June 23, 2022

RCLCO’s Real Estate Market Sentiment Survey has tracked confidence in U.S. real estate market conditions for over 10 years. The last two years have been unprecedented in many ways – resulting in more significant swings in sentiment (both positive and negative) than we have seen since the survey inception. The current index experienced its largest decline in Mid-2020 due to the speed and intensity of the economic downturn sparked by COVID-19, hitting its lowest level in the history of the series (9.2). One year later the index swung back dramatically to 89.1 by Mid-2021 as the nation reopened, vaccination rates rose, and the economy and real estate markets moved toward recovery. After a slight decline at year end 2021 driven by lingering COVID concerns and supply chain disruptions, the future index made a sharp decline in Mid-2022 to 35.1, as geopolitical uncertainty persistent high levels of inflation and Fed action have raised concerns about the risk of an impending economic recession.

Key Takeaways

- The RCLCO Current Real Estate Market Sentiment Index (RMI)[1], which measures sentiment on a 100-point scale, has decreased 47.0 points over the past six months, from 82.1 at YE 2021 to 35.1 at MY 2022, just slightly above the level of 30 which typically coincides with periods of real estate market distress/recession.

- Respondents predict that real estate market conditions will continue to deteriorate over the next 12 months, with the Future RMI dropping 10.2 points to 24.9 – this would bring sentiment into market distress/recession territory.

- Just over half of survey respondents (58%) believe real estate conditions will get moderately or significantly worse in the next 12 months.

- Almost all of respondents (92%) believe that there will be a recession in the next two years, with 54% believing it will occur in the next 12 months, and 38% believing it will occur 13-24 months from now.

