RCLCO’s Sentiment Survey has tracked real estate market conditions in the U.S. for over 10 years. Events of the last three years have generated unprecedented volatility in the index – with significant swings in sentiment (both positive and negative) with the advent of COVID-19, the recovery, and now recent Fed action to tamp down persistent inflationary pressures that stemmed from the pandemic. The RCLCO current sentiment index experienced its largest decline ever recorded in the first half of 2020 as the pandemic shuttered large swaths of the economy and affected everyday routines, dropping from 64.9 to a then new low of 9.2. One year later the index swung back dramatically to 89.1 by Mid-2021, near the all-time peak, as the economy recovered rapidly and the nation returned to some semblance of new normal. After a more optimistic 2021, the index declined significantly in 2022 to 8.3 by Year End, hitting a new low in the series, as the combination of geopolitical uncertainty, persistent high levels of inflation, and rising interest rates have pushed the economy into a recessionary zone.

Key Takeaways

- The RCLCO Current Real Estate Market Sentiment Index (RMI)[1], which measures sentiment on a 100-point scale, has decreased 26.9 points over the past six months, and more notably has dropped 80.6 points since the most recent peak, landing on a low of 8.5 at Year End 2022. This puts the index solidly into a period of real estate market distress/recession, and is in-line with the level experienced in the first months of the Covid-19 pandemic in 2020.

- Respondents predict that real estate market may have hit its low, or will in the coming months. The Future RMI is predicted to increase 11.1 points to 19.4 over the next 12 months – yet still is predicted to remain in market distress/recession territory.

- Perhaps not surprisingly, three quarters of respondents (74%) believe that real estate conditions will get moderately or significantly worse in the next 12 months, though the majority of these respondents feel conditions will only be moderately worse.

- Survey respondents feel a national economic recession is imminent: almost all of respondents (93%) believe that there will be a recession in the next two years; a strong majority (82%) believe it will occur within the next 12 months (or is already here), and the remaining (11%) predict it will occur 13-24 months from now.

- In a sign of relative optimism, the majority of respondents (90%) anticipate that the looming recession was likely to be of shallow depth and of moderate duration.

- For-sale housing has clearly moved into a downturn due to the impact of rising mortgage rates on this industry. Rental housing has likely reached its peak in the late stable phases, or has just begin to move into early downturn stage of the cycle.

- Looking ahead over the next 12 months, survey respondents expect every major real estate food group to be in some stage of downturn, even the heretofore favored industrial asset class.

- In another potential sign of optimism, approximately half of respondents (46%) predict that inflation will begin to decrease, while only 36% anticipate that it will increase, compared with 66% who predicted an increase at mid-year.

- Overall respondents predicted capital flows to real estate and homeownership rates would fall in the coming year.

- Consistent with the pessimistic outlook, a meaningful share of respondents indicated that their companies have slowed hiring (28%) or instituted a hiring freeze (16%), with only a small share hiring at higher levels (5%).

A New Low

The RMI index has had a series of dramatic peaks and valleys during the Covid-19 Pandemic and War in Ukraine, factors which have led to continual supply chain issues, inflationary woes, and increasing interest rates. RCLCO’s RMI Index in 2021 was exceptionally optimistic reaching a high of 89.1, reflecting an initial wave of confidence in what has been a recovery characterized by fluctuating conditions. Sentiment took a pronounced dive at Mid-Year 2022 dropping to 35.1, followed by another drop to 8.5 at Year End 2022 – comparable to the Mid-2020 low of 9.2 when the Nation was reeling from the first wave of the Covid-19 pandemic. This drop comes as the Fed continues to raise rates to subdue inflation, and mortgage rates have surpassed 7.0%. Rising interest rates have put a damper on the for-sale home market, but also on real estate development in general as deals become more difficult to pencil with increasing debt costs and reduced availability. While there have been recent signs that inflation is moderating, survey respondents overwhelmingly indicated that we are in a period of economic distress and that a recession is imminent.

