RCLCO’s Mid-Year 2020 Sentiment Survey: A Deep Plunge, but Some Sectors Coming off the Bottom Already

Headlines from this article:

- The RCLCO Current Real Estate Market Sentiment Index (RMI) plunged as expected in mid-2020, to a low 9.2, and the Future RMI, now at 36.8, calls for some continued declines in conditions, but also the beginnings of recovery in a few sectors, within a year.

- Industry leaders see the severe declines as being behind us, but some sectors still face a moderate downside. Only a relatively small percentage (<16%) believe the markets will be “significantly” worse over the next 12 months.

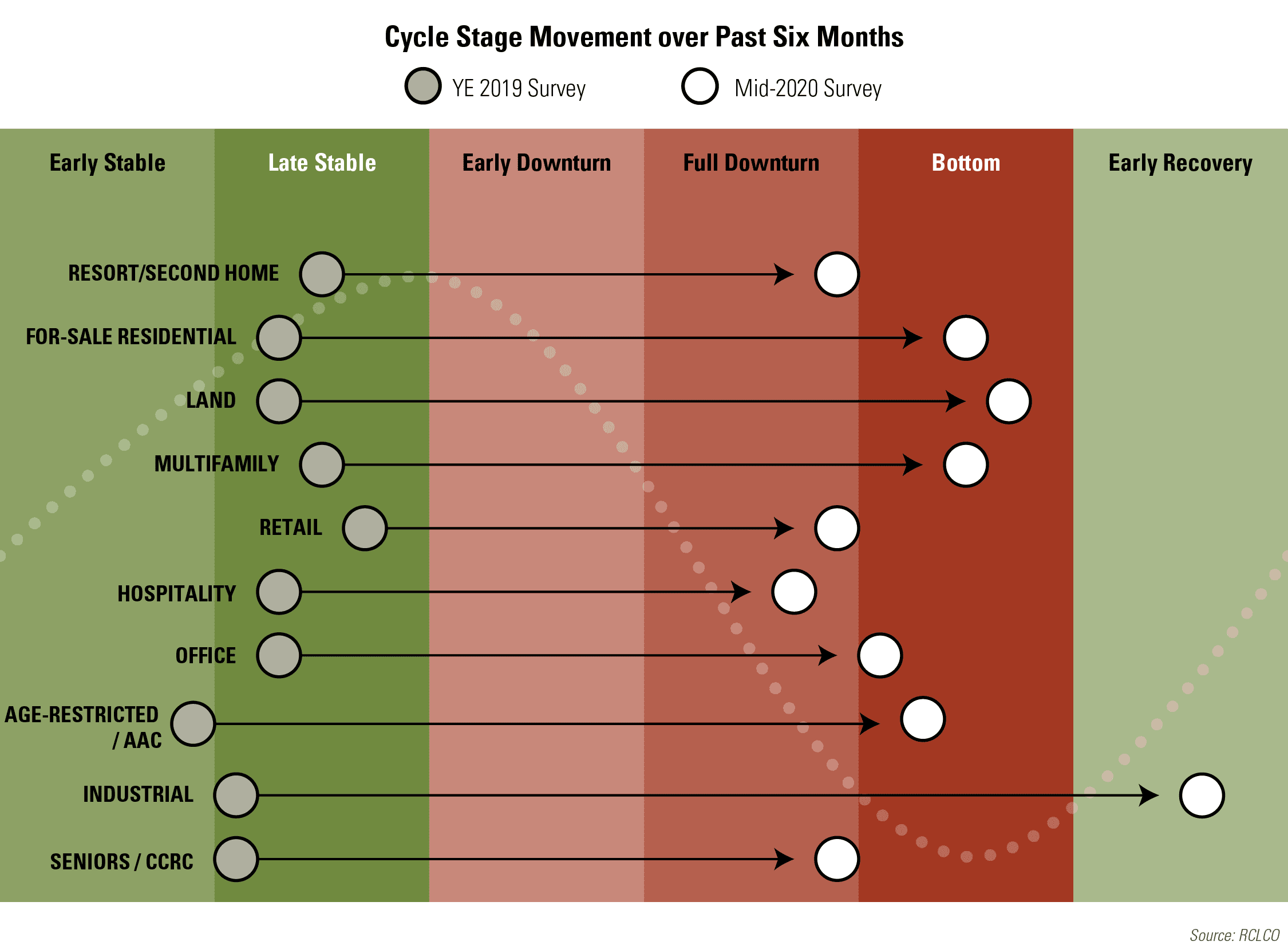

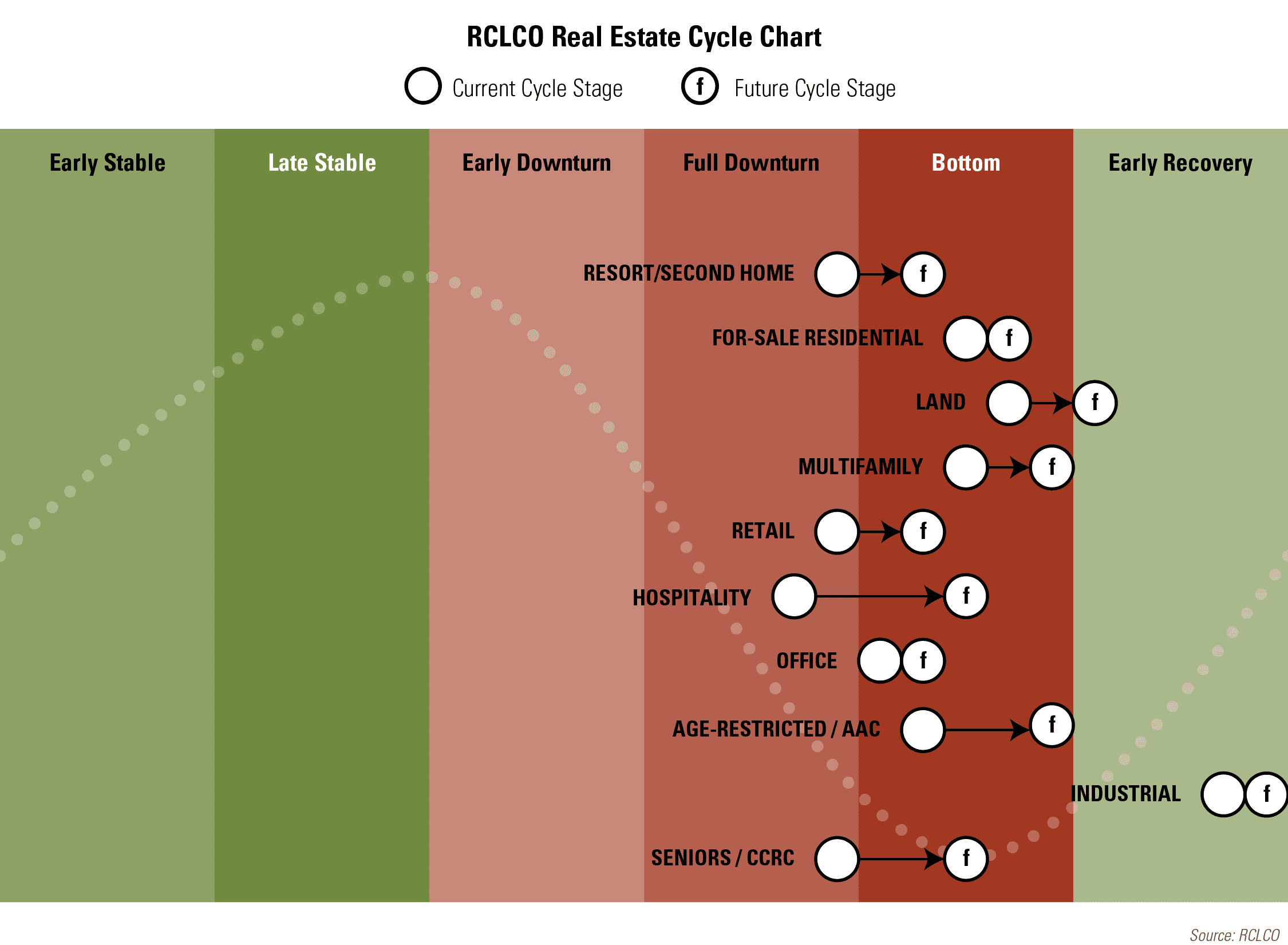

- Most believe that the multifamily rental, active adult, and for-sale residential sectors have already hit bottom, along with land; although the second home/resort, and seniors housing (IL, AL/MC) sectors are still in full downturn mode and may have some time before hitting bottom.

- Within the next twelve months, homebuilders, subdivision developers, and master-planned communities are expected by the largest number of participants to be past the downturn and well into “stable” business conditions. This is consistent with RCLCO’s expectations that strong household formation rates will resume, driving demand for new homes.

- Respondents believe that the hospitality sector is approaching or at the bottom, with luxury and resort hotels the most commonly believed to be in “full decline” or at “bottom.” The largest number of respondents believe that recovery will begin within a year in the hotel business.