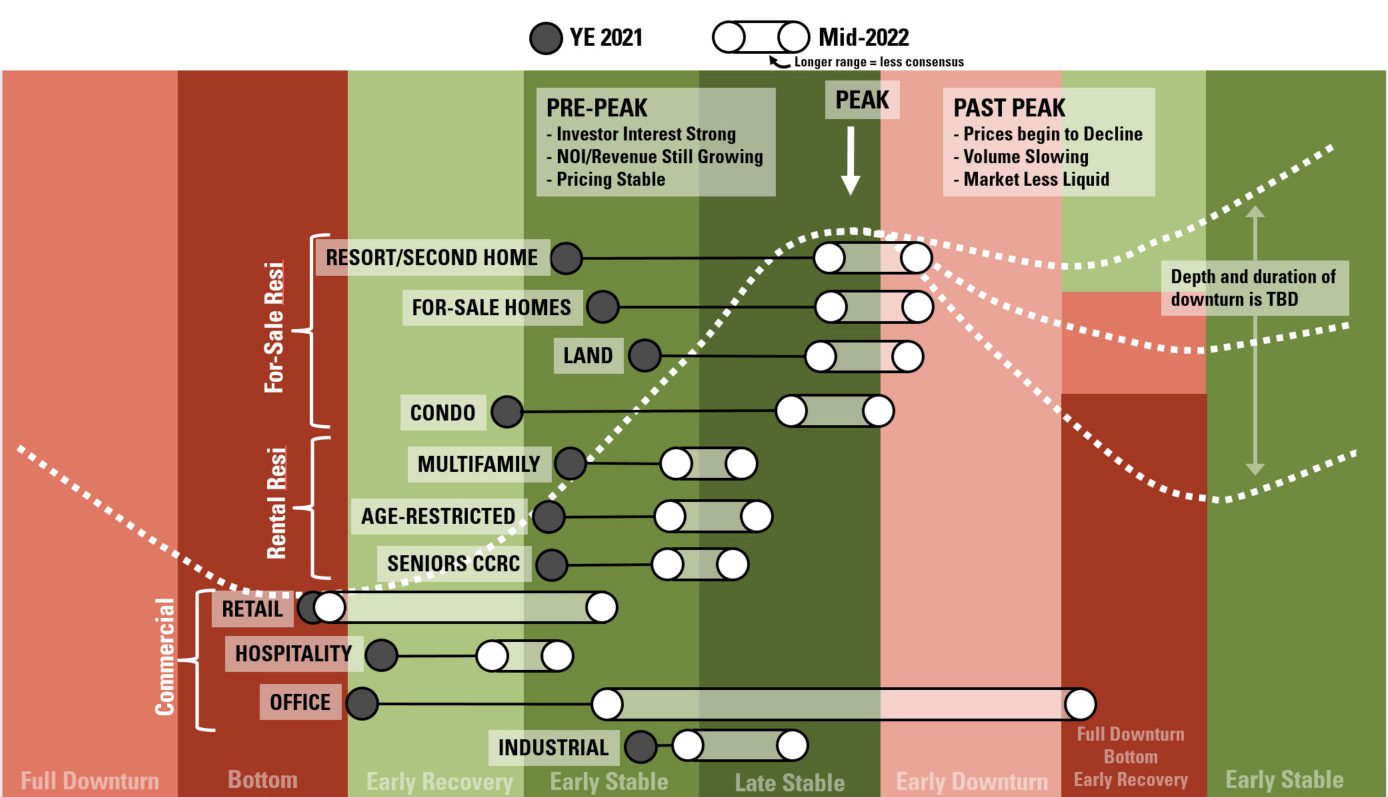

- For-sale housing remained in the expansionary phase of the cycle, but an increasing number of respondents indicated that this sector was reaching the peak, or had already crossed over into the early downturn phase. Rental housing was still firmly in expansion mode, but more respondents believed that this sector had moved from the early to late stable phase of the cycle indicating that the apartment sector may be approaching a peak.

- There was much less consensus surrounding the cycle stage of the commercial real estate sectors. Many felt that hospitality and industrial were in in the stable phases of the cycle, while there was wide variation in retail and office with respondents all over the map from early downturn to early recovery, early stable, and even late stable, perhaps reflecting the high level of uncertainty in the overall economy.

- Looking ahead, a majority of respondents expect interest rates and cap rates to rise. Respondents were split about inflation – with a mix of opinions if it would decrease or increase in the coming year, but with more expecting elevated levels of inflation over the coming year by about a 2-1 margin. Overall respondents felt capital flows to real estate and homeownership rates would fall, perhaps consistent with the pessimistic outlook for the economy.

ESG Snapshot:

- Approximately 38% of respondents have some form of an ESG (Environmental, Social, and Governance) Policy in place. Of those, approximately 75% have an identified “champion” for ESG initiatives at the leadership level.

- A significantly larger share (55% to 61%) of firms who utilize public or institutional capital sources have ESG initiatives than those who do not.

- The top three reasons for exploration or adoption of ESG-related policies, in order of importance, are:

- Alignment with Company Values

- Positive Community Impact

- Part of Fiduciary Duty

Sentiment Drops – Past Two Years have been Volatile and Unprecedented

The RMI index has had a series of dramatic peaks and valleys during the Covid-19 Pandemic and War in Ukraine, factors which have led to continual supply chain issues, inflationary woes, and increasing energy costs. Sentiment at Mid-Year 2021 was exceptionally optimistic at 89.1, reflecting an initial wave of confidence in what has been a recovery characterized by fluctuating conditions. After a slight decline at year-end during the initial Omicron wave, sentiment took a more pronounced dive at Mid-Year 2022 dropping to 47 points to 35.1, well below the long-term average of 68.0. This drop comes during persistent inflation, geopolitical instability, and ongoing issues relating to the supply chain and soaring energy prices. Mortgage rates have surpassed 5.0%, their highest level since 2009, which has begun to put a damper on the previously resilient for-sale housing market. Growing inflation continues to eat into consumer spending power, and the Fed’s monetary policies aimed at curbing inflation are simultaneously threatening to tip the economy into contraction – all factors that prompted survey respondents to predict a recession occurring at some point over the next two years.

RCLCO National Real Estate Market Index

Source: RCLCO

The current index at 35.1 remains somewhat above the level of 30, below which is typically coincident with periods of economic distress or recession, and was a more sizeable drop than was predicted at year-end. Looking forward, respondents predict that the index will decline by an additional 10.2 points over the next 12 months, ending the year at 24.9, firmly in the distress/recession zone. Despite this, the labor market remains strong (428,000 jobs were added in April), but consumer spending is beginning to show early signs of running out of steam. The most recent credit card data show that spending in May was just 10% higher from the same month last year, according to a Barclays report. For the rest of 2021, that monthly spending growth had averaged more like 20%. This is consistent with the most recent consumer expenditure data that showed retail purchases fell 0.3% in May from the month before, the first decline this year. So the waters are very choppy indeed.