RCLCO National Real Estate Market Index

Source: RCLCO

The current index at 8.3 puts the market firmly below 30 and at a level that is typically coincident with periods of economic distress or recession. The decline since the last survey was more sizeable than was predicted at mid-year. Looking forward, respondents predict that the index will increase by 11.1 points over the next 12 months to 19.4, an improvement but still in the distress/recession zone. These data suggest that the real estate sector may be performing worse than the economy as a whole. Third quarter 2022 GDP rebounded to a healthy 2.9% after falling in the first half of the year. Job growth, while slowing, is still healthy. Seasonally adjusted retail sales were up 1.6% in October and 8.3% higher than a year ago. On the other hand, borrowing for housing and commercial real estate has become both more expensive and harder to obtain over the past six months.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

Sentiment has seen dramatic peaks and valleys over the past three years. At Year-End 2022, there was relative consensus among respondents, with almost all (90%) indicating that national real estate conditions were moderately or significantly worse when compared with one year ago. The majority of those respondents felt that real estate market conditions are somewhat worse than last year, though a meaningful share felt things had gotten significantly worse. This signals that while 2021 showed a rapid and strong recovery, that it may have been short-lived as 2022 brings a return to negative sentiment and we enter 2023 with more pessimistic predictions

- The outlook for the upcoming year predicts a continued decline. Approximately three quarters of respondents predicted that national real estate market conditions would continue to get “moderately” or “significantly” worse in the next year. The remaining quarter of survey respondents were equally split between unchanged or improving conditions.

Browse Past Sentiment Surveys

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

The sentiment survey has been prone to large swings in the past, and we believe given the timing of the survey in early June that respondents are still processing many of the more recent announcements around persistent inflation, interest rates, and slowing GDP growth.

Recession Forecast

Nearly all (93%) respondents feel that a recession will occur at some point in the next two years, and the vast majority (82%) believe that this recession will occur within the next 12 months. Given the positive GDP growth in Q3 and again likely positive in Q4, RCLCO does not believe the U.S. economy will enter a technical recession in 2022. Regarding the severity of the potential future recession, a majority (57%) believe it will be moderate in depth (-1 to -2% GDP), while encouragingly another 32% believe it will be shallow (0% to -1% GDP).

When Will the Next U.S. Recession Occur?

Source: RCLCO

What Do You Believe the Depth of Recession Will Be?

Source: RCLCO

Impact on Hiring

The labor market has been relatively resilient despite periods of economic uncertainty over the past few quarters. The economy added 263,000 jobs in November, and the strong job market has been a complicating factor in the Federal Reserve’s task of tackling inflation. Asked if economic conditions were currently impacting their own hiring plans, approximately half of the respondents have made no changes. For those that indicated changes, a small share indicating they are hiring at higher levels, but notably 28% are hiring at lower levels, and 16% instituted a hiring freeze.

Is the Economy Currently Impacting your Hiring Plans?