- The retail sector was mostly seen in “full decline” in June, but there is a wide variation between secondary regional malls (considered to be in the worst shape of all), and grocery-anchored community/neighborhood centers, which are viewed as holding up well.

- The office market is still seen in decline, and there are varying opinions among participants as to the chances of recovery within the next year, reflecting uncertainties about the economy and the durability of the work-from-home trend.

- The Covid-19 pandemic has provided a boost to the industrial space market, due to increased demand for deliveries during lockdown. Cold storage and last-mile warehousing are particularly strong.

It is perhaps not surprising that the upward trajectory of the RCLCO Real Estate Market Index (RMI) that had resumed in 2019, was completely upended with the mid-year 2020 survey results, a direct result of the economic shutdown and social distancing rules imposed in response to the Covid-19 pandemic. The U.S. economy and job markets have been in full-blown downturn mode over the past several months, but may be finding the bottom now, and the economy and real estate markets (with some notable exceptions) are expected to return to growth mode over the next several quarters.

Overall Sentiment Turned Dismal, but the Outlook is Brighter

The Current RMI fell into the basement to a value of 9.2, the lowest level since RCLCO began recording the index at the end of the Great Recession. The previous low was recorded in Q4 2018 at 37.5 in the wake of the U.S. Federal shutdown that occurred in December 2018. Prior to the coronavirus pandemic, in Q4 2019 the index was just under 65.0. RMI values in the 60 to 70+ range are typically indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession. The nearly 56-point drop in so short a period mirrors the speed and depth of the damage that the pandemic has wrought upon the U.S. economy and real estate markets.

RCLCO National Real Estate Market Index

Source: RCLCO

If there is a silver lining, it is that respondents expect that conditions will improve significantly over the next 12 months. The RCLCO Future RMI dropped somewhat from the Q4 2019 reading of 52.3 to 36.8, down more than 15 points, and so there is some optimism that the worst of the downturn may be behind us, and market participants are anticipating much better market conditions a year from now.

How Would You Rate National Real Estate Market Conditions Today Compared With One Year Ago?

Current U.S. Market Sentiment over Time

Source: RCLCO

The change from the last survey is striking, with nearly 90% of respondents indicating that national real estate market conditions have gotten moderately or significantly worse compared with one year ago. This is a dramatic shift from the last survey at the end of 2019 when only 13% of respondents indicated that the market was only moderately worse than the previous 12-month period.

In addition to reflecting upon the past year, respondents were asked to predict how the U.S. economy and real estate markets would perform over the upcoming year. In most prior years, respondents have tended to predict that the U.S. economy and real estate markets would be in worse shape a year into the future—probably a reflection of late-cycle angst. Today there appears to be a high degree of uncertainty about the likely trajectory of the markets. The RCLCO Future RMI stands at 36.8, which is barely above the recession-level benchmark of 30, and there are twice as many respondents (60%) who believe the markets will be moderately or significantly worse one year from now than those that predict improving market conditions (30%).

The graph below shows the change in market sentiment over time, splitting out the responses saying that things would get worse, better, or stay the same. This graph combines together the responses saying that conditions will become “moderately worse” with those saying things will get “significantly worse,” but the reassuring thing is that the moderate responses (in both directions) far outweigh the “significant” changes.

12-Month U.S. Real Estate Market Predictions over Time

Source: RCLCO

Again, in search of a silver lining, it is perhaps comforting that only a relatively small percentage (<16%) believe the markets will be “significantly worse” over the next 12 months. In summary, these industry leaders see more adjustment ahead, but they see the severe declines as being in the rearview.

A Leap to the “Bottom”

Survey respondents universally believe that every major real estate sector has jumped from expansion to contraction in the first half of 2020. The exception is industrial, and particularly the big box warehouse, logistics, cold storage and last-mile distribution sectors, which have not been impacted in any meaningful way, and in fact, may have seen an increase in demand as e-commerce sales and home delivery have seen a surge in the pandemic. Most believe that the multifamily rental, active adult, and for-sale residential sectors have already hit bottom, along with land; although the second home/resort, and seniors housing (IL, AL/MC) are still in full downturn mode and may have some time before hitting bottom.

The majority of respondents indicate that the hotel sector is still experiencing declining market fundamentals, although the largest share of predictions by our panelists see the sector starting to recover within a year. This is consistent with the data that shows improving (albeit still historically low) hotel occupancy rates and increasing TSA checkpoint travel data that indicates that Americans are beginning to travel again (but again, still at levels far below that of previous years).