How Would You Rate National Real Estate Market Conditions Today Compared with One Year Ago?

Source: RCLCO

Over half (58%) of respondents indicated that national real estate conditions were moderately or significantly worse when compared with one year ago. The majority of those respondents felt that real estate market conditions are somewhat worse than last year, and only a small share felt things had gotten significantly worse. This signals that while 2021 showed a rapid and strong recovery, that it may have been short-lived as we enter 2022 with more pessimistic predictions.

Browse Past Sentiment Surveys

The outlook for the upcoming year predicts a more gradual decline. Approximately 67% of respondents predicted that national real estate market conditions would continue to get “moderately” or “significantly” worse in the next year. The remaining third of survey respondents were equally split between unchanged or improving conditions.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

The sentiment survey has been prone to large swings in the past, and we believe given the timing of the survey in early June that respondents are still processing many of the more recent announcements around persistent inflation, interest rates, and slowing GDP growth.

Recession Forecast

The vast majority (92%) of respondents feel that a recession will occur, defined as two consecutive quarters of negative GDP growth, at some point in the next two years. Over half of respondents (54%) believe that this recession will occur within the next 12 months. While many factors are in play that indicate a recession is becoming more likely over the next two years, it remains to be seen how deep or prolonged this recession will be, especially on the real estate industry.

When Will the Next U.S. Recession Occur?

Source: RCLCO

Uncertainty in Cycle Stages

There was considerable variation in the sentiment regarding position of various real estate sectors on cycle at Mid-Year 2022 compared with previous surveys, perhaps reflecting the uncertainty and concern about a potential looming U.S. recession. The range of responses in the Mid-Year 2022 survey are reflected in the chart below by the white circles – the longer the bar, the higher the variation in responses. Not surprisingly, sentiment around the for-sale land uses has declined somewhat as many feel that high prices coupled with increasing mortgage rate have moved these sectors into either late stable or early downturn. Rental residential has fared better, with many indicating that this sector is likely to be more resilient. There was much more variation in the sentiment regarding various commercial uses. Many felt that hospitality and industrial were in in the stable phases of the cycle, while there was wide variation in retail and office with respondents all over the map from early downturn to early recovery, early stable, and even late stable, perhaps reflecting the high level of uncertainty in the overall economy.

Cycle Stage Movement over Past Six Months

- Residential for-sale uses including resort/second home, for-sale homes, land, and condo all appear to be in the stable phases, however respondents are increasingly indicating that this sector may have reached or surpassed the peak– as a combination of high pricing and high mortgage rates has led to some slowing in the sector.

- Rental residential uses including multifamily apartment, seniors CCRC, and age-restricted rentals have relative consensus around being the expansionary stable phases.

- Retail was a sector with less consensus, some feel it has not yet emerged from the bottom of the cycle, while others feel it is in an early recovery or early stable phase. The sector is evolving to adapt to new market conditions, but in many cases a return of consumer to experiential type uses (restaurant, entertainment, etc..) has helped to bolster the sector, though a more recent pullback in consumer spending has also caused retail to falter.

- Hospitality continued to move ahead into early recovery and early stable phases as more travel restrictions lift and willingness and spending on travel increases.

- Office was the sector with the least consensus – despite moving into early recovery last cycle, respondents feel that it is anywhere between early stable to full downturn this cycle. The return to work has been inconsistent with more companies becoming open to the idea of hybrid work or remote work, which has many companies reevaluating their longer-term office space needs.

- The industrial sector remains in the stable phases, as pricing has increased and the sector is showing signs of moving closer to peak.