Source: RCLCO

Operating in the Red

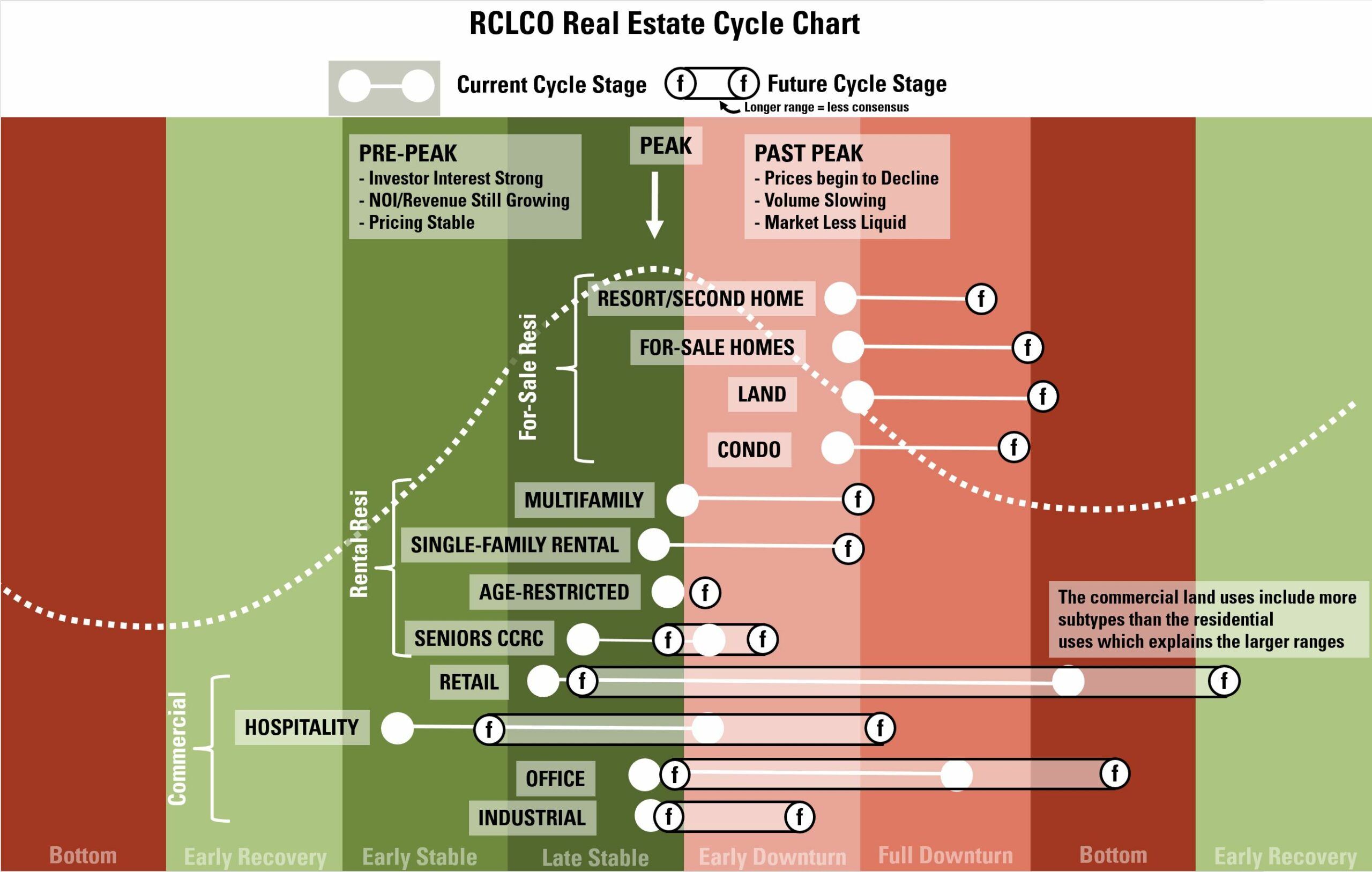

At Year End 2022, there is currently more consensus than there was at Mid-Year about economic conditions and we are already beginning to see some stress and corrections in the residential real estate sectors. As we did last time, we reflect the range of responses (when there is less consensus) in the chart below – the longer the bar, the larger the variation in responses. Not surprisingly, the commercial uses have more variation due to the fact that they contain more subsectors of varying performance than the residential groupings, which are detailed in each bullet below. Sentiment around the for-sale residential sectors has declined into downturn territory as mortgage rates continue to rise. Rental residential fares somewhat better though a growing number of respondent feel it is approaching, or may have recently surpassed its peak. Hospitality and industrial appear to have remained in the expansionary phases, while retail and office show more variation as certain subsectors outperform others in these groupings.

Cycle Stage Movement over Past Six Months

- Residential for-sale uses including resort/second home, for-sale homes, land, and condo all have moved into downturn, as rising mortgage rates have impacted pricing potential and the overall volume of sales.

- Rental residential uses including multifamily apartment, single-family rental, seniors CCRC, and age-restricted rentals are in late expansionary stages of the cycle, though there is a mix of sentiment as a growing number of respondents feel these segments have moved into early downturn territory. Single-family rental has the strongest sentiment of the group, perhaps benefiting from the fact that many households who otherwise would have bought homes are choosing to rent a single-family home instead.

- Retail was a sector with less consensus, though much of this can be explained by the unequal performance among different subsectors. Grocery anchored sectors performed the highest, with the majority feeling these were in early or late stable phases. High Street, Power Centers, Outlets, and Lifestyle centers had moderate performance with a mix between late stable and early downturn phases. Respondents felt that both Class A and Class B regional malls were in full downturn, with the Class A malls outperforming the Class B segment. Pandemic restrictions easing has allowed consumers to return to experiential retail, though customers are also grappling with reduced spending power due to inflation – and the increase in e-commerce (which predated the pandemic) continues to hurt sectors like the regional malls.