The office sector is judged at this time to be just hitting the bottom and is expected to remain at the bottom into the next 12 months as the economy struggles to get completely back to work. However, NCREIF data released this past week indicates that office rent collections in the private open-ended fund world actually improved in June (though June 15th) 2020 compared with May, and are above 91% collected.

Retail continues to struggle, and survey respondents expect this sector to remain in “bottom” conditions into 2021. While NCREIF reports that rent collections in this sector have improved since May, this sector lags all other real estate food groups with rent collections under 60% so far in the month of June.

Multifamily rental apartments are holding up well so far in this crisis, but there are concerns about rent collections continuing after some of the government relief programs start to expire. As noted above, multifamily is believed to be at “bottom” already, and is expected to be in or near an improving status in a year’s time.

Consistent with the expectation that the for-sale residential sector will be relatively close to “early recovery” mode in a year, RCLCO has learned from its master-planned community developer and homebuilder clients that sales and traffic rebounded strongly in May and June, after dropping precipitously in the early stages of the pandemic in mid-March through early April.

A Mixed Bag by Sector

We noted that this June 2020 survey portrays a snapshot in time. It does also capture an inflection point. Several respondents indicated that we are at the “bottom,” particularly in hospitality and retail. It also paints a picture of a mixed bag, with some types of real estate still in decline and just a few that might be getting to the other side, starting “early recovery.”

The survey results are an aggregation of sentiment about many different types of real estate, some with brighter prospects than others in the immediate term. Retail is in a serious downturn and still headed lower, while residential real estate is in fairly good shape, with more strength expected in the year to come. Even within retail, there are some types that are weaker than others.

As shown in the aggregated table above, 31% expect the hospitality industry to be in “early recovery” a year from now, a higher percentage by a wide margin than other sectors. Hotels were among the hardest-hit businesses, but once there is any uptick in travel, they will start to do better, although full recovery will certainly take some time.

Rental Housing

Rental housing overall is not seen as being in as bad shape as commercial real estate, placing it in “late stable” to “early downturn” status. This sector has maintained high occupancy rates, and surprisingly high rates of rent collection, even with rent forbearance and restrictions on evictions.

Rental Housing Today

Source: RCLCO

There is still some caution however surrounding large numbers of unemployed tenants and what may happen when government supports start to expire. Although some participants indicated that rentals are in “early recovery” already, many more expect rental housing to be in “early recovery” twelve months from now. This is all consistent with RCLCO’s reconnaissance suggesting that residential will come back more quickly than commercial. Single-family rental is expected to be “early stable” or “late stable” by a year from now. Interestingly, though, a small subset of the respondents (4.2%) believe that SFR will be in a “full downturn” in a year.

Rental Housing 12-Month Predictions

Source: RCLCO

That small minority who see SFR being at the “bottom” today (4.5%) are a much smaller minority when projecting out a year from now (1.8%), and there is a similar-sized shift to “early recovery” within the next 12 months (13.0% today rising to 15.4% in a year), which suggests an expected improvement.

For-Sale Residential

The for-sale housing sector went through a short pause in March and April, and then strengthened rapidly in May and June. As a consequence, the June survey reading for this sector is spread between “late stable” and “early downturn.” Separate from this survey, RCLCO is hearing builders say that May was an “amazing” month in terms of the strength of sales, with a few saying that May was their best month ever. This sentiment seems to have continued into June.

For-Sale Residential Today

Source: RCLCO

In the residential category, of the various business types, “land-owner” has the highest number saying that it is at the “bottom,” but the largest share think that land owners are in “late stable” or “early downturn” status. In the homebuilder category, 10.4% say they are in “early recovery.”

Within the next twelve months, homebuilders, subdivision developers, and master-planned communities are expected by the largest number of participants to be past the downturn and well into “stable” business conditions. This is consistent with RCLCO’s expectations that strong household formation rates will resume, driving demand for new homes.

For-Sale Residential 12-Month Predictions

Source: RCLCO

Industrial

A plurality of respondents consider the industrial sector to still be stable, overall. Big-Box/Warehouse/Logistics space is judged by 30.7% to be in the “late stable” stage, with the second-highest percentage saying it is still in the “early stable” stage, nowhere near a downturn.

Industrial Today

Source: RCLCO

The Covid-19 pandemic has provided a boost to certain facets of the industrial space market, due to increased demand for deliveries during lockdown. Cold storage and last-mile distribution are doing well, and expected to continue to do particularly well in the year ahead. All the other industrial uses are seen as improving further as well, with even more respondents shifting the expected reading past the “bottom” and into “recovery” and “stable” phases.