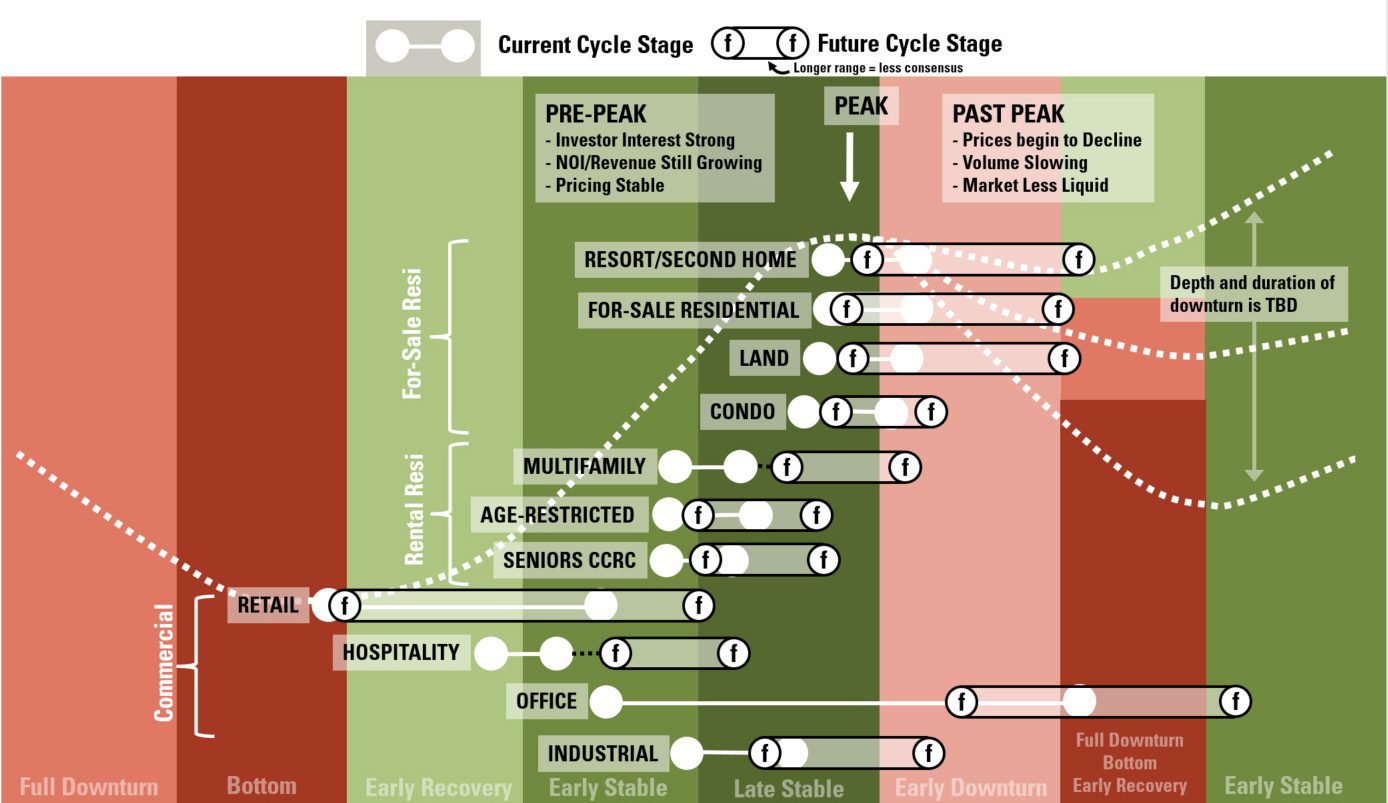

More Land Uses predicted to move Past Peak in Coming Year

Looking forward, many of the for-sale residential sectors are predicted to move into early downturn, though there is some indication that it may be a shallow cycle as a share of respondents also indicate these sectors may be in early recovery within 12 months. Many of the rental residential sectors are anticipated to continue to move along in expansion, with rental apartments being the furthest along of those sectors with a possibility of early downturn over the next year. Commercial uses continue to show mixed sentiment, though encouragingly hospitality continues to show expansion.