- Hospitality continued to remain in stable phases, as much rescheduled personal and business travel resumes. While there was some slight variation across sectors, it is less notable than was seen across other commercial types like retail and office. In particular, an early strong performer during the pandemic, Homesharing/Airbnb/VRBO is the subsector that people feel is the closest to downturn conditions, possibly due to higher supply in that sector.

- Office also had a mix of opinions depending on the subsector. Professional/Medical Office, and Life Sciences are solidly in expansionary phases with strong overall sentiment, while Co-working, Creative office, and Class A office have likely moved towards peak or into early downturn phases. A majority of respondents indicated Class B office was in full downtown, a likely result of the flight-to-quality that we have seen in the office sector.

- The industrial sector moved along into the late stable phase, the sector is showing signs of moving closer to peak.

Many Land Uses Predicted to Move into Downturn in Next 12 Months

Expansion of Most Product Types in the Upcoming Year

Looking forward, many of the residential and commercial sectors are predicted to move into downturn stages, consistent with the consensus that a recession is likely in the next 12 months. The outlook for some commercial sectors remain relatively positive: grocery-anchored retail, storage and data centers, life sciences and medical office, and many segments of the hotel industry including extended stay, budget, and select service hotels.

Economic Indicator Predictions for the Next Year

As the Federal Reserve continues efforts to quell inflation, there remains consensus that interest rates will continue to rise in the next year. Respondents to the RCLCO survey also weighed in on interest rates, as well as real estate factors such as cap rates, capital flows, homeownership and construction costs.

- Over half (57%) of respondents said that interest rates will increase at a moderate pace, while 9% predicted significant increases. 32% said that rates would stay flat or decline moderately.

- Cap rate forecasts closely follow interest rate expectations. 54% predicted a moderate increase, while 29% said that they would stay flat or decline.

- Respondents had a mixed view on inflation over the next year. The largest share (43%) believe that inflation will decrease moderately, 29% believe it will increase moderately, and 17% feel it will remain the same. There were far fewer predictions of large changes (negative or positive) than was the case at mid-year. There have been signs that the Fed’s actions have begun to curtail inflation, and as of November inflation of 7.7% was down from its summer peak of 9.1%.

- The majority (59%) of respondents predict that capital flows to real estate will decrease over the next year. This is more pessimistic than mid-year, when 38% predicted a decline.

- Over two thirds of respondents believe that the homeownership rate will fall. This is in-line with a recent NAR statistic that showed that in 2022 the median homebuyer’s age has increased to 53, as first-time homebuyers are increasingly pushed out of the market.

- The recent rapid rise in construction costs may be slowing or even reversing – 67% felt costs would fall or stay the same, while 33% felt they would increase – a more positive outlook than six months ago.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

Because it has a big impact on real estate valuation and debt costs, where do you think the 10-year treasury will be 24 months from now?

Source: RCLCO

RCLCO POV

The current RCLCO Base Case (~60% probability) is the U.S. GDP growth will slow in 2022 and 2023 to between 0% and 2% growth with the likelihood of a mild recession sometime in the next 12 to 18 months. Persistent inflation, high interest rates and weaker global growth will negatively impact the US economy. Real estate will not escape the negative impacts of the looming recession, and while there will be some buying opportunities, RCLCO does not expect widespread distress.

ECONOMIC CONDITIONS

Despite relatively strong labor markets and moderating energy prices and inflation, continuing aggressive Fed action is likely to curb demand in the near term. This together with weaker global growth will negatively impact the US economy, and to lead to a mild recession in the near-term. US GDP growth will be close to zero (0-2%) in 2022 and 2023. Depending on energy prices and supply chain issues, trend (2-3%) growth will likely resume in 2024. Job growth will moderate to 0-1 million (annual) in 2023 and 2024 and could turn negative for part of 2023. Job openings are at record levels despite early signs of moderation in August, indicating a mismatch between employer needs and employee skills.