Industrial 12-Month Predictions

Source: RCLCO

Retail

The grocery-anchored community center segment has fared the best of any retail segment. In fact, many grocery stores have experienced increasing sales as locked-down households shifted food dollars from eating at restaurants to eating at home. However, most other retail categories are under considerable stress. Fortress malls are considered to be in decline, with nearly 65% of respondents indicating that this segment is in some phase of “downturn.” Only 15% believe these massive centers have already hit bottom. Secondary regional malls are in the worst shape among shopping center types, according to respondents. The most common assessment, by a wide margin, was that this property type is in “full downturn,” at 51.3% of respondents. The second-most-common answers were “bottom” and “early downturn,” in approximately equal shares, at 15.7% and 16.5%, respectively. Looking one year into the future, more respondents (24.7%) expect the secondary malls to be hitting the bottom. A few (5.0%) think the secondary malls will be starting the next “early recovery.”

Big box and power center retail is considered now to be in “early downturn” (27% of respondents), or in “full downturn” (22%). Only 14% think it has already bottomed, implying more distress to come. Lifestyle, outlet, and High Street retail are all considered to be in “early downturn” status.

Retail Today

Source: RCLCO

Looking forward, our respondents believe that fortress malls will be at-or-closer-to-bottom one year from now. Approximately 20% said that they would reach the bottom a year from now. Interestingly, about the same percentage say that fortress malls are in “full-downturn” mode as say that they will be in “full-downturn” a year from now. Any way you slice it, these mega-malls are expected to experience major problems over the next twelve months. Power Centers are expected one year from now to still be in “full downturn” (19%) or at the bottom (17%), but there were about as many respondents who chose “don’t know” (17%) as anticipate a “bottom” (17%) in mid-2021, suggesting pessimism mixed with uncertainty about the status of this sector a year from now. Most expect grocery-anchored centers to be back to growth mode one year from now.

Retail Future (12 Months) Cycle Status

Source: RCLCO

Office

Office real estate is in “early downturn” mode, except for offices dedicated to medical and life sciences, which are performing well on average. Class-A office is in “early downturn” according to 45% of survey participants, and in “full downturn” according to a smaller group (13%). Class-B offices are much worse off, with nearly 19% of respondents judging them to be in “full downturn” and 37% saying they are still in an “early downturn.” Structural obsolescence in older office buildings will create an obstacle for value recovery in Class-B structures. Fewer than 10% think that either Class-A or Class-B is at the bottom now. Co-working is in “full downturn” (30%) or in “early downturn” status (27%). RCLCO believes that this type of office space does have a future, given its inherent flexibility to adapt to rapidly-changing space needs, but that the next year will be dicey. Creative office space is in “early downturn” according to 34% of respondents, and in “full downturn” according to 11%. The same percentage say that it is in the “early stable” stage as say it is at the “bottom” (8% for each).

Office Current Status

Source: RCLCO

Over the next twelve months, respondents expect Class-A, Class-B and creative offices to move into the next phase of the cycle, but they do not agree on what that means. For some of our industry panelists, it means dropping from “early downturn” to “full downturn” or from “full downturn” to “bottom,” but for some who reckon that we are already at the “bottom” today, they move their expectation upward, to “early recovery.” This divergence of expectations speaks to the uncertainties regarding how many workers will work from home in the years ahead and how managers and developers will have to adapt to changing health needs. Meanwhile, medical office is projected to make a clear move to stronger and more stable market conditions.

Office 12-Month Predictions

Source: RCLCO

Hospitality

The verdict is decisive for the hotel industry. Respondents judge the hospitality sector to mostly be in either “full downturn” or at the “bottom.” The business/luxury hotels and the resorts are the hotel types that are considered to be most clearly at or near the bottom. Participants consider extended stay hotels are better off, with a larger share in the “late stable” realm. Home sharing/AirBNB/VRBO is considered to be deep into decline or at the bottom, but is also heavy in “don’t know” responses, reflecting the uncertain future of this type of real estate.

Hospitality Current Cycle Status

Source: RCLCO

The graph below shows the future expectations for the hospitality industry, and suggests that the sector will come off the bottom and be in “early recovery” within a year.