Expansion of Most Product Types in the Upcoming Year

Economic Indicator Predictions for the Next Year

With the Fed’s announced plan interest rate increases, there remains significant consensus that interest rates will rise in the next year. Over half (55%) of respondents feel interest rate increases will be moderate, while 35% feel increases will be significant. These rate hikes are intended to help curtail inflation, though respondents had a relatively mixed view on how this would impact inflation over the next year. About a quarter (26%) feel inflation will decline, 7% believe there will be no change, 40% feel it will increase moderately, and another quarter (27%) feel it will increase significantly. Respondents were less bullish than they were in 2021 relating to capital flows to real estate; previously there was consensus that capital flows would increase, and now in Mid-2022 the group is relatively split between capital flows decreasing (38%), staying the same (33%), or increasing (25%). The for-sale market has begun to see impacts from mortgage rate hikes and only 13% of respondents, a much smaller share than at year-end, believe the homeownership rate will continue to rise. One area where the survey had more consensus this time around was with future cap rate levels, 55% believe rates will increase moderately, while 7% feel they will increase significantly.

What Do You Expect to Happen with the Following Economic Indicators Over the Next 6 to 12 Months Nationally?

Source: RCLCO

RCLCO POV

- The current RCLCO Base Case (~60% probability) is the U.S. GDP growth will slow in 2022 to between 0% and 2% growth with the likelihood of a shallow recession sometime in the next 12 to 18 months. High inflation, rising interest rates and weaker global growth will negatively impact the US economy. Depending upon energy prices and supply chain issues, grow will return to trend (2% to 3% growth) in 2024.

- Annual job growth will moderate to 1.0 to 1.5 million in 2023 and 2024, but not turn negative. Job openings are at record levels, indicating a mismatch between employer needs and employee skills.

- The yield on the 10-Year U.S. Treasury has risen to 3.2% as of mid-June following an above consensus May inflation report. Economists and futures markets expect that the UST will remain in the 3.0% to 3.5% range for the next several years.

- As the economy slows, U.S. real estate fundamentals will likely soften, with slightly higher vacancy rates and slower rent growth over the next three years. Industrial rents should stay strong while office and neighborhood retail rents will trend towards 0%.

- Real estate capital markets are likely to stay resilient. Real estate borrowing spreads have risen post-Ukraine, as lenders price in more risk. Equity dry powder from institutions has declined due to the denominator effect, although non-traded REITS continue to expand.

- Higher borrowing rates have led to bid/ask spreads and modest price declines (5%-10%), but large decreases are unlikely.

We will share more details on RCLCO’s POV on current economic conditions during the webinar.

ESG Snapshot

RCLCO added a special ESG segment to the Sentiment Survey as a way of taking the pulse of the real estate industry’s interest and adoption of ESG-related initiatives. There will be a special advisory on this topic released later this year, but we are including a few sneak peek findings from the survey data in this advisory article. We initially asked about how many companies currently have an ESG policy in place, while 38% of overall respondents indicated that they did – we saw significant variation across organizations that rely on public or institutional capital, versus those who do not. A meaningfully larger share (55% to 61%) of firms who utilize public or institutional capital sources have ESG initiatives compared with firms that do not.

Does Your Organization Have an ESG Policy in Place?

Source: RCLCO

Survey participants indicated their top reasons for adopting or considering ESG policies are cultural, that is, that they align with company values, and have a positive community impact. Surprisingly, cultural factors ranked higher than financial factors including maximizing value and risk-mitigation, which may indicate the risks of ignoring ESG principles are underappreciated in the market. We’ll drill into this and more in our special ESG advisory.

Please Rate the Degree to Which the Following Factors Have Led Your Firm to Explore or Adopt ESG-related Policies or Practices

Ranked by Level of Influence (Higher Value is More Important)

Source: RCLCO

Who Took the Survey?

RCLCO’s Real Estate Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and the industry. A majority (84%) of respondents have worked in the real estate industry for 20 years or more, and 82% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 42% of the sample. Another 21% are investors or capital allocators, followed by 8% in design or architecture firms. The remaining 29% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

Learn More About the Results

During our live round-up webinar in June 2022, Managing Director Charlie Hewlett, RFA Managing Director Cyndi Thomas, and Principal Kelly Mangold discussed the results of this Mid-Year Sentiment Survey, addressing RCLCO’s in-depth point-of-view, and with a high-level look into the initial findings of our first ESG survey. Click the button below to watch a recording of the webinar.

For management consulting services or more information about our strategic planning group contact Joshua A. Boren.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.