The 10-Year US Treasury rose to 4.25% near the end of October but moderated to 3.4% in the first week of December in response to moderating inflation and recession worries. Respondents are more optimistic in the survey results above than economists and futures market traders who expect that the UST will remain elevated in the 4.0-4.5% range for the next several years. Real estate capital markets have materially slowed in 2H 2022. Real estate borrowing spreads have risen, as lenders price in more risk. Equity dry powder from institutions has declined due to the denominator effect. Transaction market expected to pick up in 2023 once prices reset at 10-20% below peak values. The FTSE Nareit U.S. Real Estate Index is down over 25% from its recent peak in 2021. On the private side, which tends to react more slowly to changing economic conditions, the NCREIF all property NPI index recorded negative appreciate of -0.37% in Q3 2022, the first negative appreciation return since Q2 2020.

REAL ESTATE OPPORTUNITIES

Over the last six months, cap rates have likely expanded as much as 50 to 100bps with fewer bidders and more re-trades. Bid/ask spreads have widened to 20% or more, with meaningful variation by property type and strategy (more for properties with long leases that do not grow with inflation). Institutional investors are confronting the denominator effect but are not wholesale sellers and continue to allocate capital to strategies with strong long term demand drivers (e.g. SFR). Exit queues are developing at ODCE funds and non-traded REITs, as values look rich.

Real estate sectors that should outperform over next several years include:

- Rental Housing – Job growth and high housing costs will keep multifamily and single-family rental demand high, although supply is ramping up and rent increases are moderating.

- Industrial – Demand should stay strong as e-commerce continues to expand and build out its supply chain.

- Niche Sectors – Health care (medical office, life sciences, senior housing), data centers, and self-storage have strong long-term demand drivers.

Caution is recommended for office and non-discretionary retail, as ongoing structural shifts are creating greater risk. In addition, pricing is currently more attractive in the public markets for these and other property types.

RCLCO recommends a cautious investment approach in 2023, as values are in flux. Values for many sectors will likely fall below replacement cost, creating buying opportunities, although some office and retail properties may have limited future usefulness. Strong fundamentals and long-term growth factors support selective development and refurbishment of rental residential, industrial, and some niche property types (hotel, senior housing, medical real estate, self-storage).Widespread distress selling is unlikely, except for office.

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. A majority (70%) of respondents have worked in the real estate industry for 20 years or more, with an average respondent tenure of over 25 years, and 79% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 44% of the sample. Another 21% are investors or capital allocators, followed by 7% in design or architecture firms. The remaining 28% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Disclosures:

RFA is a SEC registered investment advisor, collectively hereinafter (“RFA”). The information provided by RFA (or any portion thereof) may not be copied or distributed without RFA’s prior written approval. All statements are current as of the date written and does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation.

Research and Outlook Disclosure:

This information was produced by and the opinions expressed are those of RFA as of the date of writing and are subject to change. Any research is based on RFA’s proprietary research and analysis of global markets and investing. The information and/or analysis presented have been compiled or arrived at from sources believed to be reliable; however, RFA does not make any representation as their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated therein. There are no material changes to the conditions, objectives or investment strategies of the model portfolios for the period portrayed. Any sectors or allocations referenced may or may not be represented in portfolios of clients of RFA, and do not represent all of the securities purchased, sold or recommended for client accounts.

Due to differences in actual account allocations, account opening date, timing of cash flow in or out of the account, rebalancing frequency, and various other transaction-based or market factors, a client’s actual return may be materially different than those portrayed in the model results. The reader should not assume that any investments in sectors and markets identified or described were or will be profitable. Investing entails risks, including possible loss of principal. The use of tools cannot guarantee performance. Past performance is no guarantee of future results. The information provided may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that shown here. The information presented, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Market indices are included in this report only as context reflecting general market results during the period. RFA may trade in securities or invest in other asset classes that are not represented by such market indexes and may have concentrations in a number of securities and in asset classes not included in such indexes. Accordingly, no representations are made that the performance or volatility of the model allocations will track or reflect any particular index. Market index performance calculations are gross of management and performance incentive fees. The charts depicted within this presentation are for illustrative purposes only and are not indicative of future performance.

Copyright ©️ 2022 RCLCO. All rights reserved. RCLCO and The Best Minds in Real Estate are trademarks of Robert Charles Lesser & Co. All other company and product names may be trademarks of the respective companies with which they are associated.