Hospitality Future (12 Months) Cycle Status

Source: RCLCO

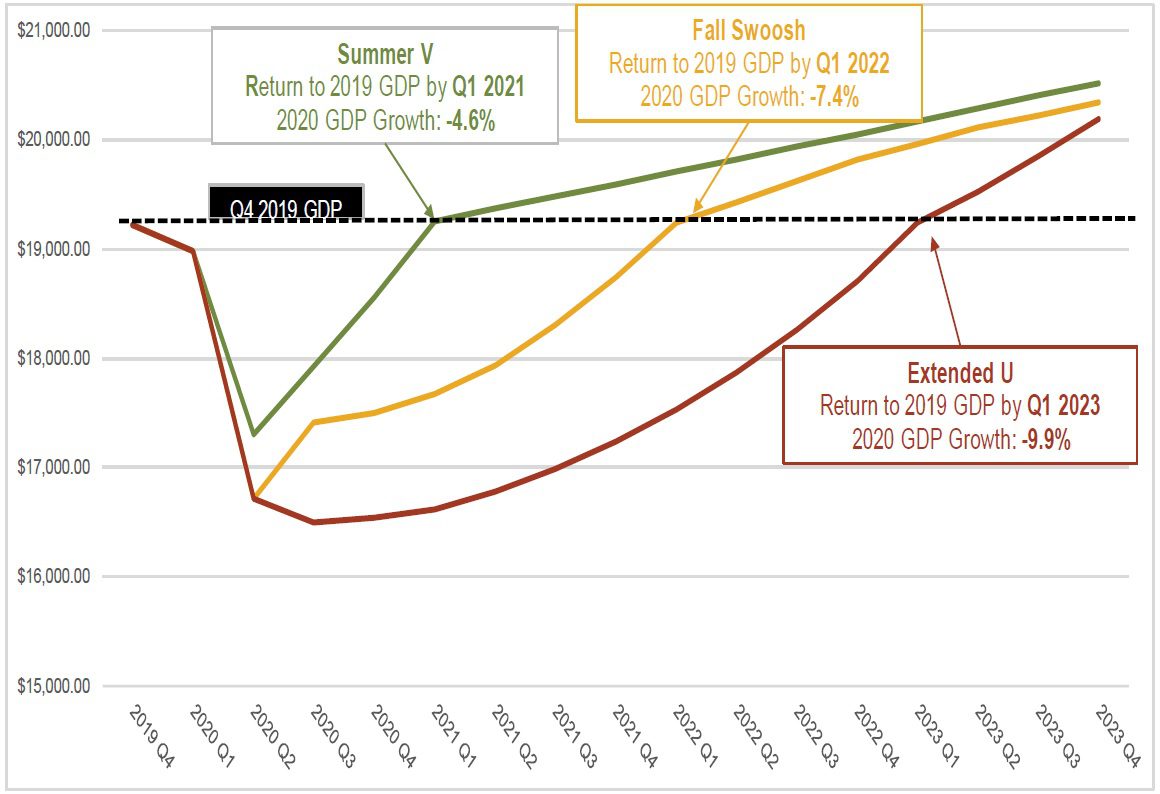

Fall Swoosh Economic Recovery

A majority (57%) of RCLCO Sentiment Survey respondents believe the “Fall Swoosh” downturn and recovery scenario is the most likely trajectory for the U.S. economy. Only 10% believe that a relatively quick “Summer V-Curve” is any longer in the cards; and a fairly sizable share (26%) are not ruling out an “Extended-U” scenario that would entail a longer and potentially deeper downturn.

Forecast Scenario Responses

Source: RCLCO

RCLCO Recovery Scenarios

Source: RCLCO

These results are consistent with the current RCLCO point of view (POV). Under the “Fall Swoosh” scenario, the U.S. economy is expected to experience a partial snap-back in H2 2020 as states begin a staged re-opening, but regional differences in the trajectory of the coronavirus hot spots force governments (especially in the South and West) to keep restrictions in place longer and suppress consumer confidence, which leads to a slower recovery. Unemployment likely peaks in Q2 2020, but remains elevated and is slower to come down. In this baseline case, U.S. GDP for 2020 is likely to decline -7.4% overall, with Q4 2019 levels of economic activity not reached again until Q1 2022, and full employment is regained by 2023.

