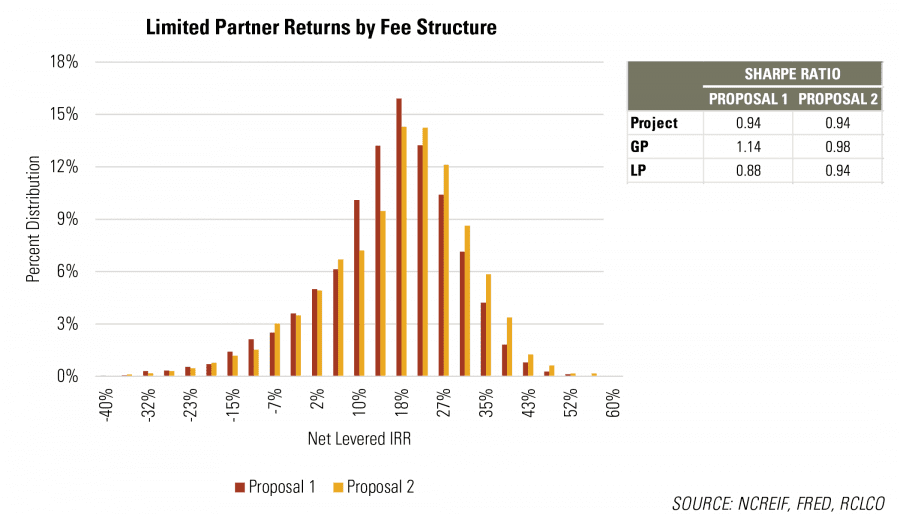

The second highlighted use for Monte Carlo simulation is in evaluation of partnership fee structures. Whether negotiating as a general partner (“GP”) or limited partner (“LP”), a simulation of proposed waterfall distribution structures through Monte Carlo simulation can improve the clarity regarding the potential fees earned and associated drag to the limited partner. Consider two incentive compensation proposals:

- Proposal 1: a simple 35% carry above a 14% IRR; and

- Proposal 2: a 20% carry above a 7% IRR, 30% carry above a 12% IRR, and 40% carry above a 15% IRR.

The return distributions shown below demonstrate that the LP is able to capture a larger share of the investment’s potential upside in the second scenario. As a result, the LP’s expected risk-adjusted return (Sharpe ratio) is substantially improved in the second proposal, with a much narrower gap relative to the GP.

Due to progress in the quality of available data, combined with the statistical tools currently available, Monte Carlo simulation offers an increasingly attractive method to assess risk during the real estate investment process. With the prospect of further improvements in information in the future, the accuracy of the analysis will only continue to improve along with its usefulness in real estate investment decision-making.

Article and research prepared by Ben Maslan, Principal.

References

[1] The Sharpe ratio is defined as the expected return of an investment less the risk free rate, divided by the standard deviation of the investment.

RCLCO’s mission is to help clients make strategic, effective, and enduring decisions about real estate. We proudly celebrate more than 50 years of providing the best minds in real estate with cutting-edge analytics, actionable advice, and the highest level of customer service. Our work includes market, economic, financial, and impact analyses; investment portfolio strategy and implementation; entity-level strategic planning; and management consulting.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us