Impact on Real Estate

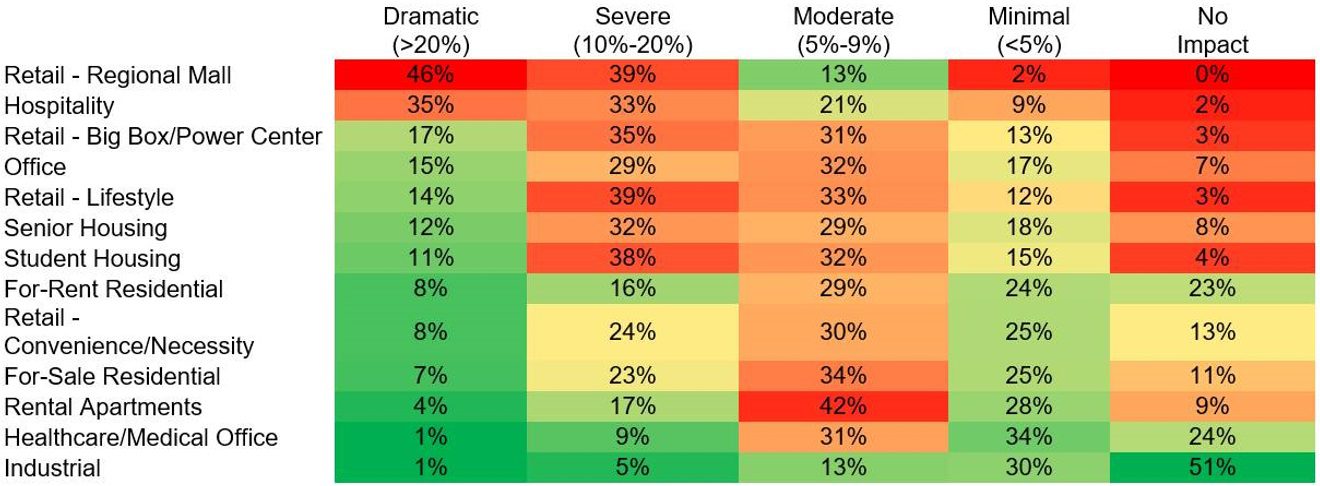

Most respondents said that the impact of their chosen forecast pattern on various sectors of real estate would range from “moderate” to “severe.” “Moderate” was defined as a 5%-9% negative impact on NOI, prices, or valuation, and “severe” was defined as a 10%-20% reduction in NOI, prices, or valuation. A “dramatic” impact was defined as a reduction greater than 20%.

Across the for-rent residential categories, for the most part, affordable/subsidized housing was judged to be unaffected by the forecast, and that was true of single-family for-rent as well. This is consistent with the way we at RCLCO see things playing out as well. Rental apartments are expected to see only a “moderate” effect from the economic swing. Student housing is expected by the largest group to suffer a “severe” impact from the economic scenario. Seniors housing and co-living both had the largest number (by a wide margin) of respondents saying “don’t know,” reflecting the high level of uncertainty and risk associated with those uses. In the office category, Class-A offices are expected to have a “moderate” reaction to the economic situation, but the impact on co-working is expected to be “dramatic.” In the retail category, the impact of the economic cycle on secondary regional malls is judged to be “dramatic” (47.0% of respondents). Meanwhile, grocery-anchored community/neighborhood centers will feel a “minimal” effect.

The following exhibit summarizes various sectors at a glance.

Source: RCLCO

Impact on Capital for Real Estate

Respondents were asked, based upon the economic forecast scenario they selected as closest to their own, how that scenario would likely affect their ability to secure capital for their real estate activities. Most said that there would be “sufficient,” but not “abundant” capital. The greatest shortfalls are expected in securing equity for planned new developments, with 47% expecting “limited availability.”

Funding Availability Responses

Source: RCLCO

Only 6% said that there would be abundant availability for equity for new developments. Ongoing construction is widely expected to continue to get funding, with 64% saying that there would be sufficient availability of money. Construction debt for new planned developments is seen as being available on a limited basis.

These results are generally in line with our experience from our consulting work, in which projects are being held to tougher underwriting standards, but the good projects are getting funded. Had we asked how this differs for the various real estate sectors, we would have expected to hear that industrial, particularly the big box segment, has hardly skipped a beat, but that any new project with a hotel or retail component has been delayed. And in just the last few weeks, we have learned that transaction volume in the favored multifamily rental sector, which had dropped to nearly zero in the early stages of the pandemic, is starting to make a strong comeback, and that many of the deals that had been pulled from the market in Q1 and Q2 2020 are likely to come back to the market in H2 2020, with very little, and for some of the best assets no, repricing. In the homebuilding space, while many builders sharply curtailed the number of spec homes started, many MPC and land developers continued with lots under development, and while many decided to delay the next phase of lots until there was better clarity on the impact of the pandemic, many have pressed forward with new phases as sales have snapped back to trend line.

RCLCO’S POV for the Economy and Real Estate

Current status and near-term outlook (as of June 2020)

While the reopening of the U.S. economy that began in May continues to progress, the lack of effective therapies and/or broad testing makes consumers cautious and keeps the economy from becoming fully engaged for the balance of 2020 and into the beginning of 2021. This underpins the uncertainty about the outlook. The RCLCO base case assumes that the U.S. economy returns to 2019 GDP levels by Q4 2021, or Q1 2022.

- There is still a chance that effective therapies and/or testing could begin to resolve uncertainly associated with the coronavirus pandemic sooner, which would enable the economy to reach full reopening in the summer and into the fall of this year. Under this “Summer-V Curve” scenario, the U.S. economy could experience a strong second-half 2020 recovery and return to 2019 GDP levels by Q1 2021. However, based on what we know now, this has to be characterized as too optimistic and is unlikely.

- There is also a more pessimistic scenario that assumes that the COVID-19 outbreak lingers for much longer and/or has a severely disruptive second wave in the fall of 2020, which would likely result in a much deeper and prolonged economic downturn. Under this “Swoosh” scenario, 2019 GDP levels would not be regained until the end of 2021 or early 2022.

The impact of this economic downturn is being felt in the real estate industry to varying degrees depending upon the sector. Rental apartments are expected to fare well, although this sector is still likely to experience downward pressure on rents and occupancies until the economy returns to growth in the private sector. The greatest disruption in multifamily however is in Class-B and market-rate Class-C properties; rent collections have held up extremely well in Class-A projects.

A key question that is on many professionals’ minds is: will things come unglued as soon as the enhanced unemployment benefits drop out and other supports fall away? The answer will be different between various types of real estate.

Class-C apartments, and to a lesser extent, Class-B apartments are home to a large number of people who are using some of the supplementary unemployment money to cover their rent. This crisis is worsening the disparity among economic groups in this country, and as a consequence the working-class apartment market-rate developments are the ones that face the most serious risks in the second half of this year. Class-A apartments, by contrast, often house people who are “renters by choice,” a group that typically has some savings that can tide them over a downturn, and those high-end apartments will likely be well supported by demand from this group.

That said, if the fiscal stimulus gets reduced too quickly, many types of commercial real estate will suffer, along with incomes and the labor market. Presumably, the variation among responses in this survey reflects, among other factors, different expectations regarding the future of government relief programs.

Who Took the Survey?

RCLCO’s Market Sentiment Survey tracks the sentiments of a highly experienced pool of real estate professionals from across the country and across the industry. Approximately two-thirds (68%) of respondents have worked in the real estate industry for 20 years or more, and 85% of respondents are C-suite or senior executives in their organizations.

Years of Experience in Real Estate

Source: RCLCO

Position in Organization

Source: RCLCO

Developers and builders comprise the largest share of respondents, at 43% of the sample. Another 20% are investors or capital allocators, followed by 7% in design or architecture firms. The remaining 30% of respondents come from a variety of other types of organizations within the real estate industry and public sector.

Type of Organization

Source: RCLCO

The respondent mix is representative of the U.S. as a whole; however, it is weighted towards those who report working primarily in coastal and Sunbelt markets. This respondent mix reflects markets where there has been significant development activity in this cycle.

Primary Region/Market

Source: RCLCO

Article and research prepared by Charles A. Hewlett, Managing Director; Brad Hunter, Managing Director; and Grace Amoh, Analyst.

References

[1] The Real Estate Market Index (RMI) is based on a semiannual survey of real estate market participants and is designed to take the pulse of real estate market conditions from the perspective of real estate industry participants. The survey asks respondents to rate real estate market conditions at the present time compared with one year earlier (Current RMI), and expectations over the next 12 months (Future RMI). The RMI is a diffusion index calculated for each series by applying the formula “(Improving – Declining + 100)/2.” The indices are not seasonally adjusted. Based on this calculation, the RMI can range between 0 and 100. RMI values in the 60 to 70+ range are indicative of very good market conditions. Values below 30 are typically coincident with periods of economic and real estate market stress/recession.

Disclaimer: Reasonable efforts have been made to ensure that the data contained in this Advisory reflect accurate and timely information, and the data is believed to be reliable and comprehensive. The Advisory is based on estimates, assumptions, and other information developed by RCLCO from its independent research effort and general knowledge of the industry. This Advisory contains opinions that represent our view of reasonable expectations at this particular time, but our opinions are not offered as predictions or assurances that particular events will occur.

Related Articles

Speak to One of Our Real Estate Advisors Today

We take a strategic, data-driven approach to solving your real estate problems.

Contact Us